By Brian Parker | Updated October 2025 | Read time:

This is one of the most terrifying questions I hear from people facing debt collection lawsuits: "Can they really take my paycheck and empty my bank account?" The short answer is yes - but only after they jump through specific legal hoops, and you have far more protection than most people realize. After 30+ years defending consumers, I can tell you that understanding your rights and protections is the difference between financial devastation and maintaining control of your assets.

Let me explain exactly what debt collectors can and cannot do, the legal process they must follow, and most importantly, how you can protect yourself before and after they obtain a judgment.

---

The Reality of Post-Judgment Collection Powers

What Happens After Default Judgment

Here's what the debt collection industry doesn't advertise: Once they obtain a judgment against you (which happens to over 70% of people who don't respond to lawsuits), they gain powerful legal tools that can devastate your finances for years.

The devastating effects of default judgment include:

Wage garnishment: Legal seizure of up to 25% of your paycheck

Bank account seizure: Freezing and draining your checking and savings accounts

Property liens: Claims against your real estate and other assets

Asset hearings: Court-ordered financial examinations under oath

From recent industry analysis: Debt collection lawsuits have surged 120% since 2019, with companies like LVNV Funding tripling their filings in 2024. They're using AI-powered filing systems to flood courts with cases, counting on the 70% default rate to obtain automatic judgments.

The Legal Authority Behind Collection Actions

Judgments create enforceable legal rights that didn't exist when you simply owed money. Before judgment, debt collectors can call and send letters. After judgment, they can:

Garnish wages directly from your employer

Freeze bank accounts without advance warning

Place liens on real property

Force you to appear for asset examination hearings

Seize non-exempt personal property

The timeline is typically swift: Once they have a judgment, garnishment paperwork can be filed within weeks, and bank account seizures can happen without any advance notice to you.

Through my work with KillDebt.ai, I've systematized defense strategies that prevent judgments in the first place - because once they have that judgment, your options become much more limited and expensive.

---

Federal Wage Garnishment Protections

The Federal Minimum Standards

The Consumer Credit Protection Act (15 U.S.C. §1673) establishes baseline protections that apply in all 50 states:

Federal garnishment limits:

25% maximum: They cannot take more than 25% of your disposable earnings

Poverty protection: They cannot reduce your take-home pay below 30 times the federal minimum wage per week

Whichever is less rule: You get the protection that leaves you with more money

Disposable earnings calculation: This means your gross pay minus legally required deductions (federal/state taxes, Social Security, unemployment insurance, and court-ordered child support).

What's Protected at the Federal Level

Completely exempt federal benefits:

Social Security retirement, disability, and survivor benefits

Supplemental Security Income (SSI)

Veterans' benefits and disability payments

Railroad retirement benefits

Federal employee retirement benefits

Unemployment compensation

These benefits remain protected even after being deposited in bank accounts - but you must prove the source to claim the exemption.

---

State-by-State Wage Protection Variations

States with Enhanced Protection

Some states provide significantly better protection than federal minimums:

Wisconsin Protects wages down to the poverty level and provides $5,000 in bank account protection beyond federal benefits.

Texas: No wage garnishment for consumer debts (except child support, taxes, and student loans). One of the most debtor-friendly states.

Pennsylvania: Limited wage garnishment - only allows garnishment of amounts over poverty guidelines.

North Carolina: Prohibits wage garnishment for consumer debts entirely (similar to Texas).

States with Minimal Protection

Other states provide only federal minimum protections:

Michigan: Provides minimal protections beyond federal requirements, leading to common and aggressive wage garnishment.

Florida: Follows federal minimums with some head-of-household protections.

New York: Standard federal protections with some enhanced exemptions for certain income types.

Garnishment protection varies dramatically by state. Some jurisdictions like Wisconsin, protect wages down to the poverty level and provide substantial bank account protection, while others like Michigan, provide minimal protections beyond federal minimums. Research your specific state's garnishment exemption laws and procedures.

---

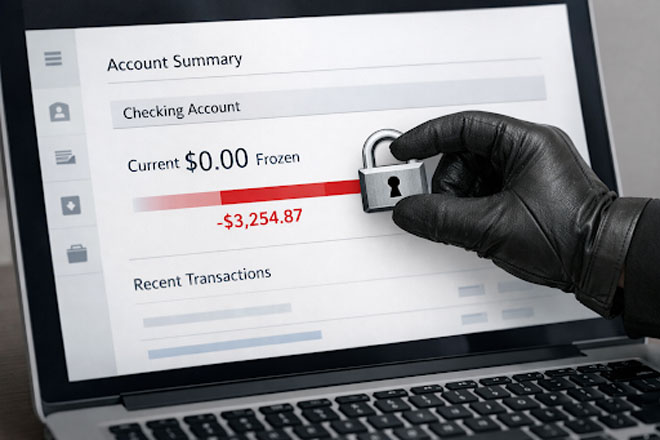

Bank Account Seizure: The Shocking Reality

How Bank Account Garnishment Works

Bank account seizure is often more devastating than wage garnishment because it happens without warning and can drain your entire account instantly.

