What Is a Justice Court Debt Answer — and Why It Could Save You

If you've just been served with court papers, a justice court debt answer is the written document you file with the court to respond to a debt lawsuit against you. Here's what you need to know right away:

Quick Answer: How to Respond to a Justice Court Debt Claim

Read your papers — identify the court, the plaintiff, and the amount claimed

Check your deadline — you typically have 14–30 days depending on your state (Texas: 14 days; Arizona, Minnesota, Montana: 20 days)

Fill out the Answer form — deny the claims, list your defenses

File with the court — filing an Answer is free in Texas and most justice courts

Serve the plaintiff — send a copy to the plaintiff or their attorney

Show up — attend your hearing with documents and evidence

Getting served with a debt lawsuit feels terrifying. One day you're going about your life. The next, you're holding official court papers saying someone is suing you for thousands of dollars.

Here's the thing most people don't know: simply filing a written response — your Answer — is often enough to completely change the outcome of your case.

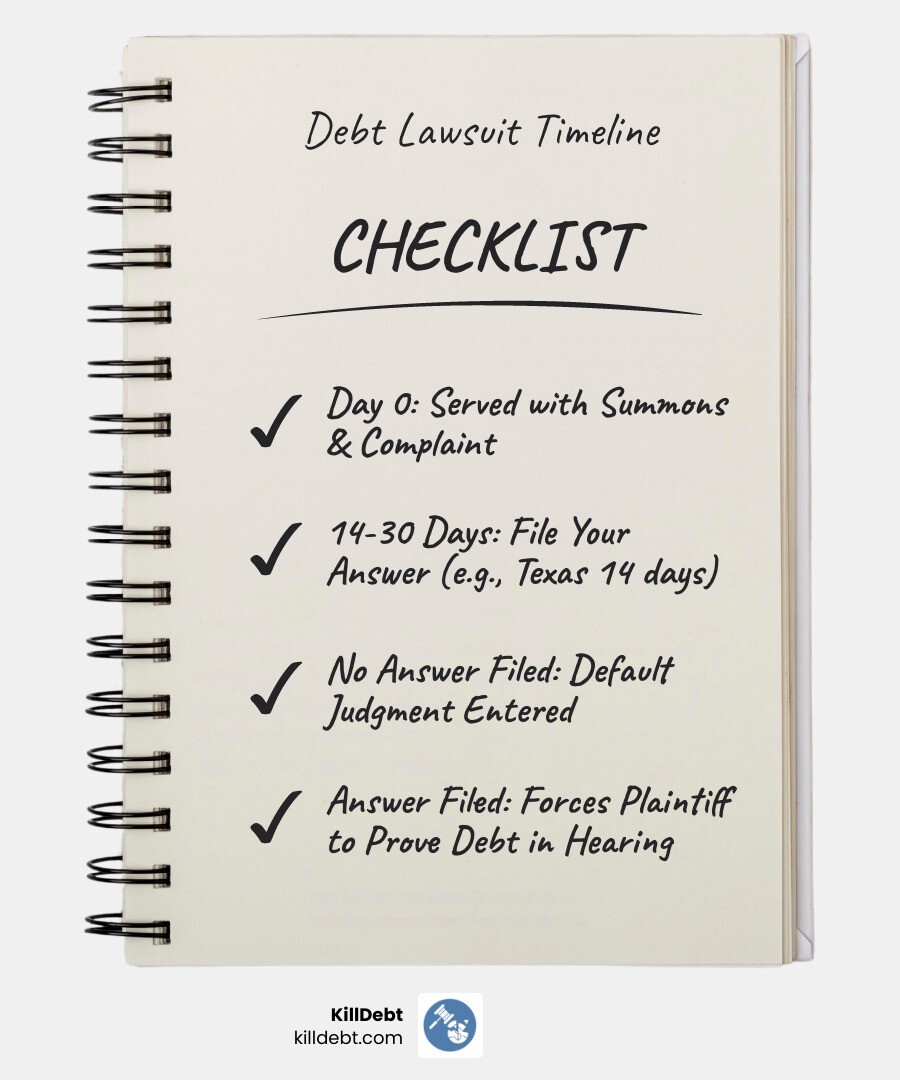

If you don't file an Answer, the court can enter a default judgment against you automatically. That means the debt collector wins without ever having to prove anything. They can then pursue wage garnishment, bank levies, or property liens.

But if you do file? You force them to prove their case. Many debt buyers — companies that purchase old debts for pennies on the dollar — don't have the paperwork to do that.

This guide walks you through every step, even if you've never set foot in a courtroom.

Understanding Your Justice Court Debt Answer Deadline

The very first thing we need to do is look at the clock. In law, deadlines are everything. If you miss your window to file a justice court debt answer, the court assumes you agree with everything the debt collector says.

