What Happens When You Get Sued — and What to Do Right Now

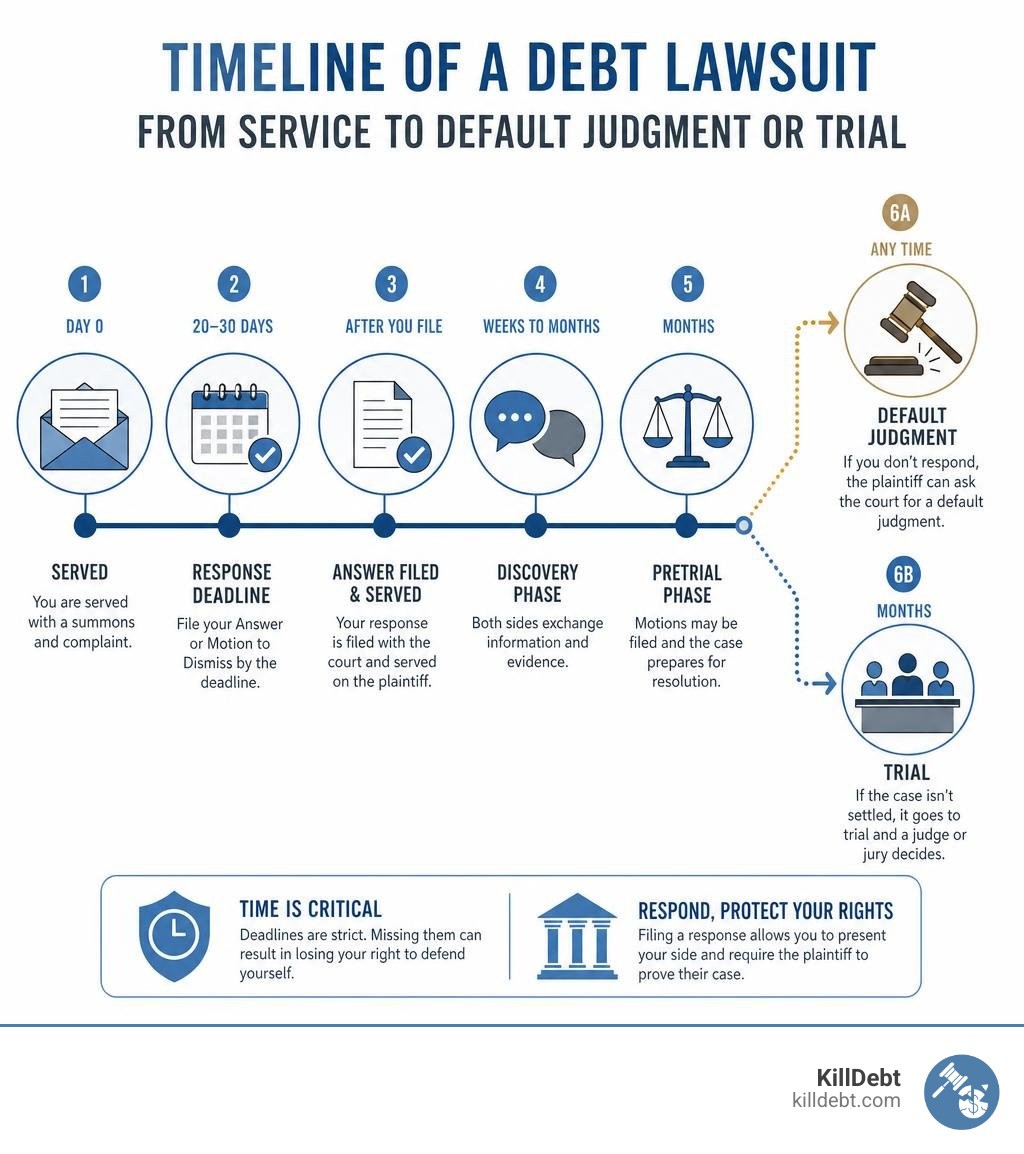

Responding to a civil complaint is one of the most time-sensitive things you'll ever do. Miss the deadline, and the court can rule against you without ever hearing your side of the story.

Here's the short version of what you need to know:

How to respond to a civil complaint — quick overview:

Check your deadline immediately. Most states give you 20–30 days from the date you were served. Weekends and holidays count.

Do not ignore it. Silence = default judgment. That means wage garnishment, bank levies, and no chance to fight back.

Decide how to respond. Your two main options are filing an Answer or filing a Motion to Dismiss.

Fill out the Answer form. Admit, deny, or state lack of knowledge for each numbered paragraph in the complaint.

Assert your defenses. List every affirmative defense that applies — you lose them forever if you don't include them now.

File with the court and serve the plaintiff. Keep a stamped copy for your records.

Getting that summons in the mail is a gut-punch moment. Most people freeze. Some hope it goes away on its own. It won't — and the clock is already running.

