Why a Letter of Debt Validation Can Stop Debt Collectors in Their Tracks

A letter of debt validation is one of the most powerful tools you have when a debt collector comes calling. Under federal law, collectors must send you a written notice with key details about the debt — and you have the right to dispute it.

Quick answer: What is a letter of debt validation?

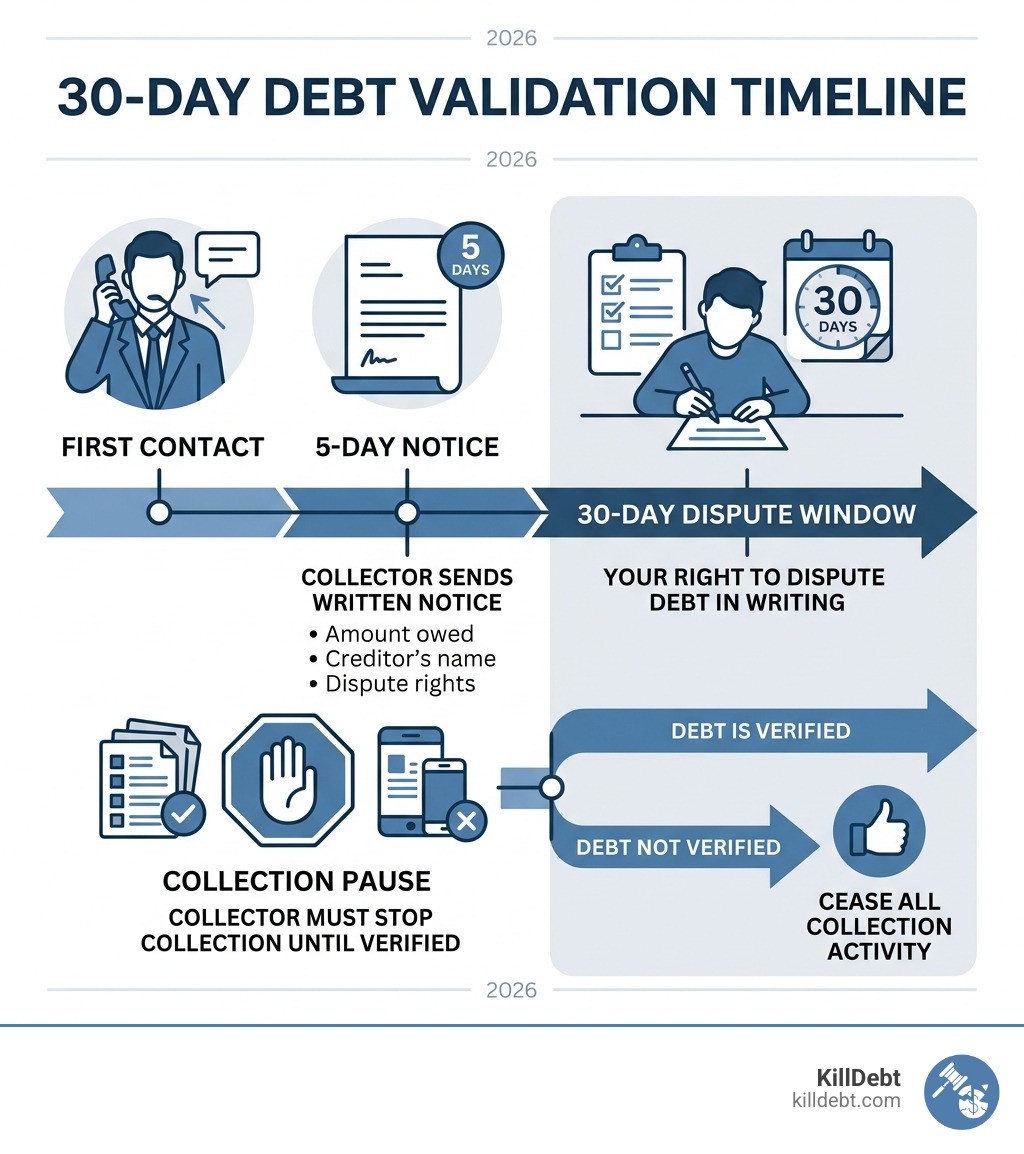

It is a written notice a debt collector must send you within 5 days of first contact

It must include: the amount owed, the creditor's name, and your right to dispute within 30 days

If you dispute in writing within 30 days, the collector must stop collection until they verify the debt

If they cannot verify it, they must cease all collection activity

Here's the thing: nearly half of all debt collection complaints involve collectors pursuing debts that aren't valid or have the wrong amount. That means getting — and responding to — a validation notice isn't just a technicality. It's your first real line of defense.

