What It Really Means to Answer a Debt Summons (And Why You Can't Ignore It)

How to answer a debt summons is something you need to know right now — before your deadline passes. Here's the short version:

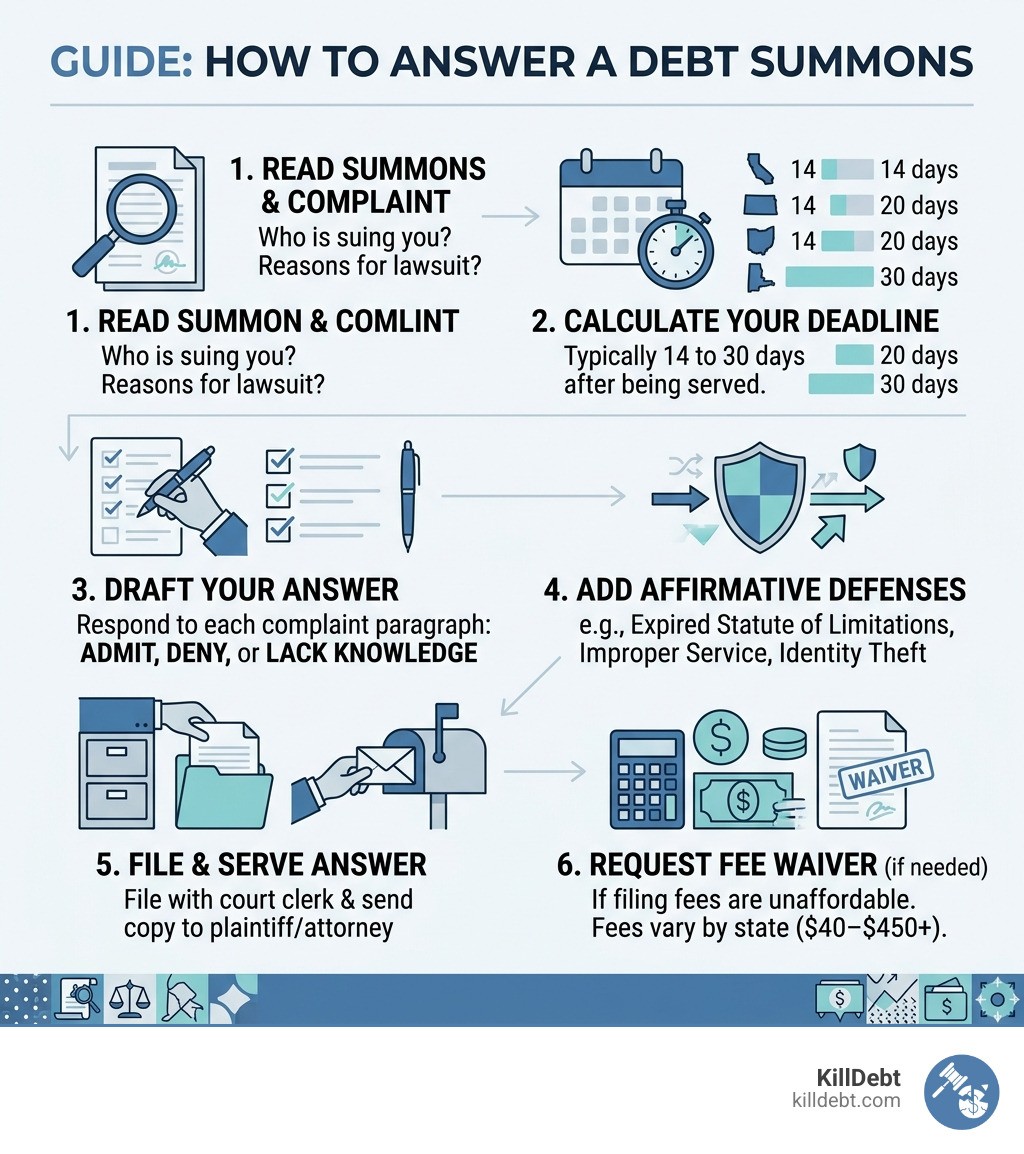

Read the summons and complaint carefully to understand who is suing you and why

Calculate your deadline — typically 14 to 30 days from the date you were served, depending on your state

Draft your Answer — respond to each paragraph in the complaint by admitting, denying, or stating you lack knowledge

Add affirmative defenses — such as expired statute of limitations, improper service, or identity theft

File your Answer with the court clerk and serve a copy on the plaintiff or their attorney

Request a fee waiver if you cannot afford the filing fee (typically $40–$450 depending on your state)

Getting served with a debt lawsuit is genuinely frightening. One day you open your door or your mailbox, and suddenly you're holding legal papers demanding thousands of dollars — often from a company you've never even heard of.

