You Just Got Served: Here's What Happens When You Are Sued by a Creditor

What happens when you are sued by a creditor follows a predictable sequence - and knowing it can make the difference between protecting yourself and losing by default:

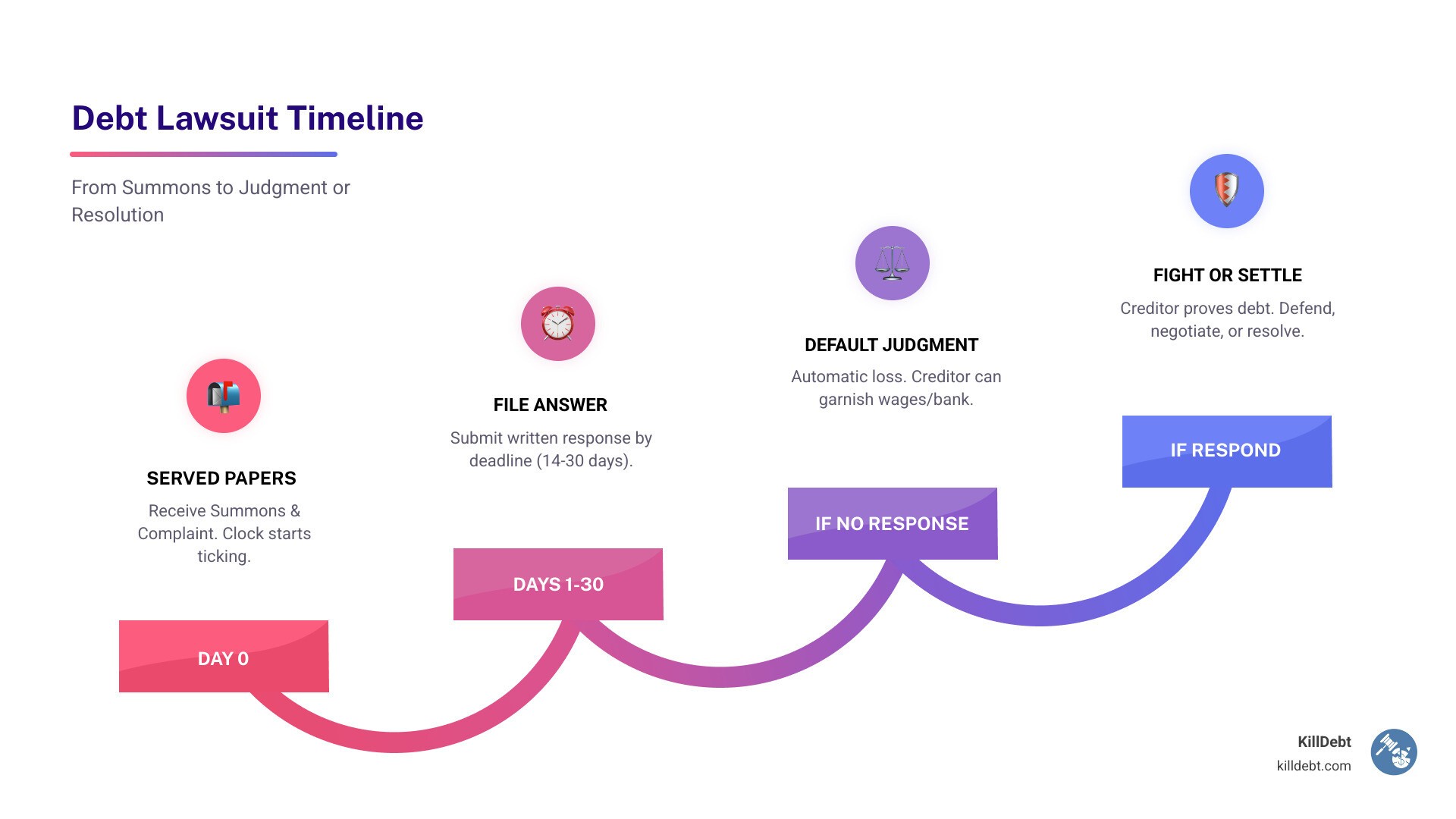

You are served with a Summons and Complaint (the official lawsuit papers)

