What the Illinois Debt Collection Statute Means for You

The Illinois debt collection statute is a set of state laws that control how debt collectors can treat you — and what you can do when they cross the line.

Here's a quick overview of what you need to know:

Topic | Key Facts |

|---|---|

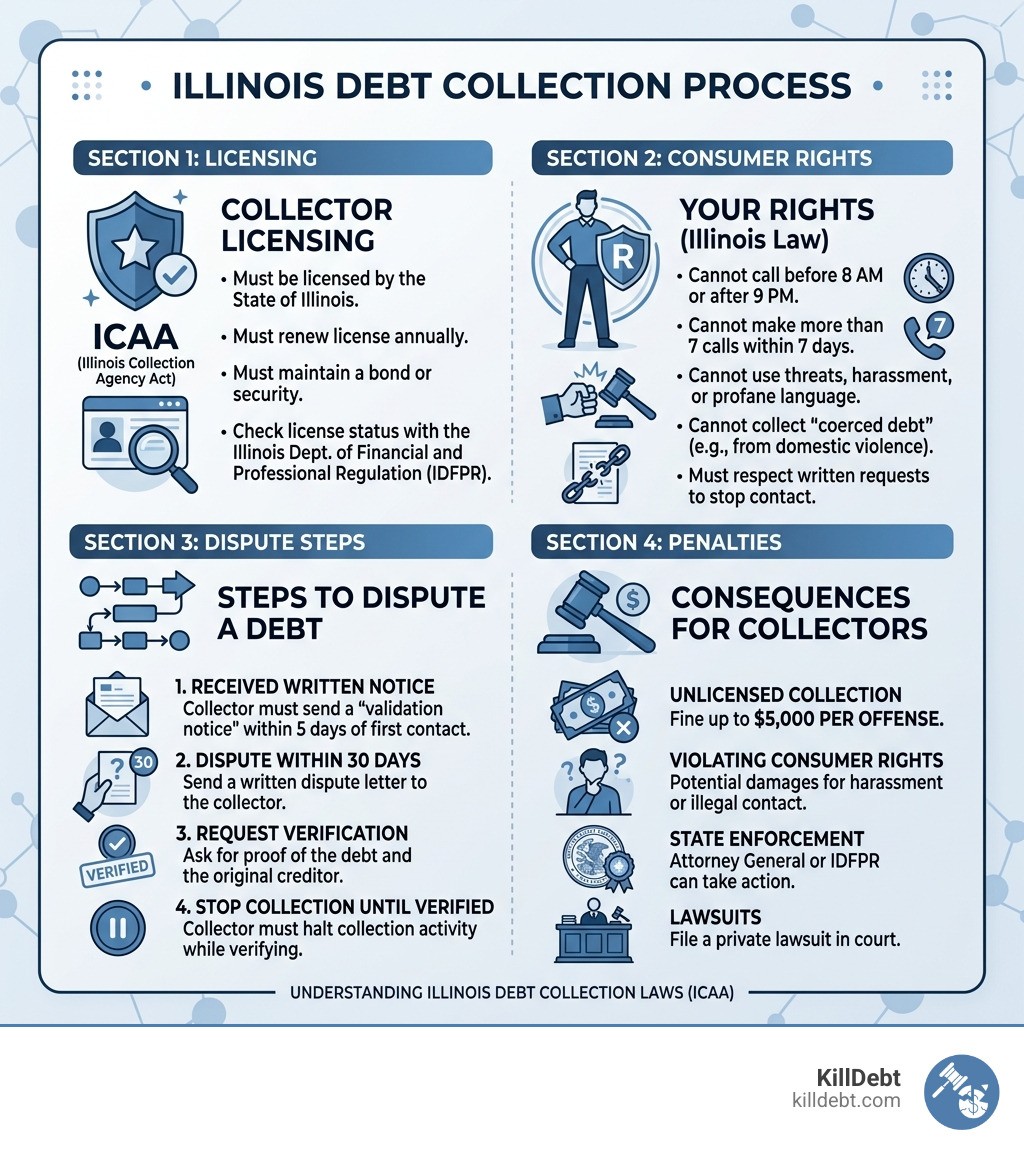

Primary state law | Illinois Collection Agency Act (ICAA), 205 ILCS 740/ |

Federal law that also applies | Fair Debt Collection Practices Act (FDCPA) |

Major recent change | SB 2457, effective January 1, 2026 |

New consumer protection | HB 3352 — bans collection of "coerced debt" |

Allowed contact hours | 8 a.m. to 9 p.m. local time only |

Call frequency limit | No more than 7 calls in 7 days |

Time to dispute a debt | 30 days from first contact |

Statute of limitations | 5 years (oral contracts), 10 years (written), 20 years (judgments) |

Penalty for unlicensed collection | Up to $5,000 per offense |

Getting a debt collection letter — or worse, a court summons — is stressful. Most people don't know their rights, and collectors count on that.

