You Have the Legal Right to Make Debt Collectors Stop Contacting You

Sending a cease and desist creditor letter is one of the fastest, most powerful moves you can make to stop debt collector harassment — and it costs less than a cup of coffee.

Here's the quick answer:

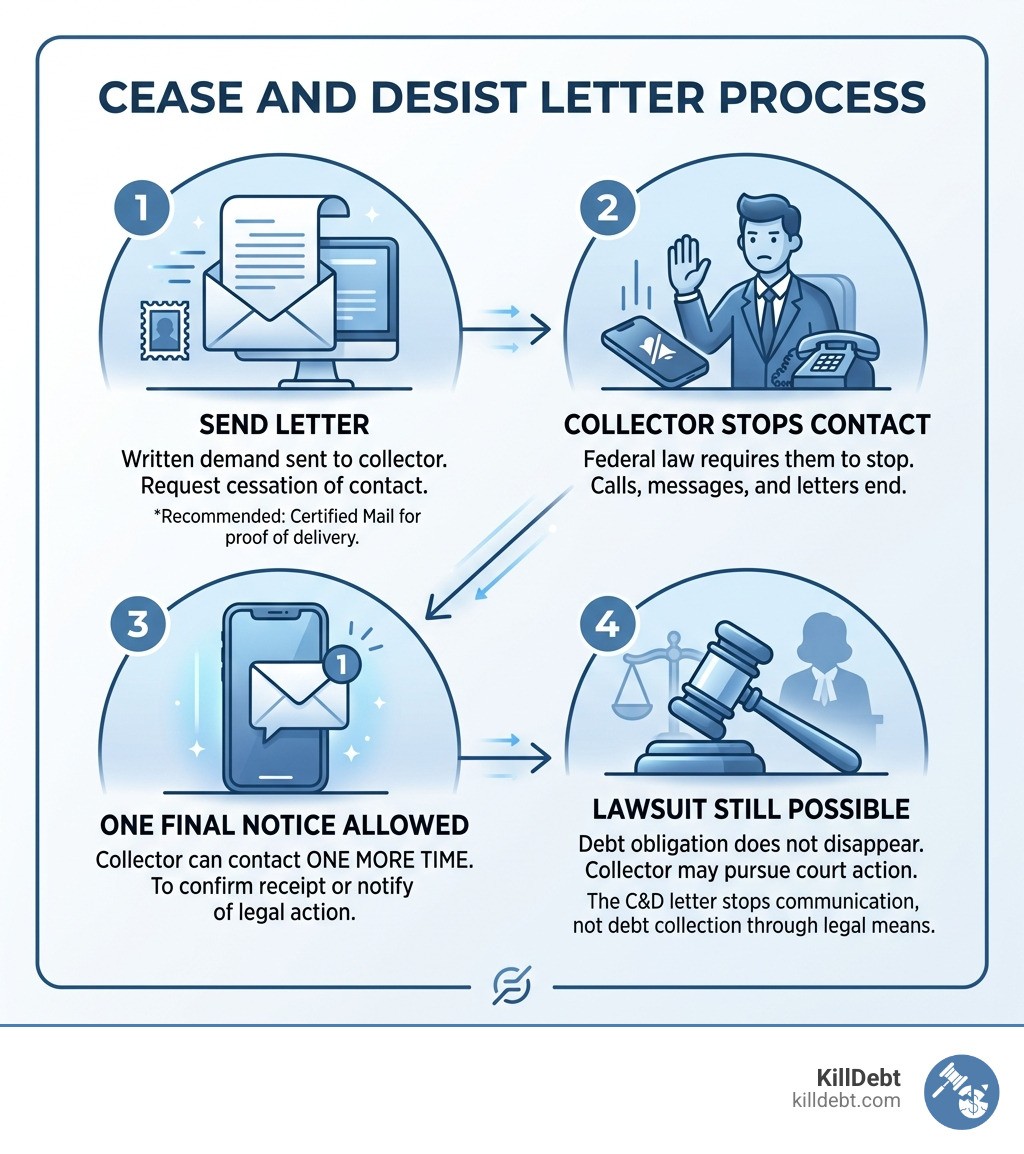

A cease and desist letter is a written demand telling a debt collector to stop contacting you

Federal law (the FDCPA, 15 U.S.C. § 1692c(c)) requires third-party collectors to honor it

Once they receive it, they can only contact you one more time — to confirm they're stopping or to notify you of a specific legal action

It does not erase the debt, but it does stop the calls, texts, and letters

Send it via USPS Certified Mail with Return Receipt Requested to create legal proof of delivery

If you're getting calls at work, late at night, or multiple times a day, you are not powerless. The law is on your side — you just need to use it.