You have a deadline - typically 14 to 30 days - to file a written response called an "Answer"

If you respond, the creditor must prove the debt is valid, the amount is correct, and they have the right to sue you

If you don't respond, the court issues a default judgment against you - automatically

With a judgment, the creditor can garnish your wages, freeze your bank accounts, or place a lien on your property

You can still fight back - through defenses, settlement negotiations, or in some cases, bankruptcy

Receiving court papers in the mail is alarming. Your hands might shake. You might set them aside, hoping the problem goes away.

It won't.

Over 70% of debt collection lawsuits end in default judgment - not because the creditor had a strong case, but because the person sued never responded. That single act of silence can hand a debt collector the legal power to take a portion of every paycheck you earn.

The good news? You have more options than you think - but only if you act before the deadline passes.

I'm Brian Parker, and for over 30 years I've been in the courtroom fighting creditors, debt buyers, and collection law firms - so I've seen what happens when you are sued by a creditor and what separates the people who protect themselves from those who lose everything by default. In the guide below, I'll walk you through every stage of the process so you know exactly what to do next.

Immediate Steps: What Happens When You Are Sued by a Creditor

When you are served with a lawsuit, it usually happens in one of two ways: a process server knocks on your door and hands you the papers, or you receive them via certified mail. Regardless of how they arrive, the clock starts ticking the second they are in your hands.

The packet you receive contains two critical documents:

The Summons: This is the court's official notice telling you that you are being sued and how long you have to respond.

The Complaint: This lists the "allegations" - the specific reasons the creditor claims you owe them money.

The very first thing you should do is stay calm and read every page. Check the names, the account numbers, and the dollar amounts. It is surprisingly common for debt buyers to sue the wrong person or for the wrong amount. If you're feeling overwhelmed, we have a sued for a debt heres exactly what to do in the first 7 days guide to help you prioritize.

You should also check the FTC's advice on debt collector lawsuits to understand your basic federal rights. We are here to help you navigate this; you can also refer to our what to do when sued by a debt collector complete first steps guide for a deeper dive into the immediate paperwork.

Understanding the Clock: Deadlines and the Answer

In the legal world, deadlines are everything. If you miss your window to respond, you lose. Period. In Florida, you generally have 20 days to file a written response. In Michigan, it's usually 21 days if you were served in person, or 28 days if you were served by mail.

Your response is called an Answer. This isn't just a letter to the creditor; it's a formal legal document filed with the court. In your Answer, you must address every numbered paragraph in the Complaint. You can:

Admit: You agree the statement is true.

Deny: You state the statement is false (this forces them to prove it).

Lack Knowledge: You don't have enough information to say if it's true or false.

Be aware that courts often charge a filing fee to submit your Answer. If you cannot afford this, you can ask the court clerk for a fee waiver application. Understanding what happens after summons is the best way to ensure you don't get tripped up by procedural red tape.

The Danger of Silence: What happens when you are sued by a creditor and ignore it?

If you ignore the lawsuit, the creditor will ask the judge for a default judgment. Because you didn't show up to defend yourself, the judge will almost always grant it.

This is exactly what debt collectors want. They know that roughly one-quarter of consumers in collections get sued, and they rely on the fact that over 70% of them won't respond. A default judgment is a "golden ticket" for a creditor. It allows them to:

Collect the original debt.

Add on years of accrued interest.

Tack on their own attorney fees and court costs.

Once that judgment is signed, the "friendly" phone calls stop, and the aggressive collection tactics begin. To see how this plays out over time, check our debt collection lawsuit timeline what happens next after youre served.

Fighting Back: Defenses and Legal Rights

Just because you are sued doesn't mean you owe what they say you owe. You have the right to raise affirmative defenses. These are legal reasons why the creditor shouldn't win, even if you did technically have a credit card at one point.

