What to Do Right Now If You've Been Sued for Credit Card Debt

Knowing how to write an answer to a credit card lawsuit could be the difference between keeping your paycheck and losing it to wage garnishment.

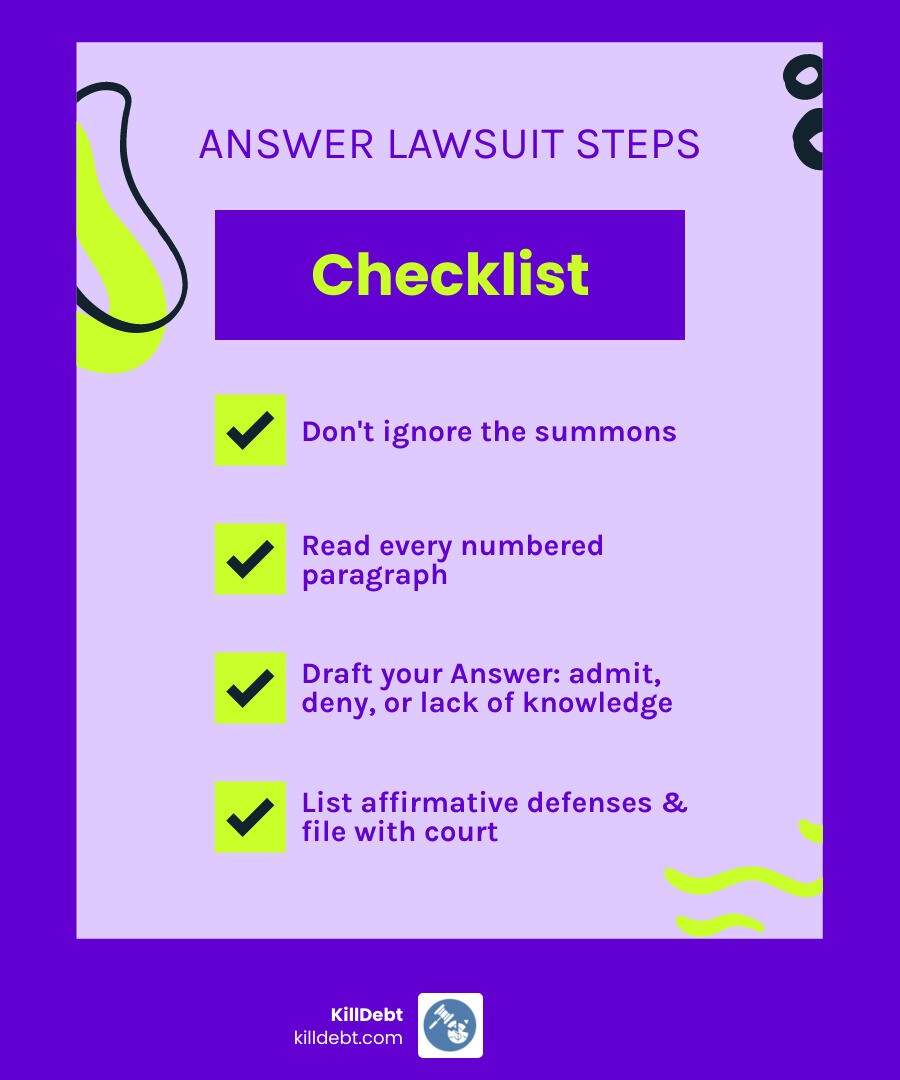

Here's the short version of what you need to do:

Don't ignore the summons. You have 20–30 days to respond, depending on your state.

Get the complaint. Read every numbered paragraph carefully.

Draft your Answer. Respond to each paragraph: admit, deny, or state lack of knowledge.

List your affirmative defenses. Statute of limitations, improper service, lack of standing — include everything that applies.

File with the court and serve the plaintiff. Keep copies of everything.

