When a Debt Collector Crosses the Line, You Have the Right to Fight Back

Knowing how to report a collection agency is one of the most powerful things you can do when a debt collector breaks the law.

Here's a quick answer if you need it now:

How to report a collection agency:

CFPB - File online at cfpb.gov/complaint (companies typically respond within 15 days)

FTC - Report at reportfraud.ftc.gov (especially for scams and fake collectors)

FDIC - Submit a complaint at ask.fdic.gov (for bank-related debt collection issues)

Your State Attorney General - Search "[your state] attorney general complaint" to find your state's form

Local agencies - NYC residents can call 311; Texas residents can call the OCCC at 800-538-1579

Debt collection problems are among the most common complaints received by the CFPB and the FDIC. That tells you something important: you are not alone, and this happens all the time.

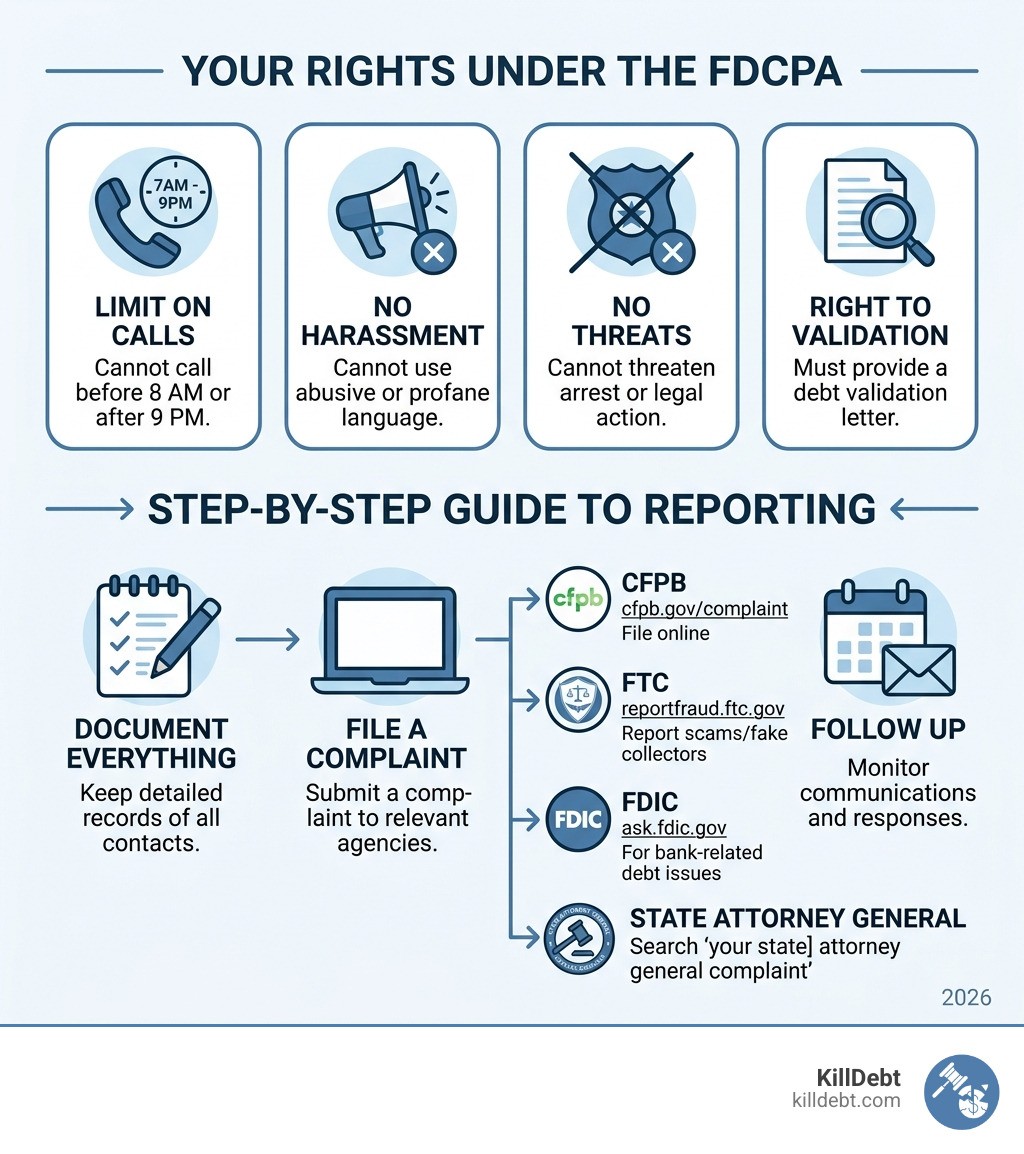

The law is on your side. The Fair Debt Collection Practices Act (FDCPA) makes it illegal for debt collectors to use abusive, unfair, or deceptive practices when they collect debts. Collectors cannot call before 8 AM or after 9 PM. They cannot threaten arrest or deportation. They cannot pretend to be attorneys or government officials.