The typical process:

Debt collector obtains judgment against you

They serve garnishment papers on your bank

Bank immediately freezes your account

You discover the freeze when your debit card is declined or checks bounce

Bank holds the money for a legal waiting period (typically 10-30 days)

Money is then transferred to the debt collector unless you file exemption claims

What Makes Bank Seizures So Devastating

Unlike wage garnishment, which is ongoing but predictable, bank seizures are:

Immediate and total: They can take everything in the account up to the judgment amount

Without advance warning: You typically discover it when trying to access your money

Cause cascading problems: Bounced checks, overdraft fees, utility shutoffs, missed rent payments

From my recent video analysis: I've documented cases where debt collectors use asset hearings (credit examinations) to force consumers to reveal all bank accounts and financial information under oath. These hearings give them roadmaps for future seizures.

Federal Benefit Protection in Bank Accounts

Federal benefits remain protected even in bank accounts, but you must prove the source:

Protected deposits:

Social Security payments (identifiable by direct deposit codes)

Veterans' benefits

Federal retirement benefits

Unemployment compensation

The burden of proof is on you to demonstrate that seized funds come from protected sources. This requires documentation and often legal proceedings to recover frozen benefits.

State Procedure Variations: While federal benefits remain protected nationwide, the procedures for claiming these exemptions and recovering seized benefit funds vary significantly from state to state. Some jurisdictions provide streamlined processes for federal benefit protection, while others require extensive documentation and court proceedings.

---

Asset Hearings: The Financial Inquisition

What Are Creditor Examinations?

Asset hearings (also called creditor examinations or judgment debtor exams) are court-ordered proceedings where you must appear and answer questions about your finances under oath.

What they can demand:

All bank account information, including account numbers and balances

Employment detail,s including salary and benefit information

Real estate ownership and property values

Personal property, including vehicles, jewelry, and other assets

Investment accounts, including retirement funds and securities

Business interests and income sources

The Perjury Trap

Everything you say is under oath. If they later discover financial information you didn't disclose, they can pursue perjury charges against you. This creates enormous pressure to reveal everything, even information that might be protected.

The strategic problem: Asset hearings give debt collectors detailed roadmaps for future collection efforts. They learn where you bank, work, and keep assets - information they use for garnishments and seizures.

Avoiding Asset Hearings

The best strategy is to prevent judgments in the first place. Once they have a judgment, asset hearings become a powerful tool they can use repeatedly to monitor your financial situation.

Asset hearing procedures and requirements vary by state and local court rules. Some jurisdictions provide more protection for judgment debtors than others, including limitations on the frequency and scope of examinations.

Perjury Standards Vary: The consequences for incomplete disclosure during asset hearings differ significantly between jurisdictions. Some states have strict perjury enforcement for credit examinations, while others focus primarily on civil contempt. The burden of proof and penalties for alleged false statements vary substantially by court system and jurisdiction.

---

Property Liens and Real Estate Attachments

How Judgment Liens Work

Judgments can create liens against real property in most states, meaning they get paid when you sell or refinance your home.

Lien procedures:

Debt collector files judgment lien in county records

Lien attaches to any real property you own in that county

Lien amount includes judgment plus accrued interest and costs

Lien remains until paid or judgment expires (typically 10-20 years)

Homestead Exemptions

Most states provide homestead exemptions that protect some equity in your primary residence:

Generous homestead states:

Texas: Unlimited homestead exemption for primary residence

Florida: Unlimited homestead exemption with acreage limitations

Kansas: $60,000 homestead exemption

Limited homestead states:

Michigan: $45,000 homestead exemption

Wisconsin: $75,000 homestead exemption

California: $75,000-$175,000 depending on circumstances

The strategic importance: Homestead exemptions can protect your primary residence from forced sale, but liens can still attach to non-exempt equity.

---

Retirement Account and Investment Protections

ERISA-Protected Retirement Accounts

Federal law provides strong protection for qualified retirement accounts:

Fully protected accounts:

401(k) and 403(b) plans

Traditional and Roth IRAs (up to $1,362,800 in 2025) (federal bankruptcy exemption amount state court collection exemptions may differ)

Pension plans

SEP and SIMPLE IRAs

403(b) tax-sheltered annuities

These protections apply even after judgment and generally cannot be garnished for consumer debts.

