What to Do When a Debt Collection Letter Lands in Your Mailbox

Debt collection letter templates are standardized written documents used to formally request payment of an overdue debt — or to defend yourself against unfair collection attempts.

Here are the most common types you need to know about:

Letter Type | Who Sends It | Purpose |

|---|---|---|

Friendly Payment Reminder | Creditor/Collector | First notice, assumes oversight |

Formal Overdue Notice | Creditor/Collector | Escalates urgency, adds late fees |

Debt Validation Notice | Creditor/Collector | Required by law within 5 days of first contact |

Debt Validation Request | You (the consumer) | Forces collector to prove the debt is real |

Cease and Desist Letter | You (the consumer) | Legally stops collection calls and contact |

Settlement Offer Letter | You (the consumer) | Negotiates a reduced payoff amount |

The most important thing to know right now: If you received a collection letter, you have 30 days from first contact to request validation of the debt in writing. Miss that window and you lose your strongest legal protection.

77% of American households carry some form of debt, and total U.S. household debt sits at a staggering $14.96 trillion. That means collection letters are landing in mailboxes — and inboxes — every single day across the country. For many people, that letter triggers panic, confusion, and a fear of doing the wrong thing.

Here's the reality: collectors count on that confusion. They know that most people don't realize they have legal rights — rights that can stop harassment, force collectors to prove what they claim you owe, and even get a debt thrown out entirely.

I'm Brian Parker, and for over 30 years I've been in the courtroom fighting creditors, debt buyers, and collection law firms. I've seen every trick they use, including the ones hidden inside debt collection letter templates that look official but are actually designed to pressure you into paying debts you may not owe. This guide gives you the same tools I've used to protect thousands of consumers — so you can fight back from wherever you are.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

Why You Need Strategic Debt Collection Letter Templates

When a collection agency reaches out to you, they are not just sending a casual note. They are deploying highly optimized, legally compliant debt collection letter templates designed to protect their interests while forcing you to pay. To level the playing field, you must understand the rules of the game.

Federal law, specifically the Fair Debt Collection Practices Act (FDCPA), governs how these letters must look and what they must contain. The Consumer Financial Protection Bureau (CFPB) even provides Debt Collection model forms and samples that collectors use to remain compliant.

The most critical legal element of any initial collection letter is the 30-day validation window. Under the FDCPA, once a debt collector contacts you, you have exactly 30 days to dispute the debt in writing. If you do, the collector must halt all collection activities until they provide written validation of the debt. If they fail to do so, continuing to collect is a federal violation.

Additionally, collectors must include the "Mini-Miranda" warning in their communications. This statement clearly discloses: "This communication is from a debt collector. This is an attempt to collect a debt and any information obtained will be used for that purpose." If this disclosure is missing, the collector has violated federal law, giving you significant leverage in your defense.

Essential Elements of Compliant Debt Collection Letter Templates

Whether you are a business trying to recover an unpaid invoice or a consumer analyzing a letter you received, certain elements must be present to ensure legal compliance. A standard, legally sound Debt Collection Letter - FindLaw or commercial Collection Letter Template typically contains:

Identities of the Parties: Clear names and contact details of the original creditor, the current collection agency, and the debtor.

Exact Debt Amount: A clear breakdown of the principal balance, plus any legally permissible interest, fees, or late charges.

Original Creditor Information: The name of the business where the debt originated.

The 30-Day Dispute Notice: An explicit statement informing the consumer of their right to dispute the debt and request verification within 30 days.

Payment Instructions: Clear methods for settling the balance safely (such as certified checks or secure online portals).

For consumers, understanding these components is your shield. If a collector sends a letter missing these details, they are violating your rights. You can read more about how to analyze these requirements in our comprehensive Credit Debt Validation Letter Guide 2026.

How to Spot Violations in Received Debt Collection Letter Templates

Not all debt collectors play by the rules. Some use deceptive debt collection letter templates that contain illegal threats or omit required disclosures. Here is what you should look out for:

False Threats of Legal Action: A collector cannot threaten to sue you, garnish your wages, or seize your property unless they actually intend to do so and have the legal right to do so.

Implying Government Affiliation: Letters designed to look like official court summonses or government documents when they are actually just collection notices are highly illegal.

Adding Unauthorized Fees: Collectors cannot tack on arbitrary "collection fees" or interest rates unless those fees were explicitly agreed to in your original contract or are allowed by state law.

Harassing Language: Using abusive, profane, or highly intimidating language violates the FDCPA.

If you spot any of these violations, you can immediately fight back. One of the most effective first steps is sending a Cease Debt Collection Letter to stop the harassment while you build your defense.

