Michigan Court Debt Cases Are Overwhelming Everyday People — Here's What You Need to Know

Michigan court debt cases are now one of the most common legal problems facing residents across the state. If you've received a court summons or a debt collection letter, you're not alone — and you do have options.

Quick answers for people facing a Michigan debt lawsuit:

Question | Answer |

|---|---|

How common are debt cases in Michigan courts? | About 37% of all civil district court cases are debt collection actions |

How long do I have to respond? | 21 days if personally served; 28 days if served by mail or from outside Michigan |

What happens if I don't respond? | The creditor wins automatically through a default judgment |

Will I face garnishment? | 68% of cases end in default judgments; nearly 80% of those lead to garnishment |

Do I need a lawyer? | Less than 2% of defendants have one — but you can defend yourself |

Debt collection lawsuits have quietly become the dominant force in Michigan's civil court system. Cases filed by debt buyers — companies that purchase old debts for pennies on the dollar — nearly doubled between 2010 and 2019. Today they make up 40% of general civil cases filed in the state.

The consequences for people who ignore these lawsuits are severe. Many Michigan residents first learn they've been sued when money is already missing from their paycheck or bank account.

This guide explains exactly how Michigan debt court cases work, what your rights are, and what steps you can take — even without a lawyer.

The Landscape of Michigan Court Debt Cases

In Michigan, the surge in debt litigation isn't just a minor trend; it is a tidal wave. Roughly 37% of all civil cases in Michigan district courts are debt collection actions. This means more than one out of every three civil lawsuits involves a creditor or debt buyer chasing a consumer for money.

What is particularly striking is the rise of the "debt buyer." These are companies that don't actually lend you money; instead, they buy portfolios of old, charged-off debt for a fraction of its value and then sue for the full amount. Between 2010 and 2019, cases filed by debt buyers in Michigan almost doubled. Today, these companies account for 40% of all general civil cases filed in the state.

Recent data shows that this trend isn't slowing down. In fact, Consumer Debt Lawsuits Are Surging Again: Here's What the Data Reveals in 2024-2025. In Michigan specifically, a staggering 55% of consumer debt collection cases were filed by just five major companies.

Filer Type | Growth Trend (2010-2019) | Current Court Share |

|---|---|---|

Debt Buyers | Nearly Doubled (+90%+) | 40% of Civil Cases |

Original Creditors | Relatively Stable | Decreasing relative to buyers |

The Impact on Michigan Communities

The burden of Michigan court debt cases does not fall equally across the state. Research from organizations like the Pew Charitable Trusts and the Michigan Justice for All Commission highlights a troubling reality: debt collection cases disproportionately impact majority Black communities.

Residents in predominantly Black neighborhoods are more than twice as likely to face debt collection lawsuits compared to those in majority-white neighborhoods. Perhaps most concerning is that this disparity persists even as incomes rise. High-income Black neighborhoods often see higher rates of debt lawsuits than low-income white neighborhoods. This suggests systemic issues in how debt is sold and pursued that go far beyond a simple lack of funds.

Navigating Michigan Court Debt Cases for Pro Se Defendants

When a debt collector sues, they almost always have a lawyer. In Michigan, nearly 100% of plaintiffs (the ones suing) are represented by counsel. On the flip side, less than 2% of defendants have an attorney.

This massive "justice gap" leads to a lopsided system where consumers feel they have no voice. Many ask, Do I Need a Lawyer for a Debt Collection Lawsuit?. While having a lawyer is great, it isn't always financially feasible.

Fortunately, resources like Michigan Legal Help offer tools for "pro se" (self-represented) defendants. At KillDebt, we’ve taken this a step further by providing a DIY legal defense system. We believe that with the right tools, you can hold these collectors to the same standards the law requires of them.

