What is a Debt Validation Letter and Why is it Important?

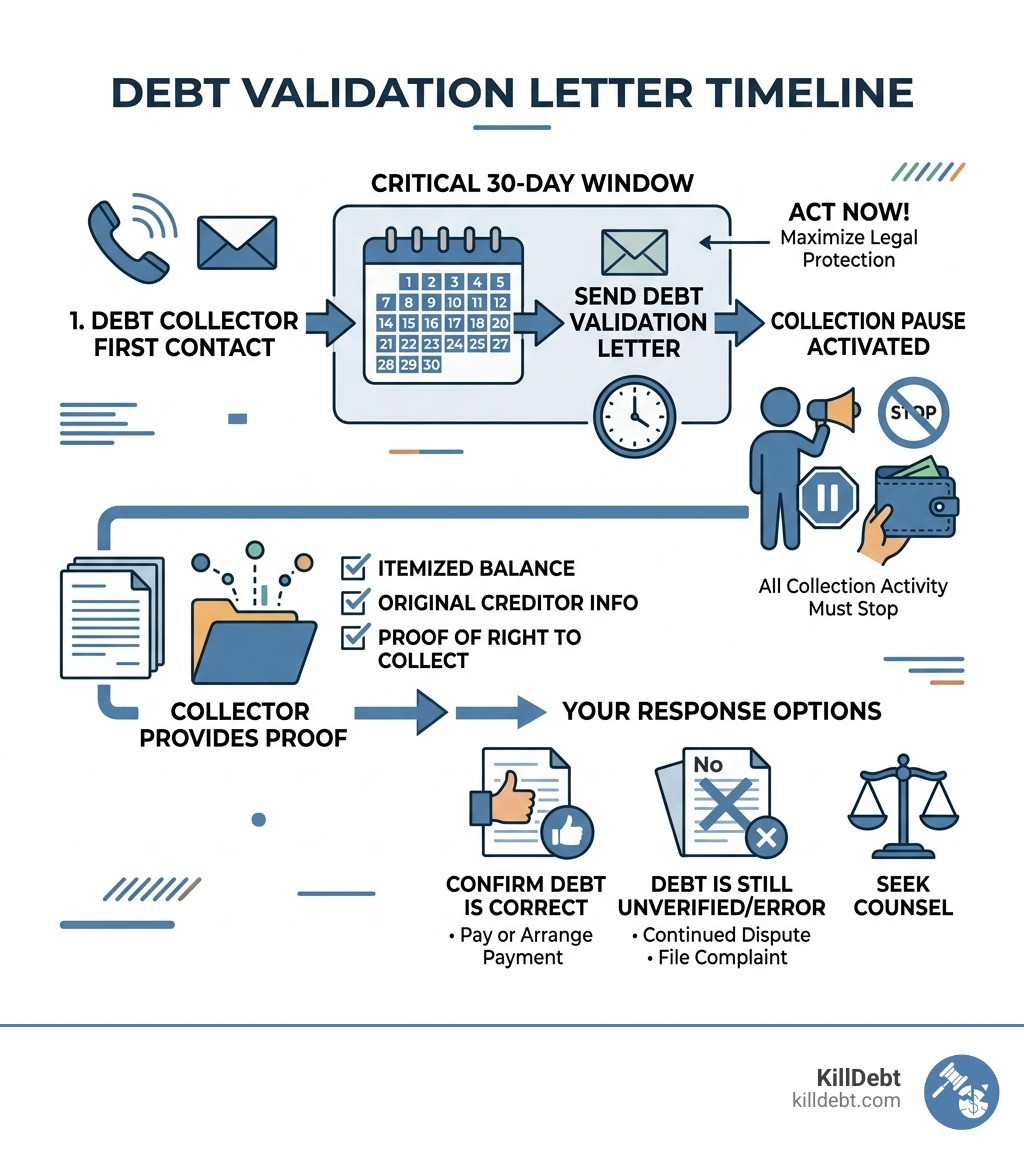

An example debt validation letter is a written request you send to a debt collector demanding they prove the debt is real, accurate, and legally theirs to collect. Here's what it does at a glance:

