You Have the Right to Sue Your Debt Collector — Here's How

If you're trying to figure out how to sue a debt collector, here's the short answer:

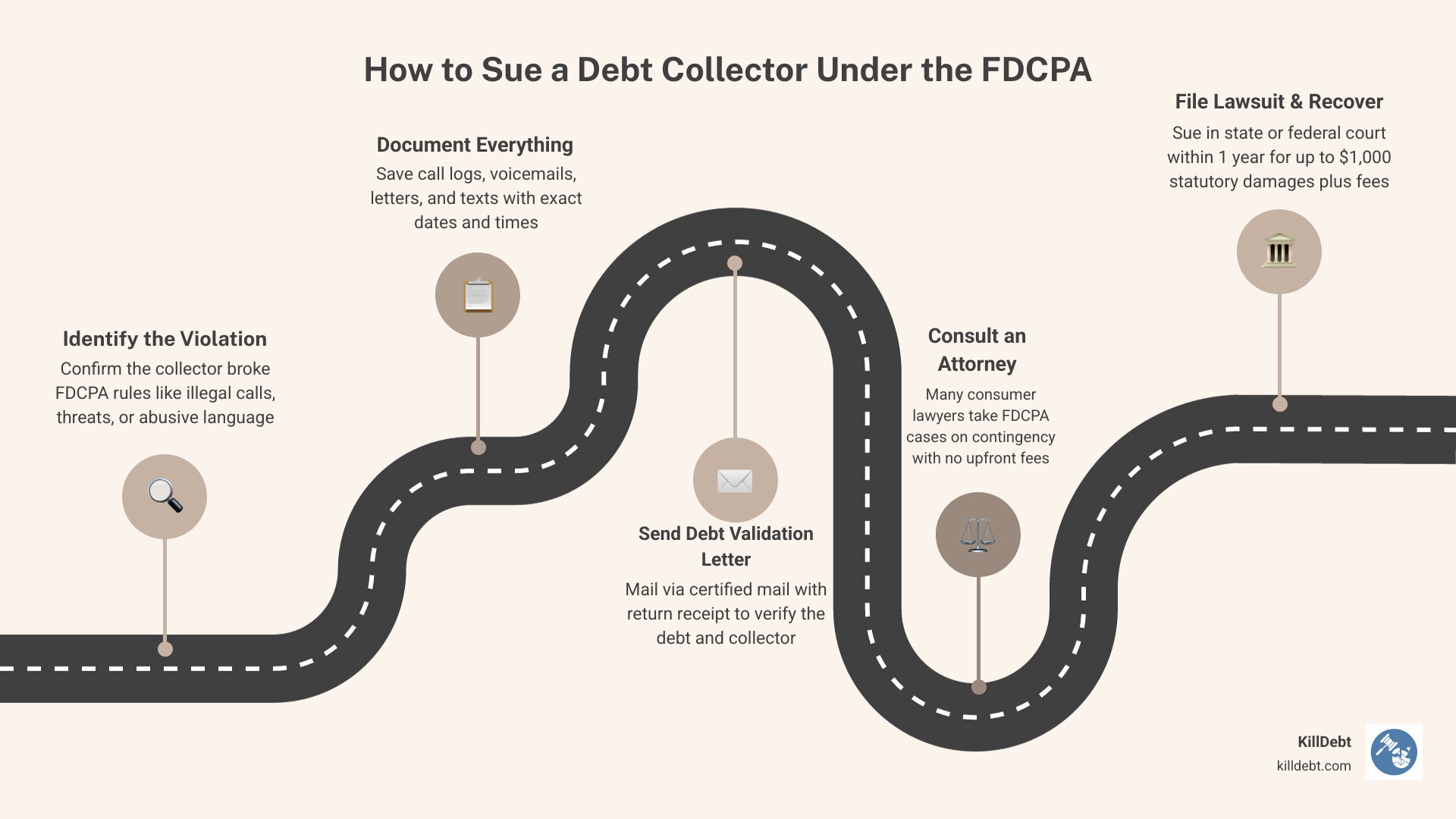

Identify the violation — confirm the collector broke a rule under the Fair Debt Collection Practices Act (FDCPA), such as calling at illegal hours, making threats, or using abusive language

Document everything — save call logs, voicemails, letters, and texts with dates and times

Send a debt validation letter — via certified mail with return receipt

Consult a consumer protection attorney — many take FDCPA cases on contingency (no upfront cost)

File your lawsuit — in state or federal court within one year of the violation

Recover damages — up to $1,000 in statutory damages, plus actual damages and attorney fees paid by the collector

Debt collectors count on you feeling too overwhelmed to fight back. But federal law is firmly on your side.

