When a Debt Collector Sues You, Do They Actually Own Your Debt?

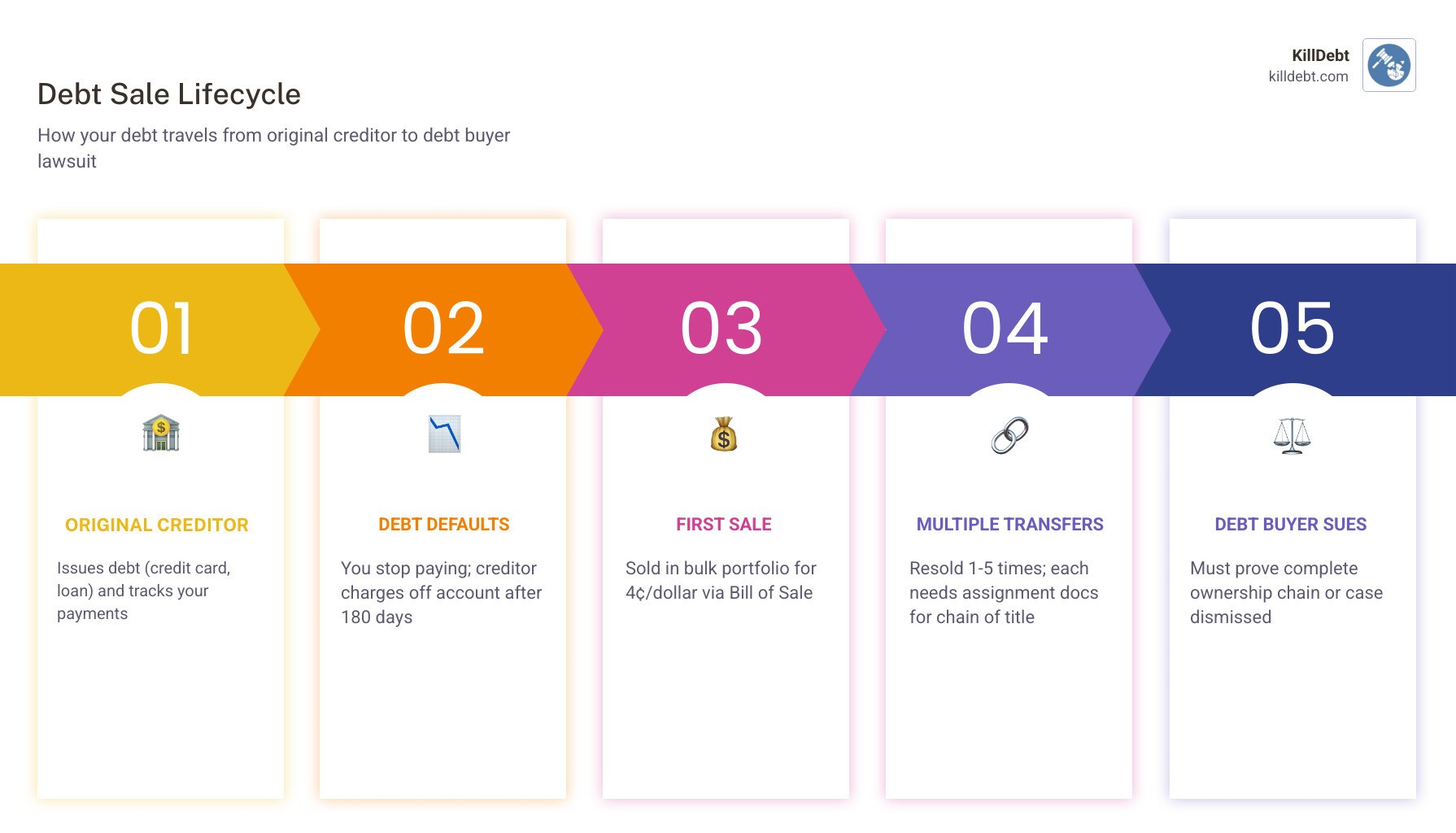

A chain of assignment debt collector is a third-party company that purchased your debt from the original creditor — or from another buyer who purchased it first — and must prove every step of that ownership transfer before they can legally collect from you.

Here's the quick answer:

What it means: Your debt was sold (assigned) one or more times. Each sale creates a "link" in the chain.

Why it matters: A debt buyer can only sue you if they can prove they own your specific account — not just a bulk portfolio of accounts.

What they must show: A complete paper trail from the original creditor to themselves, with documents identifying your account at each transfer.

Your right: You can demand proof of this chain. If they can't provide it, their case may be dismissed.

Imagine getting a court summons from a company you've never heard of. They claim you owe money — but the name on the paperwork isn't your bank, your credit card company, or anyone you ever signed a contract with.

This happens millions of times every year.

