What a Sample Answer to Complaint Actually Looks Like (And Why You Need One Fast)

A sample answer to complaint is a formal written response you file with the court after being served with a lawsuit — and if you've just received a summons, you may have as little as 21 days to file one before a default judgment is entered against you.

Here's the core structure of a sample answer to complaint at a glance:

Section | What It Does |

|---|---|

Caption | Lists the court, parties, and case number |

Paragraph Responses | Admits, denies, or states lack of knowledge for each allegation |

Affirmative Defenses | Legal reasons the plaintiff's claim should fail |

Counterclaims (if any) | Claims you bring against the plaintiff |

Prayer for Relief | States what you want the court to do |

Certificate of Service | Confirms you sent a copy to the other side |

Signature Block | Your signed certification under Rule 11 |

Missing even one of these sections — or filing even one day late — can cost you the case before it starts.

This guide walks you through every part of the process: how to read the complaint you were served, how to respond paragraph by paragraph, which affirmative defenses apply to your situation, and how to file correctly.

I'm Brian Parker, founder of KillDebt, and I've spent over 30 years in the courtroom fighting debt collectors, debt buyers, and collection law firms — drafting and reviewing countless answers to complaints along the way. I know exactly what works, what gets defendants into trouble, and how to give you the same edge in this guide.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

