Michigan Has a Debt Lawsuit Crisis — Here's What You Need to Know Right Now

Debt collector lawsuits in Michigan are filed at a staggering scale — and if you just received a summons, you are far from alone.

Quick Facts: Debt Collection Lawsuits in Michigan

What You Need to Know | The Numbers |

|---|---|

Cases filed (Jan 2010 – Sep 2021) | 1.94 million |

Total dollars in controversy | ~$3.1 billion |

Share of all civil District Court cases (2019) | 37% |

Median amount sued for | $1,600 |

Cases ending in default judgment | ~68% |

Defendants with legal representation | 0.4% |

Cases with defendant counsel dismissed | 10x more likely |

The most urgent thing to understand: if you do nothing, you will almost certainly lose.

Nearly 7 in 10 cases end in a default judgment — not because the debt collector proved their case, but because the defendant never responded. That judgment can trigger wage garnishment, bank levies, and tax return seizures.

The good news? You have more power to fight back than you think — especially if you act before your deadline.

I'm Brian Parker, and for over 30 years I've defended consumers against debt buyers, collection agencies, and high-volume law firms in courtrooms across the country. I've seen nearly every tactic used in debt collector lawsuits in Michigan and beyond — and I built KillDebt to put those same defense strategies directly in your hands. Let's walk through exactly what you're facing and what you can do about it.

Understanding the Landscape of Debt Collector Lawsuits Michigan

To fight back effectively, we have to look at the sheer volume of litigation flooding our local courts. Between 2010 and late 2021, over 1.94 million Michigan Court Debt Cases were filed in the state's District Courts. By 2019, these cases made up a massive 37% of all civil District Court filings - second only to traffic tickets.

The scale of these lawsuits is driven by a handful of "top filers." In fact, just ten plaintiffs are responsible for 71% of all debt collection lawsuits in Michigan.

Top Michigan Plaintiffs | Market Share of Lawsuits |

|---|---|

Midland Funding | 20% |

Portfolio Recovery Associates | 12% |

Others (Discover, LVNV, etc.) | 39% |

These companies aren't usually the ones you originally borrowed money from. They are part of a high-volume litigation machine designed to win by default.

The Rise of Debt Buyers in Michigan Courts

The biggest shift we've seen in Debt Collector Lawsuits Michigan over the last decade is the dominance of "debt buyers." In 2010, debt buyers filed about 40% of cases; by 2019, that number jumped to 60%.

Unlike an original creditor (like your local credit union), a debt buyer purchases "charged-off" debt for pennies on the dollar. They often receive very little documentation in the sale - sometimes just a line on an Excel spreadsheet. This creates a huge opportunity for you. If they can't prove they actually own your specific debt or provide the original contract, they may lack the "standing to sue." This is a core part of our Debt Collection Lawsuit Defense Guide.

Demographics and Disparities in Debt Collector Lawsuits Michigan

The burden of these lawsuits is not shared equally across the state. Research shows that half of all debt collection cases in Michigan target neighborhoods with median household incomes of $50,000 or less. The poorest 10% of neighborhoods see 3.3 cases per 100 residents, while the wealthiest 10% see only 0.8.

There are also significant racial disparities. Filing rates against majority Black communities are 2 to 3 times higher than majority White communities, regardless of income level. Areas like Highland Park and the Detroit Metro see some of the highest per-capita filing rates in the nation. Knowing your rights is essential for protecting your community's financial health. You can learn more about these protections in our internal resource, Michigan Debt Collection Laws: Know Your Rights Against Collectors (2026) | Legal Rights Guide.

Legal Protections and Prohibited Practices in Michigan

You aren't defenseless. Several laws regulate how collectors must behave. The federal Fair Debt Collection Practices Act (FDCPA) is the heavy hitter, but Michigan residents have a "double layer" of protection.

The Michigan Regulation of Collection Practices Act (RCPA), specifically Michigan Compiled Laws Act 70 of 1981, covers not just third-party agencies but often original creditors too. If a collector violates these rules, you might be able to sue them for damages or use the violation as leverage in your defense. For immediate steps on handling these situations, check out our Debt Collector Suing Me Advice.

Signs a Collector is Breaking the Law

If a debt collector's lips are moving, there's a decent chance they're pushing the boundaries of the law. Here are the red flags:

Illegal Hours: Calling before 8 AM or after 9 PM.

Workplace Harassment: Calling your job after you've told them your employer prohibits personal calls.

False Threats: Threatening arrest or jail time. (In Michigan, you cannot be jailed for a civil debt!)

Public Shaming: Historically, Michigan law even prohibited "shame automobiles" - cars labeled to embarrass debtors - and the spirit of that law still prevents them from "shaming" you to neighbors or bosses.

