When a Debt Collector Writes to You - Here's What You Need to Know

A credit collection letter template is a structured document used to formally demand payment of an outstanding debt — or, from your side as a consumer, to dispute one. Whether you just received a collection notice or need to respond to one, here's what matters most:

Quick answers if you're in a hurry:

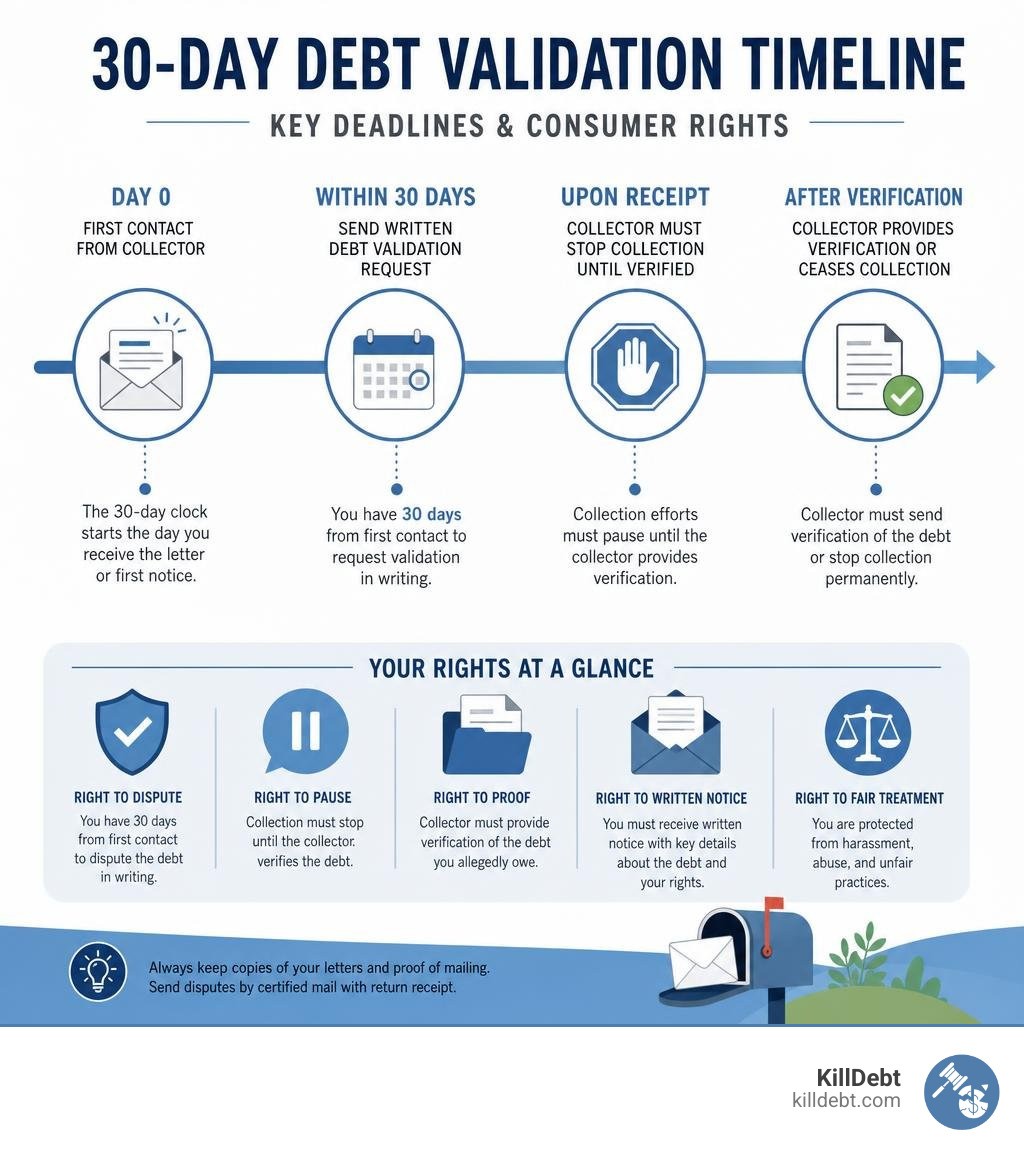

Got a collection letter? You have 30 days from first contact to request debt validation in writing.

