What to Do When You Need to Respond to a Debt Lawsuit

If you need to respond to a debt lawsuit, here are the most important steps to take right now:

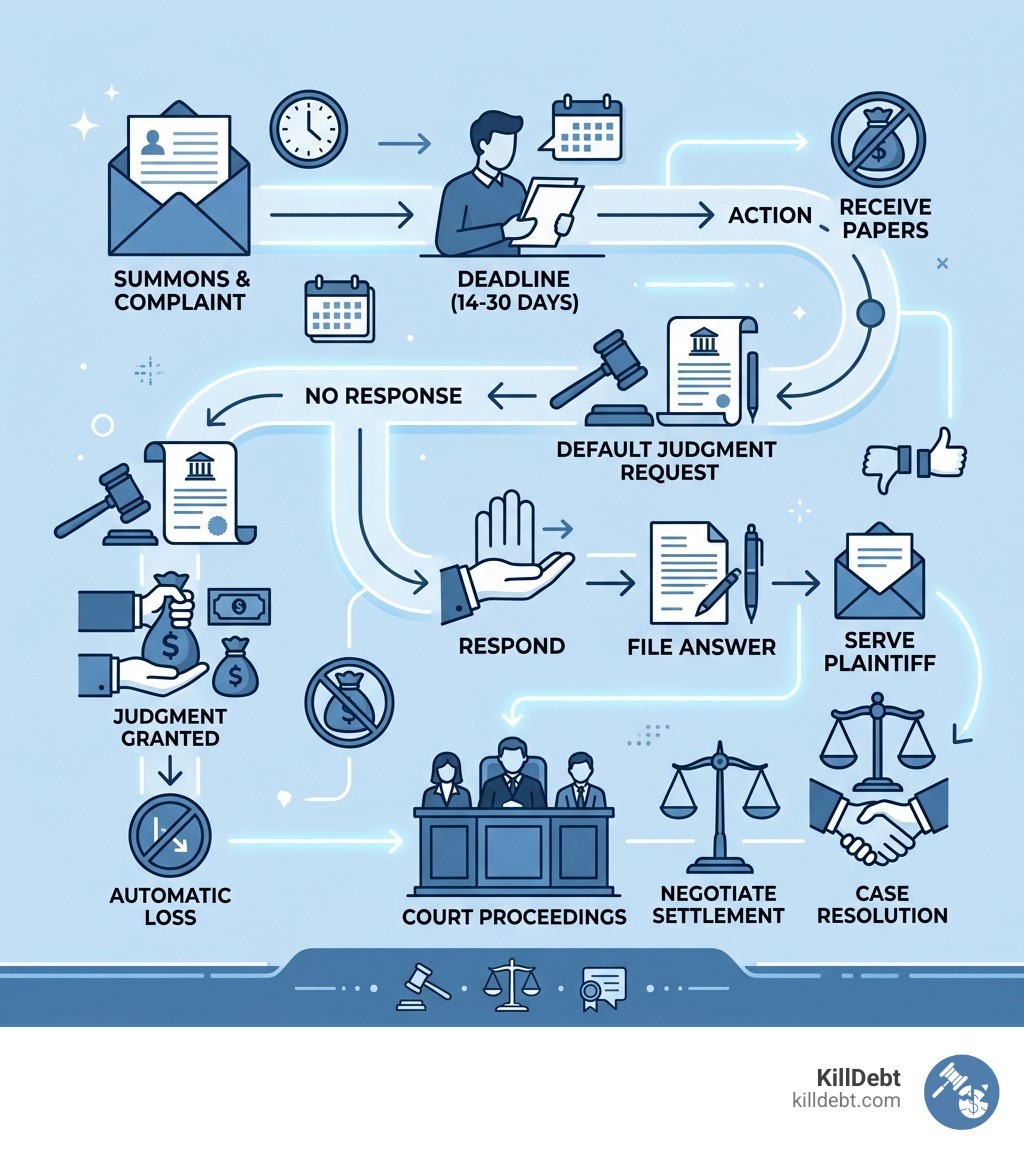

Don't ignore it — failing to respond means you automatically lose

Check your deadline — you typically have 14–30 days depending on your state

Get the right forms — in California, use form PLD-C-010 (Answer – Contract)

File your Answer — respond to each claim: admit, deny, or deny for lack of knowledge

Assert your defenses — statute of limitations, wrong amount, identity theft, and others

Serve the plaintiff — mail a copy of your Answer to the collector's attorney

Pay the filing fee or apply for a waiver — fees range from $225–$450 in California

Getting hit with a debt lawsuit is one of the most stressful legal situations a person can face. You open an envelope — or answer the door — and suddenly you're staring at a Summons and Complaint with a court case number and a deadline.