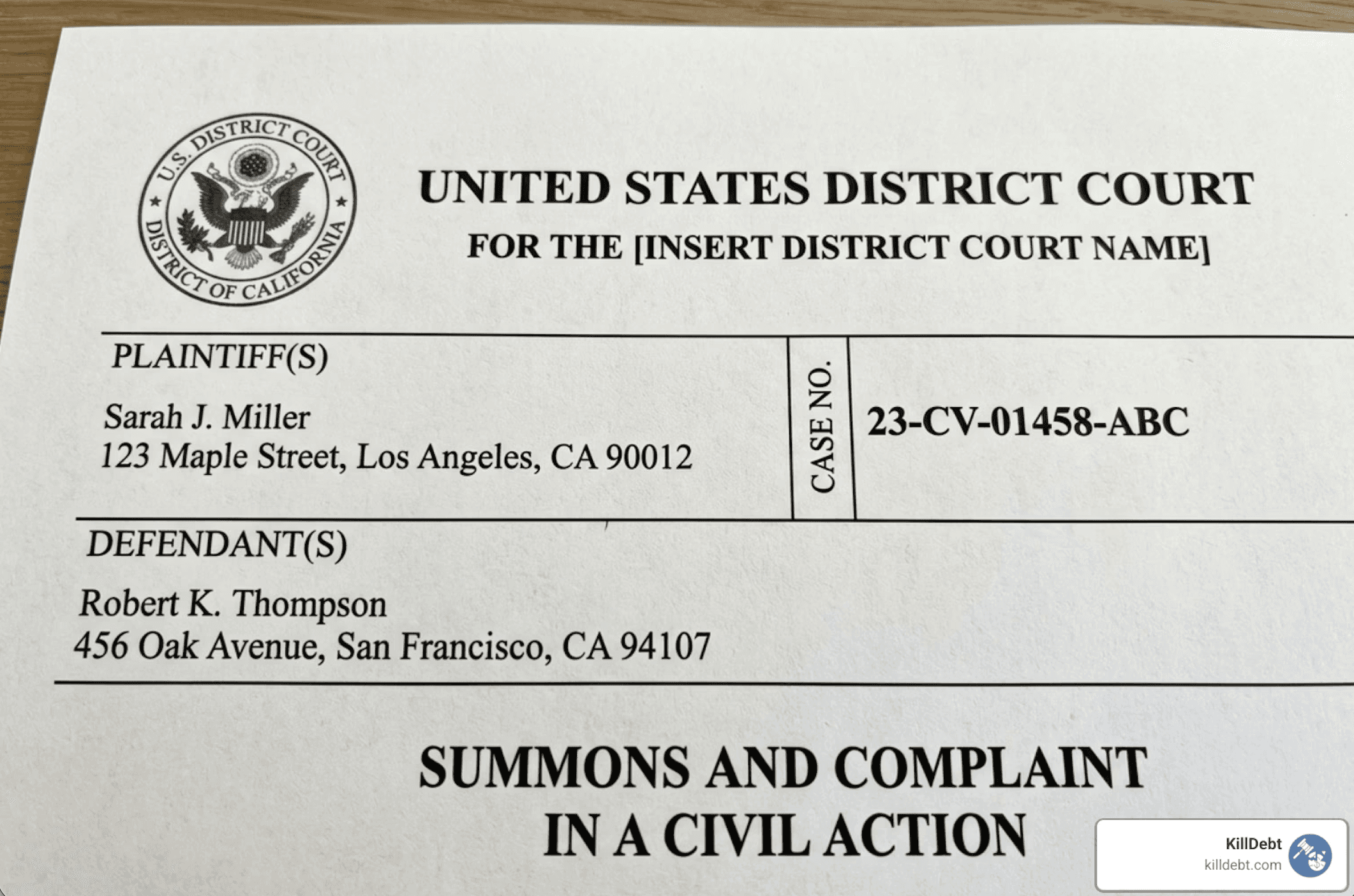

Understanding the Summons and Complaint in a Debt Lawsuit

When a debt collector decides to take legal action, they do not just send a scary letter. They initiate a formal lawsuit. This process begins when you are served with two distinct but deeply connected documents: the Summons and the Complaint.

Understanding the Difference Between Summons and Complaint in Debt Collection Lawsuit is your very first line of defense.

The Summons: This is the court’s official notice to you. It announces that you are being sued, identifies the court handling the case, and issues a strict deadline to respond.

The Complaint: This is the document where the plaintiff (the debt collector or creditor) lists their specific allegations against you. It is organized into numbered paragraphs detailing who they are, why they believe you owe them money, the exact amount they are seeking, and their legal claims (such as breach of contract or account stated).

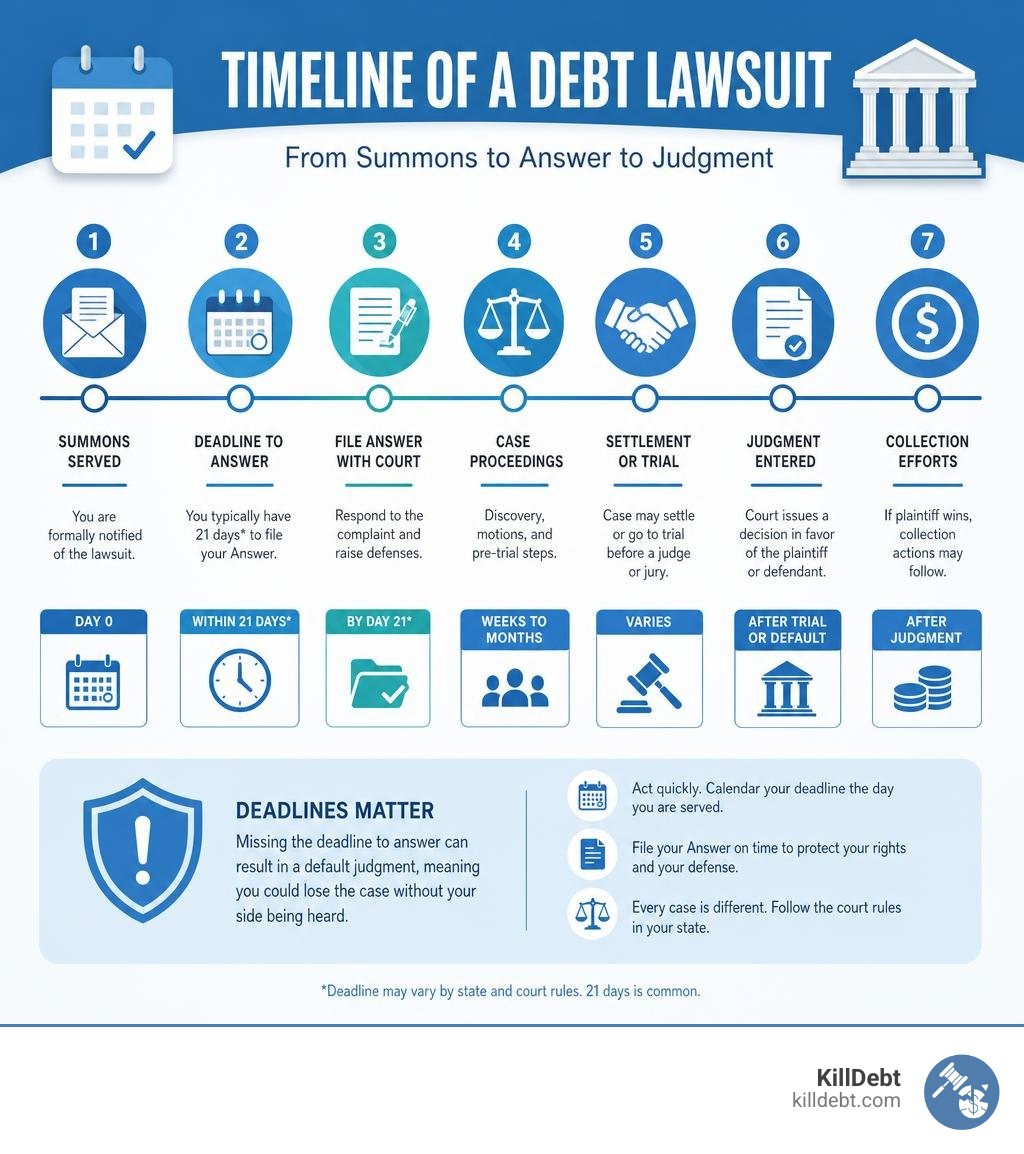

Under Federal Rule of Civil Procedure (FRCP) 12(a), a defendant in federal court must serve an answer within 21 days after being served with the summons and complaint. If you are in state court, the timelines vary but remain incredibly strict:

Florida: Under Florida Rules of Civil Procedure, you have only 20 calendar days from the date of service to file your written response.