What most people don't realize is that the company suing them may have bought your debt for as little as 4 cents on the dollar — often as part of a massive bundle of thousands of accounts. Along the way, critical paperwork identifying your specific account can get lost, incomplete, or never transferred at all.

That's where the chain of assignment becomes your most powerful defense tool.

Billions of dollars are collected annually on debts where the ownership record is broken, disputed, or simply unverifiable. Courts in multiple states are now requiring debt buyers to prove far more than they used to.

You have more rights here than you probably think.

Understanding the Chain of Assignment Debt Collector Requirements

When we talk about a "chain of title" in a debt collection case, we aren't talking about a physical chain (though it might feel like you're being dragged by one). We are talking about the documented history of who has owned the debt from the moment you first swiped that credit card until the moment a debt buyer decided to sue you.

In legal terms, a debt is a "chose in action." This is just fancy lawyer-speak for an intangible right to sue someone for money. Because you can't hold a debt in your hand like a gold bar, the only way to prove you own it is through a paper trail. This is where the concept of Assignment: Involves Transfer of Rights to Collect Outstanding Debts | Anderson Aylwin Begg & Co. comes into play.

The Original Creditor vs. The Debt Buyer

There is a massive difference between being sued by the bank that gave you the loan and a company that bought the loan later. We often explain this in our guide on Who is Suing Me? Original Creditor vs. Debt Buyer Explained.

If Capital One sues you, they don't need a chain of assignment because they are the "original creditor." They were there at the beginning. But if a company like Midland Funding or Portfolio Recovery Associates sues you, they are a chain of assignment debt collector. They must prove they have "standing to sue."

Standing is the legal right to initiate a lawsuit. To have standing, a debt buyer must show an "absolute assignment" — a total transfer of rights — in writing. If there is a single gap in that chain — say, the debt went from Bank A to Buyer B, and then Buyer C sues you without proving the transfer from B to C — the chain is broken. No chain, no standing. No standing, no lawsuit.

Critical Documents Needed to Prove Ownership

If a debt buyer wants to win in court, they can't just point at you and say, "They owe us money!" They need receipts. Specifically, they need a series of documents that link them back to your original contract.

The most common documents required include:

The Bill of Sale: This is the primary document showing that a transfer happened. However, most debt buyers use a "Master Bill of Sale." This document usually says something like, "Bank A sells 50,000 accounts to Buyer B." It rarely lists your name or account number on the face of the document.

The Assignment Agreement: This outlines the terms of the transfer. It’s the "contract for the contract."

Affidavits of Sale: These are sworn statements from employees of the companies involved. A common issue here is that these employees often have no "personal knowledge" of how the original bank kept its records, which can make their testimony "hearsay."

As we discuss in Credit Card Debt Collection: How Banks Sell Your Account, these documents are often generic. When a consumer asks, Q: What docs must a debt collector provide to validate assignment of ..., the answer is clear: they must provide enough evidence to identify your specific account as part of that mass sale.

The Role of the Account Schedule in a Chain of Assignment Debt Collector Case

The "Account Schedule" is the most important document you’ve probably never seen. When a bank sells 10,000 accounts, they attach a digital file (the schedule) that lists the names, social security numbers, and balances of every person in that bundle.

Without this schedule, a Bill of Sale is just a piece of paper. It proves a sale happened, but it doesn't prove your debt was part of it. Debt buyers hate showing these schedules because they often contain private information of thousands of other people, or worse, they don't actually have the specific data for your account.

In the modern era, debt buyers are increasingly relying on electronic records and third-party registries like the Global Debt Registry to track these transfers. While courts are becoming more comfortable with digital records, the 1.4.7.4 Chain of Title | Fair Debt Collection | NCLC Digital Library still requires that these records meet the "business records exception" to be admissible in court. This means the collector must prove the records were made at or near the time of the event by someone with knowledge of the transaction.

Common Defenses Against Incomplete Assignment Chains

If you are being sued, your job isn't necessarily to prove you don't owe the money. Your job is to force the chain of assignment debt collector to prove they have the right to collect it.

Feature | Original Creditor | Debt Buyer |

|---|---|---|

Proof of Ownership | Direct (Original Contract) | Indirect (Chain of Assignments) |

Document Quality | High (Original Statements) | Variable (Summaries/Affidavits) |

Standing Challenge | Difficult | Highly Effective |

Hearsay Risk | Low | High |

Missing Links and Generic Paperwork

The most common weakness is a "missing link." If a debt was sold from Chase to Buyer A, then to Buyer B, then to Buyer C, Buyer C must produce three separate Bills of Sale. If they only have the last one, they lose.