One of the most powerful defenses is the Statute of Limitations. This is the expiration date on a creditor's right to sue you.

In Michigan, the statute of limitations for most debts is 6 years.

In Florida, it is typically 5 years for written contracts and 4 years for oral contracts or "open-ended" accounts like credit cards.

If the debt is older than these limits, the case should be dismissed - but you must raise this defense in your Answer, or you waive it. For more on how to build your shield, see our debt lawsuit defense guide and our fight debt collection lawsuit complete guide.

Challenging the Debt: Standing and Documentation

When what happens when you are sued by a creditor involves a debt buyer (a company that bought your old debt from a bank for pennies), they often lack the paperwork to prove they actually own your specific account. This is called "standing."

The creditor has the burden of proof. They must show the court:

A valid contract signed by you.

A complete "chain of title" showing every time the debt was sold.

An accurate accounting of the balance.

If they can't produce these documents, you may be able to get the case dismissed. We explain the difference in strategy between fighting an original creditor vs a debt buyer here. You can also find more guidance on this from the Consumer Financial Protection Bureau (CFPB).

FDCPA Protections During a Lawsuit

The Fair Debt Collection Practices Act (FDCPA) doesn't stop just because a lawsuit started. Debt collectors are still prohibited from:

Using profane or abusive language.

Calling you before 8 am or after 9 pm.

Threatening to have you arrested (you cannot go to jail for a civil debt).

Lying about the amount you owe.

If a collector violates these rules during the litigation process, you might actually be able to sue them for damages. You can report these violations to the FTC or the CFPB.

The Consequences of Losing: Judgments and Collections

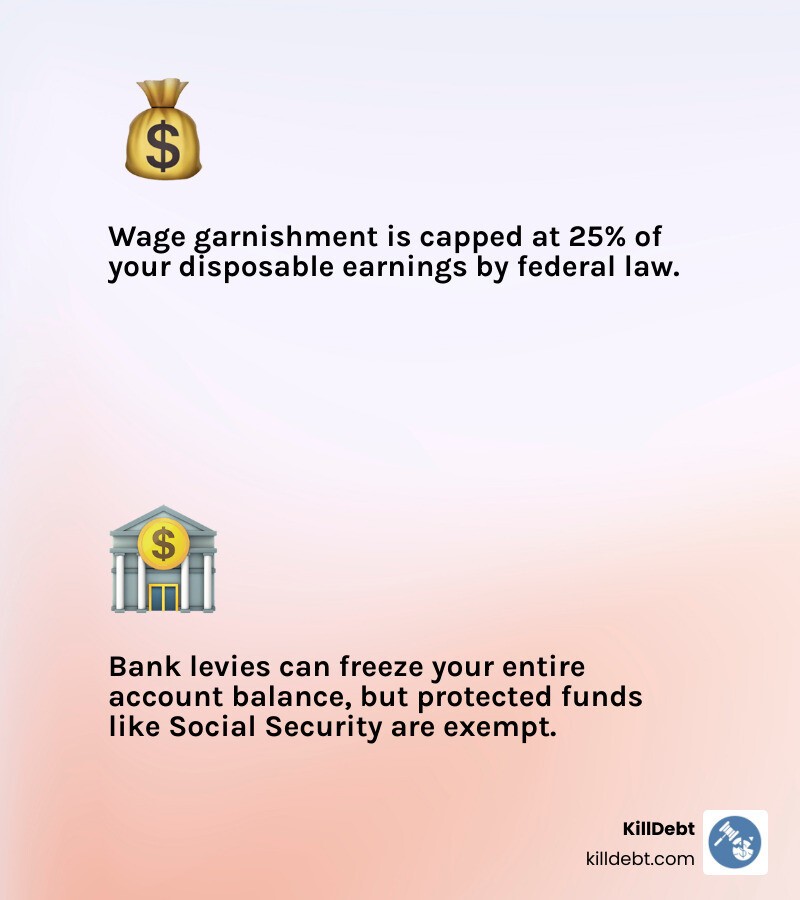

If a creditor wins a judgment against you, they become a "judgment creditor," which gives them access to much more aggressive tools than a standard collection agency.