Lying: Misrepresenting the amount you owe or pretending to be an attorney or government official.

If you spot these signs, start a log. Every illegal call is a potential $1,000 in your pocket under the FDCPA. For a roadmap on what to do first, see our What to Do When Sued by a Debt Collector: Complete First Steps Guide.

Statute of Limitations and Debt Validation

One of the most powerful defenses in Debt Collector Lawsuits Michigan is the Statute of Limitations. In Michigan, the limit for most consumer debts - including credit cards, medical bills, and written contracts - is 6 years.

The clock usually starts from the date of your last payment or the date you last acknowledged the debt in writing. Warning: Making even a $5 "good faith" payment can restart that 6-year clock from zero!

Additionally, you have a 30-day window after the first contact to request "debt validation." This forces the collector to stop all activity until they send you proof of the debt. If they can't produce it, they can't collect. We cover this extensively in our Fight Debt Collection Lawsuit: Complete Guide.

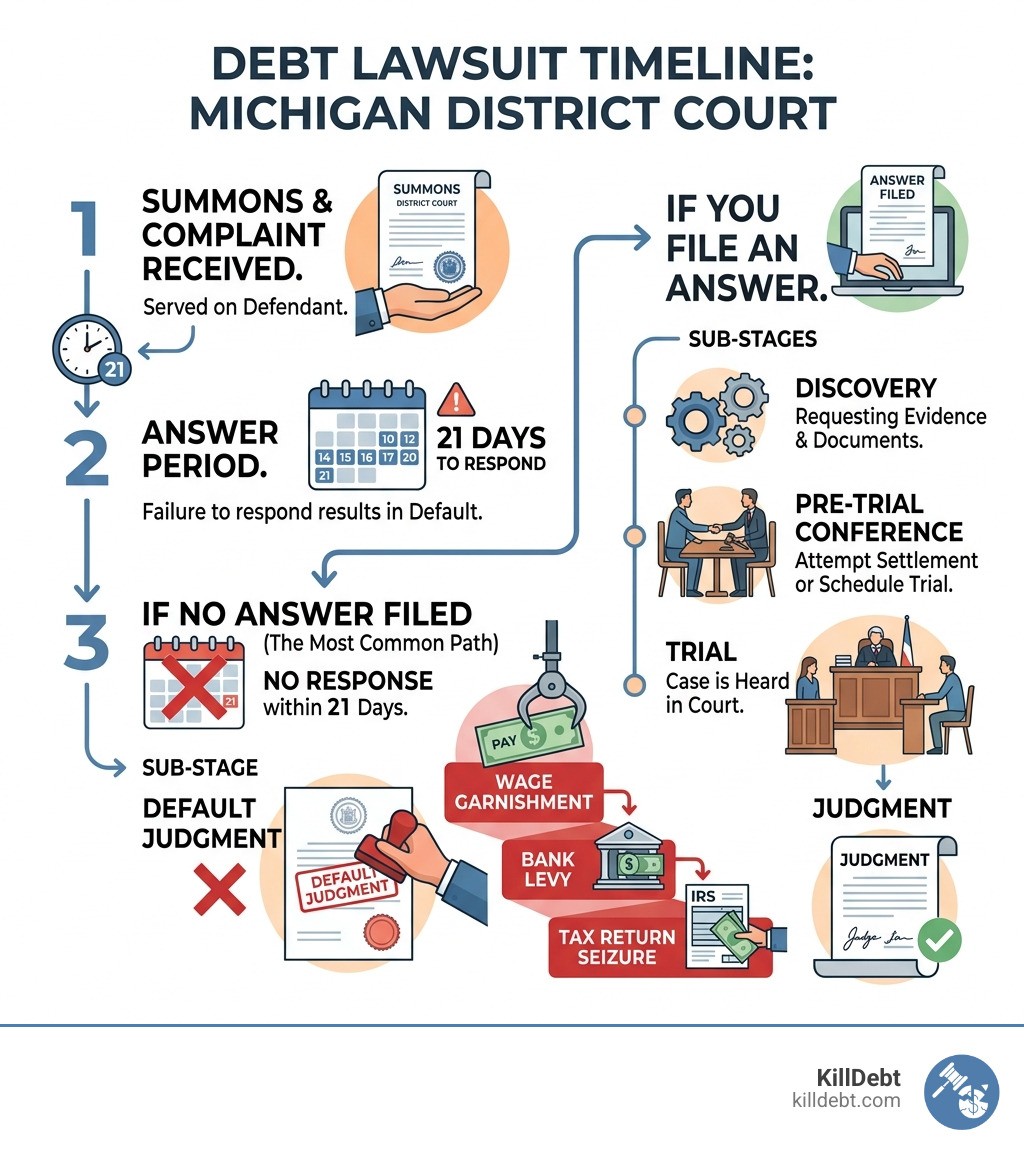

Defending Your Case: How to Respond to a Summons

When you are served with a summons, the clock starts ticking immediately. In Michigan, the deadlines are strict:

21 Days: If you were handed the papers personally.

28 Days: If you were served by mail or live outside the state.

If you miss this deadline, the court will enter a default judgment. This means the collector wins automatically without ever having to prove you owe a dime. For more on the timing, see our guides on How to Answer a Debt Summons and Time to Respond Debt Collection Lawsuit.