Most people freeze. That's exactly what debt collectors count on.

An estimated 70–90% of people sued for debt never respond at all. The result? The collector wins automatically — without ever having to prove they own the debt, that the amount is correct, or that they even had the legal right to sue.

Filing an Answer changes everything. It forces the other side to prove their case with real evidence. It opens the door to settlement. And it protects you from wage garnishment, bank levies, and property liens.

You don't need to be a lawyer to respond. You just need to know the steps — and act before your deadline.

Immediate Steps After Receiving a Summons and Complaint

The moment you receive those legal papers in April 2026, the clock starts ticking. It’s jarring, and it’s normal to feel a wave of fear or paralysis. However, your first and most powerful move is to understand exactly what you’ve been handed.

A debt lawsuit begins with two primary documents: the Summons and the Complaint. It is vital to understand the Difference Between Summons & Complaint in Debt Collection Lawsuit. The Summons is the court’s notice telling you that you are being sued and providing the deadline for your response. The Complaint is the list of allegations the creditor is making against you—essentially their "side of the story."

We recommend you immediately follow this What to Do When Sued by a Debt Collector: Complete First Steps Guide. Start by checking the Case Status with your local court. You can often do this online by searching for the case number listed on the Summons.

While reviewing the documents, keep your rights in mind. Under the federal Fair Debt Collection Practices Act (FDCPA), collectors are prohibited from using deceptive, unfair, or abusive practices. If you live in Florida or Michigan, these federal protections are your shield. Furthermore, if you are being sued in California, you are also protected by the Rosenthal Act, which extends similar protections to original creditors, not just third-party collectors.

How to Respond to Debt Lawsuit Deadlines and Requirements

When you need to respond to a debt lawsuit, the deadline is your absolute priority. If you miss this window, the court will likely enter a Default Judgment against you. This is the "forfeit" of the legal world. Once a collector has a judgment, they can legally pursue Wage Garnishment (taking a portion of your paycheck), Bank Levies (freezing your accounts), or Property Liens.

The Time to Respond Debt Collection Lawsuit varies significantly depending on where you are and how you were served. For example, the Respond to a debt lawsuit | California Courts | Self Help Guide notes that you generally have 30 days to file your response. However, if you were "substitute served" (the papers were left with someone else at your home or office), you might have 40 days.

Understanding State-Specific Deadlines to Respond to Debt Lawsuit

Each state has its own rulebook. Since we focus on helping those in Florida and Michigan, here is the breakdown:

Florida: You typically have only 20 days to file a written response after being served. Florida courts move quickly, and missing this 20-day mark can lead to an immediate default.

Michigan: The deadline is generally 21 days if you were served in person, or 28 days if you were served by mail or outside the state. You can find more details in this guide on Michigan Debt Collection Summons: How To Respond - Upsolve.

California: As mentioned, the standard window is 30 days.

Consequences of Failing to Respond to Debt Lawsuit

If you ignore the lawsuit, you aren't just letting a debt go—you are inviting an automatic loss. This means the court accepts everything the collector said as 100% true. Beyond garnishments, this results in:

Property Liens: Preventing you from selling or refinancing your home.

Severe Credit Damage: A judgment can haunt your credit report for up to 7 years.

Additional Costs: You will likely be ordered to pay the collector’s attorney fees and court costs, which can add thousands to the original debt.

If you’ve received papers, read our guide on what happens when you Have You Been Sued by a Debt Collector to understand the full gravity of a default.

Drafting Your Answer: Forms, Defenses, and Filing Fees

Your formal response to the court is called an Answer. This is not a letter or a phone call; it is a legal document where you respond to every numbered paragraph in the Complaint.

For each allegation, you have three choices:

Admit: You agree the statement is true.

Deny: You challenge the statement and force the plaintiff to prove it.

Lack of Knowledge: You don't have enough information to know if it's true or false (this effectively acts as a denial).

For a starting point on what this looks like, review this Sample Answer to Debt Collection Lawsuit.

Common Affirmative Defenses When You Respond to Debt Lawsuit

An affirmative defense is a legal reason why you shouldn't have to pay, even if the facts in the Complaint are mostly true. You must list these in your initial Answer, or you may lose the right to use them later.