The FDCPA gives every consumer — even those who genuinely owe the debt — the right to sue collectors who break the rules. And the numbers show people are using it. Consumers filed over 12,000 FDCPA lawsuits in federal court in 2022 alone, a 9% jump from the year before. The CFPB received more than 82,700 debt collection complaints that same year.

Whether you just got a threatening phone call, received a court summons, or are staring down a wage garnishment threat, you have real legal options — and real money you can recover.

I'm Brian Parker, founder of KillDebt, and for over 30 years I've been in courtrooms across the country fighting debt collectors, debt buyers, and collection law firms — and I've used every tool the FDCPA offers to help consumers how to sue a debt collector and win. Below, I'll walk you through exactly what I've seen work.

Identifying FDCPA Violations: When You Can Sue

Before you can head to court, you need to know what constitutes a "winable" case. The Fair Debt Collection Practices Act (FDCPA) is a powerful federal shield that defines exactly what a collector can and cannot do. If you want to understand the full scope of your protection, start by checking out FDCPA Explained.

Many people ask, "Who exactly am I suing?" Generally, the FDCPA applies to third-party debt collectors and debt buyers—those who purchase "zombie" debts for pennies on the dollar. It usually doesn't apply to the original creditor (like the bank that gave you the credit card), but once they hand it off to a collection agency, the rules change. You can find a deeper dive into this in What Is a Debt Collector Under the FDCPA: Your Rights Explained.

According to Debt Collection FAQs | Consumer Advice, the law covers personal, family, and household debts, including credit cards, medical bills, student loans, and mortgages.

How to sue debt collector for harassment

Harassment isn't just a "feeling"—it's a legal violation. If a collector is calling you repeatedly with the intent to annoy or abuse, they are breaking the law. Specifically, the CFPB notes that calling more than seven times within a seven-day period is a major red flag.

Common harassment tactics include:

Illegal threats: Threatening to have you arrested, claiming they will take your furniture, or threatening wage garnishment without first winning a court judgment.

Obscene language: Using profanity or derogatory slurs during calls.

Workplace calls: Continuing to call your place of employment after you've told them (or they have reason to know) that your employer prohibits such calls.

If you’re dealing with this right now, our guide on Debt Collector Harassment Stop provides immediate tactics to shut them down.

Prohibited disclosure and contact methods

Collectors often try to "shame" consumers into paying by involving others. This is a massive FDCPA violation. A collector cannot:

Contact third parties: They can generally only contact other people (like neighbors or family) once to find out your address or phone number. They cannot tell your boss or your sister that you owe money.

Abuse social media: They cannot send you private messages if you’ve asked them to stop, and they certainly cannot post about your debt on your public wall.

Violate time restrictions: Calls must happen between 8:00 a.m. and 9:00 p.m. in your time zone.

If they call you at 6:00 a.m. or midnight, they’ve just handed you a reason to sue. For a step-by-step response to these calls, see What to Do When a Debt Collector Calls: Your Complete Action Plan.

How to Sue Debt Collector: A Step-by-Step Legal Roadmap

Knowing how to sue a debt collector requires a bit of organization. You aren't just telling a story to a judge; you are presenting evidence of a statutory violation. According to How to Sue a Debt Collector for Harassment - Consumer Attorneys, the strongest cases are built on a solid paper trail. If you're ready to escalate, you should also know How to Report a Collection Agency to the FTC and CFPB to create an official record of the abuse.

How to sue debt collector in federal vs. state court

You have the option to file in either state or federal court.

Federal Court: This is often the preferred route for FDCPA claims. Federal judges are very familiar with the FDCPA, and these courts offer "fee-shifting." This means if you win, the collector has to pay your attorney’s fees.

State/Small Claims Court: This might be faster for simple cases, but you may not get the same level of expertise regarding federal consumer laws.

Many consumers wonder, "Do I Need a Lawyer for a Debt Collection Lawsuit?" While you can represent yourself (pro se), having an expert can significantly increase your payout, especially since the collector usually ends up picking up the tab for your legal help.

Building your case with documentation

Your "evidence locker" should include:

Call Logs: Every call date, time, and a summary of what was said.

Recorded Messages: Save every voicemail. They are "smoking gun" evidence.

Letters and Envelopes: Keep everything, including the envelopes (the postmark date matters!).

Validation Requests: One of your most powerful moves is sending a Debt Validation Letter within 30 days of the first contact. If the collector continues to harrass you without providing proof, they are in violation. Use our resources like Debt Validation Letters: Your First Line of Defense Against Collectors and Letter of Debt Validation to get this right.