Michigan: Under Michigan Court Rules, you have 21 days to answer if you were served in person, or 28 days if you were served by mail or if service was executed outside the state.

If you fail to file a timely response, the plaintiff can immediately ask the court for a default judgment. A default judgment means the debt collector wins automatically. With this judgment in hand, they can legally garnish your wages, freeze your bank accounts, and place liens on your property.

To prevent this, you must learn How to Answer a Debt Summons and file a formal response. Your answer is not a place to explain your life story or complain about your financial hardships; it is a highly structured legal document designed to address the plaintiff's allegations systematically.

Key Components of a Sample Answer to Complaint

A proper response must follow standard legal formatting. If you look at a professional The Defendant’s Answer to the Complaint, you will notice that it is broken down into clear, organized sections.

Every sample answer to complaint must include these essential components:

The Caption: Located at the top of the first page, this identifies the court (e.g., "In the District Court for the County of Oakland, State of Michigan" or "In the County Court in and for Broward County, Florida"), the names of the Plaintiff and Defendant, and the Case Number.

The Title: A clear title centered below the caption, such as "Defendant’s Answer to Plaintiff's Complaint."

Paragraph Responses: This is the core of your answer where you address every numbered allegation in the complaint.

Affirmative Defenses: This is where you assert legal reasons why the plaintiff should not win, even if some of their factual claims are true.

Prayer for Relief: A brief concluding statement asking the court to dismiss the lawsuit with prejudice and award you court costs or attorney fees if applicable.

Certificate of Service: A signed statement at the very end certifying that you have mailed or electronically delivered a copy of your answer to the plaintiff's attorney on a specific date.

How to Respond to Allegations in a Sample Answer to Complaint

The most critical part of drafting your response is addressing the allegations. Under FRCP 8(b) (and corresponding state rules in Florida and Michigan), you must respond to every single numbered paragraph in the plaintiff's complaint.

For each paragraph, you have exactly three options:

Admit: You agree that the entire statement in that paragraph is completely true. (For example, you might admit Paragraph 1 if it simply states your legal name and address).

Deny: You dispute the accuracy of the statement. Denying an allegation forces the plaintiff to actually produce evidence to prove it in court. If you believe an allegation is even partially incorrect, or if you want to hold the collector to their strict burden of proof, you should deny it.

Lack of Knowledge or Information: You state that you do not have sufficient information to form a belief as to the truth of the allegation. This legally operates as a denial and is highly useful when a third-party debt buyer makes claims about their corporate structure, assignment chains, or internal record-keeping that you cannot verify.

When customizing a Sample Answer to Debt Collection Lawsuit, you must match your answers exactly to the paragraph numbers of the complaint. If the complaint has 15 paragraphs, your answer must have 15 corresponding responses.

Pro Tip: A common mistake made by self-represented defendants is failing to deny legal conclusions or requests for damages. If a paragraph says, "Defendant owes Plaintiff $5,000," you must explicitly deny that paragraph. If you leave any paragraph unaddressed, the court will legally treat your silence as an admission of that fact under FRCP 8(b)(6).

Formatting Your Sample Answer to Complaint

Your document must comply with standard court rules to be accepted by the court clerk. Under Federal Rule of Civil Procedure 10 (and local state equivalents), your answer must use numbered paragraphs, standard margins, and clear, legible fonts.

When learning How to Write an Answer to a Credit Card Lawsuit, keep these formatting rules in mind:

Match the Style: Copy the exact font style, court name format, and party layout from the Summons you received.

The Signature Block: You must sign the document. If you are representing yourself (acting pro se), you must include your printed name, physical address, phone number, and email address.

Wet Signature: Many courts in Florida and Michigan require a physical, "wet" signature on paper filings, while others utilize specific electronic filing systems. Always check your local court's administrative rules.

Rule 11 Certification: By signing the answer, you are certifying to the court under Rule 11 that your responses are not being presented for an improper purpose (like delaying the case) and that your factual denials have evidentiary support or are reasonably based on a lack of information.

