What the Head of Household Exemption Means for Your Wallet — and Your Wages

The head of household exemption is a legal protection that can shield your paycheck, reduce your tax bill, or lower your property taxes — depending on where you live and what situation you're in.

Quick answer: What does it do?

Context | What It Protects | Key Threshold |

|---|---|---|

Wage garnishment (Florida) | 100% of your earnings | Earning $750/week or less in disposable income |

Property tax (New Mexico) | Up to $2,000 of taxable property value | Must be a qualifying head of family and NM resident |

Federal income tax filing | Higher standard deduction ($23,625 in 2025) | Must be unmarried and support a qualifying person |

These three protections share the same name but work very differently. And if a debt collector is threatening to garnish your wages right now, the wage garnishment version is the one you need to understand immediately.

If you're staring down a garnishment notice, here's the short version: in states like Florida, if you provide more than half the financial support for a child or other dependent, a creditor may not be able to touch your paycheck at all. But this protection is not automatic — you have to claim it, and you usually have a very short window to act.

I'm Brian Parker, and for over 30 years I've been fighting debt collectors and collection law firms in courtrooms across the country — using the head of household exemption as one of the most powerful tools to protect my clients' income. In the guide below, I'll walk you through exactly how this exemption works, who qualifies, and what steps to take before your next paycheck is at risk.

Understanding the Head of Household Exemption Across Different Laws

When we talk about the head of household exemption, we are actually talking about three distinct legal "shields" that protect your money from different entities. It is vital to understand which one you are trying to use, as the rules for the IRS aren't the same as the rules for a Florida sheriff or a Michigan court.

At its core, the Head of household status was created to acknowledge the extra financial burden carried by those who support others. Whether it's the IRS giving you a break on your 1040 or a state law preventing a credit card company from taking your grocery money, the goal is the same: keeping families afloat.

In Florida, this exemption is found under Florida Statute §222.11. This law is a powerhouse for asset protection. It essentially says that if you are the "head of family," your wages are off-limits to most creditors. In Michigan, while the terminology might differ slightly, there are still robust protections for income that is "necessary for the care and support of your family."