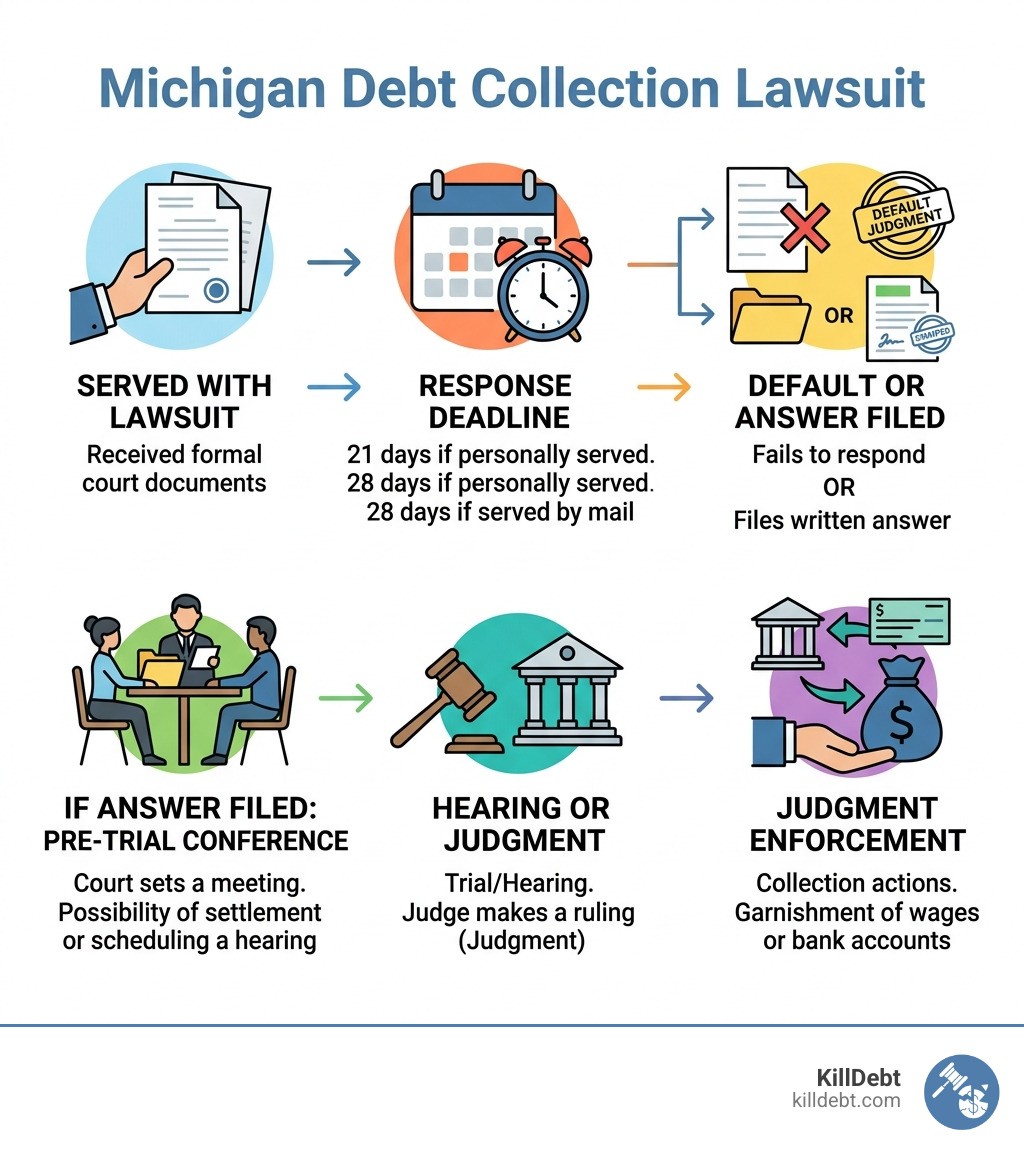

How to Respond to a Michigan Debt Collection Lawsuit

If you’ve been served with a Summons and Complaint, the clock is ticking. In Michigan, your deadline to respond depends entirely on how you were served:

21 Days: If you were personally handed the papers.

28 Days: If the papers were mailed to you or if you were served while outside the state of Michigan.

If you miss this window, the court will likely enter a "default judgment" against you. This is essentially an automatic win for the debt collector, allowing them to skip the part where they actually have to prove you owe the money. Understanding the Difference Between Summons & Complaint in Debt Collection Lawsuit is the first step in knowing what you are looking at. Once you know you've been sued, you must respect the Time to Respond: Debt Collection Lawsuit to keep your rights alive.