The "clock" starts ticking the moment you are "served." This usually happens when a process server hands you the papers or, in some cases, when they are sent via certified mail. This packet contains two vital documents: the Summons (telling you that you’re being sued and where to go) and the Complaint (listing why they think you owe money). Understanding the difference between summons and complaint in debt collection lawsuit is your first step toward a solid defense.

For our friends in Florida and Michigan, the rules are specific:

Florida: You generally have 20 calendar days from the date you were served to file a written response with the court.

Michigan: You have 21 days if you were served in person, or 28 days if you were served by mail or while you were outside the state.

If your deadline falls on a weekend or a court holiday, you usually have until the next business day. However, we always recommend aiming to file at least two days early. Life happens—traffic, printer jams, or long lines at the clerk's office shouldn't be the reason you lose a lawsuit. You can find more details on the time to respond to a debt collection lawsuit to ensure you stay on track.

Why You Must File a Justice Court Debt Answer

We cannot stress this enough: filing an Answer is your shield. It protects your legal rights and prevents the "automatic loss" known as a default judgment.

When a judge signs a default judgment, the debt collector gets a "golden ticket" to your finances. They can:

Garnish your wages: A portion of your paycheck is sent directly to the creditor before you even see it.

Freeze your bank account: You might go to buy groceries only to find your debit card declined because the bank was ordered to hold your funds.

Place liens on property: This can prevent you from selling your home or car until the debt is paid.

By filing your justice court debt answer, you stop this runaway train. You are essentially telling the court, "Wait a minute. I want to see their proof." This forces the plaintiff (the person suing you) to actually provide evidence that the debt is yours, that the amount is correct, and that they have the legal right to collect it.

State-Specific Rules for Your Justice Court Debt Answer

While the general process is similar, Florida and Michigan have their own flavors of justice court (often called County Court in Florida or District Court in Michigan).

In Florida, many small claims cases (debts under $8,000) involve a "Pre-trial Conference." You might be required to show up in person on a specific date listed on your summons rather than filing a written answer first. However, if the case is in County Court for a larger amount, that 20-day written response rule is king. Check out Facing a Debt Collection Lawsuit in Florida? Here's How to Respond for localized tips.

In Michigan, the courts provide a standardized form called MC 03, Answer (Civil). This form makes it much easier for you to respond without needing a law degree. You can also find a Do-It-Yourself Civil Answer - Michigan Legal Help tool that walks you through the process. Michigan is very strict about the 21-day limit, so don't dawdle!

How to Draft Your Response: General Denials and Defenses

Now, let's get into the nitty-gritty of the document itself. When you look at the Complaint, you’ll see numbered paragraphs. Your justice court debt answer needs to address these paragraphs one by one.

You have three main ways to respond to each allegation:

Admit: Use this only if the statement is 100% true (like your name or address).

Deny: This is your most powerful tool. By denying a claim, you are not necessarily saying "this is a lie"; you are saying "I demand that you prove this."

Lack of Knowledge: This is great for when the debt collector says something like, "The Plaintiff is a corporation organized under the laws of Delaware." You have no way of knowing that, so you state you lack sufficient information to admit or deny.

In many jurisdictions, you can use a General Denial. This is a short statement where you deny everything in the Complaint at once. This shifts the entire burden of proof onto the creditor. They must now prove every single element of their case to win.

Common Affirmative Defenses in a Justice Court Debt Answer

An "Affirmative Defense" is a reason why, even if the facts in the Complaint are true, the plaintiff should still lose. These are the "Yes, but..." arguments of the legal world. You must include these in your initial Answer, or you might lose the right to use them later.

Statute of Limitations: This is the most common defense. Every state has a time limit on how long a creditor can wait to sue you. In Florida, the limit for most credit card debts and written contracts is 5 years. In Michigan, it is generally 6 years. If they sue you after this time has passed, the case should be dismissed.

Standing (Chain of Assignment): Debt buyers often purchase thousands of accounts at once. Frequently, they lose the paperwork showing that your specific account was part of that sale. If they can't prove they own the debt, they have no "standing" to sue you.

Identity Theft: If the debt isn't yours because someone stole your information, this is a vital defense.

Payment/Settlement: If you’ve already paid this debt or settled it for a smaller amount, you need to say so.

To make your defenses even stronger, consider filing a counter-affidavit when answering a debt collection lawsuit. A key to strong answer in a collection lawsuit is a solid counter-affidavit because it puts your side of the story into a sworn statement that the judge must consider.

Step-by-Step Guide to Filing and Serving Your Answer

Once your justice court debt answer is written and signed, you have to get it to the right people. This is a two-step dance: Filing and Serving.

Step 1: Filing with the Court

You must deliver the original copy of your Answer to the Clerk of the Court where the lawsuit was filed.

Fees: In many justice or small claims courts, filing an Answer is free. However, some courts may charge a small fee.