What a debt validation letter does:

Forces the collector to pause collection activity until they provide proof

Requires them to show the amount owed, the original creditor, and their right to collect

Protects you under the Fair Debt Collection Practices Act (FDCPA)

Must be sent within 30 days of first contact for the strongest legal protection

If you just need a quick template, here's the core structure:

Your name, address, and the date

The collector's name and address

A clear statement disputing the debt

A request for proof: original creditor, account number, itemized balance, and collector licensing

Sent via certified mail with return receipt

Getting a letter from a debt collector is stressful. You might not even recognize the debt. You're not alone — according to the Consumer Financial Protection Bureau (CFPB), 53% of consumers who receive debt collection letters don't believe they actually owe the debt.

That's more than half of all people contacted.

The problem is, most people don't know they have the right to demand proof before paying anything. Under federal law, you can put the burden of proof back on the collector — in writing — and they have to stop collection activity until they respond.

That's exactly what a debt validation letter does.

At its core, a debt validation letter is your shield. When a third-party collector contacts you, they are often working with data purchased for pennies on the dollar. This data is frequently incomplete, outdated, or flat-out wrong. By using an example debt validation letter, you are exercising your rights under the Fair Debt Collection Practices Act (FDCPA), specifically Section 809.

The FDCPA is a federal law designed to protect you from abusive, deceptive, and unfair debt collection practices. One of the most powerful tools this law gives us is the right to dispute a debt. When you send this letter, you shift the "burden of proof." Instead of you having to prove you don't owe the money, the collector must prove that you do.

Why is this so important? Because the moment the collector receives your written dispute, they must cease all collection activities. This means the phone calls must stop, the letters must stop, and they cannot report the debt to credit bureaus as a "verified" account until they provide the proof you requested. As we discuss in our guide on Debt Validation Letters: Your First Line of Defense Against Collectors, this pause gives you the breathing room needed to evaluate the situation without being hounded.

If the collector cannot provide the required documentation—which happens more often than you’d think—they cannot legally continue to collect from you. You can find more technical details on what constitutes a valid request in this Sample Verification Letter from the NCLC Digital Library.