Debt collectors count on you not knowing your rights. A single, well-written letter can stop the harassment cold and put you in a much stronger legal position if things escalate.

I'm Brian Parker, and for over 30 years I've fought creditors, debt buyers, and collection law firms in courtrooms across the country — I've used the cease and desist creditor letter as a frontline tool to protect thousands of consumers from relentless harassment. At KillDebt, I've built everything I know into tools and guides so you can do the same, without needing to hire an expensive attorney.

What is a Cease and Desist Creditor Letter?

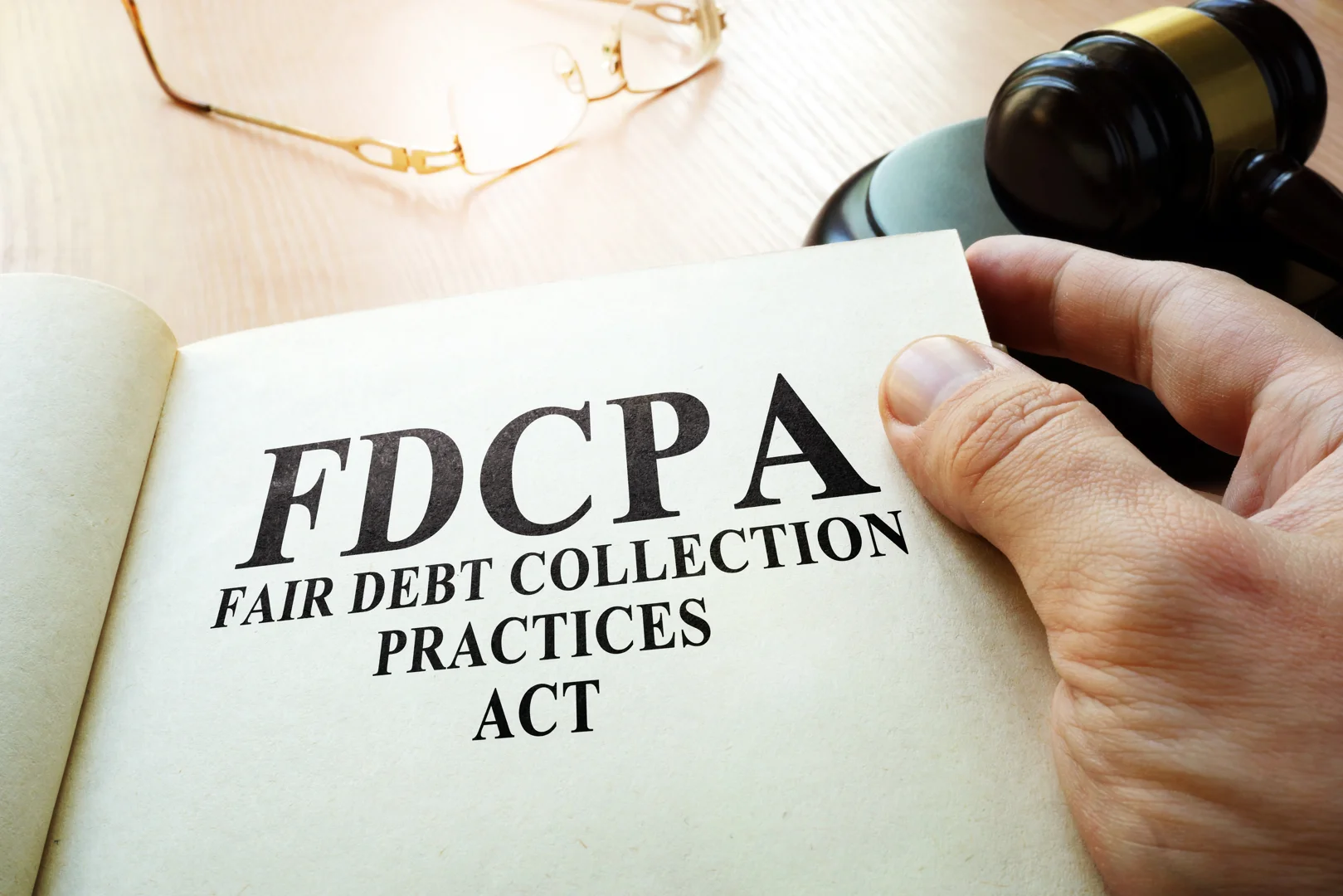

A cease and desist creditor letter is your formal "no-contact" order. It is backed by federal law, specifically the Fair Debt Collection Practices Act (FDCPA), codified at 15 U.S.C. § 1692c(c). This statute is very clear: if a consumer notifies a debt collector in writing that they refuse to pay a debt or that they wish the debt collector to cease further communication, the collector must stop.