Illinois law gives you real, enforceable protections. Collectors must be licensed, follow strict communication rules, and stop contacting you if you ask them to in writing. And thanks to recent legislative updates, those protections are getting stronger.

This guide breaks down exactly how the law works, what collectors can and can't do, and what steps you can take right now to protect yourself — without needing to hire an expensive attorney.

Understanding the Illinois Debt Collection Statute and Licensing

When we talk about the Illinois debt collection statute, we are primarily referring to the Illinois Collection Agency Act (ICAA). For a long time, this law was found under Chapter 225 of the Illinois Compiled Statutes, but it has recently been renumbered and updated. Specifically, as of early 2023, much of the core regulation shifted to 205 ILCS 740/9.2 under the umbrella of financial regulation.

The most important thing for you to know right now is that Illinois is currently in a state of transition. On August 1, 2025, Senate Bill 2457 was enacted. This bill brings sweeping amendments to the ICAA that will officially take effect on January 1, 2026.

Why does this matter? Because for years, there was a lot of "gray area" regarding who actually needed a license to collect money in Illinois. The new amendments clarify that "collection agencies" must be licensed by the Illinois Department of Financial and Professional Regulation (IDFPR). This isn't just a paperwork requirement; it’s a consumer protection measure. To get that license, an agency must:

Submit detailed applications regarding their ownership.

Maintain a $25,000 surety bond to protect creditors and consumers if the agency fails to remit funds or follows illegal practices.

Maintain separate trust accounts for collected funds, ensuring your money doesn't just vanish into their operating budget.

If an agency is calling you without this license, they are in hot water. Under the Illinois General Assembly - Financial Regulation standards, unlicensed practice can result in civil penalties of up to $5,000 per offense.

It is also vital to understand the difference between the person you originally owed money to and the person calling you now. We often see consumers confused about who is actually allowed to sue them. You can learn more about this distinction in our guide on Who Is Suing Me: Original Creditor vs. Debt Buyer Explained.

Who is a "Collection Agency" Under the Illinois Debt Collection Statute?

Not everyone who asks you for money is a "collection agency" under the eyes of the law. This is where the 2026 amendments really clean things up.

Historically, the definition of a collection agency was a bit messy. It used to include people collecting debts "on behalf of himself or herself or others." This made original creditors (like the store where you bought your fridge) worried they needed a collection license just to send you a late notice.

Under the amended Illinois debt collection statute, the definition is more focused. A collection agency is generally a third-party entity or a "debt buyer" — a company that buys old, charged-off debts for pennies on the dollar and then tries to collect the full amount from you.

The new law explicitly excludes most "first-party" collectors. If you owe money to a local retail seller or a lender who originated your loan, they generally do not need a collection agency license to call you about your balance. However, if they hire a third party to do the dirty work, that third party must be licensed under 225 ILCS 425/ - Collection Agency Act.

Licensing Exemptions and the 2026 Amendments

The 2026 amendments didn't just clarify who is a collector; they also narrowed down who is exempt. Illinois wants to make sure that if a business is already regulated by another tough law, they don't have to jump through double the hoops.

New or clarified exemptions include:

Retail Sellers: People selling goods or services on credit.

Lenders under specific acts: This includes those licensed under the Sales Finance Agency Act or the Student Loan Servicing Act.

Attorneys: Licensed attorneys are generally exempt when they are practicing law, though they still have to follow ethical guidelines and federal laws.

Banks and Real Estate Brokers: These entities are usually regulated by other state or federal agencies.

One interesting change in SB 2457 is the removal of the ICAA from the "Regulatory Sunset Act." In plain English, this means the law is no longer scheduled to expire. It is now a permanent fixture of Illinois law, ensuring that these protections aren't accidentally deleted by the legislature.