Damages and Compensation: What You Can Recover

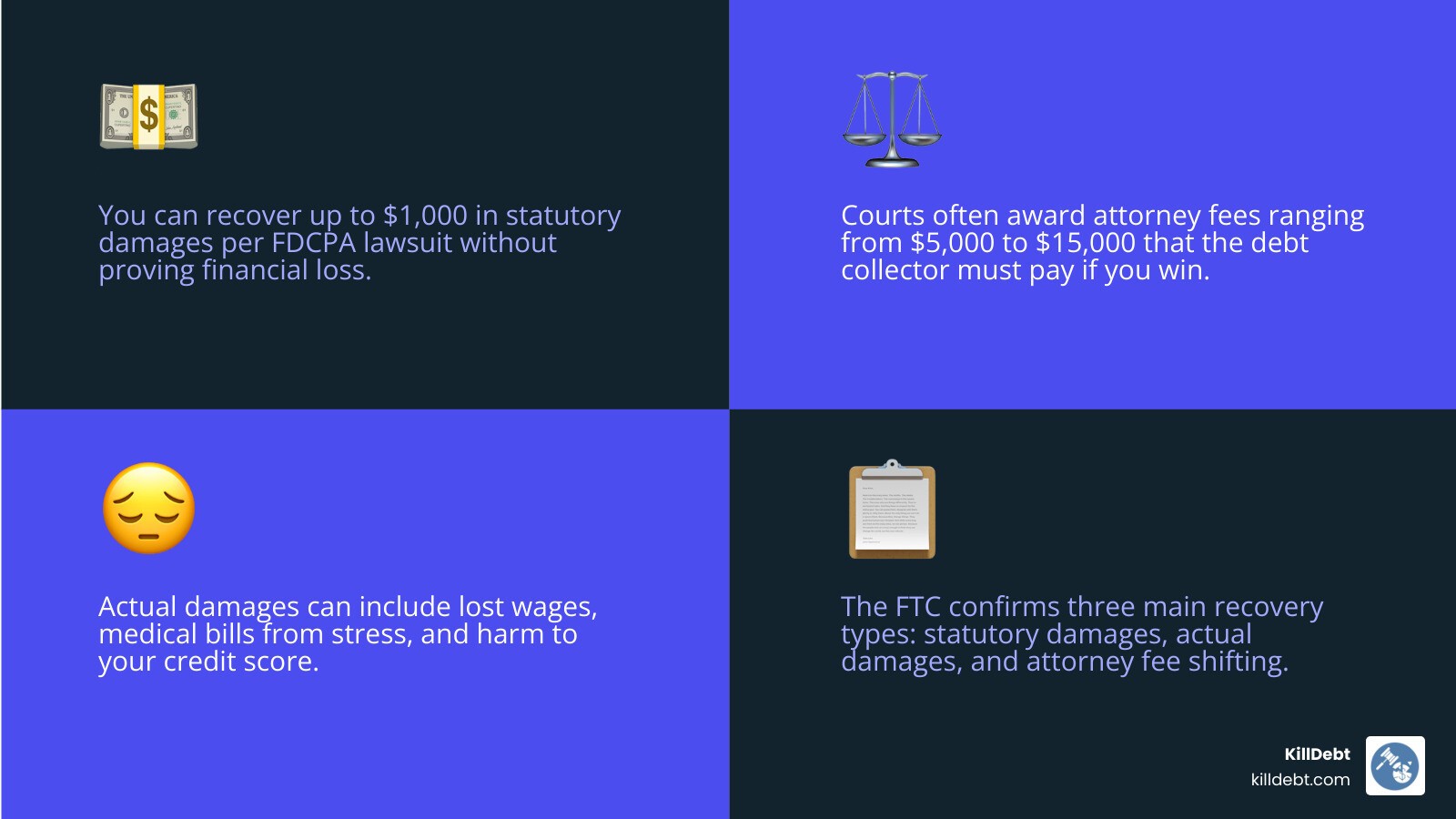

When you sue, you aren't just looking for an apology. You are looking for financial compensation. According to Debt Collection FAQs - FTC Consumer Advice, there are three main types of recovery.

Statutory damages and attorney fees

Under the FDCPA, you can be awarded up to $1,000 in statutory damages per lawsuit. The best part? You don't have to prove you lost money to get this. The mere fact that the collector broke the law is enough. Additionally, the "fee-shifting" provision is vital—it ensures that even if your case is "only" worth $1,000, an attorney can still take the case because the collector will pay their $5,000–$15,000 in fees. If you're feeling the pressure, read more about Struggling with Debt Collectors.

