A Debt Validation Letter Template Can Make Collectors Back Off — Here's How

A debt validation letter template is your fastest first move when a debt collector comes calling. Before you pay anything — or panic — you have a federal legal right to demand proof that the debt is real, accurate, and legally theirs to collect.

Here's what a debt validation letter does at a glance:

What It Is | A written request demanding a debt collector prove the debt is valid |

|---|---|

Legal Basis | Fair Debt Collection Practices Act (FDCPA), 15 U.S. Code § 1692g |

When to Send | Within 30 days of first contact from the collector |

How to Send | Certified mail with return receipt requested |

What It Can Do | Force collectors to pause collection, stop calls, and prove ownership |

What Happens If They Can't Prove It | They must stop all collection activity on the debt |

Getting a letter from a debt collector is stressful. Getting a call about a debt you don't even recognize is worse.

But here's the thing most people don't know: the collector has to prove their case before you owe them anything. Under federal law, you can demand that proof in writing — and they have to stop collecting until they provide it.

That's exactly what a debt validation letter does.

According to consumer research, 68% of people who sent validation letters successfully disputed a debt — and 41% of collectors never even responded, making the debt effectively uncollectible at that point. Successful validation efforts have led to an average debt reduction of $1,230.

This guide gives you ready-to-use templates, step-by-step instructions, and everything you need to know to put the burden of proof back where it belongs — on the collector.

Understanding Your Legal Rights Under the FDCPA

When a debt collector contacts us, it can feel like they hold all the cards. However, the playing field is leveled by a powerful federal law: the Fair Debt Collection Practices Act (FDCPA). Specifically, 15 U.S. Code § 1692g is the "magic" section that gives us the right to demand validation.

Think of the FDCPA as a set of rules for a game the collectors must play. If they break the rules, they lose. One of the most important rules is the 5-day disclosure rule. Within five days of first contacting you, a debt collector must send you a written notice containing:

The exact amount of the debt.

The name of the creditor to whom the debt is owed.

A statement that unless you dispute the validity of the debt within 30 days, the debt will be assumed valid by the collector.

A statement that if you notify them in writing within that 30-day period that the debt is disputed, they will obtain verification of the debt.

If they don't provide this, they may already be in violation of federal law. This is why Debt Validation Letters: Your First Line of Defense Against Collectors are so critical. You aren't just asking for info; you are exercising a statutory right. You can find Debt Collection model forms and samples through the CFPB, but using a targeted debt validation letter template ensures you are asking for the specific evidence needed to win.

How to Use a Debt Validation Letter Template Effectively

Using a debt validation letter template isn't just about filling in the blanks; it's about shifting the burden of proof. In debt collection, "verification" and "validation" are often used interchangeably, but they mean very different things in practice.

Feature | Debt Verification | Debt Validation |

|---|---|---|

Definition | A simple confirmation that the amount matches the collector's records. | A demand for legal proof that the debt is owed and the collector has the right to sue. |

Evidence Required | Often just a printout of a balance. | Signed contracts, itemized statements, and chain of title. |

Legal Weight | Minimal; satisfies basic FDCPA notice requirements. | High; can stop a lawsuit before it starts if the collector lacks documentation. |

When we use a template, we are demanding "competent evidence." This includes proof of ownership (how did this collector get the debt?), original creditor details, and an itemized breakdown of every penny of interest and fees added since the account was closed.

Key Elements of a Debt Validation Letter Template

To make your letter ironclad, ensure your debt validation letter template includes these specific demands:

The Statement of Dispute: Explicitly state, "I am disputing the validity of this debt."

Account Numbers: Reference the collector's internal account number and the original account number if known.

Chain of Title: Demand a list of every company that has owned this debt since the original creditor. Debt buyers often buy accounts for 4% of their value and lack the paperwork to prove they actually own your specific file.

Collector Licensing: Ask for their license number to operate in your state (especially relevant in Michigan and Florida).

Demand for Documentation: Specifically request a copy of the original signed contract or agreement.

Step-by-Step Guide to Sending Your Debt Validation Letter Template

Once you've customized your debt validation letter template, the "how" is just as important as the "what."