Method | How it Works | Limits |

|---|---|---|

Wage Garnishment | Money is taken directly from your paycheck. | Federal law caps this at 25% of disposable earnings. |

Bank Levy | The creditor freezes your bank account and takes the balance. | Varies; some funds (like Social Security) are protected. |

Property Lien | A legal claim is placed on your home or car. | Prevents selling or refinancing until the debt is paid. |

To understand the full scope of what a collection agency can do in court, read can a debt collection agency take you to court.

Protected Assets: What happens when you are sued by a creditor but have no money?

If your income and assets are below a certain threshold, you might be what lawyers call "judgment proof." This doesn't mean you don't owe the debt, but it means the creditor has no legal way to collect it right now.

Certain types of income are exempt from garnishment under federal and state law:

Social Security and VA Benefits: These are almost always protected.

Homestead Exemptions: In Florida, your primary residence is famously protected from most judgment creditors.

Disability Benefits: Generally protected from seizure.

If you are facing a small claims case in Florida, The Florida Bar provides excellent resources on what property you can protect.

Resolution Strategies: Settlement, Vacating, and Bankruptcy

Even after a lawsuit is filed, it is rarely too late to settle. In fact, many creditors prefer a settlement because it's faster and cheaper than a trial.

Settlement: You offer a lump sum (often 40-60% of the total) or a payment plan in exchange for the creditor dismissing the case. If you settle, ensure you get a "Dismissal with Prejudice," which means they can never sue you for this specific debt again.

Motion to Vacate: If a default judgment was already entered against you because you were never served or had a legitimate emergency (excusable neglect), you can ask the judge to "vacate" or cancel the judgment.

Bankruptcy: Filing for bankruptcy triggers an "automatic stay." This is a powerful legal wall that immediately stops all lawsuits, garnishments, and collection efforts.

If you are wondering if you should settle or fight, check out our article on what to do if you've been sued by a debt collector.

Conclusion: Taking Control of Your Financial Future

The most important thing to remember about what happens when you are sued by a creditor is that you are not powerless. The system is designed to move quickly against those who stay silent, but it slows down significantly when you stand up and demand proof.

At KillDebt, we believe that everyone deserves a fair fight. That's why we created ParkerGPT, an AI legal defense system trained by attorney Brian Parker. Unlike generic AI, ParkerGPT understands the specific nuances of Michigan and Florida debt law. It can analyze your lawsuit papers, spot legal weaknesses, and help you draft a professional Answer for a fraction of what an attorney would charge.

We've even introduced the Court Tester - the first AI courtroom simulation. You can upload your actual case filings and "practice" your arguments against an AI judge and opposing counsel before you ever step foot in a real courtroom.

Don't let a default judgment ruin your credit and drain your bank account. Take the first step toward killing your debt today.

Learn more about how KillDebt can help you fight back.

Get started with KillDebt pricing

Important Legal Disclaimer

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments.

Frequently Asked Questions (FAQ)

How do I find low-cost legal help?

If you can't afford a private attorney, look for Legal Aid in your area. Organizations like the Legal Services Corporation (LSC) or LawHelp.org can connect you with pro bono (free) legal services if you meet their income requirements.

Can I be sued for a debt that is 10 years old?

Technically, a creditor can file a lawsuit for an old debt, but it is time-barred. If the statute of limitations has passed (6 years in Michigan, 4-5 in Florida), you have a "slam dunk" affirmative defense. However, be careful: in some cases, making a small payment or promising to pay can "restart the clock."

Do I need a lawyer for a debt collection lawsuit?

You have the right to represent yourself (pro se). While the court rules are strict, many people successfully defend themselves using the right tools and research. However, if the debt is very large or involves complex legal issues, consulting a professional is wise. Read our guide: do i need a lawyer for a debt collection lawsuit.