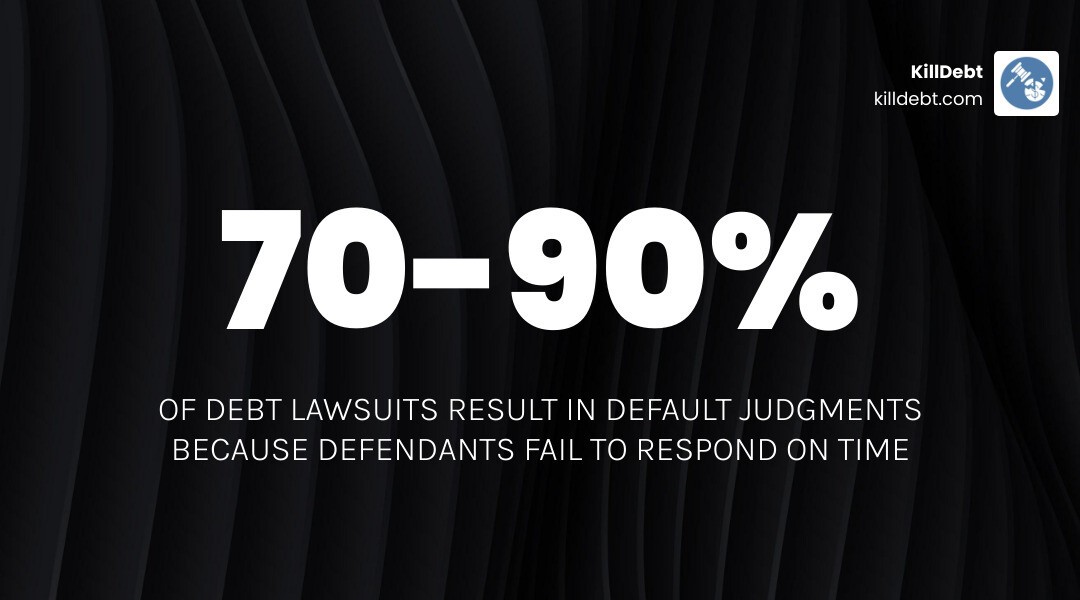

If you miss the deadline, the court can enter a default judgment against you — an automatic win for the creditor. That means they can garnish your wages, levy your bank account, or place a lien on your property. No trial needed.

More than 70% of people sued for debt lose by default simply because they didn't respond. You don't have to be one of them.

Receiving a summons is stressful. The legal language is confusing, the deadlines are tight, and the stakes are real. Debt collection law firms often file hundreds of lawsuits a day, counting on the fact that most people won't fight back. But here's the truth: simply filing an Answer forces the plaintiff to prove their case — and many collectors can't do that.

I'm Brian Parker. For over 30 years, I fought creditors, debt buyers, and collection law firms in courtrooms across the country, and I built KillDebt specifically to teach everyday people exactly how to write an answer to a credit card lawsuit — using the same strategies I used to protect thousands of consumers. Let's walk through it step by step.

Understanding the Summons and Complaint

When a process server knocks on your door or you find a thick envelope in your mail in May 2026, you aren't just looking at "paperwork." You are looking at the opening move in a legal battle. To understand how to write an answer to a credit card lawsuit, you first have to understand the two documents you just received.

The Summons: Your Official "Wake-Up Call"

The Summons is the court’s way of saying, "Hey, we’re talking to you." It identifies the court where the case was filed, the parties involved, and—most importantly—the deadline. In Florida and Michigan, this clock starts ticking the moment you are served.

Florida: You generally have 20 days to file a written response.

Michigan: You generally have 21 days if you were served personally (handed the papers).

The Complaint: The List of Accusations

The Complaint (sometimes called a Petition) is where the Plaintiff (the credit card company or debt buyer suing you) lists their Allegations. These are numbered paragraphs claiming that you opened an account, spent money, and failed to pay it back.

It is vital to understand the Difference Between Summons Complaint in Debt Collection Lawsuit so you don't get overwhelmed. The Complaint is not a "fact" yet; it is a list of claims that the Plaintiff must prove. If you don't show up to challenge them, the court assumes every word is true. This is why knowing What Happens After Summons is the first step toward winning.

How to Write an Answer to a Credit Card Lawsuit

Writing a legal response doesn't require a law degree, but it does require following a specific structure. Think of the Answer as your formal "counter-move." You aren't telling your life story here; you are responding to the Plaintiff's specific claims.

The Caption and Case Number

At the top of your Answer, you must copy the "Caption" from the Complaint exactly. This includes:

The name of the court (e.g., "In the Circuit Court of the Sixth Judicial Circuit, in and for Pinellas County, Florida").

The names of the Plaintiff and the Defendant (you).

The Case Number (or File Number).

If you get the case number wrong, the clerk might not be able to file your document, which could lead to a default judgment.

Structuring Your Response

Your Answer should mirror the Complaint. If the Complaint has 15 numbered paragraphs, your Answer should have 15 numbered responses. For every single paragraph, you have three legal options.