But here's the hard truth: some collectors do all of those things anyway — because they're counting on you not knowing your rights.

If a collector has threatened you, lied to you, or called you at all hours, that's not just rude. It may be illegal — and you can report it.

Understanding Your Rights Under the FDCPA

The Fair Debt Collection Practices Act (FDCPA) is your primary shield. It is a federal law that dictates exactly what third-party debt collectors can and cannot do. It covers personal, family, and household debts—things like your credit card balances, auto loans, medical bills, and mortgages. It does not, however, cover debts you ran up for a business.

One of the most important things to realize is what is a debt collector under the FDCPA. Generally, it’s someone working for a collection agency or an attorney who regularly collects debts for others.

Under the FDCPA, collectors must follow strict communication rules:

The 8 AM to 9 PM Rule: They cannot call you before 8 in the morning or after 9 at night (in your time zone) unless you agree to it.

Workplace Calls: If you tell a collector (orally or in writing) that your employer doesn't allow personal calls at work, they must stop calling you there immediately.

Third-Party Disclosure: They generally cannot tell your neighbors, friends, or co-workers that you owe money. They can only contact third parties to find out where you live or work, and even then, they usually can only contact that person once.

If you’re feeling pressured, you have the right to know your rights and avoid scams. Legitimate collectors are required to send you a "validation notice" within five days of first contacting you. this notice must tell you how much money you owe, the name of the creditor, and what to do if you don't think you owe the money.

Identifying Illegal Tactics Worth Reporting

Not every annoying phone call is illegal, but many common tactics used by "bottom-feeder" agencies absolutely are. If you experience any of the following, it is time to look into how to report a collection agency.

Threats of Violence or Harm: Any threat to physically hurt you, your reputation, or your property is a massive violation.

False Statements: Collectors cannot lie about the amount you owe. They also cannot pretend to be an attorney or a government representative (like a police officer or an IRS agent).

Arrest and Deportation Threats: This is a favorite tactic of scammers. A debt collector cannot have you arrested or deported for a civil debt. If they say, "Pay now or the sheriff is coming to your door," they are breaking the law.

Abusive Language: They cannot use profanity, obscenities, or racial slurs to intimidate you.

If these tactics sound familiar, you need to learn how to make the debt collector harassment stop. Even if you truly owe the money, you do not deserve to be bullied. Furthermore, be on high alert for fake and abusive debt collectors who may be trying to collect on "phantom debts" that don't even exist.

How to report a collection agency for harassment

If you are being harassed, your best weapon is documentation. You shouldn't just get mad; you should get even by keeping a meticulous paper trail.

Keep a Call Log: Write down the date and time of every call. Note the name of the person you spoke to and exactly what they said.

Record the Calls: In many states, you can record phone calls. (Check your local laws first, or simply inform the collector: "I am recording this call for my records.")

Save Everything: Don't throw away envelopes, letters, or even those sticky notes they leave on your door.

Review Official Guidance: Check the Debt Collection FAQs to see if the specific behavior you're experiencing is explicitly listed as a violation.

Step-by-Step: How to Report a Collection Agency to Federal Authorities

When you're ready to take action, you have three main federal "big brothers" who want to hear from you.

Filing a complaint with the CFPB

The Consumer Financial Protection Bureau (CFPB) is arguably the most effective place to start. Each week, the CFPB sends more than 100,000 complaints to financial companies for a response.

The Process: You can submit a complaint online in about 10 minutes.

What to Include: Be clear and concise. Include dates, amounts, and the specific names of the people you spoke with.

The 50-Page Limit: You can attach up to 50 pages of supporting documents (like your call logs or letters).

What Happens Next: The CFPB forwards your complaint to the company. Most companies respond within 15 days. If they don't provide a final response within 60 days, the CFPB will follow up.

Public Database: With your permission, the CFPB may publish an anonymized version of your story in their public database to help warn other consumers. You can read other people's stories at the CFPB's complaint portal.

How to report a collection agency for scam activity

If the "collector" refuses to give you a mailing address, threatens you with immediate arrest, or demands payment via wire transfer or gift cards, you are likely dealing with a scammer.

In these cases, reporting to the FTC is crucial. You can visit reportfraud.ftc.gov to file a report. This helps the government track patterns and shut down large-scale fraud rings. You should also check our Reports section to see if the agency contacting you has a history of shady behavior.

