What a Default Judgment Means for Your Debt — and How to Fight Back

If you're trying to figure out how remove default judgment debt from your record, here's the short answer:

Get your court file — find your case number and pull the affidavit of service

Identify your grounds — improper service, excusable neglect, or fraud

File a Motion to Vacate (also called a Motion to Set Aside) with your local court

Serve the other side — deliver a copy to the plaintiff or their attorney

Attend the hearing — present your reason and your defense to the judge

If granted — the judgment is removed and the lawsuit restarts

Act fast. Deadlines range from 14 days to 1 year depending on your state.

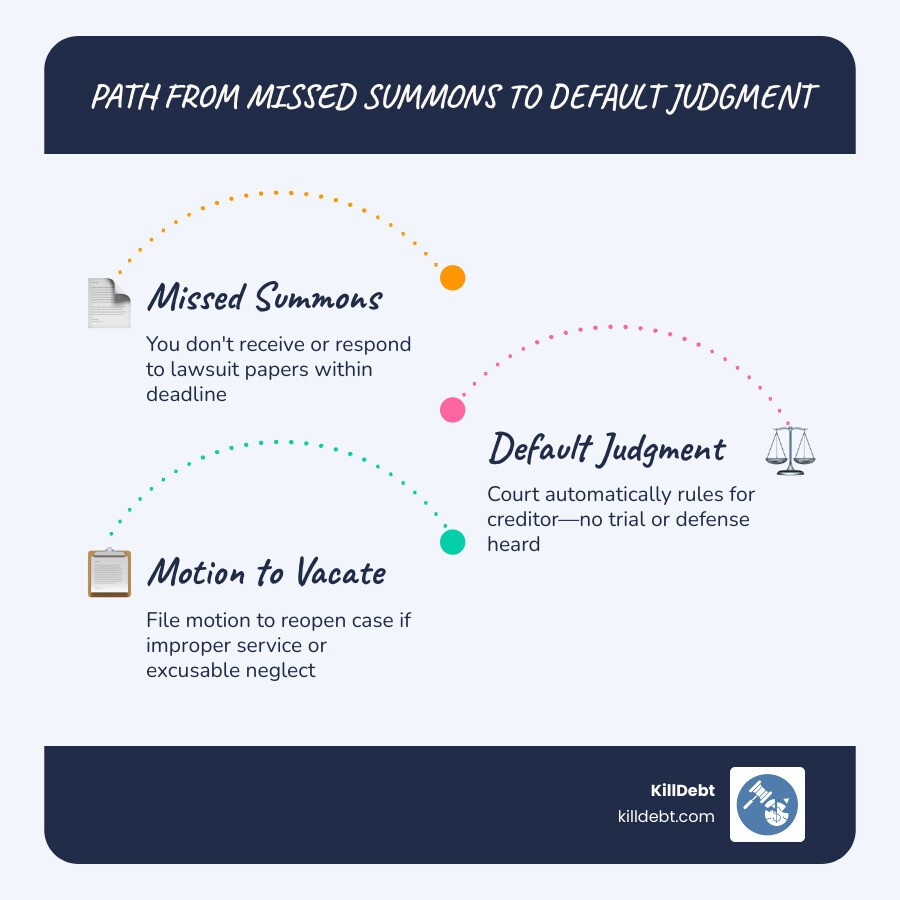

A default judgment is what happens when a creditor sues you — and you don't respond. The court doesn't hear your side. The plaintiff wins automatically.

That's it. No trial. No defense. Just a ruling against you.

And it hits hard. With a default judgment in place, creditors can garnish your wages, freeze your bank account, and place liens on your property. Over 70% of debt collection lawsuits end this way — often because people didn't know they were even being sued.

This happens more than you'd think. Process servers sometimes deliver papers to the wrong address, leave them with a child, or — in some cases — don't deliver them at all. You find out about the judgment when money disappears from your paycheck or your bank account gets locked.

The good news: a default judgment is not always the end of the road.

Courts can — and regularly do — remove default judgments when defendants act quickly and show good reason. This guide walks you through exactly how to do that, step by step.

Understanding How to Remove Default Judgment Debt

When you discover a judgment against you, the first thing we need to do is stay calm. A judgment is a court order, but it isn't etched in stone. To "remove" it, we use a legal process called "vacating" or "setting aside" the judgment.