Investment Account Vulnerabilities

Non-retirement investment accounts receive limited protection:

Regular brokerage accounts can be garnished

Mutual fund accounts outside retirement plans are vulnerable

Bank investment products (CDs, money markets) can be seized

Real estate investment properties can be attached with liens

---

The Strategic Timeline: Before vs. After Judgment

Before Judgment: Maximum Protection Opportunities

Your most powerful protection period is before they obtain judgment. During this phase:

You can challenge their right to sue using standing challenges, statute of limitations defenses, and documentation problems.

You can negotiate from a position of strength because they still face litigation costs and uncertain outcomes.

You can implement asset protection strategies while they're still legal and ethical.

You maintain leverage for favorable settlement terms.

After Judgment: Limited Protection Options

Once they have judgment, your options become reactive:

Exemption claims to protect specific assets

Payment plan negotiations to avoid garnishment

Bankruptcy consideration for automatic stay protection

Challenge improper collection methods under FDCPA

The key insight: Prevention through proper lawsuit defense is far more effective than post-judgment asset protection.

Jurisdiction-Specific Asset Protection: While federal law provides baseline protections, state asset protection strategies vary dramatically. Some states like Texas provide extensive debtor protections, while others offer minimal protection beyond federal requirements. Asset protection planning must be tailored to your specific state's laws and cannot rely on general strategies alone.

---

The KillDebt Protection Strategy

Why ParkerGPT Prevents Financial Devastation

After three decades of protecting consumers' assets, I created KillDebt.com and ParkerGPT to systematically prevent the judgments that lead to wage garnishment and bank account seizure. The recent surge in debt collection lawsuits - up 120% since 2019 - makes this protection more critical than ever.

ParkerGPT prevents asset seizure by:

Generating comprehensive lawsuit responses that challenge every element debt collectors must prove

Identifying FDCPA violations that create counterclaim leverage and settlement opportunities

Exposing documentation problems that debt buyers typically cannot overcome in court

Creating strategic settlement leverage before judgments are entered

Real Asset Protection Results

From my recent video analysis: A Virginia civil engineer named Carlos Bernol fought back when LVNV Funding sued him. He showed up in court, LVNV couldn't prove they owned the debt, and they dropped the case entirely. He then sued LVNV and Resurgent under FDCPA violations - turning defense into offense.

KillDebt Membership provides:

Immediate lawsuit response generation to prevent default judgments

Asset protection guidance specific to your state's exemption laws

Settlement negotiation strategies that resolve cases before judgment

FDCPA counterclaim development that creates offensive opportunities

Exemption claim guidance for post-judgment protection when necessary (procedures vary significantly by jurisdiction)

The economic reality: Preventing a $5,000 judgment saves years of potential garnishment. Even a $100/month wage garnishment costs $1,200 annually and can continue for decades with interest.

---

Your Asset Protection Action Plan

Phase 1: Immediate Response (If Being Sued)

[ ] Don't ignore the lawsuit - 70% of people default and face automatic asset seizure

[ ] Upload lawsuit to ParkerGPT for comprehensive response generation

[ ] Calculate exact response deadline using your state's specific rules

[ ] File proper response within 20-30 days to avoid default judgment

Phase 2: Strategic Defense Development

[ ] Challenge their standing to sue using chain of title problems

[ ] Identify FDCPA violations for counterclaim leverage

[ ] Demand complete documentation to expose authentication problems

[ ] Negotiate from strength using identified case weaknesses

Phase 3: Asset Protection Implementation

[ ] Research state exemption laws for wages, bank accounts, and property

[ ] Document protected income sources including federal benefits

[ ] Understand homestead exemptions and retirement account protections

[ ] Plan exemption claim procedures if post-judgment collection begins

Phase 4: Long-Term Financial Protection

[ ] Monitor credit reports for judgment entries and collection activities

[ ] Maintain exemption documentation for protected income and assets

[ ] Consider bankruptcy consultation if multiple judgments threaten financial stability

[ ] Stay informed about state law changes affecting exemptions and protections

---

Common Asset Protection Mistakes

Mistake #1: Ignoring the Lawsuit

Wrong approach: "I can't afford a lawyer, so I'll just ignore this"

Correct strategy: Use KillDebt.ai to generate proper responses and avoid default judgment

The math: A $5,000 default judgment can result in $20,000+ in garnishments over time with interest and costs.