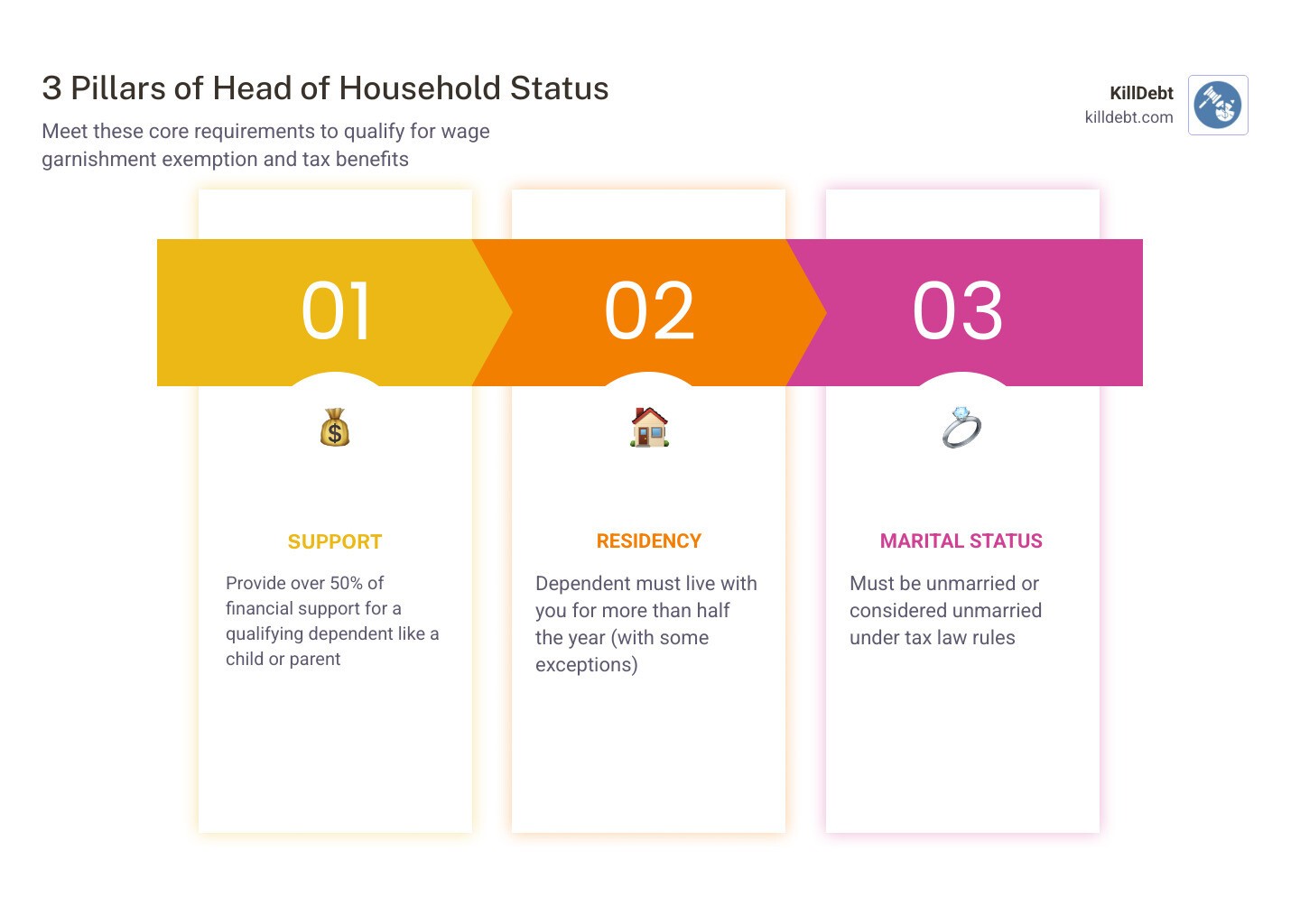

Eligibility Requirements for the Head of Household Exemption

To claim this status, you generally have to pass three main tests. If you fail one, the shield might not hold.

The Financial Support Test: You must provide more than 50% of the financial support for a dependent. This means you’re paying for the lion's share of food, rent, utilities, and medical care.

The Qualifying Person Test: This is usually a child, but it can also be a parent, a sibling, or even an adult relative who is disabled. Interestingly, for IRS purposes, a dependent parent doesn't always have to live with you, as long as you pay for more than half their living costs (like a rest home).

The Residency Rule: For tax purposes, the qualifying person usually needs to live with you for more than half the year (at least 183 days). However, for Florida wage garnishment protection, the dependent doesn't strictly have to live under your roof, though it certainly makes your case easier to prove in court.

According to the Census Population Survey, as of 2015, roughly 76% of those filing with this status were women, highlighting how often single mothers serve as the primary financial anchors for their families. For a deep dive into the tax-specific side of this, check out this Guide to Filing Taxes as Head of Household - TurboTax Tax Tips & Videos.

State-Specific Variations: Florida vs. Michigan

Since we operate in Florida and Michigan, let's look at how these protections manifest locally.

In Florida, the head of household exemption is incredibly generous. If you earn $750 or less per week in disposable earnings (that’s your take-home pay after legally required deductions), you are fully exempt from garnishment. If you earn more than $750, you are still exempt unless you have signed a very specific written waiver. And even then, that waiver has to meet strict formatting rules—like being in 14-point type—to be valid.

In Michigan, the focus is often on protecting a specific amount of income needed for basic necessities. While the "Head of Family" terminology is less prominent in Michigan statutes than in Florida, the principle remains: creditors cannot strip you of the ability to support your dependents. You often have to provide a "financial statement" to the court to show that the money they want to take is actually required for your family's survival.

Protecting Your Paycheck: The Wage Garnishment Defense

Wage garnishment is a terrifying prospect. You work 40+ hours a week, but when you check your bank account, a chunk of your hard-earned money is missing. Under federal law, creditors are generally limited to taking 25% of your disposable earnings. However, the head of household exemption can often bring that number down to 0%.

In Florida, this protection is "reactive." This means you don't file for it ahead of time like a tax return. Instead, you use it as a defense once a "writ of garnishment" has been served on your employer. If you qualify, 100% of your wages can be protected.

It's important to know that "disposable earnings" are what's left after things like federal taxes and Social Security are taken out. Voluntary deductions, like your 401(k) contribution or health insurance, don't count toward lowering that number in the eyes of the court. You can find more details on this process in this guide on What Is the Head of Household Exemption for Wage Garnishment?.