Common Affirmative Defenses and Counterclaims

An answer is your primary—and often only—opportunity to present affirmative defenses. An affirmative defense is a legal reason why the plaintiff’s claim must fail, even if you did not pay the debt in question. If you do not raise these defenses in your initial answer, you legally waive them forever.

Common affirmative defenses in consumer debt cases include:

Statute of Limitations: The legal time limit for filing a lawsuit has expired. (In Florida, the statute of limitations for most consumer debt and credit cards is 5 years; in Michigan, it is typically 6 years).

Failure to State a Claim: The plaintiff's complaint does not contain enough legal or factual basis to show they have a valid claim against you.

Lack of Standing: The plaintiff is a third-party debt buyer and has failed to show a proper chain of assignment proving they actually own your specific debt.

Laches: The plaintiff waited an unreasonable amount of time to file the suit, causing you legal or financial prejudice.

In complex litigation, defendants frequently assert a wide array of defenses to protect their rights. For example, in the federal wage case 3:13-cv-01461-G, the defendants asserted 23 separate affirmative defenses. In another federal case, 2:19-CV-00219-SAB, the defendant asserted 15 affirmative defenses. While you should not throw random defenses at the wall hoping they stick, you must be thorough.

Additionally, you can assert Counterclaims if the debt collector violated consumer protection laws—such as the Fair Debt Collection Practices Act (FDCPA) or state-specific laws like the Michigan Regulation of Collection Practices Act (MRCPA) or the Florida Consumer Collection Practices Act (FCCPA).

To understand your options fully, consult a comprehensive Debt Lawsuit Defense Guide and review the official federal guidelines on RESPONDING TO A COMPLAINT.

Affirmative Defenses vs. Counterclaims

Feature | Affirmative Defense | Counterclaim |

|---|---|---|

Definition | A legal shield that defeats or mitigates the plaintiff's claim. | An offensive legal claim asserting that the plaintiff harmed you. |

Goal | To get the plaintiff's lawsuit dismissed. | To win monetary damages or statutory penalties from the plaintiff. |

Examples | Statute of Limitations, Lack of Standing, Prior Payment. | FDCPA violations, illegal robo-calling, harassment. |

Waiver Risk | Waived permanently if not raised in your Answer. | May be brought later if not "compulsory," but best filed with the Answer. |

Conclusion: Take Control of Your Defense with KillDebt

Receiving a court summons is stressful, but ignoring it is the only guaranteed way to lose. By using a structured sample answer to complaint and asserting your legal rights, you force the debt collector to play by the rules and prove their case—something third-party debt buyers often cannot do.

At KillDebt, we believe that everyone deserves access to a powerful, professional legal defense without paying thousands of dollars in attorney fees. Our platform features ParkerGPT, an advanced AI trained on consumer debt law and real-world defense strategies developed over 30+ years by veteran consumer defense attorney Brian Parker.

Unlike generic document generators, KillDebt analyzes your specific lawsuit papers, uncovers hidden procedural defects, and builds a customized, court-ready answer tailored for Florida and Michigan courts.

Ready to see how your case holds up? We just introduced Court Tester, our brand-new AI courtroom simulation built on the actual facts of your case. Simply upload your lawsuit documents, and within minutes, you will be practicing your arguments in front of an AI judge, facing AI opposing counsel, and receiving strategic, real-time advice from a private AI co-counsel.

Don't let debt collectors run over you. Protect your rights with KillDebt today and turn the tables on collection lawsuits.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

Frequently Asked Questions (FAQ)

What happens if I miss the deadline to file an answer?

If you miss your deadline (20 days in Florida, 21–28 days in Michigan, or 21 days in federal court), the plaintiff will file a motion for a default judgment. Once the judge signs this judgment, the collector has the legal power to garnish your wages, place a levy on your bank accounts, or seize non-exempt personal property. If you have missed the deadline, you must act immediately to file a motion to set aside the default, which requires showing "excusable neglect" and a meritorious defense.

Do I need to pay a fee to file my answer?

Filing fees vary heavily by state and county. • Michigan: Most Michigan district and circuit courts do not charge a fee to file a standard answer to a civil complaint. • Florida: Many Florida county courts do charge a fee to file an answer or responsive pleading, depending on the amount of the claim (often ranging from $80 to $300). If you cannot afford the filing fee, you can ask the court clerk for a "Fee Waiver" or "Indigent Status" application. If approved, the court will waive your filing fees.

Can I settle my debt after filing an answer?

Yes! Filing an answer does not stop you from negotiating. In fact, filing a strong sample answer to complaint showing that you are willing to fight actually increases your leverage. Debt buyers purchase accounts for pennies on the dollar and expect easy default judgments. When you show that you know your rights, they are far more likely to offer a reasonable debt settlement agreement to avoid the high cost of ongoing litigation.