Mistake #2: Assuming All Assets Are Vulnerable

Wrong assumption: "They can take everything I own"

Correct understanding: Federal and state laws provide significant exemptions for wages, benefits, retirement accounts, and homestead property

Mistake #3: Hiding Assets Improperly

Dangerous approach: Transferring assets to family members or hiding accounts

Legal strategy: Use legitimate exemption laws and proper asset protection planning

Mistake #4: Not Claiming Exemptions

Common error: Failing to file exemption claims when garnishment begins

Required action: You must actively claim exemptions - they're not automatic

Mistake #5: Post-Judgment Panic

Reactive mistake: Waiting until garnishment starts to seek help

Proactive approach: Prevent judgments through proper lawsuit defense

---

State-Specific Asset Protection Highlights

Texas: Maximum Debtor Protection

Wage garnishment: Prohibited for consumer debts (except child support, taxes, student loans)

Homestead exemption: Unlimited for primary residence

Personal property: Generous exemptions for household goods, vehicles, and tools of trade

Wisconsin: Enhanced Protection

Wage protection: Down to poverty level thresholds

Bank account protection: $5,000 exemption beyond federal benefits

Garnishment procedures: More debtor-friendly than most states

Florida: Homestead Haven

Unlimited homestead exemption with acreage restrictions

Head of household protection: Enhanced wage garnishment limits for primary wage earners

Personal property exemptions: Standard federal minimums

Michigan: Limited Protection

Federal minimums only for most wage and asset protection

Homestead exemption: $45,000 (relatively low)

Garnishment procedures: Creditor-friendly environment

Asset protection laws vary dramatically by state. Some provide extensive debtor protections while others offer minimal protection beyond federal requirements. Research your specific state's exemption laws before implementing protection strategies.

---

Federal vs. State Collection Law Framework

Federal Baseline Protections

The Fair Debt Collection Practices Act (FDCPA) provides uniform national standards for debt collector behavior but doesn't address garnishment limits beyond wage calculation standards.

Federal wage garnishment law sets minimum protections that states can enhance but not reduce.

Federal benefit protections apply nationwide regardless of state variations in other exemption laws.

State Enhancement Authority

States can provide greater protection than federal minimums through:

Enhanced wage exemption calculations

Higher homestead exemption amounts

Additional personal property protections

More restrictive garnishment procedures

Expanded definitions of exempt income

States cannot reduce federal protections or allow more aggressive collection than federal law permits.

---

The Psychology of Financial Fear vs. Legal Reality

Why Fear Paralyzes Action

The threat of wage garnishment and bank account seizure creates genuine terror for most people. This fear often prevents the very actions that could provide protection.

Common fear-based reactions:

"There's no point in fighting - they'll take everything anyway"

"I can't afford a lawyer, so I'm helpless"

"If I respond, I'll just make things worse"

"They must have a strong case or they wouldn't have sued"

The Legal Reality

Most debt collection cases have serious problems that prevent collectors from winning if properly challenged:

Standing issues: Many debt buyers cannot prove they own the debts they're suing on

Documentation problems: Missing contracts, incomplete account records, improper assignments

FDCPA violations: Improper venue, false statements, deceptive practices

Statute of limitations: Many debts are beyond the legal time limit for collection

The strategic advantage: When you understand your legal protections and respond properly, you shift from victim to strategic defendant with real leverage.

Why Asset Protection Requires Proactive Defense

The Judgment Prevention Strategy

Your strongest asset protection happens before judgment. Once they have a legal judgment, your options shift from offensive to defensive, and the advantage tilts heavily toward the debt collector.

Pre-judgment advantages:

Complete leverage for settlement negotiations

Constitutional due process protections require them to prove their case

FDCPA counterclaim opportunities that can eliminate debts entirely

Standing challenges that can result in case dismissals

Post-judgment limitations:

Burden shifts to you to prove exemptions and protections

Limited settlement leverage since they already have legal authority to collect

Ongoing collection authority for 10-20 years in most states

Asset examination power to discover all financial information

The KillDebt.com Advantage

ParkerGPT transforms asset protection from reactive to proactive by providing the tools to defeat debt collection lawsuits before they become judgments.

The systematic approach includes:

Immediate case analysis identifying winnable defense strategies

Federal and state law violation detection creating counterclaim opportunities

Standing challenges exposing debt buyer documentation problems

Settlement leverage development using identified case weaknesses

From the LVNV Funding example: Proper defense not only prevented judgment but created opportunities for FDCPA counterclaims against the debt collector. This transforms potential financial devastation into offensive legal action.