Another defense is challenging "hearsay." If a debt buyer brings an affidavit from their own employee to "verify" the records of the original bank, you can object. That employee doesn't work for the bank; they have no idea how the bank's computers work or if the bank's data entry was accurate. This is a common reason why Why Debt Collectors Buy Old Debts for so little — they know the records are often a mess.

If the collector can't provide the paperwork, you can file a Motion to Dismiss for lack of standing or a Motion for Summary Judgment. As noted in What Happens When a Debt Buyer Can't Prove Chain of Title, if the court finds the evidence is insufficient, the case is over.

State-Specific Rules for a Chain of Assignment Debt Collector

Because KillDebt focuses on Florida and Michigan, we need to look at the specific hurdles collectors face in these states.

Florida Proof Requirements

In Florida, the law is quite protective of consumers regarding debt assignments. Under The 2025 Florida Statutes - Online Sunshine, specifically Florida Statute 559.715, an assignee (the debt buyer) must give the debtor written notice of such assignment within 30 days of the assignment.

Furthermore, Florida courts generally require the debt buyer to attach the assignment documents to the complaint itself. If they don't, the complaint might be "facially deficient," meaning it can be kicked out of court before you even argue the facts.

Michigan Proof Requirements

Michigan has also stepped up its game. Recent changes in Michigan Courts Increase Requirements of Proof of Assignment in ... show that judges are no longer accepting "trust me" as a valid legal argument. Debt buyers in Michigan must now provide more granular evidence of the transfer. If the paperwork is generic or the affidavit is "robo-signed" (signed by a machine or someone who didn't read it), Michigan courts are increasingly likely to dismiss the case.

How to Dispute a Debt and Demand Proof

You don't have to wait for a lawsuit to demand proof of the chain of assignment. In fact, you should start the moment you get that first "validation notice."

Under the Fair Debt Collection Practices Act (FDCPA), a collector must send you a notice within five days of their first contact. This notice tells you how much you owe and who the original creditor was. You then have a 30-day window to dispute the debt in writing.

When you dispute, you aren't just saying "I don't owe this." You are demanding verification. For a chain of assignment debt collector, this means they should provide:

The name of the original creditor.

The date of the last payment.

A copy of the chain of assignment documents.

We break down these rights further in our guide: What is a Debt Collector Under the FDCPA? Your Rights Explained.

If they sue you, the "discovery" phase begins. This is your chance to demand:

Interrogatories: Written questions they must answer under oath (e.g., "State the date of every transfer of this account").

Request for Production of Documents: Demanding the actual Account Schedule and every Bill of Sale in the chain.

Conclusion: Take Control of Your Defense

The chain of assignment debt collector relies on one thing above all else: your silence. They bank on the fact that 90% of people sued for debt never show up to court. When you show up and demand a valid chain of title, you change the math of the entire case.

At KillDebt, we believe you shouldn't need a law degree to defend your rights. That’s why we created ParkerGPT, an AI legal defense system trained specifically on consumer debt law and real-world strategies developed over 30 years by attorney Brian Parker.

Whether you are in Florida or Michigan, our platform analyzes your lawsuit documents, identifies the exact "missing links" in the collector's chain, and generates court-ready responses.

Want to see how you'd do in front of a judge? Our brand-new Court Tester tool is an AI courtroom simulation. You can upload your actual filings and "practice" your arguments against an AI opposing counsel, with a private AI co-counsel (trained by Brian Parker) whispering winning strategies in your ear.

Don't let a broken chain pull you down. Visit KillDebt.com today and start building your defense.

Frequently Asked Questions (FAQ)

What happens if a debt buyer cannot prove the chain of title in court?

If the debt buyer fails to prove the chain of title, they lack "standing." This usually results in a case dismissal. Depending on the judge, the case might be dismissed "with prejudice" (meaning they can never sue you again for this debt) or "without prejudice" (meaning they can try again if they find the paperwork). Even a dismissal without prejudice is a huge win, as it gives you massive leverage to settle for pennies or forces the buyer to give up because the cost of finding the paperwork exceeds the value of the debt.

Should I respond to a lawsuit even if I believe the debt is valid?

Yes! Absolutely! Even if you remember having the credit card, that doesn't mean the company suing you actually owns it. If you ignore the lawsuit, the debt buyer gets a "default judgment." This is like winning a game because the other team didn't show up. With a default judgment, they can garnish your wages or put a levy on your bank account in Florida and Michigan. By responding, you force them to prove their case, which they often cannot do.

Can debt buyers rely on generic affidavits to prove they own my debt?

They certainly try. This is often referred to as "robo-signing." However, as discussed in DEBT BUYERS MAKING YOUR CASE IN COURT, these affidavits are often vulnerable to hearsay objections. To be valid, the person signing the affidavit must have personal knowledge of how the records were created and maintained. Most debt buyer employees have never seen the original bank’s computer system, making their "knowledge" second-hand at best.