Fee Waivers: If you cannot afford the filing fee, ask the clerk for a "Fee Waiver" or "Indigency" form. If you meet certain income requirements, the court will let you file for free.

Methods: You can usually file in person, by mail, or through an electronic filing system (e-filing) if your county supports it. If you go in person, bring an extra copy and ask the clerk to "date-stamp" it for your records. This is your proof that you met the deadline.

Step 2: Serving the Plaintiff

You are legally required to give the other side a copy of your Answer.

Certificate of Service: At the end of your Answer form, there is usually a section called the "Certificate of Service." You fill this out to tell the court how and when you sent the copy to the plaintiff's attorney.

Method: In most cases, you can send this via regular First-Class Mail. Some people prefer Certified Mail with a Return Receipt for extra peace of mind.

For a more detailed walkthrough, check out our what to do when sued by a debt collector: complete first steps guide.

Requesting a Jury Trial and Changing Venue

Sometimes, the court where you were sued isn't the right one.

Venue: Generally, you must be sued in the county where you live or where the contract was signed. If you live in Miami and are being sued in Jacksonville, you can file a "Motion to Transfer Venue."

Jury Trial: If you want a jury of your peers to hear your case instead of just a judge, you must request this in writing—often right in your Answer. Be aware that there is usually a fee for a jury trial, and it involves more complex rules. To see how this fits into the bigger picture, review the debt collection lawsuit timeline: what happens next after you're served.

Protecting Your Assets and Preparing for the Hearing

Filing the Answer is the beginning, not the end. While you wait for your hearing date, you need to know what property is safe from creditors. Even if you lose the case, certain types of income and property are "exempt" under Florida and Michigan law.

Asset Type | Florida Protections | Michigan Protections |

|---|---|---|

Social Security | 100% Exempt | 100% Exempt |

Wages | Head of Family (up to $750/wk) | Partial protection (varies) |

Homestead | Unlimited value (with limits) | Up to $40,475 (varies by age) |

Retirement (401k/IRA) | Generally 100% Exempt | Generally 100% Exempt |

Veterans Benefits | 100% Exempt | 100% Exempt |

Listing these exemptions in your justice court debt answer is a smart move. It tells the creditor right away that even if they win, they might not be able to collect anything from you. This is often called being "judgment proof."

When the hearing date arrives, don't show up empty-handed. Bring:

Three copies of every document (one for you, one for the judge, one for the other side).

Proof of payments (bank statements, cancelled checks).

Any correspondence with the debt collector.

A list of your witnesses.

Don't let debt collection lawsuit myths trip you up—like the idea that the case will just "go away" if you ignore it. Preparation is your best friend.

Conclusion

Filing a justice court debt answer is the single most important step you can take to protect your future. It moves you from a victim of the system to an active participant in your defense.

At KillDebt, we believe that everyone deserves a fair fight. That’s why we built ParkerGPT, our AI legal defense system. It’s trained on the real-world strategies of Brian Parker, an attorney with over 30 years of experience fighting debt collectors in Michigan and Florida.

Instead of staring at a blank page and guessing which boxes to check, you can use our platform to analyze your lawsuit documents and generate a court-ready response. And if you’re feeling nervous about the hearing? Our brand-new Court Tester lets you practice in an AI courtroom simulation. You can argue your motions in front of an AI judge and see how an AI opposing counsel might respond—all while a private AI co-counsel whispers winning strategies in your ear.

Don't let the debt collectors win by default. Take a deep breath, follow the steps in this guide, and remember: you have rights, and we are here to help you use them.

Ready to take the first step? Visit KillDebt today and let's get to work on your defense.

Frequently Asked Questions (FAQ)

Do I need a lawyer for a justice court case?

The short answer is: No, you aren't required to have one. Justice courts are designed to be accessible to regular people (this is called appearing "Pro Se"). The rules are simplified compared to higher courts. However, debt collectors will have an attorney. If you're worried about the cost of a lawyer, you aren't alone. We wrote an entire guide on do I need a lawyer for a debt collection lawsuit to help you weigh the pros and cons. This is exactly why we created KillDebt—to give you attorney-level strategies without the attorney-level price tag.

What happens if I miss the filing deadline?

If you miss the deadline and a default judgment is entered, all is not lost, but it gets much harder. You would need to file a "Motion to Set Aside Default Judgment" or a "Motion to Vacate Judgment." You usually have to prove that you had a "good excuse" for missing the deadline (like being in the hospital) and that you have a "meritorious defense" (a real reason why you might win the case). If you're in this boat, read our guide: Have you been sued by a debt collector?

How do I handle a debt buyer I don't recognize?

This is very common. You might have had a credit card with Chase, but now a company called "Portfolio Recovery" or "Midland Funding" is suing you. In your justice court debt answer, you should deny that you have a contract with this new company. Make them prove the "Chain of Title"—the legal paper trail showing exactly how they bought your debt from the original creditor.