Think of it as a legal communication ban. When we help people at KillDebt, we emphasize that this is a procedural right. You don't need a judge to sign off on it. You don't need a lawyer to draft it. You just need to put your demand in writing and send it to the right person.

It is important to understand the landscape of debt law to use this tool effectively. You can learn more about how these laws work in our guide on fdcpa explained. This law was designed to protect you from the psychological warfare debt collectors often use to pressure you into paying money you might not even owe. For a deeper dive into who these people are, check out what is a debt collector under the fdcpa your rights explained.

Who Must Honor Your Cease and Desist Creditor Letter?

Not every company that sends you a bill is legally required to stop calling just because you ask. The FDCPA primarily applies to third-party debt collectors. This includes:

Debt Buyers: Companies that buy "charged-off" debt for pennies on the dollar and try to collect the full amount.

Collection Agencies: Firms hired by a creditor to collect on their behalf.

Collection Attorneys: Law firms that handle more than two debt cases a year are generally bound by these rules.

However, there is a catch. Original creditors — like the credit card company or bank you originally signed the contract with — are generally not covered by the federal FDCPA's cease and desist requirements. They are often governed by different state-level consumer protection acts. In Florida and Michigan, where we focus our efforts, the rules can be nuanced. While the federal cease-and-desist right is specific to third-party collectors, original creditors still cannot harass you. If you are dealing with a bank directly, you might use a Sample Cease Communications Letter To Creditor to request they stop, though their legal obligation to comply is different than a collection agency's.

Legal Protections Under Regulation F

As of May 2026, we are operating under "Regulation F," which gave the FDCPA more "teeth." One of the biggest wins for consumers is the 7-in-7 rule. Under this rule, a debt collector is presumed to be harassing you if they:

Call you more than seven times...

Within a seven-day period...

Regarding a specific debt.

Furthermore, once they actually speak to you on the phone, they have to wait another seven days before calling you again about that debt. Regulation F also covers digital communications like emails and texts. If a collector ignores your cease and desist creditor letter and continues to blow up your phone, they are likely racking up violations that could lead to you getting paid. You can read more about stopping this behavior at Debt Collector Harassment Stop.

When and How to Send Your Letter

Knowing when to send the letter is just as important as knowing how. If a collector is calling you at your place of employment after you've told them your boss doesn't allow it, or if they are calling you at 10:00 PM, they are already breaking the law.

You should send a cease and desist creditor letter when:

The harassment is affecting your mental health or job performance.

You don't recognize the debt and want to stop the calls while you investigate.

The debt is "zombie debt" (past the statute of limitations).

You are prepared for the possibility that the collector might sue you (more on that later).

For a specific breakdown of the letter itself, visit our page on the cease debt collection letter.

Step-by-Step Guide to Mailing a Cease and Desist Creditor Letter

If you send your letter via regular mail, the debt collector will likely "lose" it in the shredder. To make this stick, you must create a paper trail.

Draft the Letter: Keep it simple. You don't need to tell your life story or explain why you can't pay.

Use Certified Mail: Go to the Post Office and ask for Certified Mail with Return Receipt Requested.

Keep the "Green Card": The return receipt (the green card) will be mailed back to you once the collector signs for the letter. This is your "smoking gun" evidence in court.

Create an Evidence Package: Staple your copy of the letter, the postal receipt, and eventually the green card together. If they call you even once after that green card is signed (outside of the one allowed exception), they owe you money.

For more tips on drafting these, you can look at resources like Write a Cease & Desist Letter That STOPS Debt Collector ... - Upsolve.