Not sure you owe the debt? Send a written debt validation request immediately — the collector must stop collection until they verify.

Need a template now? The key elements any valid collection letter must include are:

The amount owed (itemized)

The name of the original creditor

The mini-Miranda warning ("This is an attempt to collect a debt...")

Your 30-day right to dispute

Separate addresses for payments and disputes

The collector's license number (required in most states)

Most people feel blindsided when a collection letter arrives. The language is formal. The deadlines feel urgent. And the consequences — wage garnishment, lawsuits, damaged credit — sound terrifying.

But here's the truth: collectors make mistakes constantly. According to CFPB data, 53% of consumers who receive collection letters are being pursued for debts they don't believe they owe or for incorrect amounts. That means your letter may already be on shaky legal ground.

Knowing how to read, respond to, or write a credit collection letter is one of the most valuable things you can do to protect yourself financially — and it costs you nothing but a little knowledge.

I'm Brian Parker. For over 30 years, I've been in the courtroom fighting creditors, debt buyers, and collection law firms — and I've seen every credit collection letter template trick collectors use to pressure people into paying debts they may not legally owe. At KillDebt, I've distilled that courtroom experience into tools and guides that put you back in control.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

What is a Credit Collection Letter Template and Why Does It Matter?

A credit collection letter template is more than just a piece of paper with a balance and a payment address. It is a formal, legal instrument that initiates the collection cycle. For businesses, a well-crafted template helps recover past-due accounts receivable and directly improves Days Sales Outstanding (DSO) metrics. In fact, organizations that implement a consistent, structured collection letter sequence often see a 15% to 20% reduction in DSO.

For consumers, understanding the mechanics of this template is your shield. Under federal law, the moment a third-party debt collector sends you an initial demand letter, it triggers your right to demand verification. This is where Debt Validation Letters: Your First Line of Defense Against Collectors become critical.

Under the Fair Debt Collection Practices Act (FDCPA) Section 809(b), if you dispute the debt in writing within 30 days of receiving their initial notice, the collector must completely cease all collection activities. They cannot call you, write to you, or report the debt to credit bureaus until they obtain verification of the debt and mail that proof to you. This completely shifts the burden of proof back onto the collector. They must prove that:

They have the legal right to collect the money.

The amount they are claiming is accurate down to the penny.

You are the actual person responsible for the account.

As of June 2026, compliance standards are stricter than ever. Under the Consumer Financial Protection Bureau’s (CFPB) Regulation F, debt collectors are required to provide a highly detailed, itemized breakdown of the debt. They can no longer simply send a letter listing a lump sum. They must show the balance as of the "itemization date," along with any interest, fees, or payments applied since that date.

It is also vital to distinguish between an original creditor and a third-party collector. Under federal law, the FDCPA generally applies only to third-party debt collectors (such as collection agencies or debt buyers). However, if you live in Florida, the Florida Consumer Collection Practices Act (FCCPA) applies to both original creditors and third-party collectors, offering you powerful local protections against abusive collection tactics.

Key Components of a Legally Compliant Collection Letter

If you are reviewing a letter sent to you, or drafting a response using a credit collection letter template, you must look for specific elements. If a collector's letter lacks these components, they may be in direct violation of federal and state laws.

A legally compliant collection letter must include:

Clear Sender and Recipient Details: The full legal name of the collection agency, their physical address, and their state license number (highly relevant in Michigan, where collection agencies must be licensed under the Occupational Code).

Original Creditor Details: The clear name of the original creditor and any associated account numbers (redacted for privacy).

Itemized Debt Breakdown: A line-by-line breakdown showing the principal, interest, and fees as required by Regulation F.

The Mini-Miranda Warning: A conspicuous disclosure stating: "This communication is from a debt collector. This is an attempt to collect a debt and any information obtained will be used for that purpose."