Think of it as a "Ctrl+Z" for a court case. When a judge grants a Motion to Vacate, the judgment is cancelled. It’s as if the "automatic win" for the creditor never happened. However, it’s important to understand that this doesn’t usually make the debt vanish instantly—it simply puts the lawsuit back at the beginning, giving you the chance to fight the claim on its merits.

To succeed, you generally have to prove two things to the court:

A Good Reason: Why didn't you respond to the lawsuit originally? (e.g., you weren't served papers).

A Meritorious Defense: If the case is reopened, do you actually have a legal reason why you don't owe the money? (e.g., the debt is past the statute of limitations).

Understanding the debt collection lawsuit timeline is crucial because the law favors "finality." This means the longer you wait after finding out about a judgment, the harder it becomes to convince a judge to reopen the case.

Common Grounds for Removing Default Judgment Debt

Judges don't set aside judgments just because you're a nice person or because the debt is a burden. You need specific legal "grounds." Here are the most common reasons we see:

Improper Service (The "Sewer Service"): This is the most powerful ground. If the process server lied about giving you the papers—or left them with your 10-year-old neighbor—the court never actually had the authority to rule against you. In many states, like New York, there is no time limit to vacate a judgment if you were never properly served.

Excusable Neglect: This is the "reasonable excuse" category. Maybe you were hospitalized, dealing with a death in the family, or you were out of the country when the papers arrived.

Fraud or Misconduct: If the creditor lied to the court or told you "don't worry about the court date, we're settling this," and then went behind your back to get a judgment, that is fraud.

Meritorious Defense: You must show that if the case continues, you have a chance to win. This could include identity theft, the debt being already paid, or the creditor lacking the proper paperwork to prove they own the debt.

Knowing what to do when sued by a debt collector starts with identifying which of these categories fits your situation.

The Role of Personal Jurisdiction

In the legal world, "Personal Jurisdiction" is a fancy way of saying the court has the power to make a decision about you. For a court to have this power, you must be properly notified of the lawsuit through a Summons and Complaint.

If the creditor failed to serve you according to the strict rules of your state (Florida or Michigan, for example), the court lacks jurisdiction. A judgment entered without jurisdiction is "void." We often find that debt buyers are sloppy with service, which is your best opening to how remove default judgment debt.

Step-by-Step Process to Vacate a Judgment

If you've discovered a judgment on your credit report or via a garnishment notice, follow these steps immediately.

1. Locate the Court and Case Number You can find this on your credit report, the garnishment paperwork, or by calling your local courthouse. You need the "Index Number" or "Case Number."

2. Get the Court File Go to the courthouse where the judgment was entered. Ask the clerk for the complete file. Specifically, look for the Affidavit of Service. This is the document where the process server swore under oath that they delivered the papers to you. If the description of the person served doesn't match you, or the address is a place you haven't lived in five years, you have your evidence.

3. Determine Your Deadline Every state has a time to respond and specific windows for vacating. In Michigan, for instance, you typically have only 21 days from the entry of a default judgment to ask to set it aside. In other areas, you might have up to a year for "excusable neglect," but "lack of service" often has no expiration date.

Drafting the Motion and Affidavit of Meritorious Defense

This is the "meat" of your request. You cannot just write a letter to the judge. You must file a formal Motion to Set Aside Default Judgment.

Along with the motion, you must include an Affidavit of Meritorious Defense. This is a sworn statement, signed in front of a notary, where you explain your side. You need to be specific. Don't just say "I don't owe this." Say, "I do not owe this debt because the statute of limitations expired in 2021," or "I never had an account with this original creditor."

Using a solid counter-affidavit is the key to showing the judge that reopening the case isn't a waste of the court's time.

Filing and Serving Your Legal Papers

Once your papers are drafted:

File with the Clerk: Take the originals to the courthouse. You may have to pay a filing fee, though most courts offer fee waivers if you are low-income.

Get a Hearing Date: The clerk will give you a date and time to appear before the judge.

Serve the Plaintiff: You must send a "file-stamped" copy of your motion to the creditor’s attorney. This is usually done by certified mail or a process server.

File Proof of Service: You must prove to the court that you sent the papers to the other side. This is often called a Certificate of Service.

State-Specific Deadlines and Requirements

Because we focus on Florida and Michigan, it is vital to know that the rules change the moment you cross state lines.