Essential Elements to Include in the Template

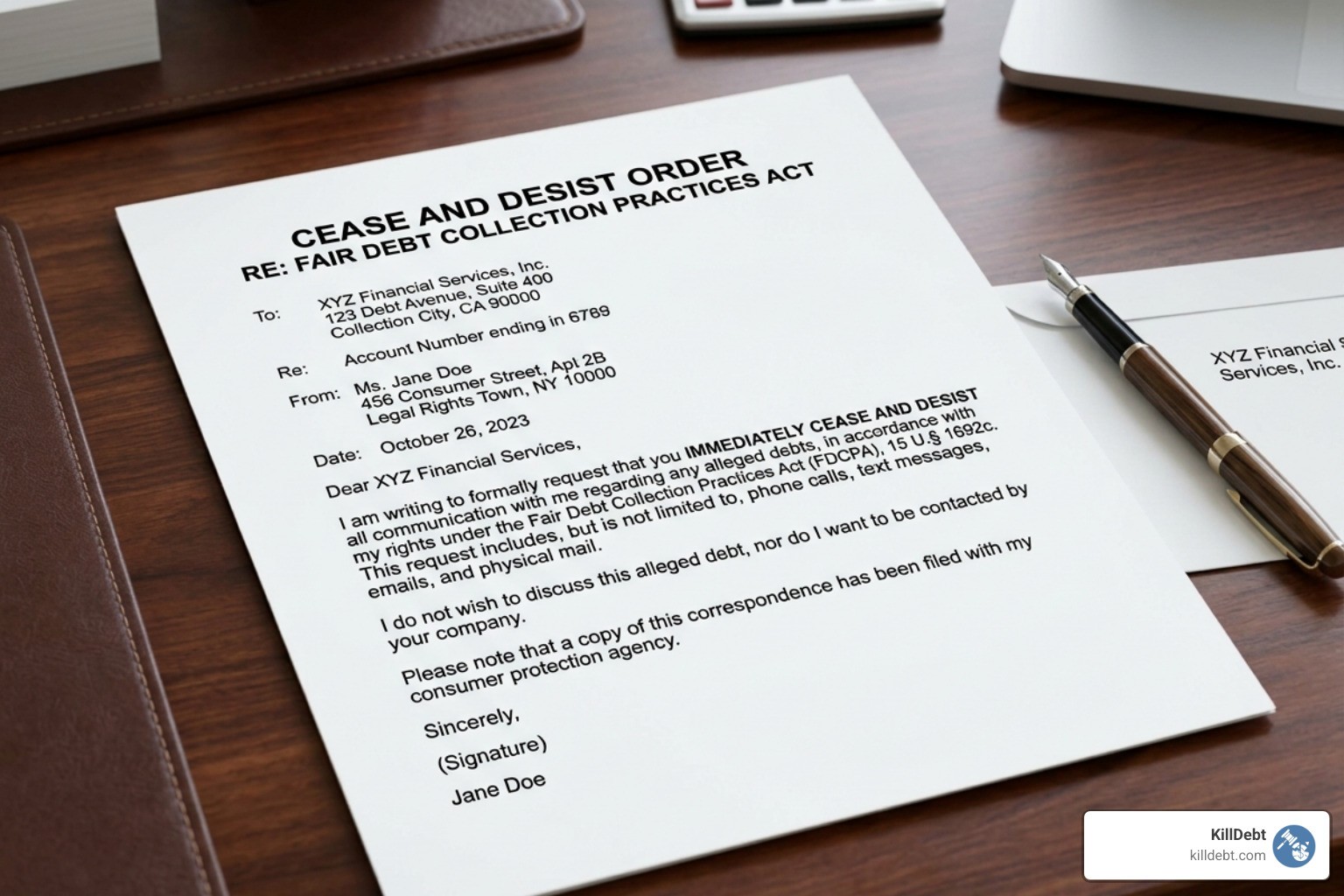

Your cease and desist creditor letter should be professional and assertive. Do not be rude; just be firm. Essential elements include:

Your Information: Name and address.

Collector Information: Their full name and mailing address.

Account Details: Use the account or reference number they provided.

The "Alleged Debt" Phrase: Never call it "my debt." Always refer to it as "the alleged debt" or "the debt referenced above." This prevents you from accidentally admitting you owe it.

Statutory Citations: Mention 15 U.S.C. § 1692c. It lets them know you aren't an easy target.

The Demand: Clearly state: "I am exercising my rights under the FDCPA to demand that you cease all communication with me regarding this alleged debt."

Workplace Ban: Explicitly state if your employer prohibits personal calls at work.

We often recommend combining this with a letter of debt validation if you are within the first 30 days of contact.

Strategic Risks: Does This Stop a Lawsuit?