The good news? Filing a response forces the plaintiff to prove their case. You don't need to be a lawyer to do that. You just need to know the rules and follow them.

I'm Brian Parker, and I've spent over 30 years in the courtroom battling debt collectors, debt buyers, and collection law firms — which means responding to civil complaints is something I've done thousands of times. I founded KillDebt to put those same tools directly in your hands, so keep reading for a clear, step-by-step breakdown of exactly what to do next.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

Your Options for Responding to Civil Complaint: Answer vs. Motion

When a debt collector or credit card company decides to sue you, they initiate a formal lawsuit. To understand what you are looking at, you must first grasp the Difference Between Summons Complaint in Debt Collection Lawsuit.

The Summons is the official notice from the court telling you that you are being sued, where the lawsuit is filed, and how long you have to respond. The Complaint is the document containing the specific allegations against you—the "who, what, why, and how much" of the lawsuit.

When it comes to responding to a civil complaint, you generally have two paths to choose from: filing a written Answer or filing a pre-answer Motion. Making the right choice is critical because your response strategy dictates the entire trajectory of your case. For a deeper look into this strategic fork in the road, you can read about Responding to a Complaint in Federal Court: Answer or Motion? .

The Golden Rule of Responding to Civil Complaint: Watch the Deadline

The single most important rule in civil litigation is simple: never miss your deadline. If you fail to respond within the court’s strict timeframe, the plaintiff can immediately ask the court for a default.

To understand the severe consequences of letting this clock run out, see our guide on What Happens After Summons.

Because we focus our operations on helping consumers in Florida and Michigan, you must pay close attention to the specific timelines of these jurisdictions:

Florida State Courts: You have exactly 20 calendar days from the day you were personally served to file your response.

Michigan State Courts: You have 21 days to respond if you were served personally. If you were served by mail or outside the state of Michigan, you have 28 days.

Federal Courts: If you are sued in federal court (in Florida or Michigan), you generally have 21 days from service to file your response.

Do not assume weekends or holidays pause this countdown. If your deadline falls on a Saturday, Sunday, or legal holiday, your response is typically due on the next business day. However, waiting until the final hours is a recipe for disaster.

Deciding Between an Answer and a Motion to Dismiss

An Answer is your formal, paragraph-by-paragraph response to the allegations. It is the most common way to respond.

A Motion to Dismiss, on the other hand, is a request for the judge to throw the case out before you even file an Answer. You would typically file a Motion to Dismiss under specific legal circumstances, such as:

Improper Service: The plaintiff did not deliver the lawsuit papers to you according to state laws.

Lack of Jurisdiction: The court does not have the legal authority to hear the case or rule over you.

Failure to State a Claim: Even if everything the plaintiff says in the complaint is 100% true, they still have no legal right to win a judgment against you.

If you are unsure of which route to take, we break down the pros and cons in our guide on how to Respond to Debt Lawsuit. If you file a Motion to Dismiss and the judge denies it, you will still be required to file an Answer shortly after the ruling.

How to Fill Out a Civil Complaint Answer Form

If you decide to file an Answer, you need to draft a document that matches the court's strict formatting standards. The document must be printed on standard 8.5" x 11" white paper, double-spaced, with clear margins.

To see what a completed response looks like, you can review a Sample Answer to Complaint.

Every formal Answer consists of three primary sections:

The Caption: This is the header at the very top of the first page. It must match the Complaint exactly. It includes the name of the court, the names of the Plaintiff (the debt collector) and the Defendant (you), the Case Number, and the Judge's name.

The Body: This is where you address each numbered paragraph of the complaint and assert your defenses.

The Signature and Verification: You must sign and date the document. In some jurisdictions, you may also need to include a "verification" under penalty of perjury stating that your responses are true.

While general self-help resources like the Fill out Answer form to respond | California Courts | Self Help Guide offer general structural tips, you must use forms and language approved for your local Florida or Michigan court.

Step-by-Step Guide to Responding to Civil Complaint Paragraphs

The body of the Complaint will consist of numbered paragraphs. In your Answer, you must address every single paragraph individually. You cannot ignore a paragraph. For each numbered allegation, you have three legal options:

Admit: You agree that the statement in that paragraph is entirely true. (e.g., admitting your name and address).

Deny: You state that the allegation is false. Denying an allegation is not lying; it simply means you are demanding the plaintiff produce evidence to prove it.

Lack of Knowledge: You do not have enough information to know if the statement is true or false. In court, this has the legal effect of a denial, forcing the plaintiff to prove the claim.

If you are dealing with a simple case, you might be tempted to look for a General Denial Answer Form. However, general denials are rarely permitted in debt collection lawsuits in Florida and Michigan. Instead, you must go paragraph by paragraph.

For federal cases, templates like the Instructions: Answer – Responding to the Complaint – District of Nevada show how courts expect you to list your paragraph-by-paragraph responses clearly (e.g., "Defendant denies the allegations in Paragraphs 4, 5, and 6").

