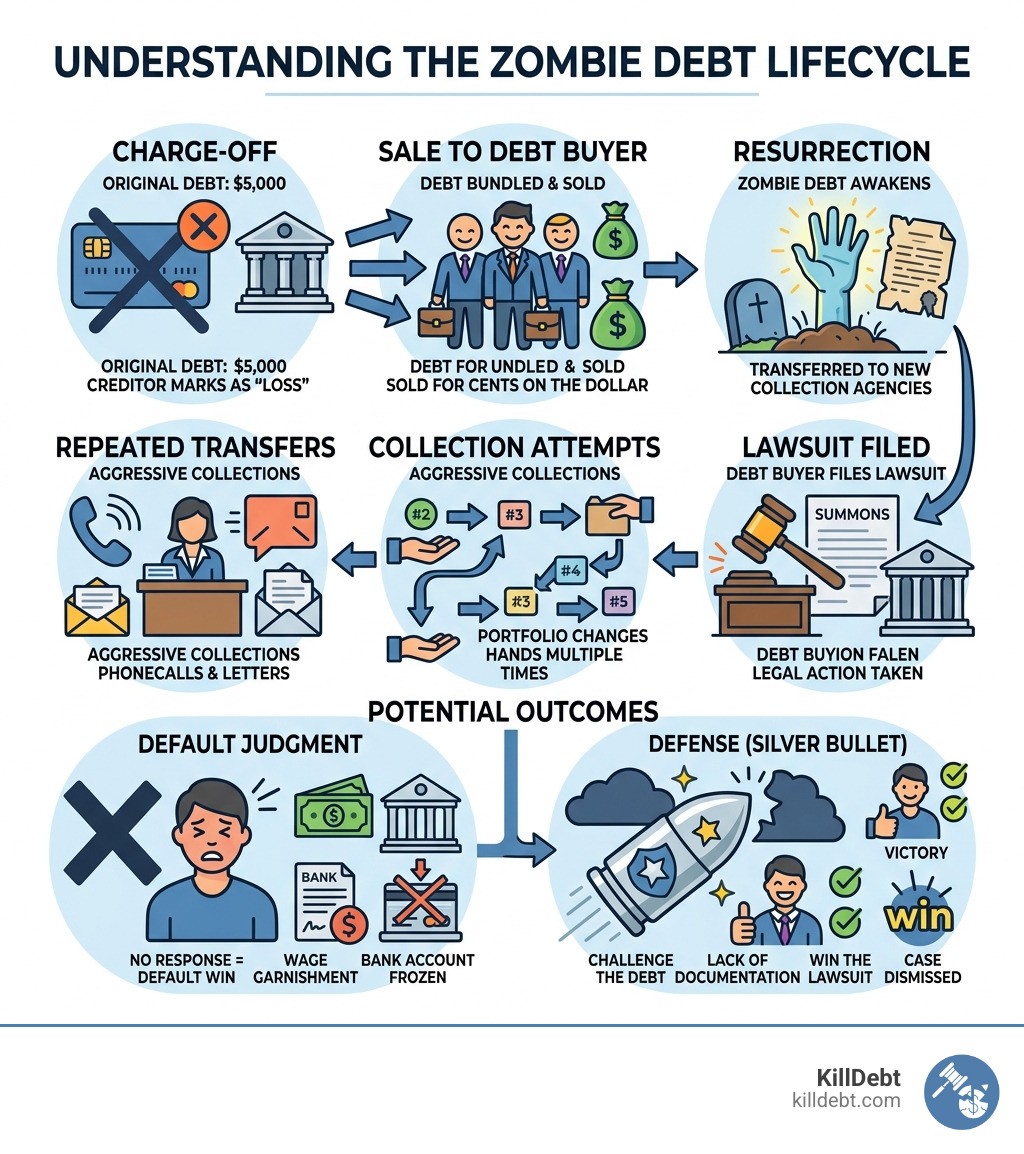

Understanding the Resurrection of Zombie Debt

To understand how win zombie lawsuit tactics, we first have to look at why these debts "rise from the grave." In the financial world, when you stop paying a credit card, medical bill, or mortgage, the original creditor eventually "charges off" the debt. This doesn't mean the debt is gone; it just means the bank has moved it from the "asset" column to the "loss" column for tax purposes.