Documentation Needed to Prove Your Head of Household Exemption Status

If you're going to tell a judge that you're the "Boss of the House," you need the receipts to prove it. Creditors will fight you on this, so come prepared with:

Tax Returns: Your most recent federal filing showing your status.

Pay Stubs: To prove your income and the $750/week threshold.

Bank Statements: Showing that your wages are being used for household expenses.

Household Bills: Leases, utility bills, and grocery receipts that show you are paying more than 50% of the costs.

Birth Certificates: To prove the relationship with your dependents.

How to Claim Your Exemption and Stop a Garnishment Immediately

Time is your enemy here. In Florida, once you receive notice of a garnishment, you typically have only 20 days to file a "Claim of Exemption." If you miss this window, the employer is legally required to start sending your money to the creditor.

Here is the step-by-step process we recommend:

File the Claim of Exemption: This is a notarized affidavit where you swear under oath that you provide more than half the support for a dependent.

Notify Everyone: You must deliver this claim to the court, the creditor’s attorney, and your employer's payroll department.

Prepare for a Hearing: If the creditor objects (and they often do), a judge will set a hearing. You’ll need to bring your documentation.

Use AI Tools: At KillDebt, our ParkerGPT tool can help you analyze the garnishment papers and generate the correct response forms in minutes.

For more on the mechanics of this, read our detailed breakdown: Can Debt Collectors Take My Wages And Bank Account.

IRS Filing Status vs. Legal Exemptions: What You Need to Know

Many people confuse the "Head of Household" filing status on their taxes with the legal exemption that stops garnishment. While they often overlap, they are not the same thing.