This is the most important part of the guide. A cease and desist letter is NOT a "Get Out of Debt Free" card.

In fact, sending this letter is often called the "nuclear option." Why? Because if a collector is legally barred from calling or writing to you, they only have one tool left in their toolbox: suing you.

Feature | Cease and Desist Letter | Debt Collection Lawsuit |

|---|---|---|

Stops Phone Calls | Yes | No (but usually transitions to legal service) |

Erases the Debt | No | No |

Forces Proof | No | Yes |

Risk Level | Low (stops harassment) | High (can lead to garnishment) |

If you send a cease and desist creditor letter for a valid, large debt that is still within the statute of limitations in Florida or Michigan, you might actually accelerate a lawsuit. The collector realizes they can't talk you into paying, so they hand the file to a lawyer. If you get a summons after sending this letter, don't panic. You'll need to look into legal letters for debt collection to see how to respond to a court filing.

Why You Should Request Debt Validation First

Before you go nuclear with a cease and desist, we almost always recommend sending a Debt Validation Letter first. By law, you have a 30-day window after the first contact to demand proof that you actually owe the money, that the amount is correct, and that the collector has the legal right to collect it.

If you send a cease and desist without validating the debt, you might be silencing the very person who is required to send you the evidence you need to win a case later. Debt buyers often don't have the original paperwork. If they can't validate the debt, they have to stop collecting anyway.

Check out debt validation letters your first line of defense against collectors and our debt validation letter template to start there first.

What Happens After the Collector Receives the Notice?

Once that green return receipt is signed, the "one final contact" rule kicks in. Under the FDCPA, the collector may contact you one last time to:

Advise you that their collection efforts are being terminated.

Notify you that they may invoke specific remedies that are ordinarily invoked by them (like filing a lawsuit).

Notify you that they intend to invoke a specific remedy.

If they call you a week later just to "check in" or "see if you've changed your mind," they have violated federal law.

Dealing with FDCPA Violations and Statutory Damages

If a collector ignores your cease and desist creditor letter, they aren't just being annoying — they are potentially becoming a source of income for you. The FDCPA allows you to sue a collector for violations and recover:

Statutory Damages: Up to $1,000 per lawsuit.

Actual Damages: If the harassment caused you physical illness or lost wages.

Attorney's Fees: The collector has to pay for your lawyer if you win.

Keep a "Violation Log." Write down the date, time, and name of anyone who calls after the letter was received. Save your voicemails. Take screenshots of your call logs. This is how we build a defense that turns the tables on the collectors.

Conclusion

A cease and desist creditor letter is a powerful shield, but it isn't a magic wand. It stops the noise so you can think clearly and plan your next move. Whether you are dealing with a simple mistake of identity or a massive debt buyer, knowing how to silence the phones is the first step toward taking back your life.

At KillDebt, we believe that nobody should be bullied by a multibillion-dollar collection agency. That's why we created ParkerGPT, our AI legal defense system. Trained by me, Brian Parker, with over 30 years of real-world trial experience, ParkerGPT can help you analyze collection letters, identify FDCPA violations, and even help you draft court-ready responses if you get sued.

If you are worried that your cease and desist letter might trigger a lawsuit, we've got you covered there, too. Our brand-new Court Tester tool allows you to upload your legal filings and argue your case in an AI courtroom simulation. You'll face an AI judge and opposing counsel, while your private AI co-counsel whispers winning strategies in your ear.

Don't let debt collectors dictate the terms of your life. Take action today, send your letter, and if they decide to take it to court, we'll be right there with you. Visit us at https://killdebt.com/ to start your DIY legal defense.

Frequently Asked Questions (FAQ)

Can I send a letter for a debt I actually owe?

Yes. Your right to be free from harassment does not depend on whether the debt is valid. Even if you owe every penny, you have the right to tell a third-party collector to stop contacting you.

What if the collector ignores my letter and keeps calling?

This is a violation of 15 U.S.C. § 1692c(c). You should file a complaint with the Consumer Financial Protection Bureau (CFPB) and contact a consumer protection attorney. Every call after the letter is received is evidence for a potential lawsuit where you could be awarded $1,000.

Does this letter apply to my original credit card company?

Usually, no. The FDCPA applies to "debt collectors" (third parties). However, Florida and Michigan have state laws that prohibit original creditors from engaging in "harassing" or "deceptive" behavior. While they might not have to honor a "cease all communication" request in the same way, they still cannot call you 20 times a day or threaten you with jail.