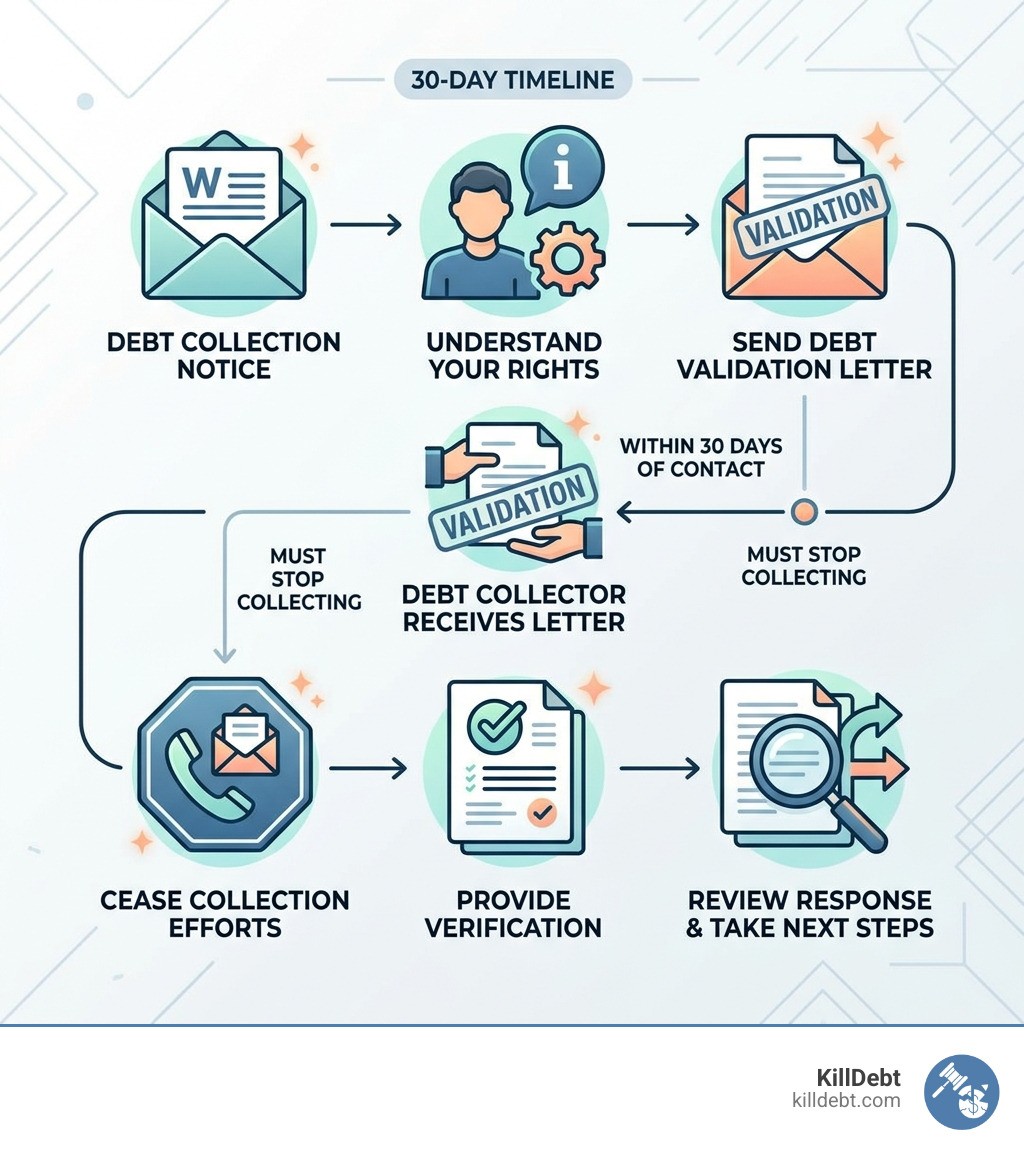

The 30-Day Window: You must send this within 30 days of the first written notice you receive. If you wait longer, the collector can legally assume the debt is valid.