How to Write an Effective Example Debt Validation Letter

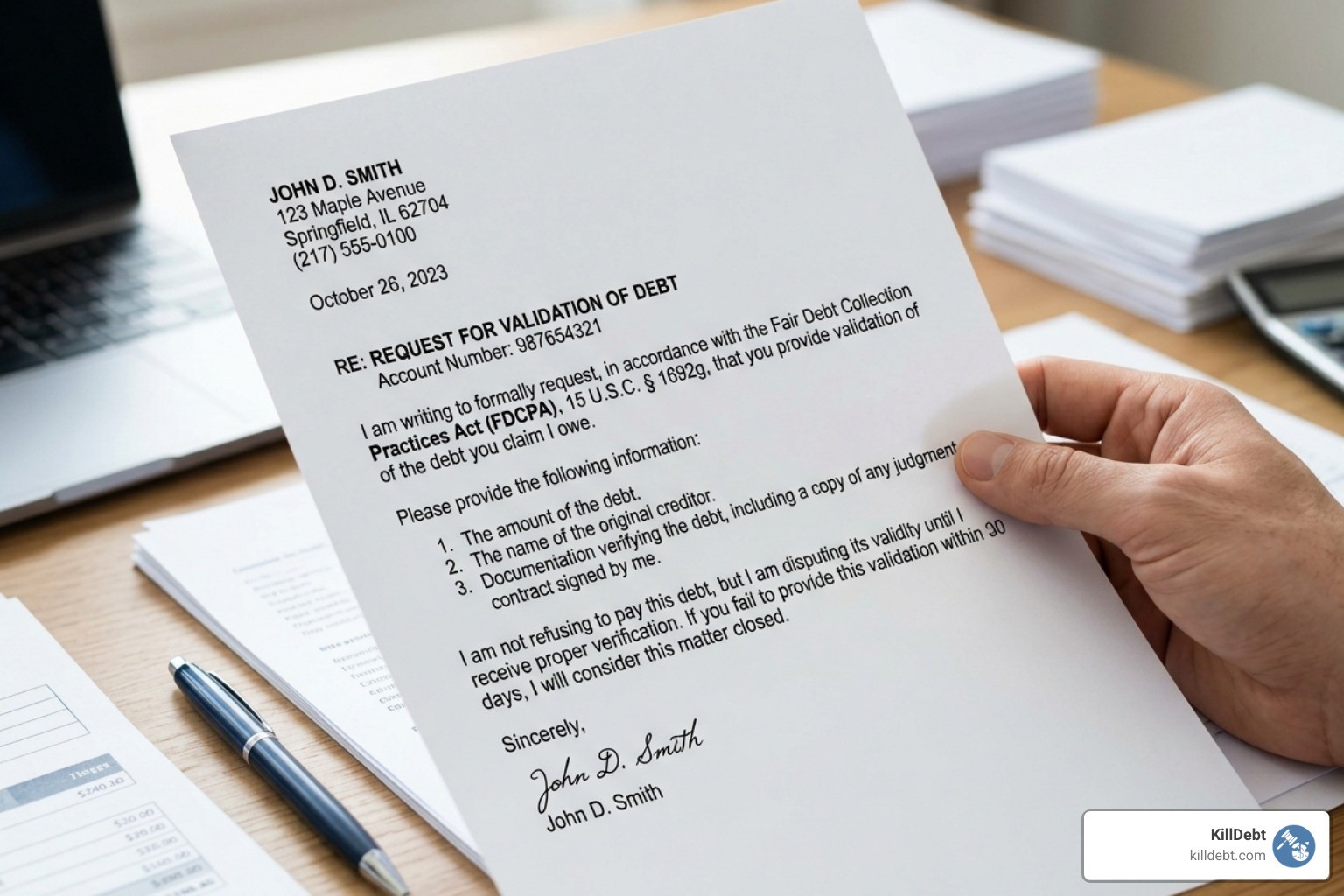

Writing this letter doesn't require a law degree, but it does require precision. You want to be firm, clear, and avoid saying anything that could be interpreted as admitting you owe the debt. We’ve seen collectors try to use a consumer's own words against them in court, so "I'm not sure if I owe this" is much safer than "I can't pay this right now."

When drafting your letter, your goal is to make the collector work. You aren't just asking if the debt exists; you are asking for the "receipts."

In Michigan and Florida, where we focus our efforts, collectors must adhere strictly to these federal guidelines. If they are an out-of-state agency, you should also demand proof that they are licensed to collect debt in your specific state.

Essential Components of an Example Debt Validation Letter

To ensure your letter carries legal weight, it must include several key elements:

Identifying Information: Include your name, address, and the collector’s internal account number (usually found on the notice they sent you).

Explicit Dispute Statement: Clearly state, "I am disputing the validity of this debt." You don't need to provide a long story about why; the statement itself is enough to trigger your rights.

Request for Specific Proof: Don't just ask for a bill. Demand an itemized breakdown of the balance, including original principal, interest, and any fees added.

Original Creditor Information: Ask for the name and address of the original creditor.

Collector Authority: Request proof that the agency has the legal right to collect this debt (such as a copy of the assignment or contract from the original creditor).

Statute of Limitations: Ask for the date of the last payment or activity on the account. This helps determine if the debt is "time-barred," meaning it's too old for them to legally sue you over.

If you are currently Struggling with Debt Collectors, getting these details is the first step toward taking back control.

Sending Your Letter and Managing the 30-Day Window

Timing is everything. Federal law gives you a 30-day "validation period" starting from the day you receive the initial notice from the collector. If you send your letter within this window, your legal protections are at their peak. The collector must stop all activity until they validate.

If you miss the 30-day window, you can still send the letter, but the collector isn't legally required to stop collecting while they process it. However, it’s still worth sending to create a paper trail.