The Three Responses: Admit, Deny, or Lack Knowledge

Response | When to Use It | Legal Effect |

|---|---|---|

Admit | When the statement is 100% true (like your name or address). | You agree this fact is true; the Plaintiff no longer has to prove it. |

Deny | When the statement is wrong, or you want the Plaintiff to prove it. | The "Burden of Proof" stays on the Plaintiff to show evidence. |

Lack Knowledge | When you don't have enough info to say if it's true or false. | This acts as a legal denial, forcing the Plaintiff to prove the claim. |

Many people feel guilty about clicking "Deny," but in the legal world, denying an allegation is simply saying, "Prove it." According to How to Answer a Credit Card Lawsuit (with Pictures) - wikiHow Legal, if you aren't 100% sure about the exact dollar amount or the "chain of custody" of the debt, you should deny it or state that you lack sufficient knowledge.

Step 1: How to Write an Answer to a Credit Card Lawsuit Paragraph by Paragraph

When you sit down to write, take it one number at a time.

Paragraph 1: "The Defendant is a resident of Oakland County, Michigan."

Your Response: "Admit." (Since this is a simple fact of where you live).

Paragraph 2: "The Defendant owes Plaintiff the sum of $4,852.14."

Your Response: "Defendant denies the allegations in Paragraph 2 and demands strict proof thereof."

Why deny? Because credit card companies often add hidden fees, incorrect interest rates, or "zombie" charges. By denying, you force them to produce the original contract and a full accounting of the balance. If you are in Michigan, you can find helpful templates at Do-It-Yourself Civil Answer - Michigan Legal Help.

Common Mistakes When Learning How to Write an Answer to a Credit Card Lawsuit

We see the same errors over and over again. Avoiding these will put you ahead of 90% of other defendants:

Admitting Liability Too Early: People think being "honest" means admitting they owe the money. In court, you are entitled to see the evidence. If the Plaintiff is a third-party debt buyer (someone who bought the debt from the original bank), they often don't have the paperwork to prove they actually own your specific account.

Providing Too Much Information: Your Answer is not the place to explain that you lost your job or had a medical emergency. While those things are difficult, they are not "legal defenses." Providing a long narrative can actually give the Plaintiff's attorney ammunition to use against you. Keep it brief.

Missing Deadlines: This is the "Flag of Defeat." If you are one day late, the creditor can file for a default. Always check the Time to Respond Debt Collection Lawsuit for your specific jurisdiction.

Ignoring Paragraphs: If you skip a paragraph in your Answer, the judge will treat it as an "Admission." You must address every single number.

Identifying Your Affirmative Defenses

This is where the real magic happens. An Affirmative Defense is a legal reason why the Plaintiff shouldn't win, even if some of their allegations are true. You must list these in your Answer, or you may waive your right to use them later.

Statute of Limitations

This is the "expiration date" on debt. In Florida and Michigan, the statute of limitations for credit card debt (breach of contract) is typically 5 years in Florida and 6 years in Michigan. If the last time you made a payment or used the card was longer ago than that, the debt is "time-barred." You can ask the judge to dismiss the case entirely.

Lack of Standing (Chain of Custody)

If "Global Debt Recovery LLC" is suing you for a "Chase Bank" card, they must prove they bought your specific debt. Often, these companies buy debts in bulk (thousands of accounts at once) for pennies on the dollar. They might have a bill of sale for the bulk purchase, but not the specific "Assignment" for your account. If they can't prove they own it, they have no "Standing" to sue you.

Improper Service

If the process server just threw the papers on your lawn or gave them to your 10-year-old child, you might have a defense for improper service. However, be careful: this usually only delays the case rather than ending it.

Identity Theft or Mistaken Identity

If the debt isn't yours, or you were a victim of fraud, this is a powerful affirmative defense. You should include a police report or FTC affidavit if possible. For a deeper dive, check our Debt Lawsuit Defense Guide.

In some cases, you might even need to file a Filing a Counter-Affidavit When Answering a Debt Collection Lawsuit if the Plaintiff attached a sworn statement to their Complaint.

Filing and Serving Your Response

Once your Answer is written, you aren't done. You have to get it into the hands of the court and the Plaintiff’s attorney.

1. Filing with the Court

You must file the original Answer with the Clerk of the Court listed on your Summons.

Filing Fees: Some courts charge a fee to file an Answer (ranging from $80 to over $400 depending on the debt amount). If you cannot afford this, ask the clerk for a Fee Waiver form.