Actual damages for financial and emotional harm

If the collector's behavior caused you real-world harm, you can sue for "actual damages." This includes:

Lost Wages: If you were fired because of illegal calls to your boss.

Medical Bills: If the stress led to physical illness, anxiety, or the need for therapy.

Bank Fees: If they illegally froze your account. You can learn more about how they try to do this at Can Debt Collectors Take My Wages and Bank Account.

Defending Yourself When the Collector Sues You First

Sometimes, the best defense is a good offense. If a collector sues you, you can often "counter-sue" within the same case for FDCPA violations. As What To Do if a Debt Collector Sues You | Consumer Advice points out, the worst thing you can do is ignore the summons. Between 70% and 90% of consumers lose by default because they don't show up. If you've been served, you need to act fast—see Sued for a Debt? Here's Exactly What to Do in the First 7 Days.

Responding to a summons and complaint

You must file a written "Answer" with the court. This isn't just a letter; it's a formal legal document where you admit or deny their claims. You should also include "affirmative defenses"—reasons why they shouldn't win even if the debt is yours. We provide a How to Answer a Debt Summons guide and a Sample Answer to Debt Collection Lawsuit to help you through this.

Challenging time-barred debts and ownership

Many debt buyers sue on "zombie debt"—debts that are past the statute of limitations. In Florida and Michigan, once a debt is "time-barred," they cannot legally sue you for it. Furthermore, they must prove they actually own the debt. If they can't show a clear "chain of title," the case should be dismissed. Learn how to beat these at How to Win Zombie Lawsuit and understand the Chain of Assignment Debt Collector.

State-Specific Protections and Statutes of Limitations

While the FDCPA is federal, state laws often provide extra layers of protection. KillDebt focuses specifically on Florida and Michigan, where we have deep roots and specific expertise.

Navigating Maryland and Florida collection laws

Note: While Maryland has strong laws, we focus our primary defense tools on Florida and Michigan residents. In Florida, the Florida Consumer Collection Practices Act (FCCPA) is even stronger than the federal FDCPA in some ways. For example, it can apply to original creditors, not just third-party collectors. If you're in the Sunshine State, check out How to Protect Yourself: Debt Collections | My Florida Legal and be aware of the rules for About Small Claims Collection Lawsuits - The Florida Bar.

Michigan debt defense strategies

In Michigan, the statute of limitations for most contract debts is six years. Michigan courts have very specific local rules about how evidence must be presented. If you're a Michigander, you'll want to review Michigan Debt Collections Attorney: Stop Debt Collectors! and Michigan Court Debt Cases to understand the local landscape. For those in neighboring areas, the Illinois Debt Collection Statute also provides a good comparison of regional rights.

Conclusion

Suing a debt collector doesn't have to be a sweat-inducing nightmare. With the right tools and a clear understanding of your rights, you can turn the tables on abusive agencies. At KillDebt, we've revolutionized this process with ParkerGPT, our AI legal defense system. Trained on over 30 years of my personal trial experience, ParkerGPT analyzes your specific lawsuit documents and helps you draft court-ready responses that identify the collector's weakest points.

We’ve also just launched Court Tester, an AI courtroom simulation. You can upload your actual filings and "practice" your motion in front of an AI judge before you ever step foot in a real courthouse. Don't let debt collectors bully you into silence. Whether you're in Florida or Michigan, we're here to help you fight back.

Ready to take the next step? Check out our Fight Debt Collection Lawsuit Complete Guide or Take Control of Your Case Today by letting ParkerGPT build your defense.

Frequently Asked Questions (FAQ)

What is the statute of limitations for filing an FDCPA lawsuit?

You have exactly one year from the date the violation occurred to file your lawsuit. This is a "hard" deadline. If they harassed you on May 1st, 2025, you must file by May 1st, 2026. This is why documentation is so vital—you need to prove when the clock started.

Can I sue a debt collector if the debt is actually mine?

Yes. This is the biggest misconception in debt law. The FDCPA regulates the behavior of the collector, not the validity of the debt. Even if you owe every penny, a collector is not allowed to lie to you, threaten you, or call you at 3:00 a.m. If they break the rules, you can sue them and potentially use the settlement to wipe out the debt you owe.

How do I report a debt collector to federal authorities?

You can file a complaint online with the FTC or the CFPB. While these agencies don't usually represent you individually, your complaint goes into a database that helps them identify "bad actors" for major enforcement actions. To see how to turn a complaint into a defense, read our Fight Debt Collection Lawsuit Complete Guide.