Here's the thing most people don't know: debt collectors are counting on you to do nothing.

Many debt collection lawsuits are won by default — meaning the defendant simply never responded. When that happens, the court hands the creditor an automatic win called a default judgment. That judgment can be used to garnish your wages, freeze your bank account, or put a lien on your property.

But filing a written Answer changes everything. It forces the other side to actually prove their case with real evidence. And that's harder than it sounds — especially when the debt has been sold multiple times or the paperwork is incomplete.

The good news? You don't need an expensive attorney to respond. Thousands of people successfully defend themselves in debt collection lawsuits every year. This guide will show you exactly how.

Understanding the Debt Summons and Complaint

When you are sued for a debt, you won't just receive a single piece of paper. You will receive a package of legal documents, usually delivered by a process server or sent via certified mail. This is called "service of process." Understanding the Difference Between Summons & Complaint in Debt Collection Lawsuit is your first step toward building a defense. As noted by the Consumer Financial Protection Bureau (CFPB), ignoring these documents can lead to severe financial consequences.

The Summons is the court’s official notice to you. It tells you that you are being sued, identifies the court where the case is filed, and—most importantly—specifies how many days you have to respond. The Complaint (sometimes called a Petition) is the document where the person suing you (the Plaintiff) lists their grievances against you (the Defendant).

Identifying the Parties and Allegations

Don't panic if you don't recognize the name of the company suing you. Often, the original creditor (like a big bank) sells "charged-off" debt to a debt buyer. These companies purchase thousands of accounts for pennies on the dollar and then sue to collect the full amount.

Check the top of the Summons for the Case Number. You will need this for every document you file. Then, look at the Complaint. It will be broken down into numbered paragraphs. Each paragraph is an "allegation"—a statement the Plaintiff claims is true. Knowing Who is Suing Me? Original Creditor vs. Debt Buyer Explained helps you determine if the Plaintiff even has the legal right to sue you.

The Risks of Ignoring a Summons

Ignoring these papers is the most expensive mistake you can make. If you don't file a written Answer, the Plaintiff will ask for a default judgment. Once they have this, they can:

Garnish your wages: In many states, they can take up to 25% of your take-home pay.

Freeze your bank account: They can seize the funds in your checking or savings.

Place property liens: They can attach a legal claim to your home or car.

There are many Debt Collection Lawsuit Myths: 7 Things That Won't Save You, but the biggest myth is that the problem will go away if you hide. It won't. It will only get more expensive as they add interest, court costs, and attorney fees to your bill.

How to Answer a Debt Summons: Step-by-Step Instructions

You do not need a law degree to protect your rights. Defending yourself "Pro Se" (representing yourself) is a right guaranteed to you. By following our What to Do When Sued by a Debt Collector: Complete First Steps Guide, you can stop the debt collector in their tracks.

Calculating Your Deadline to Respond to a Debt Summons

Your clock starts ticking the moment those papers touch your hand. Every state has different rules for the Time to Respond: Debt Collection Lawsuit.

Florida: You generally have 20 days to file a written response.

Michigan: You usually have 21 days (if served in person) or 28 days (if served by mail or outside the state).

If your deadline falls on a weekend or a court holiday, you usually have until the next business day, but we always recommend filing early to be safe. If you miss the deadline, check with the court clerk immediately. If the Plaintiff hasn't requested a default yet, you may still be able to file your Answer.

Drafting Your Answer and Affirmative Defenses to a Debt Summons

Your Answer is not the place to tell a long, emotional story. It is a formal response to the numbered paragraphs in the Complaint. For each paragraph, you have three options:

Admit: Use this only if the statement is 100% true (like your name and address).

Deny: This is the most common response. It doesn't mean you are lying; it means "I demand you prove this with evidence."

Lack of Knowledge: Use this if you don't have enough information to know if the statement is true (common when a debt buyer claims they purchased your specific account).

Next, you must list your Affirmative Defenses. These are legal reasons why the Plaintiff should lose even if the debt was originally yours. Common defenses include:

Statute of Limitations: The creditor waited too long to sue (often 3-6 years depending on the state). You can research specific state rules through resources like the Legal Information Institute.