Step-by-Step: How to Respond to Debt Collector Lawsuits Michigan

Responding to a lawsuit involves filing a written "Answer." This isn't the time to tell your life story; it's a formal document where you respond to each numbered paragraph in the plaintiff's complaint.

Admit, Deny, or Lack Knowledge: For every allegation, you must choose one of these three.

The "Prove It" Strategy: Denying a claim doesn't necessarily mean you're saying it's false—it means you are demanding the plaintiff meet their burden of proof.

Counter Affidavit: If you are sued on an "Account Stated" (where they claim you agreed to the balance by not objecting to a bill), you must file a notarized Counter Affidavit to dispute the accuracy of that account.

Filing: You must file the original with the court and mail a copy to the plaintiff's attorney via certified mail.

You can find a Sample Answer to Debt Collection Lawsuit on our site to see what this looks like.

Common Affirmative Defenses

An affirmative defense is a reason why, even if the facts in the complaint are true, the plaintiff shouldn't win. Common defenses include:

Lack of Standing: The debt buyer can't prove they own the debt chain from the original creditor to them.

Statute of Limitations: The debt is older than 6 years.

Identity Theft: You never opened the account.

Payment in Full: You already paid this, or a settlement was reached previously.

Unconscionable Contract: The terms were so one-sided they shouldn't be enforced.

Wondering if they can even take you to court? Read Can a Debt Collection Agency Take You to Court for more details.

The Consequences of Inaction: Judgments and Garnishments

The statistics are grim: 96% of plaintiffs in Michigan have lawyers, but only 0.4% of defendants do. This massive gap is why 68% of cases end in default.

Once a judgment is entered, the collector becomes a "judgment creditor" with scary new powers. In Michigan, 78% of judgments that aren't dismissed result in at least one garnishment.

Wage Garnishment: They can take up to 25% of your disposable earnings.

Bank Levies: They can freeze and seize funds directly from your checking or savings account.

Tax Offsets: 66% of garnishments in Michigan involve seizing state income tax returns.

A judgment in Michigan is valid for 10 years and can be renewed for another 10. It is a financial shadow that doesn't go away on its own. If you're wondering Do I Need a Lawyer for a Debt Collection Lawsuit, the answer is that while a lawyer helps, you can defend yourself effectively using the right tools.

Conclusion

Facing Debt Collector Lawsuits Michigan is intimidating, but the system relies on you giving up. When defendants show up with a proper legal response, their chances of a dismissal increase tenfold.

At KillDebt, we’ve revolutionized how you fight back. We provide a DIY legal defense system powered by ParkerGPT—an AI trained specifically on consumer debt law and the real-world strategies I’ve used for over 30 years.

We don't just give you a template. Our platform analyzes your actual lawsuit documents, identifies specific weaknesses in the collector's case, and generates court-ready responses. We even just rolled out our Court Tester—an AI courtroom simulation where you can upload your filings and practice arguing your motion in front of an AI judge before you ever step foot in a real courthouse.

You don't need to spend thousands on an attorney to get an attorney-level defense. Take control of your case today at KillDebt.com.

Frequently Asked Questions (FAQ)

What is the statute of limitations for credit card debt in Michigan?

In Michigan, the statute of limitations for credit card debt, medical debt, and most written contracts is 6 years. This period begins from the date of last activity—usually your last payment. Be careful: acknowledging the debt in writing or making a partial payment can restart this 6-year clock.

Can a debt collector garnish my wages without a court order?

No. For ordinary consumer debt (like credit cards or medical bills), a collector must first sue you and win a money judgment before they can garnish your wages. Once they have a judgment, they can legally take the lesser of 25% of your disposable income or the amount by which your weekly income exceeds 30 times the federal minimum wage.

What should I do if I am sued for a debt I don't recognize?

First, do not ignore the summons. You should raise "Identity Theft" or "Mistaken Identity" as an affirmative defense. Demand "debt validation" and force the plaintiff to produce the original signed contract and a full statement of account. The burden of proof is on them to show that you are the correct debtor and the amount is accurate.