When you are sued, the "burden of proof" is on the person suing you (the plaintiff). However, if you don't show up to the fight, they win by default. That is where the general denial answer form comes in. It is your way of saying to the court, "I disagree with everything they said, and I want them to prove it."

In civil procedure, a general denial is a broad stroke. Instead of answering paragraph one, then paragraph two, then paragraph three, you simply deny the entire complaint in its entirety. This is a powerful procedural tool because it forces the plaintiff to produce actual evidence for every single claim they’ve made—from the amount of the debt to their right to sue you in the first place.

For many defendants, especially those dealing with debt collectors, using a General Denial (PLD-050) or a similar state-specific template is the most efficient way to respond. It stops the clock on a default judgment and buys you the time needed to build a real defense. If you are feeling overwhelmed by the paperwork, our Debt Lawsuit Defense Guide can help you navigate the initial shock of being served. Knowing how to answer a debt summons is the difference between losing your wages to garnishment and keeping your financial freedom.

State-Specific Requirements and Deadlines for Filing

While the concept of a general denial is similar across the country, the "fine print" varies wildly depending on where you live. Because KillDebt specializes in helping folks in Florida and Michigan, we want to pay extra close attention to how these states handle your response.

In Florida, you have a strict 20-day window to file your answer. If you miss this, the creditor can move for a default judgment almost immediately. Florida courts generally require you to respond to each allegation, but a "General Denial" can be effective if you truly dispute every material fact. Under Florida Rule 1.110, you must be careful—any allegation you don't deny is considered "admitted" by the court.

In Michigan, the process is governed by specific court rules that require a bit more detail. While you can deny allegations generally, Michigan courts often prefer the use of the MC 03, Answer (Civil). This form allows you to check boxes or write in your denials.

Here is a quick look at the landscape:

State | Rule Reference | Key Deadline |

|---|---|---|

Florida | Rule 1.140 | 20 Days |

Michigan | MCR 2.108 | 21 Days (28 if served by mail) |

Texas | Rule 92 | 20 days + Monday @ 10 AM |

Alabama | Rule 12(a)(1) | 30 Days |

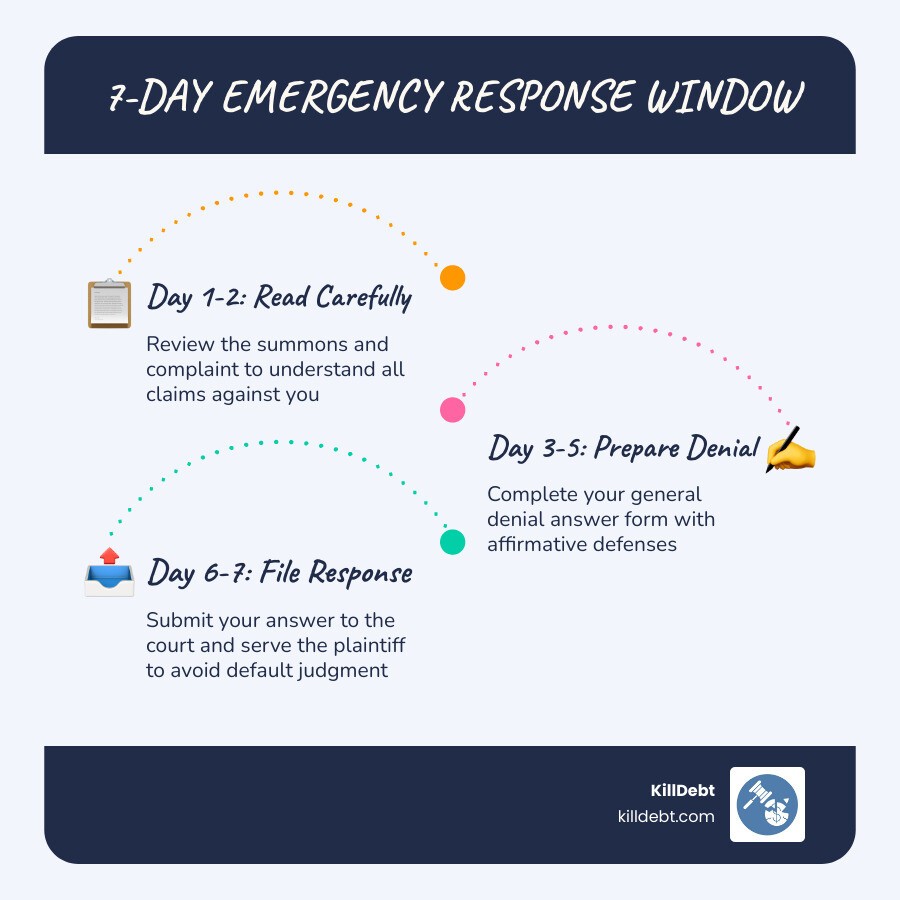

Regardless of where you are, the timeline of a debt collection lawsuit moves fast. You need to know exactly what to do in the first 7 days to ensure you don't waive your rights.