These losses are then bundled into massive portfolios and sold to third-party debt buyers. These buyers—major players in a $15 billion industry—purchase your personal information for fractions of a cent on the dollar. Because they bought the debt so cheaply, even a small settlement represents a massive profit for them.

The problem? These portfolios often change hands five or six times. By the time a debt buyer sues you, they might only have a spreadsheet with your name, an account number, and a balance. They often lack the original contract you signed or a complete "chain of title" proving they actually own the right to sue you. This lack of documentation is the "silver bullet" we use to defeat them.

How Win Zombie Lawsuit: Your Immediate Legal Defense Strategy

If you have been served with a Summons and Complaint, the clock is ticking. The absolute worst thing you can do is ignore it. If you do nothing, the debt buyer wins by default. A default judgment allows them to garnish your wages or freeze your bank accounts—turning a "zombie" debt into a very real financial nightmare.

In Florida and Michigan, the time to respond debt collection lawsuit is generally 20 to 21 days. You must file a written "Answer" with the court. In this document, you should generally deny the allegations. Why? Because it is the plaintiff's job to prove their case; it is not your job to help them.

One of the most effective tools in your arsenal is a solid counter-affidavit. This is a sworn statement where you challenge the accuracy of the debt buyer's claims. If they provide a "robosigned" affidavit (a document signed by someone who hasn't actually reviewed your specific file), your counter-affidavit can strip that evidence of its power.

Using the FDCPA to learn how win zombie lawsuit

The Fair Debt Collection Practices Act (FDCPA) is a federal law that protects you from abusive collection tactics. Under the FDCPA, you have the right to demand debt validation. If a collector contacts you, you have 30 days to send a validation letter.

When you demand validation, the collector must provide:

The amount of the debt.

The name of the original creditor.

Proof that they have the legal right to collect it.

If they can't provide this, they must stop collection efforts. Many people find that zombie debt: what is it and how to avoid bringing it back from the dead starts with this simple demand. If they sue you without having this proof, they may be violating federal law, potentially giving you the right to sue them for damages.

Challenging documentation to how win zombie lawsuit

To win, a debt buyer must prove they own the debt. This is called "standing." Because these debts are sold in bulk, the "proof" is often just a generic "Bill of Sale" that doesn't even mention your name.

We always check for:

The Chain of Ownership: Did Company A sell to Company B, who then sold to the Plaintiff? If there is a "break" in this chain, they lose.

The Original Agreement: Do they have the actual contract you signed? Often, they don't.

The Account Stated: Can they show a line-by-line breakdown of how the balance reached the amount they are claiming?

Understanding who is suing me: original creditor vs. debt buyer explained is vital. An original creditor (like a big bank) usually has the paperwork. A debt buyer usually does not. If you force them to produce the original signed bill, many zombie debt buyers will simply dismiss the case because they know they can't find it.

Powerful Affirmative Defenses to Kill the Case

Affirmative defenses are legal reasons why the debt buyer should lose, even if the debt was originally yours. When filing a counter-affidavit when answering a debt collection lawsuit, you must list these defenses specifically.

1. Statute of Limitations This is the most common way to win. Every state has a time limit for how long a creditor has to sue you. In Florida, the limit for most consumer debt is 5 years. In Michigan, it is 6 years. If the last time you made a payment was 10 years ago, the debt is "time-barred." The collector can still ask you to pay, but they cannot legally win a lawsuit.

2. Laches Laches is an "equitable" defense. It basically says that the creditor waited so long to sue you that it's unfair to let them proceed now. Perhaps your records were destroyed in a move, or the original bank went out of business. If their delay has made it impossible for you to defend yourself, laches can kill the case.

3. Unclean Hands If the debt buyer has engaged in unethical or illegal behavior—like charging illegal interest rates or misrepresenting the debt—you can argue they have "unclean hands" and should be barred from recovery.