Whether the debt isn't yours, the amount is wrong, or you just aren't sure, knowing how this process works can save you from paying money you don't owe.

Understanding the Letter of Debt Validation and Your Rights

When a debt collector reaches out to us, they aren't just making a friendly suggestion that we pay up. They are initiating a legal process governed by the Fair Debt Collection Practices Act (FDCPA). This federal law is our shield, and the letter of debt validation is our first move in the game.

Under the FDCPA, a debt collector is legally required to provide us with specific information about the debt they claim we owe. This isn't optional. If they don't provide this information during their first conversation with us, they must send a written notice within five days. This notice is often called a "G-Notice" or a validation notice.

The primary goal of this notice is transparency. It prevents collectors from "blindside" tactics where they demand money without proving they have the right to collect it. According to Investopedia, these rights are essential because debt is often sold and resold. By the time a collector calls us, the paperwork might be a mess, the amount might be inflated with illegal fees, or the debt might not even belong to us anymore.

Essential Information in a Letter of Debt Validation

A legally compliant validation notice isn't just a bill; it must contain specific "validation information." If any of these pieces are missing, the collector might be in violation of federal law. According to the Consumer Financial Protection Bureau (CFPB), the notice must include:

The amount of the debt: This should be itemized, showing interest, fees, and payments made since the "itemization date."

The name of the creditor: This is the current creditor to whom the debt is owed.

A statement of your rights: The notice must explicitly state that you have 30 days to dispute the debt.

The original creditor: If you request it in writing within 30 days, the collector must provide the name and address of the original creditor.

A "tear-off" dispute form: Recent 2021 updates to the FDCPA (Regulation F) often require a prompt for you to dispute the debt directly on the notice.

If you receive a notice that is just a vague demand for money without an account number or the name of the original creditor, don't reach for your wallet. Reach for your keyboard and prepare a dispute.

When Must a Collector Send the Notice?

Timing is everything in debt collection. The law states that the collector must provide this validation information either in the initial communication (the first phone call or email) or in a written notice sent within five days of that first contact.

In our experience at KillDebt, collectors sometimes try to skip this step, hoping we'll just pay out of fear. However, if they fail to send this notice, they are violating the FDCPA. This notice can be sent via traditional mail or, in some cases, electronically if you have consented to that method of communication. Keep a close eye on your mailbox; the 30-day clock starts the moment you receive that letter.

Debt Validation vs. Debt Verification: Knowing the Difference

There is often a lot of confusion between "validation" and "verification." While they sound similar, they represent two different sides of the same coin.

Validation Notice: This is the document the collector sends to you. It is their opening move to tell you what they think you owe.

Verification Request: This is the letter you send to the collector. It is your way of saying, "Prove it."

Feature | Debt Validation Notice | Debt Verification Request |

|---|---|---|

Who sends it? | The Debt Collector | The Consumer (You) |

When is it sent? | Within 5 days of first contact | Within 30 days of receiving notice |

Purpose | To inform you of the debt details | To dispute the debt and demand proof |

Legal Effect | Fulfills collector's FDCPA duty | Pauses all collection activity |

As we highlight in our guide on debt validation letters: your first line of defense against collectors, sending a verification request is how you take control of the situation. It shifts the burden of proof back onto the agency.

What to Include in a Debt Verification Request

When you write back to a collector to verify a debt, you shouldn't just say "I don't owe this." You want to be specific to ensure they can't just send back a computer printout and call it a day. A strong letter of debt validation (sent by you) should ask for:

Proof of ownership: A copy of the contract or agreement signed by you.

Chain of title: Documentation showing how the debt moved from the original creditor to this specific collector.

Itemized breakdown: A clear list of the original balance plus every cent of interest and fees added since.

Licensing info: Proof that the collector is licensed to collect debts in your state (especially important for our friends in Michigan and Florida).

Statute of Limitations: Information regarding the last date of activity on the account to see if the debt is "time-barred."

Your Rights Under the FDCPA: The 30-Day Rule

The "30-day rule" is perhaps the most critical protection for any consumer. From the moment you receive that validation notice, you have a 30-day window to dispute the debt in writing.

Why is this 30-day window so important? Because if you send your dispute within this timeframe, the collector must stop all collection efforts until they provide you with the verification you requested. They can't call you, they can't send you more bills, and they can't report the debt as "un-disputed" to credit bureaus during this pause.