Drafting a Strong Answer and Counter Affidavit

Your "Answer" is your formal written response to the court. You must go through the Complaint paragraph by paragraph and state whether you "Agree," "Disagree," or "Do Not Know" (which has the legal effect of a denial).

One of the most critical components in Michigan court debt cases involves "Account Stated" claims. If a collector claims you owe a debt based on a final statement they sent you that you didn't dispute, they are using an "Account Stated" theory. To fight this effectively, you must file a Defendant’s Counter Affidavit.

Filing a Counter-Affidavit When Answering a Debt Collection Lawsuit is vital because it denies the accuracy of the account under oath. Without this notarized document, the court may assume the collector's numbers are correct. It is often the Key to Strong Answer in a Collection Lawsuit: Solid Counter-Affidavit.

Understanding the Role of Debt Buyers

As we mentioned, many plaintiffs in these cases are debt buyers rather than the original creditor (like your bank or credit card issuer). This is a huge advantage for you if you know how to use it.

Debt buyers must prove they have the legal right to sue you, known as "standing." This requires showing a clear "chain of title" — a paper trail of every time the debt was sold from the original creditor down to the company suing you now. Often, these companies have sloppy records or missing links in the chain. Knowing Who Is Suing Me? Original Creditor vs. Debt Buyer Explained helps you identify these weaknesses.

Common Defenses and Legal Strategies in Michigan

A defense is a legal reason why you shouldn’t have to pay. In Michigan, you must raise these defenses in your initial Answer, or you might lose the right to use them later.

Statute of Limitations: This is the "expiration date" on a debt. For most breach of contract cases in Michigan, the limit is 6 years from the date of last activity.

Installment Sales (Vehicles): If the debt is from a car loan or goods sold on an installment plan, the limit is often shorter — 4 years.

Mobile Homes: Sales contracts for mobile homes generally have a 3-year statute of limitations.

Prior Payment: If you already paid the debt, or reached a settlement, you must provide proof.

Identity Theft: If the debt isn't yours, this is a complete defense, though you'll need to provide supporting evidence like a police report.

You can find more details on these in this guide on Defenses in a Debt Collection Case.

Challenging Unauthorized Interest and Fees

Debt collectors often try to pad their profits by adding interest to the debt. However, Michigan law (MCL 438.31) generally limits interest to 5% per annum on "silent contracts" (contracts that don't specify an interest rate).

A major victory for consumers occurred in the case of Nelson v. I.Q. Data International, Inc. (2025). The court ruled that debt collectors cannot unilaterally add this 5% interest before they even file a lawsuit. The court found that adding unauthorized interest can be a violation of the Fair Debt Collection Practices Act (FDCPA). You can read the full document here: Nelson v. I.Q. Data International, Inc., No. 4:2022cv12710 - Document 64 (E.D. Mich. 2025).

Federal Protections and the FDCPA

Federal laws like the FDCPA provide a shield against abusive practices. For instance, if you dispute a debt, the collector must flag that debt as "disputed" when reporting it to credit bureaus.

A recent Michigan federal court ruling found that if a debt collector fails to update a credit agency after a consumer withdraws a dispute, or if their internal records conflict with what the credit agency shows, it creates a "genuine issue of fact." This prevents the debt collector from getting an easy win and allows the consumer to take the case to trial. These FDCPA protections are powerful tools for Michigan residents.

The Consequences of Inaction: Default Judgments and Garnishments

The biggest mistake you can make in Michigan court debt cases is doing nothing. Roughly 7 out of 10 people sued for debt in Michigan never respond. This leads to a 68% default judgment rate.

Once a creditor has a judgment, they don't just wait for you to pay. In Michigan, nearly 80% of debt judgments lead to a garnishment order.