If the debt involves a bank or a bank-regulated entity, you can also file a complaint with the FDIC. They provide specialized assistance for debt collection issues involving banks.

State-Specific Resources and Legal Recourse

While federal laws provide a baseline, many states have even tougher consumer protection laws.

Michigan Residents: If you are in the Great Lakes State, you can file a complaint with the Michigan Attorney General. Michigan has specific licensing requirements for collection agencies, and the state's Department of Licensing and Regulatory Affairs (LARA) keeps a close watch on them.

Florida Residents: If you're dealing with a "debt bully" in the Sunshine State, you can file a complaint with the Florida Attorney General. Florida law provides robust protections against consumer fraud and unfair trade practices.

Suing for FDCPA violations

Sometimes, filing a report with a government agency isn't enough to make you "whole." If a collector has caused you actual distress or financial loss, you have the right to sue them in state or federal court.

Under the FDCPA, if you win your case, you can be awarded:

Statutory Damages: Up to $1,000, even if you can't prove you lost money.

Actual Damages: Compensation for things like lost wages or medical bills caused by the stress of the harassment.

Attorney Fees: The collector may have to pay for your lawyer!

That you generally have only one year from the date of the violation to file a lawsuit. If you are struggling with debt collectors, consulting with a consumer law attorney or using a DIY legal tool can help you determine if a lawsuit is the right move.

Essential Actions Before You File a Report

Before you hit "submit" on that government complaint, make sure you've taken these defensive steps. They will make your report much stronger.

Demand Debt Validation: Within 30 days of that first phone call, send a Debt Validation Letter. This forces the collector to prove that the debt is yours and that they have the legal right to collect it. This is your first line of defense.

Send a "Cease Contact" Letter: If you just want them to stop calling, you can mail a letter telling them to stop all communication. Once they receive this, they can only contact you one more time to tell you they are stopping or to notify you that they are taking a specific legal action (like filing a lawsuit).

Use Certified Mail: Always send these letters via certified mail with a "return receipt requested." This gives you legal proof that the collector received your request.

Feature | Debt Validation | Debt Dispute |

|---|---|---|

Purpose | Forces collector to prove the debt is real | Tells collector you disagree with the debt |

Timing | Must be sent within 30 days of first notice | Can be sent anytime (but 30 days is best) |

Legal Effect | Collector must stop until they provide proof | Collector must mark the debt as "disputed" |

Best For | Finding out if the debt is a scam | Fixing errors on your credit report |

Conclusion: Take Control of Your Case Today

Reporting a collection agency is a vital step in protecting your peace of mind and your financial future. But sometimes, reporting isn't enough—especially if the agency decides to sue you.

That’s where we come in. At KillDebt, we believe that everyone deserves a fair fight in the courtroom, regardless of their bank account balance. Our platform is powered by ParkerGPT, an AI trained on the real-world strategies of attorney Brian Parker, who has over 30 years of experience fighting debt collectors.

We don't just give you generic advice. Our system analyzes your specific lawsuit documents, identifies the collector's weaknesses, and helps you generate court-ready responses. We’ve even introduced the Court Tester, an AI courtroom simulation where you can practice your motion in front of an AI judge before you ever step foot in a real courthouse.

Don't let the bullies win. Whether you need to send a validation letter or defend yourself against a billion-dollar collection firm, we have the tools to help you stand your ground.

Ready to fight back? Start your defense today at KillDebt.com and show them you aren't an easy target.

Frequently Asked Questions (FAQ)

Can I stop a debt collector from contacting me?

Yes! Under the FDCPA, you have the absolute right to tell a collector to stop contacting you. You must do this in writing. Once they get your letter, they are legally barred from calling or writing you again, except for very specific legal notifications. This doesn't make the debt go away—they can still sue you—but it does stop the phone from ringing. For more details on this process, visit the CFPB's guide on stopping contact.

What happens after I submit a complaint to the CFPB?

After you submit your complaint, it is assigned a case number. The CFPB forwards it to the company, which usually has 15 days to respond. You can log into the CFPB portal to track the status. Once the company responds, you have 60 days to review their answer and provide feedback. If the company's response is unsatisfactory, the CFPB uses that information to inform their enforcement and supervision work.

How do I identify a fake debt collector?

Scammers often use high-pressure tactics that legitimate agencies avoid. Look for these red flags: • They refuse to give you their physical address or a callback number. • They ask for payment via "untraceable" methods like gift cards or wire transfers. • They threaten you with "jail time" or "police intervention" for a credit card bill. • The debt is something you don't recognize at all. Always refer to the FTC's guide on fake collectors if you suspect a scam.