What to Do When a Debt Collector Sues You

If you're looking for debt collector suing me advice, here is the short version: respond to the lawsuit before the deadline, or you automatically lose.

Quick Action Plan:

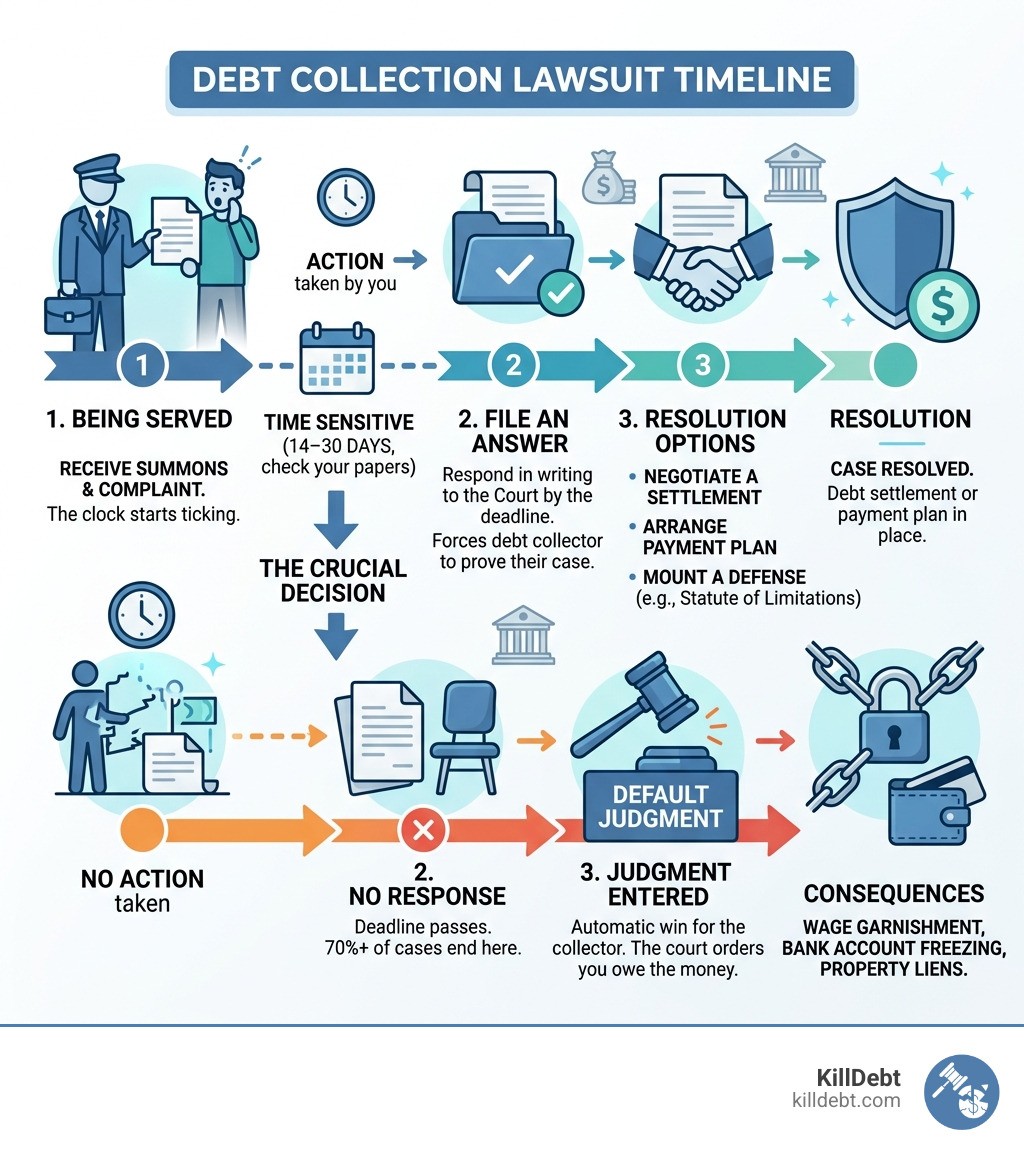

Don't ignore it. Over 70% of debt collection cases end in a default judgment — simply because the person never responded.

Read every document carefully. You'll have a Summons and a Complaint. Note your response deadline (usually 14–30 days).

File a written Answer with the court. This forces the debt collector to prove the debt is valid, the amount is correct, and they have the legal right to collect it.

Check the statute of limitations. If the debt is too old, the collector may not legally be able to sue you.

Look for FDCPA violations. Debt collectors who break the law can be sued — even if the underlying debt is real.

Explore your options. You can settle, negotiate a payment plan, raise defenses, or in some cases file for bankruptcy.

Get help if you need it. Free legal aid, nonprofit credit counselors, and AI-powered tools exist for people who can't afford a lawyer.