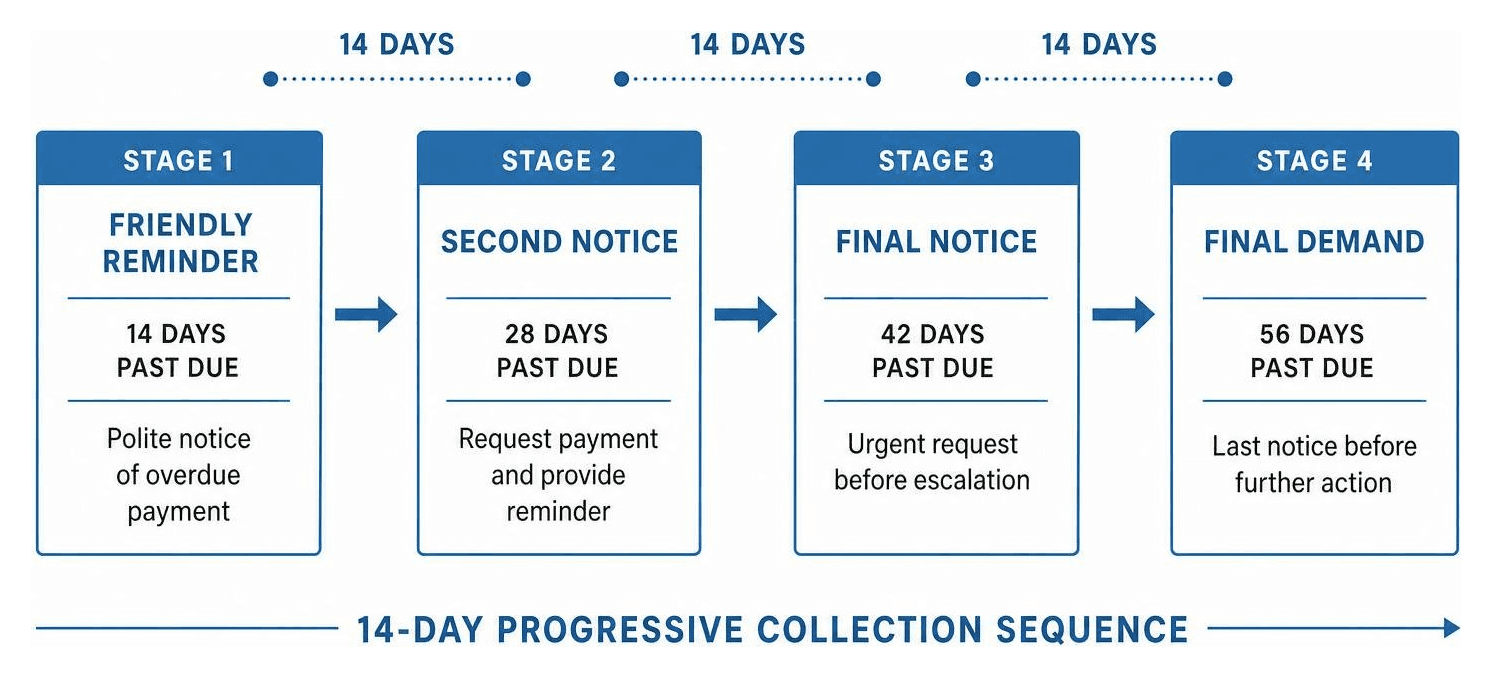

The Progressive Collection Letter Sequence: From Reminder to Final Demand

For businesses and creditors, recovering past-due accounts requires a careful balance between preserving customer relationships and protecting cash flow. Most organizations see a 15-20% reduction in Days Sales Outstanding (DSO) after implementing a consistent, progressive collection letter strategy.

This sequence typically moves through four distinct stages, spaced at 14-day intervals.

Here is how the stages compare from a consumer defense perspective:

Stage | Timing | Tone | Key Consumer Defense Action |

|---|---|---|---|

Stage 1: Friendly Reminder | 14 Days Past Due | Soft, helpful, polite | Verify records; check if the invoice is accurate. |

Stage 2: Overdue Notice | 28 Days Past Due | Firm, direct, structured | Review original contract terms for late fee validity. |

Stage 3: Urgent Demand | 42 Days Past Due | Strict, legal, urgent | Send a debt validation request immediately. |

Stage 4: Final Notice | 56 Days Past Due | Final, legal warning | Prepare defense; check statute of limitations. |

Stage 1: The Friendly Payment Reminder

The first collection letter is sent roughly 14 days after an invoice goes past due. At this stage, the creditor assumes the non-payment is simply an oversight.

The tone is friendly and helpful. It includes basic invoice details, the outstanding balance, and convenient payment options. For consumers, this is the best time to resolve any billing discrepancies before the account escalates.

Stage 2: The Formal Overdue Notice

If the first reminder is ignored, a more formal overdue notice is sent around 28 days past due. The tone becomes firmer and more direct.

This letter typically outlines an updated account summary, references the previous communication, and may introduce late fees if authorized by the original contract. If you are drafting these, you can utilize a professional Credit Collection Letter Template to maintain a respectful yet assertive tone.

Stage 3: The Urgent Demand and Validation Notice

At 42 days past due, the tone shifts to strict urgency. This letter is often the point where third-party debt collectors get involved.