Certified Mail, Return Receipt Requested: This is non-negotiable. It provides a "green card" signature that proves exactly when the collector received your letter. This starts the clock on their requirement to stop collecting until they validate.

Record Keeping: Keep a copy of the signed letter, the certified mail receipt, and the tracking information.

USPS Tracking: Monitor the delivery online so you know exactly when the 30-day "silence" period begins.

Navigating the 30-Day Rule and Statute of Limitations

The 30-day rule is your strongest shield, but what about the age of the debt? This is where the Statute of Limitations (SOL) comes in. The SOL is the time limit a creditor has to sue you for a debt. In Florida and Michigan, these timelines vary depending on the type of debt (usually 4 to 6 years).

If a debt is "time-barred," it means they can no longer successfully sue you for it. However, be extremely careful. In many states, making even a small partial payment or acknowledging that you owe the debt can "restart the clock," giving the collector a brand-new window to sue you.

This is why a debt validation letter template is safer than a phone call. By using a Sample Verification Letter, you are demanding info without admitting you owe a dime. If you receive a response, check it against a Debt collector response template - Ballard Spahr to see if they are actually following the law or just sending you "junk" documentation.

Post-Validation: What to Do if the Collector Responds (or Doesn't)

After you send your letter, one of three things usually happens:

The "Sweet Silence" (41% of cases): The collector realizes they don't have the paperwork to back up their claim and they simply stop contacting you. If they don't respond, they cannot legally continue collection efforts or report the debt to credit bureaus.

The Withdrawal: The collector sends the debt back to the original creditor or sells it to someone else. If it’s sold, the 30-day validation window resets with the new collector!

The Validation Response: They send you a pile of papers.

If they do respond, don't assume the battle is over. Review the documents carefully. Are they just computer printouts they made themselves? That isn't validation. Did they provide the original contract? If not, they may still be in violation of the FDCPA.

With a 68% success rate in disputing debts via validation, the odds are in your favor. If a collector continues to call you or fails to mark the debt as "disputed" on your credit report after receiving your letter, they are likely committing an FDCPA violation. This could entitle you to statutory damages of up to $1,000, plus actual damages and attorney fees.

Conclusion

U.S. household debt has climbed to over $17.29 trillion, and collectors are more aggressive than ever. But you don't have to be a victim of the system. By using a debt validation letter template, you are taking the first step toward a DIY legal defense that puts you back in control.

At KillDebt, we believe you shouldn't need a law degree to defend your wallet. Our system is powered by ParkerGPT, an AI trained specifically on consumer debt law and real-world strategies from attorney Brian Parker, who has over 30 years of experience. Whether you are sending your first validation letter or facing a full-blown lawsuit, we provide the tools to identify weaknesses in the collector's case.

Ready to see how a real defense works? Our brand-new Court Tester allows you to upload your filings and argue your motion in an AI simulation before you ever step foot in a real courtroom. Don't let collectors bully you into paying debts they can't prove. Take control of your debt defense with KillDebt today.

Frequently Asked Questions (FAQ)

Does sending a validation letter stop collection calls and credit reporting?

Yes—temporarily. Under the FDCPA, once a collector receives your written dispute within the 30-day window, they must cease all collection activity until they provide the requested validation. This includes phone calls, letters, and reporting the debt to credit bureaus. If the debt is already on your credit report, they must mark it as "disputed."

Can I still dispute the debt after receiving validation?

Absolutely. Receiving "validation" doesn't mean you automatically owe the money. You can still dispute based on identity theft, unauthorized charges, or simple accounting errors. If the records they send are inaccurate, you can use that as evidence in a court case or a follow-up dispute with the credit bureaus.

What are common mistakes to avoid when sending a validation letter?

The biggest mistake is admitting liability. Never say "I know I owe this, but..." or "I can't pay this right now." Your letter should remain neutral: "I am requesting validation of this alleged debt." Other mistakes include missing the 30-day deadline, using aggressive or "pro-se" legal jargon that makes no sense, and failing to use trackable mail.