Improper Service: You weren't served the papers according to legal rules.

Lack of Standing: The debt buyer cannot prove they own your specific debt.

Identity Theft: The debt isn't yours.

Response Type | What it Means | Strategy |

|---|---|---|

General Denial | Denying all or most allegations. | Forces the Plaintiff to provide strict proof for every claim. |

Affirmative Defense | Bringing up new facts (like the debt is too old). | Can get the case dismissed entirely regardless of the debt's validity. |

A Key to Strong Answer in a Collection Lawsuit: Solid Counter-Affidavit is often required if the Plaintiff attached an affidavit to their Complaint. Denying their affidavit with one of your own is a powerful move.

Filing Your Response and Serving the Plaintiff

Once your Answer is drafted, you must make copies. Usually, you need three: one for the court, one for the Plaintiff’s attorney, and one for your own records.

Handling Court Fees and Local Forms

In some states, filing an Answer is free. In others, it can cost between $40 and $450. In Florida, fees vary by county and the amount of the debt. In Michigan, you can use form MC 03 to file your Answer.

If you cannot afford the fee, ask the court clerk for a Fee Waiver (sometimes called an "Affidavit of Indigency"). If your income is below a certain level or you receive public assistance, the court will likely let you file for free.

When you file, you must also include a Certificate of Service. This is a simple statement telling the court that you sent a copy of your Answer to the Plaintiff's attorney. We always recommend sending it via Certified Mail with Return Receipt Requested so you have proof of delivery. This is a critical step in Filing a Counter-Affidavit When Answering a Debt Collection Lawsuit.

What Happens After You File Your Answer?

Filing the Answer is just the beginning. It stops the automatic win and moves the case into the "Discovery" phase. This is where both sides exchange information. You can use this time to ask the Plaintiff for the original contract, payment history, and proof of debt ownership.

Our Debt Collection Lawsuit Timeline: What Happens Next After You're Served explains that most cases never actually go to a full trial. Once you show you are willing to fight, the debt collector's math changes. It becomes more expensive for them to pay a lawyer to fight you than to settle.

Negotiating a Settlement Post-Filing

Filing an Answer gives you leverage. Now that the collector knows they have to work for the money, they may be open to:

Lump-sum settlements: Offering 40-60% of the total to close the case.

Payment plans: Spreading the debt over several months without further legal action.

If you reach an agreement, get it in writing before you pay a single dime. Ensure the agreement states that the lawsuit will be "Dismissed with Prejudice," which means they can never sue you for this specific debt again.

Conclusion

Knowing how to answer a debt summons is the difference between financial disaster and taking control of your future. You don't have to be a legal expert to stand up for yourself.

At KillDebt, we believe the legal system should be accessible to everyone, not just those who can afford $300-an-hour attorneys. Our DIY legal defense system is powered by ParkerGPT, an AI trained by attorney Brian Parker with over 30 years of consumer debt experience. We don't just give you a generic template; we analyze your specific lawsuit documents to find the "cracks" in the collector's case.

Want to see how you'd perform in front of a judge? Our new Court Tester tool allows you to upload your filings and practice your arguments against an AI judge and opposing counsel. It's the ultimate simulation to ensure you're ready for the real thing.

Don't let debt collectors win by default. Start your defense today and let us help you turn the tables.

Frequently Asked Questions (FAQ)

What if I actually owe the money?

Even if you recognize the debt, you should still file an Answer. Why? Because the amount they are suing for is often inflated with incorrect fees and interest. Furthermore, a debt buyer might not actually have the legal "standing" or evidence to prove they own the debt. Filing an Answer forces them to meet their burden of proof. You might find yourself asking, "Do I Need a Lawyer for a Debt Collection Lawsuit?" While a lawyer is helpful, many people find that AI tools like ParkerGPT provide the same strategic edge at a fraction of the cost.

Can I protect my Social Security or exempt income?

Yes. If your only income is Social Security, disability, or certain public assistance, you may be "judgment proof." This means that even if the creditor wins a judgment, they legally cannot seize that money. However, being judgment proof is a defense you must assert. You still need to file an Answer to protect these assets from being frozen temporarily.

What if I missed the 30-day deadline?

If a default judgment has already been entered, you aren't necessarily out of luck. You can file a Motion to Vacate Judgment. You will generally need to show "excusable neglect" (a good reason why you missed the deadline, like being in the hospital) and that you have a "meritorious defense" (a good reason why you might win the case).