If you miss this window, the collector is legally allowed to assume the debt is valid. While you can still dispute it later, you lose that automatic "pause" button on their collection activities.

Can You Send a Letter of Debt Validation After 30 Days?

Yes, you can still send a dispute letter after the 30-day mark, but your legal "teeth" are a bit duller. After 30 days, the collector doesn't have to stop calling or writing while they look for your verification.

However, it is still worth doing. If the debt is "zombie debt" (very old debt) or if you suspect identity theft, a late dispute still puts the collector on notice. In states like Michigan and Florida, continuing to collect on a debt that is clearly invalid or past the statute of limitations can still lead to legal trouble for the collector, regardless of whether you missed the initial 30-day window.

How to Send Your Dispute and What to Include

When it comes to the law, "it's not what you know, it's what you can prove." If you call a collector to dispute a debt, you have almost no protection. The FDCPA specifically requires disputes to be in writing to trigger the requirement for the collector to cease activity.

Step-by-Step Guide to Mailing Your Letter

Use a Template: Don't reinvent the wheel. Use a reliable template that cites the FDCPA correctly.

Be Clear: State clearly that you are disputing the debt and requesting "verification."

Certified Mail is King: Always send your letter of debt validation via Certified Mail with a Return Receipt Requested. This gives you a green card signed by the collector proving they received your letter.

Keep Copies: Keep a copy of your letter, the certified mail receipt, and any response you get.

Don't Give Too Much Info: You don't need to explain your whole life story or why you can't pay. Simply demand the proof.

At KillDebt, we've seen many cases where a collector claims they "never got the letter." Having that USPS tracking number and the signed return receipt is your "get out of jail free" card in court.

What Happens After You Dispute a Debt?

Once the collector receives your dispute, they have a choice: find the proof or give up. Because many debt buyers purchase thousands of accounts for pennies on the dollar, they often don't have the original contracts. If they can't find the paperwork, they often simply stop contacting you.

If they do send verification, you need to review it carefully. Does the math add up? Is it actually your signature on the contract? If the verification is insufficient, you can continue to dispute it.

What if the Collector Fails to Validate?

If a collector cannot validate the debt but continues to call you or report the debt to your credit report, they are likely in violation of the FDCPA. This is where you can turn the tables.

Cease Collection: They must stop all efforts to collect.

Credit Reporting: They must notify the credit bureaus that the debt is disputed. If they can't verify it, they should remove it from your report.

Legal Recourse: You may be able to sue the collector for up to $1,000 in statutory damages, plus attorney fees.

Conclusion: Take Control with KillDebt

Dealing with debt collectors is stressful, but you don't have to do it alone or spend thousands on an attorney. At KillDebt, we believe in empowering you with the same tools the "big guys" use.

Our DIY legal defense system is powered by ParkerGPT, an AI trained on over 30 years of consumer debt law and real-world strategies from attorney Brian Parker. Whether you need to generate a perfect letter of debt validation or you've been served with a lawsuit, our platform identifies the collector's weaknesses and helps you fight back.

We even offer the Court Tester, an AI courtroom simulation. You can upload your actual court filings and practice your motion in front of an AI judge before you ever step foot in a real courtroom. It’s like having a private co-counsel whispering the winning strategy in your ear.

Don't let collectors bully you into paying debts they can't prove. Use your rights, send your letters, and let technology level the playing field.

Frequently Asked Questions (FAQ)

How long does a collector have to respond?

Interestingly, the FDCPA does not set a hard deadline for how long a collector has to respond to your verification request. They could take two weeks or two years. However, the catch is that they cannot try to collect from you until they do respond. If they never respond, they can never legally collect the debt. It creates an indefinite pause in the collection process.

Can small businesses use debt validation letters?

The federal FDCPA primarily covers "consumer" debts—money owed for personal, family, or household purposes. It generally does not cover business-to-business debts. However, some state laws provide additional protections. If you are a small business owner in Florida or Michigan being harassed by a collector, it is worth checking local statutes, as some state-level "Fair Debt Collection" acts are broader than the federal version.

What if the debt is already paid or not mine?

This is exactly what the letter of debt validation is for! If you've already paid the debt, include a copy of your cancelled check or bank statement with your dispute. If it's a case of identity theft, state that clearly and offer to provide a police report. Never pay a "settlement" on a debt that isn't yours just to make it go away—that can actually damage your credit further by acknowledging a debt that wasn't yours to begin with.