4. Debt Acceleration In cases like student loans or mortgages, the "clock" for the statute of limitations often starts when the debt is "accelerated" (when the lender demands the full balance). As seen in recent court victories, if a debt buyer tries to sue six years after a previous owner sent an acceleration letter, the case can be tossed. Knowing that zombie debt: don't let it rise to bite you often means looking back at old correspondence to find that acceleration date.

Fighting Zombie Mortgages and Foreclosure Attempts

One of the scariest forms of undead debt is the zombie mortgage. These are often second mortgages or Home Equity Lines of Credit (HELOCs) from the mid-2000s. During the housing crash, many homeowners thought these were "wiped out" or forgiven. However, as home values have risen, debt buyers are now digging up these old liens and threatening foreclosure.

In Florida, we see many cases where homeowners are suddenly hit with a $200,000 bill for a $50,000 HELOC they haven't heard about in 15 years. Because the first mortgage is now paid down and the house is worth more, the debt buyer sees an opportunity to "equity strip" the home.

You can fight back using:

TILA/RESPA Violations: Federal laws require lenders to send you monthly statements and notices when your loan is transferred. If they went silent for a decade, they may have violated the Truth in Lending Act (TILA).

Statute of Limitations: In some states, like Florida, there are strict limits on how long a lender has to foreclose after a default.

Lack of Standing: Just like credit cards, mortgage debt buyers often lack the original "Note" or a proper assignment of mortgage.

There are at least 15 ways to fight foreclosure of zombie second mortgages, ranging from challenging the interest calculations to filing for bankruptcy. If you are facing this, you should immediately research zombie mortgage debt to understand your rights before they take your home.

Conclusion: Taking Control of Your Financial Future

Facing a zombie lawsuit feels like a nightmare, but remember: you are the one with the power. These debt buyers rely on your fear and your silence. They expect you to ignore the summons so they can win by default. When you stand up and demand proof, you change the entire game.

At KillDebt, we believe that everyone deserves a fair fight. That’s why we created ParkerGPT, an AI legal defense system trained on the strategies of Brian Parker, an attorney with over 30 years of experience in consumer debt law. Generic AI might give you a basic definition, but ParkerGPT analyzes your specific lawsuit documents to find the "cracks" in the debt buyer's case.

We’ve also introduced the Court Tester, an AI courtroom simulation. You can upload your actual court filings and practice your arguments against an AI opposing counsel. You’ll see exactly how a judge might react to your defenses before you ever step foot in a real courtroom.

Don't let the "undead" ruin your credit or take your home. You have the rights, you have the defenses, and now you have the tools. Start your defense today and put these zombie debts back in the grave where they belong.

Frequently Asked Questions (FAQ)

Can I ignore a zombie debt summons?

Absolutely not. Ignoring a summons is a guaranteed way to lose. If you don't respond, the court will enter a default judgment. Once they have a judgment, the debt collector can: • Garnish up to 25% of your paycheck. • Freeze your bank accounts and take the balance. • Place a lien on your property. Understanding the debt collection lawsuit timeline: what happens next after you're served is crucial. You usually have about three weeks to act. Use that time to file an Answer and force the collector to prove their case.

Does making a small payment restart the statute of limitations?

Does making a small payment restart the statute of limitations? Yes—and this is a dangerous trap. Debt collectors will often try to convince you to make a "good faith payment" of just $20. Do not do this! In many states, including Florida and Michigan, making a single payment can "toll" or restart the statute of limitations clock. This effectively brings a "dead" debt back to life, giving the collector a brand new 5 or 6-year window to sue you. Before you send a dime, you should beware of zombie debt - Florida bankruptcy lawyer advice: check the age of the debt first. If it's already expired, paying anything is a massive mistake.

Can bankruptcy discharge a zombie mortgage?

Yes. If you file for Chapter 7 bankruptcy, your personal liability for the debt is usually discharged. However, the lien on the house might remain. In Chapter 13 bankruptcy, you may be able to "strip" a junior lien (like a zombie second mortgage) if your home is worth less than what you owe on the first mortgage. This is a complex strategy, but it's a powerful way to kill a zombie lien for good. If you're overwhelmed, check out our what to do when sued by a debt collector: complete first steps guide.