When Old Debt Comes Back to Haunt You — Know Your Rights

An expired debt statute defense is one of the most powerful legal tools available to consumers facing collection lawsuits. Here's a quick overview of what it means and when it applies:

Top expired debt statute defenses at a glance:

Time-barred debt — The statute of limitations (SOL) on your debt has expired, meaning a creditor can no longer win a lawsuit against you to collect it.

Affirmative defense in court — You must actively raise the expired SOL in your court response. Judges will not apply it automatically.

FDCPA protection — Federal law prohibits debt collectors from suing or threatening to sue you over time-barred debt.

No default judgment — You must show up and respond to any lawsuit, even for old debt, or you automatically lose.

Clock triggers matter — The SOL clock typically starts on the date of your first missed payment, not when a collector contacts you.

If you just received a court summons or a collection letter for a debt that feels ancient, you are not alone — and you may have more legal protection than you think.

Most consumers don't realize that creditors have a limited window to sue over unpaid debt. That window is called the statute of limitations. Once it closes, the debt is considered "time-barred." The creditor still technically exists as your creditor — but they lose the legal right to use the courts to force you to pay.

Here's the catch: that protection disappears the moment you ignore a lawsuit. If you don't show up and raise the defense, a judge can — and often will — hand the creditor an automatic win. That means wage garnishment, bank levies, and liens on your property. All for a debt that may have legally expired years ago.

The good news? You don't need an expensive attorney to fight back. You just need to know the rules.

I'm Brian Parker, and for over 30 years I've been in the courtroom fighting creditors, debt buyers, and collection law firms — and the expired debt statute defense is one of the most reliable shields I've used to protect consumers facing exactly the situation you may be in right now. I founded KillDebt to put those same courtroom-tested strategies directly in your hands, so let's break down exactly how to use this defense.

Understanding the Expired Debt Statute Defense

In debt collection, time is more than just money—it’s your best defense. The expired debt statute defense is what we call an "affirmative defense." This means that even if you truly owe the money, you can still win the case if the creditor waited too long to sue you.

When a debt passes the state-mandated deadline for filing a lawsuit, it becomes "time-barred." According to the Consumer Financial Protection Bureau (CFPB), while a debt collector might still try to contact you, they are legally prohibited from suing or threatening to sue you once that clock runs out.

However, the burden of proof is on you. A judge isn't going to look at the date on your old credit card bill and dismiss the case for you. You must file a response—an Answer—and explicitly state that the statute of limitations has expired. If you ignore the summons, the creditor can get a default judgment, which effectively "resurrects" the debt and allows them to garnish your wages or seize your bank accounts, regardless of how old the debt was.

Under the Fair Debt Collection Practices Act (FDCPA) and the newer Regulation F, debt collectors are restricted in how they handle time-barred debt. In many cases, it is a violation of federal law for a collector to even imply they might sue you for an expired debt. Understanding these protections is the first step in our Debt Lawsuit Defense Guide.

How to Identify if Your Debt is Time-Barred

To know if your debt is "ancient history," you have to find the "date of last activity." This is the moment the stopwatch started. Generally, the statute of limitations clock begins ticking when you miss a payment and the account becomes delinquent.

Calculating this requires digging through old records. You are looking for the date of the first missed payment that led to the account being charged off. The time to respond to a debt collection lawsuit is usually very short—often 20 to 30 days—so you need to act fast.

The length of the statute of limitations depends on the type of debt:

Written Contracts: Formal agreements signed by both parties (like medical bills or some personal loans).

Open-ended Accounts: Accounts with revolving balances (like credit cards).

Oral Agreements: Verbal promises to pay (hardest for creditors to prove).

Promissory Notes: Detailed written promises to pay a specific amount by a specific date (like student loans or mortgages).

Different states have vastly different rules. For example, while 13 states have a short 3-year limit on credit card debt, others can stretch up to 10 years. You can find more details on how these rules function in specialized guides for time-barred debts.

Using the Expired Debt Statute Defense in Florida

Florida is a unique battlefield for debt defense. As of May 2026, Florida ranks 10th in the nation for credit card debt, with an average per-household debt of $3,340. The state also sees high levels of auto debt, ranking 7th with $5,580 per household.

In Florida, the statute of limitations on debt is generally:

5 years for written contracts.

4 years for oral agreements and open-ended accounts (like credit cards).

This means if you haven't made a payment on a Florida credit card in over four years, you likely have a rock-solid expired debt statute defense. Given that Florida has the 12th highest state debt in the U.S. but the 5th lowest per capita debt, creditors are often aggressive in trying to recover funds from individual residents. Knowing your rights in Florida is essential for protecting your assets.