E-Filing: Many counties in Florida and Michigan now require electronic filing. If you are representing yourself (Pro Se), some courts still allow paper filing, but you should call the clerk to verify.

2. Serving the Plaintiff

You are legally required to send a copy of your Answer to the Plaintiff's attorney. This is usually done via Certified Mail with a Return Receipt Requested. This gives you a "green card" signature proving they received it.

3. The Certificate of Service

At the very bottom of your Answer, you must include a "Certificate of Service." This is a short paragraph where you swear to the court that you sent a copy to the Plaintiff. It looks like this:

"I HEREBY CERTIFY that a true and correct copy of the foregoing was served via U.S. Mail to [Attorney Name and Address] this [Date] day of May, 2026."

Many people wonder, Do I Need a Lawyer for a Debt Collection Lawsuit? While a lawyer is helpful, many people successfully file their own Answers using DIY tools to save on the $1,500–$5,000 in fees an attorney might charge.

State-Specific Rules and Deadlines

Since KillDebt is based in Florida and Michigan, let's look at the specific nuances of these two states.

Florida Procedures

The 20-Day Rule: Florida is strict. You have 20 calendar days from the date you were served. If the 20th day falls on a weekend or legal holiday, you usually have until the next business day.

Small Claims vs. Civil: If you are being sued for less than $8,000, it’s a Small Claims case. You might be given a "Pre-Trial Conference" date instead of being required to file a written Answer immediately, but filing a written Answer anyway is always a safer bet to protect your rights.

Michigan Procedures

The 21-Day Rule: If you were served personally, you have 21 days. If you were served by mail or outside of Michigan, you have 28 days.

Verified Complaints: If the Plaintiff "verified" their Complaint (signed it in front of a notary), you must also verify your Answer.

Affidavits of Account: Michigan creditors often attach an "Affidavit of Account." If you don't specifically dispute the amount with your own affidavit, the court might take their word for it.

For those outside these areas, such as the West Coast, the California Debt Lawsuit Answer process has its own unique forms (like PLD-C-010), but the core principles of admitting and denying remain the same.

Conclusion: Fight Back with KillDebt

Learning how to write an answer to a credit card lawsuit is an empowering first step, but you don't have to do it alone. At KillDebt, we provide a DIY legal defense system that levels the playing field.

Our platform is powered by ParkerGPT, an AI trained specifically on consumer debt law and real-world strategies developed over 30 years by attorney Brian Parker. Unlike a search engine, ParkerGPT doesn't just give you general advice; it analyzes your actual lawsuit documents, identifies specific legal weaknesses in the Plaintiff's case, and generates court-ready responses.

Introducing Court Tester: We’ve just rolled out our most powerful tool yet—Court Tester. It’s an AI courtroom simulation built on the facts of your actual case. You can upload your filings and, within minutes, "argue" your motion in front of an AI judge. You'll face an AI opposing counsel, while a private AI co-counsel whispers strategies and tips that only you can see. It’s like having a dress rehearsal for your day in court, ensuring you are prepared, confident, and ready to win.

Don't let a credit card company bully you into a default judgment. Whether you are in Florida, Michigan, or anywhere else, you have rights. Protect your rights and fight back today with the tools and technology designed to help you win.

Frequently Asked Questions (FAQ)

What happens if I ignore the summons?

Ignoring the summons is the absolute worst thing you can do. It leads to a Default Judgment. Once a creditor has a judgment, they don't need your permission to take your money. They can: • Garnish your wages: Taking up to 25% of your take-home pay. • Bank Levy: Freezing your bank account and taking every cent up to the judgment amount. • Property Lien: Placing a claim on your home so you can't sell or refinance it without paying them first.

Can I settle the debt after filing an Answer?

Yes! In fact, filing an Answer makes you more likely to get a good settlement. When you don't answer, the collector knows they get 100% of the money for zero effort. When you file an Answer, you become "expensive" to sue. They now have to pay their attorney to show up for hearings and handle discovery. This often makes them willing to settle for 40–60% of the debt just to make the case go away. Always get a settlement agreement in writing and ensure it includes a "Dismissal with Prejudice" (meaning they can never sue you for this debt again).

Do I need a lawyer to file my Answer?

You have the right to represent yourself (Pro Se). However, the court will expect you to follow the same rules as an attorney. This is where AI assistance comes in. Generic tools might give you a template, but they don't analyze your specific case.