What Setting Aside a Default Judgment Actually Means — and What to Do Right Now

Setting aside a default judgment is the legal process of asking a court to cancel a ruling that was entered against you because you didn't respond to a lawsuit or missed a court date.

If that's happened to you, here's the short version of what you need to know:

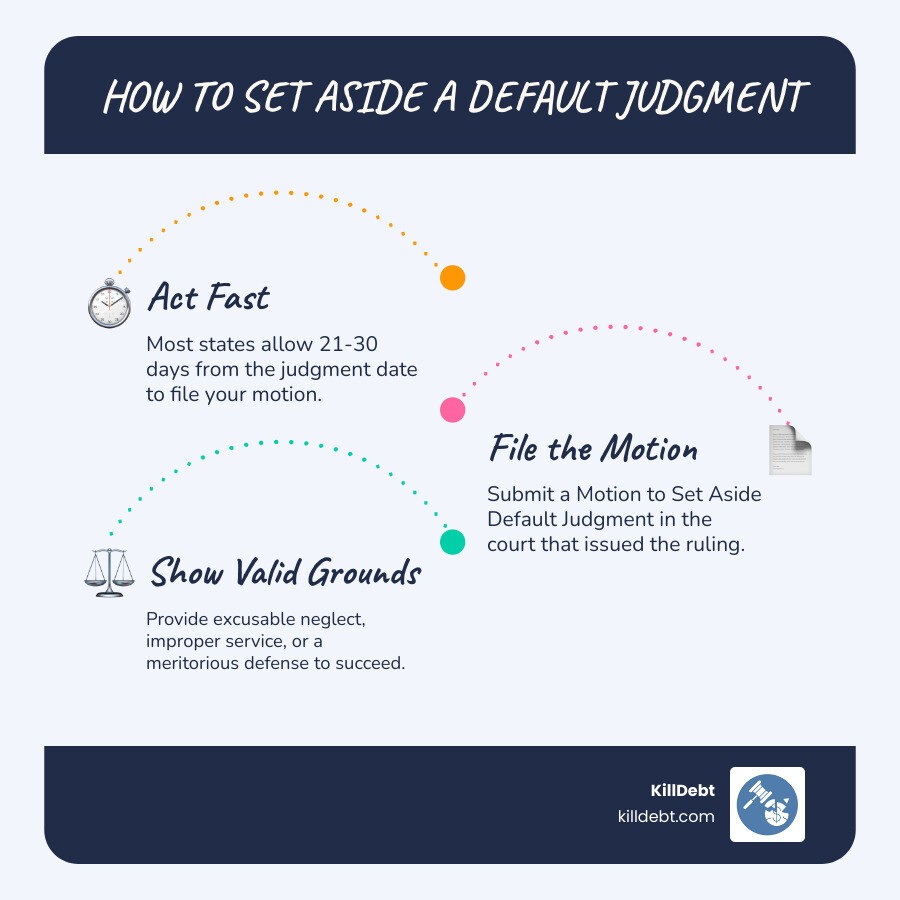

How to set aside a default judgment — quick overview:

Act fast. Most states give you 21–30 days from the judgment date to file a motion. Some states allow longer windows under specific circumstances.

File a Motion to Set Aside Default Judgment with the court that issued the ruling.

Give the court a valid reason — such as improper service, excusable neglect, or a procedural error.

Show a meritorious defense — meaning you have a real, legitimate reason to contest the underlying claim.

Attend the hearing and present your case to the judge.

A default judgment can feel like a punch to the gut. One day you're dealing with collection letters, and the next you find out a court has already ruled against you — and a creditor now has the legal power to garnish your wages, freeze your bank account, or put a lien on your property.

But a default judgment is not necessarily the end of the road.

Courts enter default judgments every day against people who were never properly served, who had a genuine emergency, or who simply didn't understand the legal process. The good news: the law in most states gives you a real path to fight back — if you move quickly.

My name is Brian Parker, and for over 30 years I've been in the courtroom fighting creditors, debt buyers, and collection law firms — I've helped thousands of consumers navigate the exact process of setting aside a default judgment. I'll walk you through everything you need to know to defend yourself, step by step.

Understanding the Legal Grounds for Setting Aside Default Judgment

When we talk about setting aside default judgment, we aren't just asking the judge for a "do-over" because we’re unhappy with the result. Judges like finality; they don't enjoy reopening cases unless there is a compelling legal reason to do so. To succeed, you must fit your situation into specific "grounds" recognized by the law.

In our experience helping people in Florida and Michigan, the most common grounds fall into a few specific buckets. If you've recently discovered a judgment and are panicking, take a deep breath and see if your situation fits one of these:

Excusable Neglect: This is the legal version of "I have a really good excuse." It’s not for people who just ignored the papers, but for those who had a legitimate reason for missing the deadline. Think of things like a serious medical emergency, being hospitalized, or a death in the immediate family.