Avoiding a Reset of Your Expired Debt Statute Defense

One of the most dangerous traps a debt collector can set is "restarting the clock." This is often called "zombie debt" because a collector tries to bring a dead debt back to life.

In many states, including Michigan and Florida, taking certain actions can reset the statute of limitations to zero, giving the collector a brand-new window to sue you. These "revival" actions include:

Making a partial payment: Even sending $5 "in good faith" can restart the entire 4 or 5-year clock.

Acknowledging the debt in writing: Signing a letter that says "I know I owe this and will pay soon" can be enough to lose your defense.

Entering a payment plan: This creates a new contract, essentially erasing the time you've already waited.

There are also "tolling" events. Tolling is when the clock is paused. This usually happens if you leave the state where the debt was incurred. If you move from Florida to Michigan, the time you spent outside of Florida might not count toward your Florida statute of limitations. For more on these traps, check out our guide on debt collection lawsuit myths.

Critical Steps to Raising Your Defense in Court

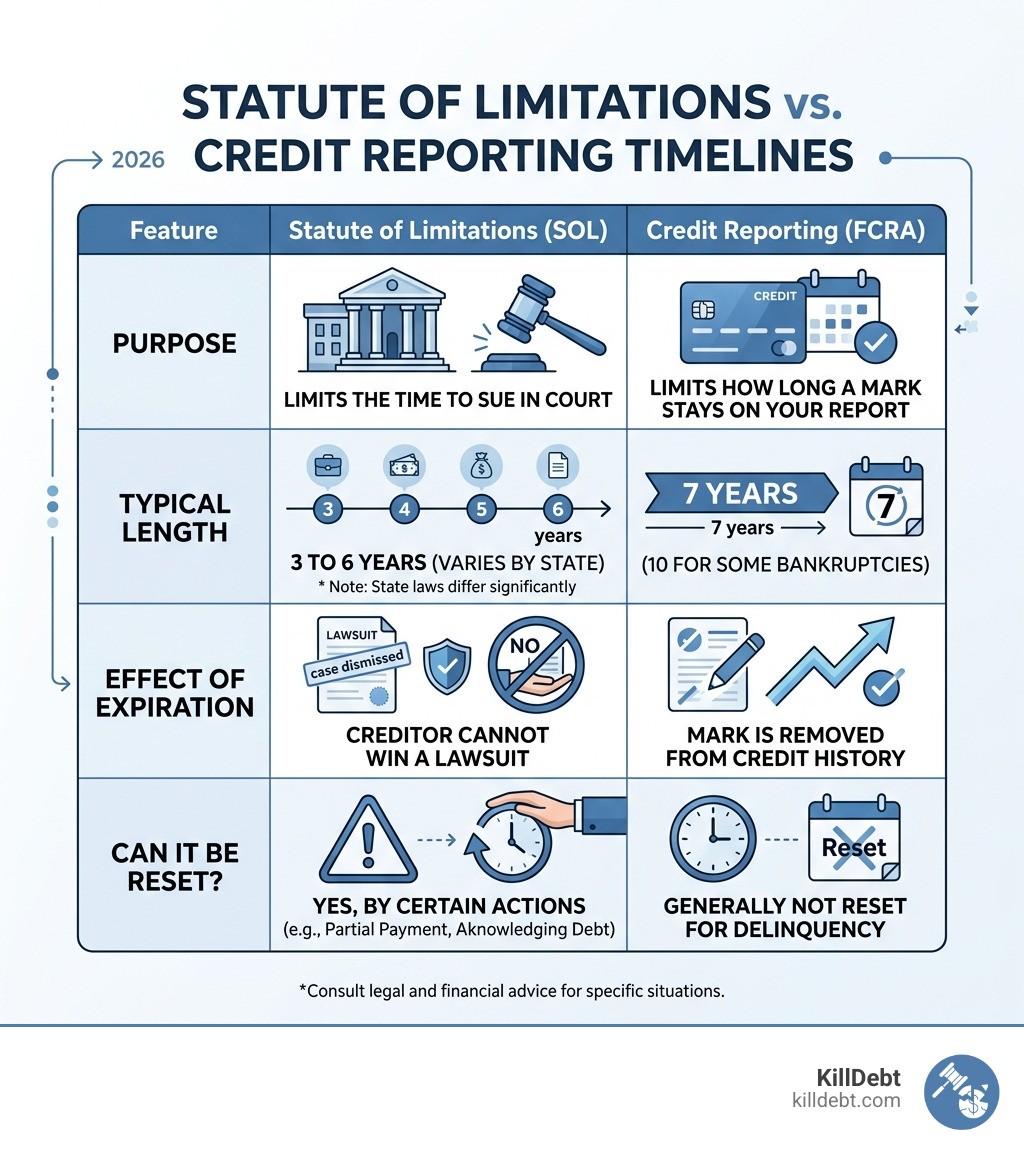

If you are sued, the statute of limitations is your shield—but you have to pick it up. Here is a comparison of how the legal clock differs from the credit reporting clock:

Feature | Statute of Limitations (SOL) | Credit Reporting (FCRA) |

|---|---|---|

Purpose | Limits the time to sue in court | Limits how long a mark stays on your report |

Typical Length | 3 to 6 years (varies by state) | 7 years (10 for some bankruptcies) |

Effect of Expiration | Creditor cannot win a lawsuit | Mark is removed from credit history |

Can be Reset? | Yes (by payment or acknowledgment) | No (starts from date of delinquency) |

To use the expired debt statute defense, you must follow these steps:

File an Answer: You must respond to the court summons within the deadline. You can use our sample answer to a debt collection lawsuit to get started.

Assert the Affirmative Defense: Explicitly state: "The Plaintiff's claim is barred by the applicable statute of limitations."

Request Validation: Force the collector to prove the date of the last payment. Often, debt buyers don't even have the original records.

Motion to Dismiss: If the debt is clearly past the limit, you can file a motion to dismiss the case entirely.

Ignoring the lawsuit is the worst thing you can do. Even if the debt is 20 years old, a collector can win a judgment if you don't show up to defend yourself. For a deep dive into the process, read our fight debt collection lawsuit complete guide.

Conclusion: Take Control of Your Legal Defense

Facing a debt collector feels like David vs. Goliath, but the law provides you with a very large stone: the statute of limitations. Whether you are in Florida or Michigan, understanding when a debt is "ancient history" can save you thousands of dollars and years of stress.

At KillDebt, we believe you shouldn't have to be a lawyer to defend your rights. That’s why we created ParkerGPT, our DIY legal defense system. It’s an AI trained on over 30 years of consumer debt law and real-world strategies from attorney Brian Parker.

We’ve recently introduced the Court Tester, an AI courtroom simulation that allows you to upload your actual lawsuit filings. Within minutes, you can "practice" arguing your motion in front of an AI judge, facing AI opposing counsel, while a private AI co-counsel whispers the best strategies in your ear. It’s the ultimate way to prepare for your day in court without the high cost of a traditional law firm.

Don't let "zombie debt" ruin your financial future. If you're wondering, "Do I need a lawyer for a debt collection lawsuit?", the answer is that with the right tools, you can often handle it yourself.

Start your defense today and put your ancient debt to rest once and for all.

Frequently Asked Questions (FAQ)

Can a collector still call me if the debt is expired?

Yes, in most states, a debt collector can still contact you to ask for payment on a time-barred debt, provided they don't threaten legal action they can't take. However, under the FDCPA, you have the right to tell them to stop. If you send a written "Cease and Desist" letter via certified mail, the collector must stop contacting you (except to tell you they are stopping or to notify you of a specific legal action). If they continue to harras you or make vague threats of a lawsuit on an expired debt, they may be violating federal law. As the Georgia Attorney General's office points out, while you may have a moral obligation to pay, your legal obligation to be sued expires with the statute.

Does the statute of limitations affect my credit report?

This is a common point of confusion. The statute of limitations and the Fair Credit Reporting Act (FCRA) are two different animals. • The SOL determines if you can be sued (usually 3-6 years). • The FCRA determines how long a negative mark stays on your credit report (7 years). A debt might be time-barred (meaning you can't be sued), but it can still show up on your credit report for a full seven years from the date of the first delinquency. Conversely, a debt might "age off" your credit report after 7 years, but if your state has a 10-year statute of limitations, you could still be sued in year eight. You can learn more about these independent timelines here.

What happens if I ignore a lawsuit for time-barred debt?

Ignoring a lawsuit is like handing a blank check to a debt collector. If you don't respond, the court will likely grant a "default judgment." This judgment is a new legal document that typically lasts much longer than the original debt (often 10 to 20 years) and can be renewed. Once a collector has a judgment, they can: • Garnish your wages (taking a percentage of your paycheck). • Level your bank account (taking everything in your savings). • Place a lien on your home. In Michigan court debt cases, for example, once a judgment is entered, the "expiration" of the original debt no longer matters. You have effectively waived your right to the expired debt statute defense.