The Validation Notice: Verbatim text explaining your 30-day right to dispute the debt.

Separate Addresses: Clear, distinct addresses for where to send payments versus where to mail disputes.

You can compare these requirements against professional legal structures by reviewing the Credit And Collection Letter guide.

Essential Disclosures in a Credit Collection Letter Template

Let's look closer at the mandatory legal disclosures. If a collector attempts to bury these disclosures in tiny fine print, or paraphrases them to weaken their impact, they run afoul of the "least sophisticated consumer" standard used by courts to evaluate FDCPA violations.

The mini-Miranda must be printed in bold, uppercase text, at a font size no smaller than the body text. Similarly, the 30-day dispute window notice must clearly state that if you do not dispute the validity of the debt within 30 days of receiving the notice, the collector will assume the debt is valid.

If you need to draft a dispute letter that holds collectors accountable to these standards, utilizing a structured Debt Validation Letter Template ensures you use the correct verbatim statutory language to assert your consumer rights.

B2B vs. B2C Collection Letters: Critical Differences

It is a common mistake to treat business-to-business (B2B) collection letters the same as business-to-consumer (B2C) letters. They operate in entirely different legal worlds.

Feature | Business-to-Consumer (B2C) | Business-to-Business (B2B) |

|---|---|---|

Primary Governing Law | FDCPA, Regulation F, State Laws (FCCPA in FL) | State Contract Law, Uniform Commercial Code (UCC) |

Validation Disclosures | Mandatory 30-day validation notice & mini-Miranda | Not required |

Itemization Requirements | Strict line-by-line breakdown under Reg F | Standard statement of account or invoice details |

Contact Restrictions | Strict hours (8 AM - 9 PM), no workplace harassment | Standard business communications permitted |

Statutory Damages | Up to $1,000 per violation + attorney fees | Limited to contractual terms and actual damages |

In a B2C context, the consumer is protected by a vast net of federal and state regulations designed to prevent harassment and deception. For example, in Florida, collectors cannot contact a consumer before 8 a.m. or after 9 p.m. without consent.

In a B2B context, the relationship is commercial. The FDCPA does not apply. Instead, the collection process is governed by the original contract, purchase orders, and the Uniform Commercial Code. If you are looking for templates specifically tailored to the commercial agency side, you can explore the Collection Letter by Collection Agency Template to see how agencies structure these demands.

The Strategic Timeline: Sequencing and Timing Your Responses

In accounts receivable, timing is everything. A meticulously planned collection letter sequence helps prevent invoices from aging further, directly protecting cash flow.

Experts agree that communicating about past-due invoices should happen early in the process — just 14 days past the payment due date. If the first letter does not receive a response within two weeks, a second notice should be sent. A sequence of 3-4 letters, spaced approximately 14 days apart, usually provides sufficient opportunity for response before escalating to legal action.

However, from the consumer's perspective, this 14-day sequence is a pressure tactic. Your focus should be on the 30-day validation period established by federal law.

When you receive a collection notice, the clock starts ticking. You must mail your validation request within 30 days. To protect your rights, always mail your dispute using a trackable shipping method, such as USPS Certified Mail with a Return Receipt. This gives you irrefutable, court-ready proof of when the collector received your dispute. You can study a real-world example of how to frame this response by reading our Example Debt Validation Letter.

How to Customize a Credit Collection Letter Template for Delinquency Stages

When creditors or agencies customize a credit collection letter template, they progress through distinct stages of escalation:

First Reminder (14 Days Past Due): Friendly and professional. It assumes the missed payment was a simple oversight.

Second Notice (28 Days Past Due): Firmer tone. It requests immediate payment and asks the debtor to contact the billing department if they are facing financial hardship.

Urgent Action Notice (42 Days Past Due): Direct and urgent. It outlines potential late fees or interest charges contractually permitted.

Final Notice / Demand Letter (56 Days Past Due): Formal warning. It states that the account is being prepared for legal referral or credit reporting.

If you are on the receiving end of this escalation, sending a formal Letter of Debt Validation at any stage forces the collector to halt their progression. This pause gives you the breathing room needed to assess your options, check the statute of limitations, or prepare a defense.