Asserting Affirmative Defenses and Counterclaims

After responding to the numbered paragraphs, you must list your Affirmative Defenses. An affirmative defense is a legal reason why the plaintiff should lose, even if their basic facts are true.

If you do not raise these defenses in your initial Answer, you legally waive them and cannot bring them up later in the lawsuit. To learn how to spot these opportunities, read our comprehensive Debt Lawsuit Defense Guide.

Affirmative Defense | What It Means | Real-World Debt Example |

|---|---|---|

Statute of Limitations | The legal time limit for filing a lawsuit has expired. | A debt buyer sues you in Florida on a credit card debt where the last payment was made over 5 years ago. |

Lack of Standing | The plaintiff does not have the legal right to sue you. | A junk debt buyer sues you but cannot produce the chain of title proving they purchased your specific account. |

Accord and Satisfaction | The debt was already settled and paid. | You settled the debt with the original creditor for 50% of the balance, and they accepted it as payment in full. |

Failure to State a Claim | The complaint lacks the necessary legal elements to win. | The collector sues you for breach of contract but fails to attach a copy of the contract or account statements. |

Serving and Filing Your Answer with the Court

Once your Answer is filled out, you must follow the correct procedure to file it with the court and serve it to the plaintiff. Failing to complete both steps properly can result in a default judgment.

To make sure you don't miss a step, read our guide on How to Answer a Debt Summons.

Here is the process you must follow:

Make Copies: Make at least three copies of your completed and signed Answer. One for the court, one for the plaintiff’s attorney, and one for your personal records.

Serve the Plaintiff: You must send a copy of your Answer to the plaintiff’s attorney. This is usually done by first-class mail.

Include a Certificate of Service: At the end of your Answer, you must include a signed "Certificate of Service" stating exactly when and how you sent the copy to the plaintiff's attorney.

File the Original: File the original Answer with the Clerk of Court. In Florida, this is typically done online via the Florida Courts E-Filing Portal. In Michigan, it can be done via MiFILE or in person at the clerk's office.

Get a Stamped Copy: If filing in person, bring your extra copy and ask the clerk to "date-stamp" it. This is your proof of filing.

If you are a low-income consumer in Florida, resources like the CONSUMER RESOURCES - Jacksonville Area Legal Aid offer detailed guides on local service rules and how to ask the court to waive your filing fees if any apply.

Local Rules and Jurisdictional Variations

Every county and courthouse has its own local rules. For example, some judges require specific cover sheets, while others have strict electronic filing mandates.

Before you submit your documents, call the local county clerk's office or visit their website to confirm if there are any additional local forms you must attach. To navigate these local quirks, consult our Fight Debt Collection Lawsuit Complete Guide.

Conclusion

Responding to a civil complaint doesn't have to be terrifying. By understanding the deadlines, answering each paragraph honestly, and asserting your affirmative defenses, you level the playing field and force the debt collector to prove their case.

At KillDebt, we provide a DIY legal defense system powered by ParkerGPT—an AI trained specifically on consumer debt law and real-world court strategies developed over 30+ years by defense attorney Brian Parker. We analyze your lawsuit documents, identify legal weaknesses, and generate customized, court-ready responses for a fraction of the cost of a traditional attorney.

Even better, we just rolled out our brand-new tool: Court Tester. This is an AI courtroom simulation built directly around your actual case. You can upload your real court filings, and within minutes, you'll practice arguing your case in front of an AI judge, facing off against an AI opposing counsel, while a private AI co-counsel whispers winning strategies that only you can see.

Don't let debt collectors win by default. Get started with KillDebt today and take control of your legal defense.

Get started with KillDebt pricing

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments.

Frequently Asked Questions (FAQ)

What happens if I miss the deadline to file my Answer?

If you miss the deadline, the plaintiff can file a motion for default. Once a default is entered, you lose your right to file an Answer or defend yourself. The court will then enter a default judgment, which allows the debt collector to garnish your wages, freeze your bank accounts, and place liens on your property. If you are running out of time and need professional document preparation, consider our Court Answer Drafting Service to get a customized, court-ready response generated quickly.

Does it cost money to file an Answer to a lawsuit?

In Florida and Michigan state courts, filing an Answer is generally free. Unlike the plaintiff, who must pay a fee to start the lawsuit, a defendant does not have to pay a fee just to file a basic Answer. However, if you file a counterclaim or a motion, there may be associated fees. You can review a Sample Answer to Debt Collection Lawsuit to see how a standard, fee-free response is structured.

What should I do if I cannot afford an attorney?

If you cannot afford a private attorney, you have options. You can contact local legal aid organizations in your area to see if you qualify for free legal representation. For Florida residents, resources like Completing an Answer to a Petition/Complaint and/or a Response to ... by Bay Area Legal Services provide excellent guidance for self-represented litigants. If you do not qualify for legal aid, you can represent yourself (pro se) using specialized legal technology tools designed for consumer defense.