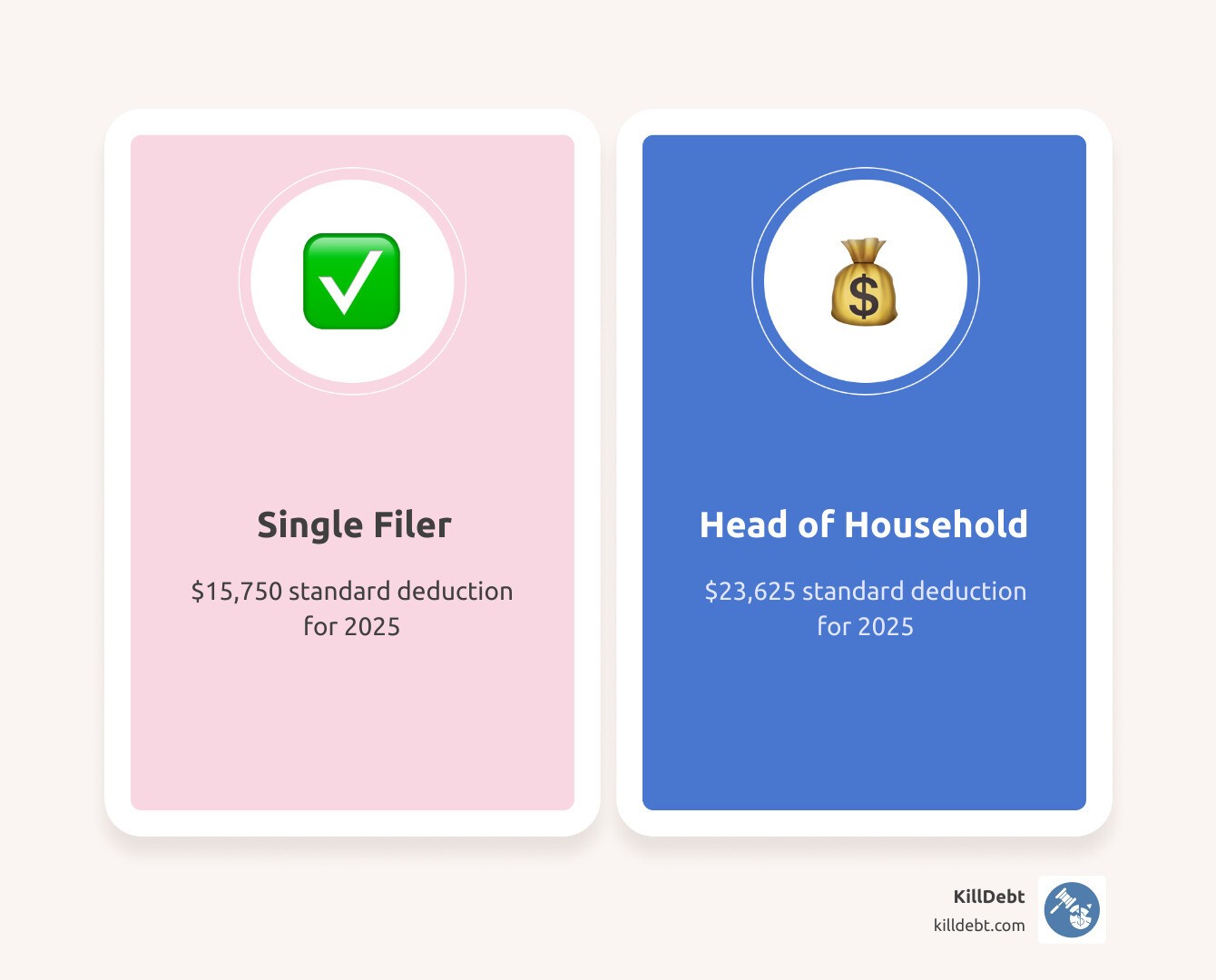

For the tax year 2025 (filing in May 2026), the standard deduction for a Head of Household is $23,625. Compare that to just $15,750 for single filers. That’s nearly $8,000 in income you aren't taxed on just for being the primary supporter of your home.

You can even qualify as "considered unmarried" by the IRS if you are still legally married but have lived apart from your spouse for the last six months of the year. This is a vital loophole for those in the middle of a long separation who are still footing all the bills. States like California have their own specific rules, which you can see at Head of Household | FTB.ca.gov, but for our friends in Florida and Michigan, the federal guidelines are the primary focus.

Benefits of Filing as Head of Household in 2026

The benefits are massive. Beyond the higher standard deduction, you also get access to wider tax brackets. This means more of your money is taxed at the 10% and 12% rates before you jump into higher percentages.

For a single parent earning a modest income, this status can save hundreds, if not thousands, of dollars. In fact, eliminating this status would cost American families an estimated $16 billion per year.

Conclusion

Defending your home and your income from debt collectors doesn't require a law degree, but it does require the right tools. The head of household exemption is one of the strongest shields in your arsenal, but you have to know when and how to lift it.

At KillDebt, we’ve taken the 30+ years of courtroom experience from attorney Brian Parker and built it into ParkerGPT. We don't just give you generic templates; our AI analyzes your specific lawsuit or garnishment documents to find the "cracks" in the creditor's case.

Ready to see if you can win? Our brand new Court Tester allows you to upload your filings and practice your defense in an AI courtroom simulation. You'll face an AI judge and opposing counsel, while a private AI co-counsel whispers the winning strategy in your ear. Don't let a debt collector take what you've earned for your family.

Take action today. Use ParkerGPT to protect your paycheck and your peace of mind. More info about debt defense services

Frequently Asked Questions (FAQ)

Can both spouses in one home claim Head of Household status?

Generally, no. The IRS and state courts usually view a "household" as a single economic unit. However, there is a rare exception: if two unmarried people live in the same house but maintain completely separate financial lives—separate food, separate bills, separate support for separate children—they might both qualify. But be warned: this is a "red flag" for audits and requires meticulous record-keeping.

Does my dependent have to live with me to qualify for the exemption?

For federal tax purposes, a "qualifying child" must live with you for more than half the year. However, a qualifying parent does not have to live with you. If you pay for more than half the cost of your mother’s apartment or her stay in an assisted living facility, you can still file as Head of Household. For Florida wage garnishment, the "support" is more important than the "address," though living together makes the legal argument much stronger.

What happens to my exempt wages once they are deposited into a bank account?

In Florida, your exempt wages stay protected for six months after they hit your bank account, provided they can be "traced." This is where most people get into trouble. If you mix your paycheck with other money (like a tax refund or a gift from a friend), it becomes "commingled." Creditors will argue the money is no longer "wages." Pro-tip: Open a dedicated "Wage Account" where only your direct-deposited paycheck goes. This makes tracing the funds simple and keeps the debt collectors' hands off your cash.