Lack of Personal Jurisdiction (Bad Service): This is a heavy hitter. If the debt collector never actually served you with the lawsuit, the court never had the power (jurisdiction) to rule against you in the first place. For example, if the process server says they handed the papers to you in Detroit, but you can prove you were in Miami that day, the judgment is likely void. You can learn more about this in our Debt Lawsuit Defense Guide.

Fraud or Misconduct: If the plaintiff (the person suing you) lied to the court to get the judgment, that’s a major ground for Vacating a Default Judgment.

Void Judgment: A judgment is void if the court lacked the authority to enter it, such as if the lawsuit was filed in the wrong court or after the statute of limitations had already expired.

Procedural Irregularity: This happens when the court or the creditor skips a step. For instance, if they didn't send you the required notice of the default hearing, you might have grounds to pull the plug on that judgment.

If you’re wondering how this affects your specific debt, check out our guide on How to Remove Default Judgment Debt.

Proving Good Cause and a Meritorious Defense

In most jurisdictions, especially in Michigan and Florida, just having a "good excuse" (Good Cause) isn't enough. The judge also wants to know that if they reopen the case, you actually have a chance at winning. This is called a Meritorious Defense.

Think of it like this: The judge doesn't want to waste the court's time reopening a case just so you can lose all over again. You need to show that you have a "real" defense.

What is NOT a meritorious defense?

"I'm broke and can't pay."

"I forgot about the debt."

"The interest rate is too high."

What IS a meritorious defense?

"I already paid this debt."

"This isn't my account (Identity Theft)."

"The amount they are claiming is wrong, and I have the records to prove it."

"The plaintiff doesn't have the legal right to sue me (lack of standing)."

To prove this, you'll often need to file a Key to Strong Answer in a Collection Lawsuit: Solid Counter-Affidavit. This is a sworn statement where you lay out the facts of your defense. In Michigan, for example, under MCR 2.603(D), you must file a verified statement of facts showing this defense before the court will even consider setting aside default judgment.

Deadlines and Time Limits Across Different Jurisdictions

Time is your absolute worst enemy when a judgment is involved. In the legal world, "sleeping on your rights" is a fast way to lose them. While we specialize in Florida and Michigan, it’s helpful to see how these deadlines compare so you understand the urgency.

State | Standard Deadline to File Motion | Special Notes |

|---|---|---|

Michigan | 21 Days | From the date the default judgment was entered. |

Florida | 1 Year | For excusable neglect or fraud; "Reasonable time" for others. |

Texas | 30 Days | 14 days in Justice Court. |

Nevada | 6 Months | From the date of written notice of entry of judgment. |

Virginia | 2 Years | Specifically for fraud on the court. |

In Michigan, the rule is quite strict. According to MCR 2.603(D), you generally have only 21 days after the default judgment is entered to file your motion if you were personally served. If you wait until day 22, your path becomes much steeper, requiring a "Motion for Relief from Judgment" under MCR 2.612, which has a higher burden of proof.

In Florida, Rule 1.540(b) allows you up to one year to file for reasons like mistake, inadvertence, or excusable neglect. However, "one year" is the maximum. The law says you must file within a "reasonable time." If you find out about a judgment in January and wait until December to do something about it, the judge might decide that wasn't a "reasonable" delay and deny your motion.

For a deeper dive into the timing of these cases, see our Debt Collection Lawsuit Timeline: What Happens Next After You're Served. And remember, the clock starts ticking the moment the judge signs that order, not necessarily when you find out about it!

Exceptions to the Standard Timeline for Setting Aside Default Judgment

There are a few "get out of jail (mostly) free" cards when it comes to these deadlines. If you weren't personally served — meaning the papers weren't handed to you or a resident at your home — the rules often change.

Service by Publication: If the creditor couldn't find you and "served" you by putting a notice in a legal newspaper you never read, many states (like Texas and California) allow up to two years to challenge the judgment.

Military Duty Protections: Under the Servicemembers Civil Relief Act (SCRA), if you were on active duty when the judgment was entered, you have significant protections. Courts generally cannot enter a default against an active-duty member without appointing an attorney for them, and you can often reopen these cases long after the standard deadlines have passed.

Lack of Actual Notice: In California, Section 473.5 allows you to set aside a default if the service didn't result in "actual notice" to you, provided you act within 180 days of learning about the judgment.

If you’re confused about whether you were properly served, read our article on What Happens After Summons.

Step-by-Step Guide to Filing Your Motion

Now we get to the "how-to" part. If you're ready to fight, you'll need to prepare a package of documents for the court. Don't worry; we do this every day at KillDebt.

Step 1: Get the Case File. Go to the courthouse where the judgment was entered. Ask the clerk for a copy of the "Proof of Service" or "Affidavit of Service." This tells you who the creditor claims they served, when, and where. If it says they handed it to a 6-foot-tall man at your house, but you live alone and are 5-foot-2, you’ve found your first weapon.