Under FDCPA §809, this communication must include the 30-day validation notice. If you receive a letter at this stage, you must act quickly. Sending a customized Debt Validation Letter Template is your best tool to force the collector to halt their efforts and prove they have the right to collect.

Stage 4: The Final Notice Before Legal Action

The final notice, typically sent 56 days past due, is a pre-litigation demand. It warns that if payment is not received within a specified window (usually 14 days), the account will be forwarded to legal counsel, reported to credit bureaus, or filed in small claims court.

These letters are often sent via certified mail to establish court-admissible proof of delivery. If you receive one of these, you are facing a potential lawsuit and must prepare your legal defense.

How Consumers Can Fight Back Against Unfair Collection Letters

Receiving a collection letter does not mean you have to pull out your wallet and pay. In fact, doing so blindly can be a massive mistake.

Did you know that debt buyers purchase delinquent accounts from original creditors for an average of just 4% to 10% of the debt's face value? Because they buy these debts in bulk for pennies on the dollar, they rarely receive the complete, accurate paperwork required to prove the debt in a court of law.

When you fight back, you force the collector to spend money to locate those records. Often, they cannot produce them, leaving them with no choice but to drop the collection effort entirely.

Sending a Letter of Debt Validation

Your most powerful weapon is a formal validation request. Under FDCPA §809(b), if you send this request within 30 days of receiving their initial notice, the collector must stop all collection activities—including phone calls and credit reporting—until they mail you validation.

To see what a proper validation request looks like, review our Example Debt Validation Letter. When drafting yours, ensure you ask for:

Proof of the original agreement.

A complete itemization of the balance, interest, and fees.

Evidence that the collector has the legal license to collect debts in your state (such as Florida or Michigan).

You can easily generate and customize your own Letter of Debt Validation to send to any agency pursuing you.

Using a Cease and Desist Creditor Letter

If a collector is calling you constantly, contacting your workplace, or stressing you out, you have the legal right to make them stop. Under federal law, if you send a written request telling them to stop contacting you, they must comply.

By sending a Cease and Desist Creditor Letter, you legally restrict their communication channels. Once they receive it, they can only contact you to confirm they are stopping communication or to notify you of a specific legal action (like filing a lawsuit). This stops the daily harassment and gives you peace of mind while you figure out your next steps.

Responding to a Court Summons

If a collector decides to skip letters and file a lawsuit, ignoring it is the worst thing you can do. If you fail to respond to a court summons within your state's deadline (usually 20 to 30 days), the collector wins a default judgment against you. This allows them to legally garnish your wages or freeze your bank accounts.

Defending yourself starts with filing a formal, written Answer with the court. You can review a Debt Summons Response Letter Sample to understand how to structure your response, deny their unproven allegations, and assert your legal defenses.

Conclusion: Take Control of Your Debt Defense Today

Dealing with debt collectors can feel overwhelming, but you do not have to go through it alone or spend thousands of dollars on an expensive attorney. At KillDebt, we provide a DIY legal defense system powered by ParkerGPT—an AI trained specifically on consumer debt law and real-world court strategies developed over 30+ years of active practice.

Whether you need to draft a compliant validation letter, respond to a harassing collector, or analyze complicated court filings, our platform gives you the exact tools you need. We’ve also recently rolled out our brand-new tool, Court Tester!

Court Tester is an AI courtroom simulation built on the actual details of your case. You can upload your real filings and, within minutes, practice arguing your motion in front of an AI judge, face off against an AI opposing counsel, and receive private, strategic tips from an AI co-counsel that only you can see.

Don't let debt collectors dictate the terms. Take control of your financial future, check out our straightforward KillDebt Pricing, and start defending your rights today at KillDebt DIY Legal Defense.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments.

Frequently Asked Questions (FAQ)

What should I do if I receive a debt collection letter for a debt I don't owe?

If you receive a letter for a debt you don't recognize, do not ignore it. Immediately send a written dispute and validation request. You can use our Validation of Debt Letter template to formally state that you do not owe the debt and demand full documentation. Keep a copy of your letter and send it via USPS Certified Mail with Return Receipt Requested so you have proof they received it.

Can a debt collector contact me after I send a cease and desist letter?

Under the FDCPA, they must stop all standard communication. They are only allowed to contact you one final time to acknowledge your letter or to notify you that they are taking a specific legal action, such as filing a lawsuit. If they continue to call or mail you standard collection notices after receiving your cease and desist, they are violating federal law, and you can sue them for up to $1,000 per violation. Learn more about your options using Legal Letters for Debt Collection.

How do I negotiate a settlement using debt collection letter templates?

If the debt is valid and you want to settle it, never do it over the phone. Debt collectors will promise anything on a call and change their tune once they have your money. Always negotiate in writing. A good strategy is to send a written settlement offer starting at 60% of the total balance. In your letter, state clearly that your offer is contingent upon receiving a signed agreement from them stating that the payment settles the debt in full and that they will report the account as "paid in full" or "settled" to the credit bureaus.