Getting served with a debt collection lawsuit is one of the most stressful things that can happen when you're already struggling financially. That thick envelope shows up — a Summons, a Complaint, legal language you've never seen before — and it's easy to freeze up.

That reaction is exactly what debt collectors count on.

Many collectors file lawsuits with incomplete records, knowing that most people won't respond. When you don't respond, the court hands them a default judgment automatically. That judgment gives them powerful tools: they can garnish your wages, freeze your bank account, or put a lien on your property — all without ever having to prove the debt in court.

The good news? Responding changes everything. It shifts the burden of proof onto them. It opens the door to negotiation. And it protects rights you didn't even know you had.

This guide will walk you through exactly what to do — step by step — so you can face this with clarity instead of panic.

Immediate Steps: What to Do After Being Served

The moment a process server hands you those papers, the clock starts ticking. In the legal world, silence equals consent. If you don't say anything, the court assumes everything the debt collector says is 100% true.

Your first and most important piece of debt collector suing me advice is to find your deadline. This isn't a suggestion; it’s a hard cutoff.

In Michigan: If you were personally served (handed the papers), you usually have 21 days to respond. If you were served by mail or live outside the state, you have 28 days.

In Florida: For most civil cases, you have 20 calendar days to file a written response.

If you miss this window, the collector can file for a "Default," which is the legal equivalent of winning a game because the other team didn't show up. We want to make sure you're on the field and ready to play. For a deeper dive into these initial moments, check out our What to Do When Sued by a Debt Collector: Complete First Steps Guide or review the official guidance from the Consumer Financial Protection Bureau.

Understanding the Summons and Complaint

When you open that envelope, you’ll find two primary documents. They might look like gibberish at first, but they serve very specific purposes.

The Summons: This is the official notice from the court. It tells you that you are being sued and identifies the court handling the case. Most importantly, it tells you how long you have to respond.

The Complaint: This is where the "Plaintiff" (the person suing you) lists their grievances. It will contain numbered paragraphs alleging that you owe a certain amount of money to a specific company.

You are the "Defendant." The company suing you is the "Plaintiff." Sometimes the Plaintiff is a company you recognize (like a big bank), but often it’s a "debt buyer"—a company that bought your old debt for pennies on the dollar and is now trying to collect the full amount. Understanding the Difference Between Summons & Complaint in Debt Collection Lawsuit is key to knowing how to fight back.

The Danger of Default Judgments

We mentioned earlier that more than 70% of debt collection cases result in a default judgment. This is a staggering statistic. It means millions of people lose their cases simply because they were too intimidated or confused to file a piece of paper.

A default judgment is essentially a "blank check" for the debt collector. Once they have it, they can:

Garnish your wages: In both Michigan and Florida, a portion of your paycheck can be taken before you even see it.

Freeze your bank account: They can "levy" your account, meaning the bank hands your balance over to the collector.

Place liens on property: They can attach the debt to your home or car, making it impossible to sell or refinance without paying them first.

Ignoring the problem won't make it go away; it only makes the collector's job easier. To understand the full scope of what they can take, read Can Debt Collectors Take My Wages and Bank Account.

Expert Debt Collector Suing Me Advice for Your Defense

The most empowering thing you can learn is this: The burden of proof is on them. In a debt collection lawsuit, the debt collector must prove three things:

That you are the person who actually owes the debt.

That the amount they are claiming is accurate to the penny.

That they have the legal right to sue you (especially if they are a third-party debt buyer).

Often, debt buyers have very little paperwork. They might have a spreadsheet with your name on it, but they may lack the original contract or the "chain of title" showing how the debt moved from the original bank to them. If you don't challenge them, the court won't ask for this proof. If you do challenge them, they might realize they can't win and drop the case entirely.

Filing a Formal Answer: Essential Debt Collector Suing Me Advice

Your "Answer" is your formal response to the Complaint. For every numbered paragraph in their Complaint, you must respond. In Michigan and Florida, you generally have three choices for each allegation:

Admit: You agree the statement is true.

Deny: You state the statement is false. (This forces them to prove it).

Lack of Knowledge: You state you don't have enough information to know if it's true. (This also forces them to prove it).

In addition to responding to their claims, you can raise "Affirmative Defenses." These are legal reasons why you shouldn't have to pay, even if the debt was originally yours. Common defenses include the statute of limitations or that the debt was already paid. A Key to Strong Answer in a Collection Lawsuit: Solid Counter-Affidavit can be the difference between a win and a loss.

Verifying the Debt: More Debt Collector Suing Me Advice

Don't take the collector's word for it. Errors are incredibly common in the debt industry. Sometimes they sue the wrong person with a similar name, or they try to collect an amount that includes illegal fees and interest.

You have the right to demand "Discovery." This is a pre-trial phase where you can ask the Plaintiff for documents, such as the original signed agreement or a full breakdown of the account history. If they can't produce these, their case starts to crumble. It’s also vital to know Who is Suing Me: Original Creditor vs. Debt Buyer Explained, as your strategy might change depending on who is across the aisle.