When to Use a Specific vs. General Denial Answer Form

Not every case allows for a general denial answer form. You have to look at the "Complaint" or "Petition" you were served with.

Verified Complaints: If the plaintiff signed the complaint under penalty of perjury (verified it), many states require you to provide a "Specific Denial." This means you must respond to every numbered paragraph individually.

Limited Civil Cases: In places like California, you can use a general denial for cases under $35,000, but only if the complaint isn't verified.

Amount in Controversy: If the debt is small (often under $1,000), courts are much more lenient and almost always allow a simple general denial form.

If you are unsure which one to use, it is usually safer to use a specific denial format where you address each paragraph. Our Fight Debt Collection Lawsuit: Complete Guide breaks down these nuances so you don't get tripped up by technicalities.

Essential Components of a General Denial Answer Form

A valid answer is more than just a piece of paper that says "I didn't do it." To be "court-ready," your general denial answer form should include:

The Caption: This is the header that includes the court name, the parties (Plaintiff vs. Defendant), and the Case Number. Copy this exactly from the Summons you received.

The Denial: A clear statement that you deny all allegations.

Affirmative Defenses: These are legal "reasons" why you shouldn't have to pay, even if the debt was originally yours (e.g., the Statute of Limitations has expired).

Verification/Unsworn Declaration: Some states require you to sign the document under penalty of perjury.

Certificate of Service: This is a statement telling the court that you sent a copy of your answer to the plaintiff's attorney.

We provide a Sample Answer to Debt Collection Lawsuit that shows exactly how these pieces fit together. In some cases, you may also need to include a counter-affidavit if the plaintiff attached a "sworn account" to their lawsuit.

Strategic Impact: Affirmative Defenses and Discovery

Filing your general denial answer form is just the beginning. The real "teeth" of your defense lie in your Affirmative Defenses.

An affirmative defense is a fact that, if proven, defeats the plaintiff's claim even if everything they said is true. Common examples include:

Statute of Limitations: The debt is too old to sue over (in Florida, this is usually 5 years for written contracts; in Michigan, it is 6 years).

Lack of Standing: The company suing you (a debt buyer) hasn't proven they actually own the debt.

Accord and Satisfaction: You already settled this debt for a specific amount.

If you don't list these defenses in your initial answer, you might waive them forever. That means you can't bring them up later at trial. This is why a solid counter-affidavit and a well-drafted list of defenses are so critical. Once the answer is filed, the case moves into "Discovery," where you can demand the plaintiff show you the original contract and the chain of title for the debt.

Risks of Improper Filing and Default Judgments

The biggest risk in a lawsuit isn't losing at trial—it's losing because you didn't show up. If you fail to file a general denial answer form on time, or if you file it incorrectly (like forgetting to serve the other side), the court will enter a Default Judgment.

A default judgment is a "win" for the debt collector by forfeit. With that judgment in hand, they can:

Garnish your wages: Take a percentage of your paycheck before you even see it.

Freeze your bank account: Levy your funds to pay the debt.

Place liens on property: Make it impossible to sell your home or car without paying them first.

Many people fall for debt collection lawsuit myths, believing that if they ignore the papers, the problem will go away. It won't. The only way to stop the "Judgment Entered" stamp is to take action. If you've just been served, follow our First Steps Guide to protect your assets.

Conclusion

Facing a lawsuit is stressful, but you don't have to do it alone. The general denial answer form is your first line of defense, and at KillDebt, we’ve built the tools to make sure that defense is ironclad.

Our system is powered by ParkerGPT, an AI trained on over 30 years of real-world debt defense strategies from attorney Brian Parker. We don't just give you a generic template; we analyze your specific lawsuit documents to find the weaknesses the debt collectors are trying to hide.

Want to see how you'll fare in court? Use our brand new Court Tester. It’s an AI courtroom simulation where you can upload your filings and argue your motion in front of an AI judge. You'll face AI opposing counsel while a private AI co-counsel whispers winning strategies directly to you. It’s the ultimate "practice run" before the real deal.

Don't let a debt collector take your hard-earned money by default. Take control of your defense today and fight back with the expertise of a seasoned attorney at a fraction of the cost.

Frequently Asked Questions (FAQ)

What is the difference between a general denial and a specific denial?

A general denial is one statement that denies everything in the lawsuit. A specific denial responds to each paragraph of the complaint individually (e.g., "Defendant admits the allegations in paragraph 1 but denies the allegations in paragraph 2"). Specific denials are often required if the complaint is "verified" or if the case is in a higher-level court.

Can I file a general denial if the complaint is verified?

In many jurisdictions, no. If the plaintiff has sworn to the truth of the complaint under oath (verified it), you must usually provide a verified specific denial. Filing a general denial against a verified complaint can sometimes be treated as an admission of the facts.

What happens if I miss the 20-day deadline to file my answer?

In Florida, the plaintiff can immediately file a "Motion for Default." If the clerk enters a default, you lose your right to contest the debt unless you can prove "excusable neglect" and a "meritorious defense" through a motion to set aside the default—which is much harder than simply filing the answer on time.