Crucial Tip: Use Certified Mail Never send a debt validation letter via standard mail. Always use USPS Certified Mail with a Return Receipt Requested.

Why? Because debt collectors have a "habit" of losing mail. If you end up in court, that green "return receipt" card with their signature on it is your "get out of jail free" card. It proves exactly when they received your dispute.

Validation vs. Verification: What’s the Difference?

While people often use these terms interchangeably, there is a technical difference in debt defense:

Feature | Debt Validation | Debt Verification |

|---|---|---|

Source | Sent by the Consumer to the Collector | Sent by the Collector to the Consumer |

Purpose | To demand proof of the debt's legitimacy | To provide the "proof" (often just a statement) |

Legal Basis | FDCPA Section 809(b) | FDCPA Section 809(a) |

Deadline | Within 30 days of initial contact | Within 5 days of initial contact (Notice) |

What Happens After You Send the Letter?

Once the collector receives your example debt validation letter, they have a few choices:

They provide validation: They send you documentation. You must then review it carefully. Does the math add up? Is the original creditor correct? Is the debt past the statute of limitations?

They stop collecting: Many times, if the collector realizes they don't have the paperwork to back up the claim, they will simply stop calling and move on to an easier target.

They sell the debt: Sometimes they sell the "uncollectible" debt to another agency. If this happens, the new agency must also provide you with a 30-day window to dispute.

If the collector responds with inadequate validation—like just a printout of their own internal screen—that is often not enough to satisfy the law. If they continue to harrass you without providing real proof, they may be committing an FDCPA violation. You could be entitled to $1,000 in statutory damages, plus actual damages and attorney fees.

If you find yourself in a situation where the collector ignores your letter and moves straight to a lawsuit, don't panic. Check out our What to Do When Sued by a Debt Collector: Complete First Steps Guide for an immediate action plan.

Conclusion

Sending an example debt validation letter is the single most effective way to stand up for yourself when a debt collector comes knocking. It costs less than five dollars in postage, but it can save you thousands in illegitimate or unproven debts.

At KillDebt, we believe you shouldn't have to be a lawyer to defend your wallet. We provide a DIY legal defense system powered by ParkerGPT, our specialized AI. ParkerGPT isn't just a chatbot; it's trained on over 30 years of real-world court strategies from attorney Brian Parker. It analyzes your specific situation, identifies the collector's weaknesses, and helps you generate the documents you need to win.

We’ve even introduced the Court Tester, an AI courtroom simulation. You can upload your actual filings and "practice" your motion in front of an AI judge, with a private AI co-counsel whispering strategy only you can see. Whether you're sending your first validation letter or preparing for a day in court, we are here to provide the tools you need at a fraction of the cost of a traditional attorney.

Don't let debt collectors bully you into paying money they can't prove you owe. Take the first step today and visit KillDebt.com to arm yourself with the best defense technology available.

Frequently Asked Questions (FAQ)

Can I send a debt validation letter after 30 days?

Yes, you can. While you lose the automatic "stop collection" protection that comes with the initial 30-day window, sending the letter still forces the collector to realize you are informed. It also prevents them from claiming in court that the debt was "undisputed." Even after 30 days, the burden of proof in a lawsuit still lies with the collector.

Does a validation request stop a lawsuit?

If a lawsuit has already been filed, a debt validation letter alone will not stop the court clock. You must file a formal "Answer" with the court to avoid a default judgment. However, the lack of validation can be a powerful defense in your court case. If they sued you without being able to validate the debt, they might have violated the FDCPA.

What if the collector ignores my letter?

If they ignore your letter and keep calling or reporting the debt to credit bureaus, they are likely in violation of federal law. Your next steps should be: • Filing a complaint with the Consumer Financial Protection Bureau (CFPB). • Reporting them to your State Attorney General (in Michigan or Florida). • Disputing the item directly with the credit bureaus (Equifax, Experian, and TransUnion) by providing a copy of your certified mail receipt.