Step 2: Draft the Motion to Set Aside Default Judgment. This is your formal request to the judge. It should clearly state:

The date the judgment was entered.

The reason (Grounds) you missed the deadline (e.g., "I was never served").

The fact that you have a meritorious defense.

Step 3: Prepare the Affidavit of Meritorious Defense. This is a sworn, notarized statement. You must explain why you would win if the case went to trial. In Michigan, this is a requirement under Setting Aside Judgments rules. You can find a Sample Answer to Debt Collection Lawsuit to see how defenses are typically phrased.

Step 4: Draft a Proposed Order. Judges are busy. If you provide them with a "Proposed Order" that they can simply sign if they agree with you, it makes their life easier. It should simply say "The Motion to Set Aside Default Judgment is hereby GRANTED."

Step 5: Schedule the Hearing. In most courts, you can't just drop off papers and wait. You have to get a hearing date from the clerk and then "serve" notice of that hearing on the creditor's attorney.

Procedural Requirements for Setting Aside Default Judgment

Don't let a "technicality" ruin your chance at justice. There are a few boring but vital steps you must follow:

Filing Fees: It usually costs money to file a motion. However, if you are low-income, you can ask for a Fee Waiver.

Certificate of Service: You must prove to the court that you sent a copy of your motion to the creditor’s lawyer. Usually, mailing it via first-class mail is enough, but you must file a signed paper saying you did it.

Consult the Clerk: Every court has its own "local rules." Some want three copies of everything; some want blue ink only. A quick, polite call to the Clerk of Court can save you a lot of headaches.

For a complete walkthrough of the defense process, check out our Fight Debt Collection Lawsuit Complete Guide and our specific advice for Justice Court Debt Answer.

What Happens After the Judgment is Set Aside?

If the judge smiles upon you and grants your motion, congratulations! But don't pop the champagne just yet. Setting aside a default judgment doesn't mean the debt goes away; it just means the "game is back on."

Here is what happens next:

The Case Restarts: The clock resets. You are now back at the beginning of the lawsuit.

Filing a Formal Answer: Usually, the judge will give you a specific window (like 14 or 21 days) to file a formal "Answer" to the original lawsuit. If you miss this deadline, you'll end up right back in default. Check our guide on How to Answer a Debt Summons to make sure you do it right.

Discovery Process: Both sides can now ask each other for documents and evidence. This is where you can demand the debt buyer prove they actually own the debt.

Stopping Wage Garnishment: If the creditor was already taking money from your paycheck, a set-aside order should stop that immediately. You will need to take a certified copy of the judge's order to your employer's HR department.

Removing Judgment Liens: If they put a lien on your house, you’ll need to record the new order with the county records office to clear your title.

For more on dealing with the creditor after the reset, see Debt Collector Suing Me Advice.

Conclusion

Facing a default judgment is stressful, but you don't have to face it alone. At KillDebt, we believe that everyone deserves a fair day in court, regardless of their bank balance.

We’ve built ParkerGPT, an AI trained specifically on consumer debt law and real court strategies developed over 30+ years by attorney Brian Parker. Unlike generic AI, ParkerGPT analyzes your actual lawsuit documents, identifies the procedural weaknesses, and generates court-ready motions with step-by-step instructions.

And if you’re nervous about that upcoming hearing? We just rolled out the Court Tester. It’s an AI courtroom simulation built on your actual case. You can upload your filings and, within minutes, find yourself arguing your motion in front of an AI judge. You'll face AI opposing counsel, while a private AI co-counsel whispers strategy only you can see. It’s the ultimate way to build confidence before you step into the real courtroom.

Don't let a debt collector take your hard-earned wages without a fight. The law gives you the tools to fight back—we just give you the power to use them.

Start your defense today and take the first step toward setting aside default judgment and reclaiming your financial future.

Frequently Asked Questions (FAQ)

Can I set aside a judgment if I was never served?

Absolutely. In fact, "Lack of Personal Jurisdiction" due to bad service is one of the strongest reasons to vacate a judgment. If you can prove you weren't served, the judgment is "void." In some states, like New York, this might lead to a "Traverse Hearing" where the process server has to testify, and you get to prove they’re lying. If you win, the case is often dismissed "without prejudice," meaning they have to start all over again from scratch (if they even can).

Does setting aside a judgment wipe out the debt?

No. It wipes out the judgment. The lawsuit still exists. Think of it like hitting the "reset" button on a video game. You still have to play the level, but you get a second chance to win. This is the perfect time to look for a settlement or a complete defense based on the merits of the case.

When should I consult an attorney for a default judgment?

While we provide the tools for a DIY defense, you should consider a pro if: • The debt is massive (e.g., over $50,000). • The creditor is claiming complex fraud. • You missed the standard deadlines by several years. • You have a complicated military status issue.