Common Pitfalls and Legal Risks in Debt Collection Correspondence

Using a poorly drafted credit collection letter template carries massive legal risks for collectors. Under the FDCPA, consumers can sue collectors for statutory damages of up to $1,000 per lawsuit, plus actual damages and attorney's fees. For agencies, non-compliant templates can lead to devastating class-action lawsuits.

Common pitfalls include:

Threatening Legal Action They Cannot Take: Collectors often threaten to sue or garnish wages on debts that are past the statute of limitations. In Florida, the statute of limitations for a written contract is 5 years. In Michigan, it is 6 years. Threatening a lawsuit on a time-barred debt is a major FDCPA violation.

Wrong-Party Contacts: Sending a collection letter addressed to "you" or implying a recipient owes a debt without verifying their identity can lead to lawsuits if the letter is opened by a third party.

Harassment and Coercion: Using abusive language, threatening to notify employers, or repeatedly calling after receiving a Cease Debt Collection Letter.

Inaccurate Credit Reporting: Reporting a disputed debt to credit bureaus without marking it as "disputed" violates the Fair Credit Reporting Act (FCRA).

If you are facing aggressive collectors, you should familiarize yourself with consumer guides like How to Deal with Debt Collectors to understand your local rights in Michigan and Florida.

Conclusion

Receiving a collection letter doesn't mean you have to surrender your hard-earned money to aggressive debt buyers. Whether you are dealing with a stressful collection notice, a sudden court deadline, or a confusing lawsuit summons, you have the power to fight back and win.

At KillDebt, we believe that every consumer deserves access to top-tier legal defense without paying thousands of dollars in attorney fees. Our DIY legal defense system is powered by ParkerGPT — an AI trained specifically on consumer debt law and real-world courtroom strategies developed over my 30+ years as a consumer defense attorney.

Unlike generic templates, ParkerGPT analyzes your actual lawsuit filings, identifies critical weaknesses in the collector's chain of title, and generates highly customized, court-ready responses.

We also just rolled out our brand-new tool: Court Tester. This is an AI courtroom simulation built directly on your actual case. By uploading your filings, you can practice arguing your motion in front of an AI judge, face off against an AI opposing counsel, and receive private, real-time strategy tips from an AI co-counsel whispering in your ear.

Don't let debt collectors intimidate you. Take control of your financial future today by visiting KillDebt and exploring our pricing options to find the perfect tools for your defense.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments.

Frequently Asked Questions (FAQ)

What should I do if a debt collector fails to validate the debt?

Under FDCPA Section 809(b), if a collector fails to provide proper validation but continues to contact you or report the debt to credit bureaus, they are violating federal law. You should immediately send a Cease and Desist Creditor Letter instructing them to stop all communications. Additionally, you can file a formal dispute with the credit bureaus (Equifax, Experian, and TransUnion) demanding they remove the unverified collection account from your credit profile. You can also report the collector to the CFPB, the Federal Trade Commission (FTC), and your state’s Attorney General.

Can a collection agency contact me after I send a validation request?

Once they receive your validation request, they are legally barred from contacting you to collect the debt. They may only contact you for two reasons: 1 To provide the written validation documents you requested. 2 To formally notify you that they are terminating their collection efforts or filing a lawsuit against you. Any other call, letter, or email constitutes a separate FDCPA violation. You can find resources and draft templates to protect yourself using Free Debt Validation and Credit Dispute Letters.

Does stopping contact from a collector cancel the debt?

No. Sending a cease-and-desist letter stops the collector from calling or writing to you, but it does not erase the underlying debt. The creditor or collector still retains the legal right to: • Sell the debt to another collection agency (which starts the contact cycle over again). • Report the negative history to credit bureaus (subject to FCRA timelines). • File a civil lawsuit against you to obtain a judgment for wage garnishment or bank account levies. If you actually owe the debt and want to resolve it, debt settlement — negotiating to pay a lump sum for a fraction of what you owe — is often a highly effective strategy once validation has been established.