Common Defenses and Your Rights Under the FDCPA

One of the most powerful tools in your arsenal is the Statute of Limitations. This is a law that sets a time limit on how long a creditor has to sue you. Once that time passes, the debt is "time-barred."

Debt Type | Michigan | Florida |

|---|---|---|

Written Contracts | 6 Years | 5 Years |

Oral Agreements | 6 Years | 4 Years |

Open-Ended Accounts (Credit Cards) | 6 Years | 4 Years |

Note: In some cases, making a small payment or even acknowledging the debt in writing can "restart the clock." This is why you should be very careful about communicating with collectors before you have a plan.

Fair Debt Collection Practices Act (FDCPA) Protections

The FDCPA is a federal law that protects you from abusive, deceptive, and unfair debt collection practices. Even if you owe the money, the collector must follow the rules. If they don't, you might be able to sue them for damages up to $1,000 plus your attorney fees.

Common violations include:

Calling you before 8 a.m. or after 9 p.m.

Using profane or abusive language.

Threatening you with arrest or jail time (which is illegal).

Contacting your boss or neighbors about your debt.

Failing to send a "Validation Notice" within five days of their first contact.

If a collector has been harassing you, keep a log of every call and save every letter. These are pieces of evidence that can be used as a counterclaim in your lawsuit.

Challenging the Collector's Standing

"Standing" is a legal term that basically means "Do you have the right to be here?" When a debt buyer like Midland Funding or Portfolio Recovery Associates sues you, they must prove they own the debt. This requires a "Chain of Assignment"—a paper trail showing the debt moving from the original creditor to them.

If there is a gap in that trail, they lack standing. You can challenge this by Filing a Counter-Affidavit When Answering a Debt Collection Lawsuit. This forces them to produce the actual purchase agreement, which they often don't want to show because it reveals how little they paid for your account.

Conclusion: Take Control of Your Case

The most important debt collector suing me advice we can give you is this: you have more power than you think. Debt collectors rely on your fear and your silence. When you stand up and demand proof, you break their business model.

At KillDebt, we believe that everyone deserves a fair fight, regardless of their bank account balance. That’s why we created a DIY legal defense system powered by ParkerGPT.

ParkerGPT isn't just a chatbot; it’s an AI trained on consumer debt law and real-world strategies developed over 30 years by veteran attorney Brian Parker. It doesn't just give you generic advice—it analyzes your specific lawsuit documents, identifies the collector's weaknesses, and helps you generate court-ready responses.

And for those who want to be truly prepared, we recently introduced the Court Tester. This is an AI courtroom simulation built on your actual case. You can upload your filings and, within minutes, "argue" your motion in front of an AI judge and against AI opposing counsel. It’s like a dress rehearsal for your defense, complete with a private AI co-counsel whispering strategy only you can see.

Don't let a debt collector dictate your financial future. Take the first step, file your Answer, and show them you aren't part of that 70% who gives up.

Ready to fight back? Learn more about our DIY legal defense services and start your journey toward being debt-free today.

Frequently Asked Questions (FAQ)

Will I go to jail for an unpaid debt?

No. This is one of the most common fears, and it is entirely unfounded. Debt collection is a civil matter, not a criminal one. You cannot be arrested or sent to jail for simply owing money or losing a debt collection lawsuit. The only rare exception is if you ignore a direct court order to appear for a "debtor's exam" after a judgment has been entered. Even then, you aren't in trouble for the debt; you're in trouble for "contempt of court" for ignoring the judge. As long as you respond to court papers, jail is not on the table. For more on this, read Debt Collection Lawsuit Myths: 7 Things That Won't Save You.

How does a lawsuit affect my credit score?

A lawsuit itself doesn't necessarily show up on your credit report immediately, but the underlying collection account does. If the collector wins and gets a judgment, that used to appear in the "Public Records" section of your credit report. However, due to changes in how credit bureaus report data, many civil judgments no longer appear on standard credit reports. That said, the impact is still felt. A judgment makes it much harder to get a mortgage or a car loan because lenders can see the outstanding debt and the risk of garnishment. Collection accounts generally stay on your report for seven years from the date the account first went delinquent.

Do I need a lawyer for a debt collection lawsuit?

Whether you need a lawyer depends on the size of the debt and the complexity of the case. • Pro Se (Self-Representation): Many people successfully defend themselves, especially in small claims court. • Legal Aid: If you are low-income, you may qualify for free legal help through organizations like Michigan Legal Help or various Florida legal aid societies. • Consumer Attorney: If the debt is large (e.g., $10,000+), hiring an attorney might save you more than it costs. Many people are now turning to "Legal Tech" solutions—tools that provide the guidance of an attorney at a fraction of the cost. Check out our guide on Do I Need a Lawyer for a Debt Collection Lawsuit to weigh your options.