Statute of Limitations: The debt is too old to be sued upon. In Florida and California, this is typically 4 years for credit cards.

Lack of Standing: The company suing you (often a debt buyer) cannot prove they actually own the debt or have a legal right to sue you.

Identity Theft: The debt was never yours to begin with.

Paid Debt: You have already settled or paid this account in full.

In some cases, you may also need to consider Filing a Counter-Affidavit When Answering a Debt Collection Lawsuit. This is often the Key to Strong Answer in a Collection Lawsuit: Solid Counter-Affidavit because it specifically disputes the accuracy of the sworn statements provided by the creditor.

Navigating Court Filing Fees and Fee Waivers

Filing an Answer isn't always free. In California, filing fees are some of the highest in the country, ranging from $225 to $450 depending on the county and the amount of the debt. Florida also requires fees for small claims and civil cases, which you can learn about through About Small Claims Collection Lawsuits - The Florida Bar.

If you cannot afford these fees, do not let that stop you from responding. You can file Form FW-001 (Request to Waive Court Fees) in California, or similar "Indigent" status forms in Florida and Michigan. If approved, the court will allow you to file your Answer for free.

Location | Typical Filing Fee Range | Fee Waiver Form |

|---|---|---|

California | $225 – $450 | FW-001 |

Florida | $55 – $300+ | Application for Indigent Status |

Michigan | $20 – $150+ | Fee Waiver Request (MC 20) |

Serving the Plaintiff and Finalizing Your Defense

Once your Answer is drafted, you must "serve" it. This means providing a copy to the plaintiff’s attorney. You cannot just drop it in the mail and call it a day; you must file a Proof of Service with the court to prove the other side received it.

After you respond to a debt lawsuit, the case enters the Discovery Phase. This is where both sides exchange information and evidence. This is often the best time for Settlement Negotiation. Debt collectors are often willing to settle for 40% to 60% of the total debt amount once they see you are willing to fight. In fact, for older debts or debt buyers, settlements can sometimes be as low as 10% to 30%.

To see what the road ahead looks like, check the Debt Collection Lawsuit Timeline: What Happens Next After You're Served and our Fight Debt Collection Lawsuit: Complete Guide.

Exploring Debt Relief and Legal Assistance Options

If the debt is overwhelming and you have multiple creditors suing you, it might be time to look at broader options.

Chapter 7 Bankruptcy: This provides an Automatic Stay, which immediately halts all debt lawsuits and garnishments.

Legal Aid/Pro Bono: If you are low-income, you may qualify for free legal assistance through organizations like the Northwest Justice Project or local Florida legal aid offices.

Self-Representation: Many people successfully defend themselves. If you are wondering, "Do I Need a Lawyer for a Debt Collection Lawsuit", the answer is often "not necessarily," especially with the right AI-powered tools.

For those appearing in lower courts, understanding a Justice Court Debt Answer can help simplify the procedural hurdles.

Conclusion

At KillDebt, we believe that the legal system shouldn't only work for those who can afford expensive attorneys. We provide a DIY legal defense system powered by ParkerGPT, an AI trained specifically on consumer debt law and real-world strategies developed over 30 years by attorney Brian Parker.

Our platform analyzes your lawsuit documents, identifies the collector's weaknesses, and generates court-ready responses. We’ve even introduced the Court Tester, an AI courtroom simulation where you can practice arguing your case against an AI judge before you ever step foot in a real courtroom.

Don't let a debt collector take your wages or freeze your future. Use the tools available to you, stand your ground, and Protect your wages today. Whether you are in Florida, Michigan, or California, the first step is always the same: respond.

Get started with KillDebt pricing

Important Legal Disclaimer

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments.

Frequently Asked Questions (FAQ)

Can I settle the debt after filing an Answer?

Yes! In fact, filing an Answer makes settlement more likely. It shows the collector that you aren't an easy target and that they will have to spend money on legal fees to beat you. Most settlements happen after the Answer is filed but before the trial begins.

What is the statute of limitations on debt in California?

In California, the statute of limitations for most consumer debts (credit cards, medical bills, auto loans) is 4 years. For mortgages and personal loans, it is 6 years. Once this time has passed from the date of your last payment or activity, the debt is "time-barred," and you can use this as a powerful affirmative defense.

How do I check the status of my court case?

You can check the status by visiting the court clerk’s office or searching the court’s online portal using your case number. It is vital to monitor your case status regularly to ensure you don't miss any hearing dates or new filings from the plaintiff.