Prohibited Practices and Consumer Protections

Illinois law doesn't just care about who is collecting; it cares deeply about how they do it. The Illinois debt collection statute mirrors many of the protections found in the federal Fair Debt Collection Practices Act (FDCPA), but it often adds its own local flavor.

The golden rule for debt collectors in Illinois is: No Harassment. They cannot use profanity, threaten violence, or lie to you. For example, they can't tell you that you'll be arrested (debt is a civil matter, not a criminal one) or that they are "with the government" if they aren't.

One of the most powerful tools in your arsenal is the "7-in-7" rule. Under both federal and Illinois guidelines, a collector generally cannot:

Call you more than 7 times in a 7-day period.

Call you within 7 days of having a telephone conversation with you about that specific debt.

If your phone is blowing up ten times a day, they are likely violating the law. You can read more about these federal-level protections in our article What Is a Debt Collector Under the FDCPA: Your Rights Explained.

Comparison: ICAA vs. FDCPA Rules

Practice | Illinois ICAA | Federal FDCPA |

|---|---|---|

Contact Hours | 8 a.m. to 9 p.m. | 8 a.m. to 9 p.m. |

Licensing | Requires state license & bond | No federal license required |

Workplace Calls | Prohibited if employer objects | Prohibited if employer objects |

7-in-7 Rule | Strictly enforced | Strictly enforced |

Debt Buyers | Covered as "Collection Agencies" | Covered if principal purpose is debt |

New Protections Against Coerced Debt in Illinois

One of the most compassionate updates to the Illinois debt collection statute is House Bill 3352 (HB 3352), which addresses "coerced debt."

Coerced debt happens when someone is forced into debt through fraud, duress, or domestic abuse. This often occurs in situations involving identity theft, elder abuse, or human trafficking. Under this new law, if you are a victim of coerced debt, you have a path to stop the collection entirely.

To assert this defense, you must provide the collector with a "statement of coerced debt." This statement must include:

Identification of the specific debt.

An affirmation that you didn't authorize the debt.

Supporting documentation, such as a police report or a court order.

Once a collector receives a complete statement, they must cease all collection activity for at least 90 days while they investigate. If they ignore this and keep hounding you, they can be held liable for actual damages or a penalty of up to $2,500, plus your attorney fees. This is a massive win for survivors in Illinois. You can find the legislative text for these types of protections at Illinois General Assembly - Public Act 095-0437.

Communication Restrictions Under the Illinois Debt Collection Statute

Illinois law is very specific about when and where a collector can talk to you. If they are calling you at 11 p.m., they are breaking the law. If they are calling your boss after you told them not to, they are breaking the law.

Key restrictions include:

The 8-to-9 Window: Calls are only allowed between 8 a.m. and 9 p.m. local time.

Attorney Representation: If a collector knows you have a lawyer, they must stop calling you and talk to the lawyer instead.

Third-Party Disclosure: They generally cannot tell your neighbors, friends, or family that you owe money. They can only contact third parties to find out where you live or work, and even then, they usually can't mention the debt.

Workplace Contact: If they know your employer prohibits personal calls, they must stop calling you at work immediately.

If you find yourself overwhelmed by these calls, we have a guide on Struggling with Debt Collectors that can help you regain your peace of mind.

How to Dispute a Debt and Defend Against Lawsuits

The moment a debt collector contacts you, a clock starts ticking. Within five days of that first contact, the collector is required by the Illinois debt collection statute to send you a written notice. This notice must tell you how much you owe and the name of the creditor.

More importantly, it must inform you of your right to dispute the debt within 30 days.

If you send a "Debt Validation Letter" within that 30-day window, the collector must stop trying to collect until they provide you with proof that the debt is actually yours. This is your first and best line of defense. You can find out more about how to draft these in our guide on Debt Validation Letters: Your First Line of Defense Against Collectors.

If the situation has already escalated to a lawsuit, don't panic. Many people ignore a summons, which leads to a "default judgment." This is exactly what the collectors want! Instead, you should follow our What to Do When Sued by a Debt Collector: Complete First Steps Guide to ensure your voice is heard in court.

Statute of Limitations for Illinois Debts

One of the most common ways we help people beat debt collectors is by checking the "expiration date" on the debt. In legal terms, this is the statute of limitations.