---

Next Steps in Your Asset Protection Journey

Understanding your rights is crucial, but taking action protects your assets. Your next learning priority should focus on:

What to Do When Sued by a Debt Collector: Complete First Steps Guide - Immediate action plan to prevent the judgments that lead to garnishment and seizure

Default Judgment Explained: Why 70% of People Lose Without Fighting - Understanding how automatic judgments create collection authority and how to avoid them [Coming Soon]

FDCPA Rights: What Debt Collectors Cannot Do to You - Federal protections that create counteroffensive opportunities against debt collectors [Coming Soon]

---

Related Defense Strategies - How to File an Answer to a Debt Collection Lawsuit: Step-by-Step Guide - Comprehensive response strategies that prevent judgment and protect your assets

Affirmative Defenses in Debt Cases: 15+ Defenses That Work - Legal strategies that defeat debt collectors before they gain collection authority [Coming Soon]

Settlement Negotiations: When and How to Negotiate with Debt Collectors - Strategic settlement approaches that resolve cases without judgment [Coming Soon]

Debt Collection Lawsuit Timeline: What Happens Next After You're Served - Understanding the complete process from lawsuit to potential asset collection [Coming Soon]

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have developed comprehensive strategies that protect assets by preventing the judgments that create garnishment authority. Through KillDebt.com, I've systematized these proven defense strategies to help more consumers understand their rights and take proactive action before facing wage garnishment, bank account seizure, and asset hearings. My approach recognizes that the best asset protection comes from aggressive legal defense that prevents judgments, rather than reactive measures after collection authority is established.

Frequently Asked Questions (FAQ)

Can a debt collector take my wages or bank account without suing me?

No. A debt collector cannot garnish wages or seize your bank account without first suing you and winning a court judgment. Collection calls and letters alone do not give them this power. Wage garnishment and bank account levies only become possible after a judgment is entered.

How much of my paycheck can be garnished if they get a judgment?

Under federal law, debt collectors can take up to 25% of your disposable earnings, or the amount that exceeds 30 times the federal minimum wage per week — whichever is less. Some states provide much stronger protections, and a few states prohibit wage garnishment for consumer debts entirely.

Can debt collectors freeze my bank account without warning?

Yes. Bank account garnishment often happens without advance notice. Once a judgment is obtained, a collector can serve papers directly on your bank, which may immediately freeze your account. You usually discover this when your debit card is declined or checks bounce. However, protected funds may still be exempt if you act quickly.

Are Social Security, disability, and veterans benefits protected?

Yes. Federal benefits like Social Security, SSI, VA benefits, and unemployment are protected from garnishment, even after they are deposited into a bank account. That said, you may need to prove the source of the funds and formally claim the exemption to have frozen money released.

What is the best way to prevent wage garnishment and bank seizures?

The most effective strategy is preventing a judgment in the first place. Responding properly to a debt collection lawsuit, challenging standing and documentation, and asserting valid defenses can stop collectors from ever gaining garnishment power. Once a judgment exists, your options become limited and reactive.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and extensive debt collection defense experience. This information is provided for educational purposes only and does not constitute legal advice for any specific situation.

Critical Multi-State Variations:

Wage garnishment protections: Range from no garnishment (Texas, North Carolina) to federal minimums only (Michigan, Florida)

Bank account exemptions: Vary dramatically from $200 (some states) to $5,000+ (Wisconsin) beyond federal benefits, with different claim procedures

Homestead exemptions: Range from $0-$30,000 to unlimited protection depending on state

Asset hearing procedures: Frequency, scope, and debtor protections vary significantly by jurisdiction

Personal property exemptions: Vehicle, household goods, and tools of trade protections differ substantially

Judgment collection periods: Range from 5-20 years with varying renewal procedures

Perjury enforcement: Standards and penalties for incomplete asset disclosure vary substantially between jurisdictions

State-Specific Legal Requirements:

Asset protection laws, exemption procedures, and garnishment rules vary significantly by state and local jurisdiction

Specific exemption claim procedures and deadlines differ substantially between jurisdictions

Some states provide extensive debtor protections while others offer minimal protection beyond federal requirements

Individual circumstances may require different asset protection strategies than those described

Professional Legal Advice Required: This content cannot replace personalized legal advice from a qualified attorney licensed in your jurisdiction. Before implementing asset protection strategies or facing collection activities, consult with a debt defense attorney familiar with the specific exemption laws and procedures in your state.

No Attorney-Client Relationship: Reading this content does not create an attorney-client relationship. For specific legal advice about protecting your assets from debt collection, co