Wage Garnishment: They can take a portion of your paycheck before you ever see it.

Bank Levies: They can freeze your bank account and seize the funds inside.

Tax Garnishments: Michigan is one of the few states that allows private creditors to garnish your state income tax returns.

People often believe Debt Collection Lawsuit Myths: 7 Things That Won't Save You, like thinking they are "judgment proof." But once the garnishment starts, it’s much harder to stop. If you're worried about your income, read up on Can Debt Collectors Take My Wages and Bank Account?.

Exemptions and Protections Against Garnishment

There are some protections, but they are often outdated. Michigan’s garnishment exemptions have not been significantly updated for inflation since 1964. This means the amount of money you are allowed to keep to live on is based on the cost of living from sixty years ago!

However, certain funds are generally exempt from garnishment:

Social Security benefits.

Public assistance (welfare).

Unemployment compensation.

Earned Income Tax Credits (EITC).

The Michigan Justice for All Commission has recommended urgent reforms to adjust these exemptions for modern inflation and to protect low-income residents from being pushed into total poverty by debt collectors.

Recent Legal Precedents and Reform Efforts in Michigan

Michigan's legal landscape is shifting to be more protective of property rights. A landmark case, Rafaeli, LLC v. Oakland County, changed how the state handles tax foreclosures. The Michigan Supreme Court ruled that when the government forecloses on a home for unpaid taxes, it cannot keep the "surplus proceeds" (the profit made from selling the home after the tax debt is paid).

In 2024, the court clarified in Hathon v. State of Michigan that this ruling applies retroactively. This means thousands of Michiganders whose homes were taken in the past may be entitled to get their equity back. You can view the opinion here: MSC 165219 LYNETTE HATHON V STATE OF MICHIGAN Opinion on Application.

Criminal Debt and Restitution Procedures

Debt isn't always about credit cards; sometimes it's "criminal debt" like court-ordered restitution. In the Eastern District of Michigan, these payments are now handled through Pay.gov.

A recent appellate case, People of Michigan v. Christopher Shane Babcock, highlighted how the "Clean Slate" law interacts with debt. The court ruled that a conviction that was automatically set aside cannot be reinstated just because restitution hasn't been paid in full — as long as the person has made a "good-faith effort" to pay. This is a huge win for those trying to rebuild their lives while managing old debts. COA 370899 PEOPLE OF MI V CHRISTOPHER SHANE BABCOCK Opinion.

Conclusion

Facing Michigan court debt cases can feel like an uphill battle, especially when you're up against massive corporations and their legal teams. But the law provides you with rights and defenses that can level the playing field.

At KillDebt, we provide a DIY legal defense system designed to help you fight back without the high cost of a traditional law firm. Our platform is powered by ParkerGPT, an AI trained on real-world strategies from attorney Brian Parker, who has over 30 years of experience in consumer debt law.

We recently introduced the Court Tester, an AI courtroom simulation. You can upload your actual case filings and "practice" your arguments against an AI judge and opposing counsel before you ever step foot in a real courtroom. It’s like having a private co-counsel whispering strategy in your ear.

Don't let a debt collector take your hard-earned wages through a default judgment. Take action, file your response, and stand up for your rights.

Frequently Asked Questions (FAQ)

How long do I have to respond to a debt lawsuit in Michigan?

You generally have 21 days if you were served in person and 28 days if you were served by mail or live outside of Michigan. It is vital to track your Debt Collection Lawsuit Timeline: What Happens Next After You're Served to ensure you don't miss these windows.

Can a debt collector add 5% interest to my debt in Michigan?

Under MCL 438.31, they can only do this if a contract allows it or after a judge awards it. They cannot just tack it on during the collection phase before a lawsuit is filed. As seen in Nelson v. I.Q. Data, doing so may violate the FDCPA.

What is the statute of limitations for debt in Michigan?

For most credit cards and personal loans, the limit is 6 years. This time usually starts from the date of your last payment or last activity on the account. Be careful — making even a small payment can sometimes "reset" this clock!