In Illinois, the timelines are quite specific:

Oral Contracts: 5 years. (Think "handshake deals" or unwritten agreements).

Written Contracts: 10 years. This includes most promissory notes and written loans.

Credit Cards: 10 years. (While some states have 3-year limits for credit cards, Illinois is notoriously long at 10 years).

Judgments: 20 years. If a collector already won a court case against you, that judgment is valid for two decades.

CRITICAL WARNING: In Illinois, if you make even a small partial payment on an old debt, you might "reset" the clock. A debt that was 9 years old and about to expire could suddenly be valid for another 10 years just because you sent them $5. Always validate the debt before you pay a dime.

To understand how the clock moves once a lawsuit starts, check out our Debt Collection Lawsuit Timeline: What Happens Next After You’re Served.

Responding to a Summons and Complaint Under the Illinois Debt Collection Statute

If you receive a summons in Illinois, you usually have two main tasks: filing an Appearance (telling the court you're participating) and filing an Answer (responding to the specific claims).

In your Answer, you have the chance to raise "affirmative defenses." These are reasons why, even if the facts the collector stated are true, they still shouldn't win. Common defenses include:

The statute of limitations has expired.

The collector doesn't have the "standing" (proof of ownership) to sue you.

The debt was already paid or settled.

The debt is "coerced debt" as defined by the new HB 3352.

We often recommend using a Solid Counter-Affidavit to challenge the collector's evidence. You should also make sure you understand the Difference Between Summons & Complaint in Debt Collection Lawsuit so you don't miss any deadlines.

Penalties for Violations and Unlicensed Activity

The state of Illinois doesn't take kindly to rogue debt collectors. If an agency violates the Illinois debt collection statute, they face significant penalties.

Civil Penalties: Unlicensed practice can cost an agency $5,000 per offense.

Disciplinary Fines: For licensed agencies that break the rules, fines start at $5,000 for a first violation and jump to $10,000 for subsequent ones.

Consumer Lawsuits: You have the right to sue a collector for violations. If you win, they may have to pay for your actual damages, additional statutory damages (up to $1,000 under FDCPA), and your attorney fees.

One of the biggest fears consumers have is what happens if they lose. Can they take your house? Your car? Your paycheck? While Illinois does allow for wage garnishment, there are strict limits and exemptions to protect your ability to live. We break this down in detail in Can Debt Collectors Take My Wages and Bank Account.

Conclusion

Navigating the Illinois debt collection statute can feel like trying to read a map in a thunderstorm. Between the renumbered statutes, the 2026 amendments in SB 2457, and the new coerced debt protections in HB 3352, there is a lot to keep track of.

But here is the good news: You don't have to do it alone.

At KillDebt, we provide a DIY legal defense system powered by ParkerGPT. This isn't just a chatbot; it's an AI trained specifically on consumer debt law and real-world court strategies developed over 30+ years by our lead attorney, Brian Parker. We’ve built this tool to analyze your specific lawsuit documents, identify the collector's weaknesses, and generate court-ready responses.

We’ve even introduced the Court Tester, an AI courtroom simulation. You can upload your actual filings and "practice" your arguments in front of an AI judge, with a private AI co-counsel giving you strategy tips that only you can see. It’s like having a 30-year veteran attorney whispering in your ear, at a fraction of the cost of hiring a law firm.

Whether you're just starting to get calls or you've already been served with papers, knowledge is your best defense. If you've been hounded by a collector, check out our guide: Have You Been Sued by a Debt Collector. We are here to help you stand your ground and kill that debt for good.

Frequently Asked Questions (FAQ)

Can a debt collector contact my employer in Illinois?

Yes, but with heavy restrictions. Under the ICAA, they can generally only contact your employer after you have been in default for 30 days, and they must give you 5 days' prior written notice. Even then, if your employer prohibits such calls or if you have a lawyer, they must stop.

What is the "7-in-7" rule for debt collection calls?

This is a rule that prevents collectors from harassing you with constant calls. They cannot call you more than 7 times in a rolling 7-day period regarding a single debt. If they actually speak to you, they have to wait another 7 days before calling again about that same debt.

How do I stop a collector from calling me?

The most effective way is to send a "Cease and Desist" letter via certified mail. Once they receive it, the Illinois debt collection statute and federal law require them to stop all communication, except to tell you they are stopping or to notify you of a specific legal action (like a lawsuit).