State | Deadline to File Motion | Common Requirement |

|---|---|---|

Michigan | 21 Days from Entry | Must show "Good Cause" and "Meritorious Defense" |

Florida | "Reasonable Time" (usually 1 year) | Must show "Excusable Neglect," "Due Diligence," and "Meritorious Defense" |

Texas | 30 Days (14 in Justice Court) | Must show the failure to answer was an accident or mistake |

New York | 1 Year (Excusable Default) | No limit for lack of personal jurisdiction |

In Michigan, if you miss that 21-day window, you have to file a "Motion for Relief from Judgment," which has a much higher bar for success. In Florida, the "Three-Prong Test" is famous: you must prove you had a good reason for missing the deadline, you acted quickly once you found out, and you have a real defense to the debt.

Navigating the Hearing to Remove Default Judgment Debt

When the day of your hearing arrives, show up early. Dress like you’re going to a job interview—professionalism goes a long way with judges.

When your case is called, you will speak first. Briefly explain to the judge:

"Your Honor, I am asking to set aside this judgment because I was never served with the summons."

Show your evidence (e.g., a lease showing you lived elsewhere).

State your defense: "Furthermore, I have a meritorious defense because this debt is time-barred."

The creditor’s attorney will likely be there (or on the phone) to argue against you. Stay calm. Don't interrupt. The judge may ask if you need a lawyer, and while you can do this yourself, being prepared with the right facts is what wins the day.

Possible Outcomes of the Motion

There are generally three ways this goes:

Motion Granted: The judgment is gone! The case is reopened. You must file an "Answer" to the original lawsuit immediately to prevent a second default.

Motion Denied: The judgment stays. The creditor can continue garnishing your wages. At this point, you might need to look into settlement or bankruptcy.

Conditional Grant: The judge might say, "I'll vacate the judgment, but only if you pay the creditor's legal fees for today's hearing."

Don't fall for lawsuit myths—simply showing up doesn't guarantee a win. You must have your paperwork in order.

Consequences of Ignoring a Default Judgment

Ignoring a judgment is like ignoring a fire in your kitchen—it only gets bigger. In Michigan and Florida, a judgment isn't just a piece of paper; it’s a weapon for the creditor.

Wage Garnishment: Creditors can take up to 25% of your disposable income directly from your paycheck.

Bank Levies: They can wipe out your entire checking or savings account in one day.

Property Liens: The judgment can be attached to your home. You won't be able to sell or refinance your house without paying the creditor first.

Interest: Judgments accrue interest. In some states, this is 10% or more per year. A $5,000 debt can quickly turn into $10,000.

We've detailed exactly how debt collectors take wages and bank accounts in our companion guides, and the reality is that a judgment gives them the keys to your financial life.

Conclusion

Removing a default judgment is one of the most empowering things you can do for your financial health. It stops the garnishments, clears your record, and gives you a second chance to stand up for your rights.

At KillDebt, we know that the legal system can feel like it's designed to make you lose. That's why we created a DIY legal defense system powered by ParkerGPT. This AI is trained on consumer debt law and real-world court strategies developed over 30 years by attorney Brian Parker.

Unlike generic templates, our system analyzes your actual lawsuit documents and generates court-ready responses tailored to your specific case. We also recently introduced the Court Tester, an AI courtroom simulation. You can upload your filings and practice arguing your motion in front of an AI judge, with a private AI co-counsel whispering strategy to you.

Don't let a procedural mistake ruin your finances. Whether you're in Michigan, Florida, or beyond, you have the right to be heard. Take control of your case with KillDebt today.

Frequently Asked Questions (FAQ)

What happens if I missed the deadline to set aside the judgment?

If the standard 21-day or 30-day window has passed, you aren't necessarily out of luck. You can file for "Equitable Relief." This is a plea to the judge's sense of fairness. If you can prove "extraordinary circumstances"—like being in a coma or serving overseas in the military—the court may still listen. If all else fails, a judgment can often be settled for 50-70% of the total amount if you can offer a lump sum.

Can I remove a judgment from my credit report?

Yes, but only if it's vacated. Since 2017, most tax liens and civil judgments were removed from standard credit reports (Equifax, Experian, TransUnion). However, they still exist in public records and can be seen by mortgage lenders or employers. If you vacate the judgment, you should send the "Order Vacating Judgment" to the credit bureaus to ensure it is completely purged.

Does vacating a judgment mean the debt is gone?

No. It means the judgment is gone. The lawsuit is now "active" again. You will be required to file a formal Answer and potentially go to trial or engage in the "discovery" phase (where you exchange evidence). This is actually a good thing—it gives you the leverage to negotiate a much better settlement or win the case outright if the creditor can’t prove their claims.