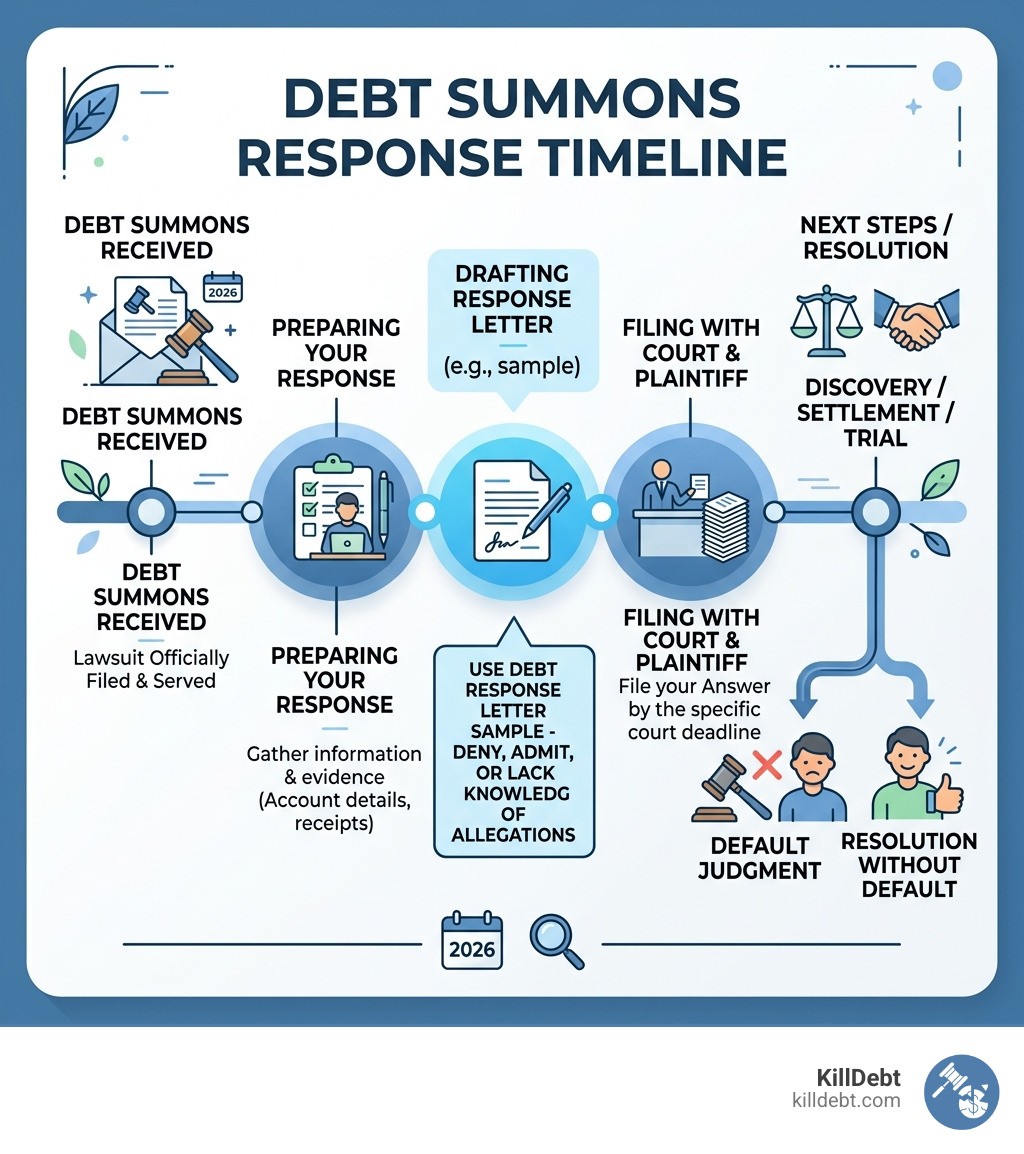

What to Do When You Receive a Debt Summons (And How to Respond)

A debt summons response letter sample is a legal document you file with the court to formally answer a debt collection lawsuit — and using one correctly can be the difference between keeping your paycheck and losing it to garnishment.

Here's a quick overview of how to respond to a debt summons:

Read the summons carefully — note the response deadline (usually 20–30 days, depending on your state)

Draft a written Answer — respond to each allegation in the complaint (admit, deny, or state lack of knowledge)

Include affirmative defenses — such as expired statute of limitations or lack of standing

File your Answer with the court clerk — pay the filing fee or request a fee waiver

Serve a copy on the plaintiff — typically via certified mail, then file proof of service

Being sued for credit card debt is stressful. Most people freeze up or ignore the paperwork entirely — and that's the worst thing you can do.

If you don't respond in time, the court can issue a default judgment against you. That means the debt collector wins automatically, without ever proving they have a valid case. From there, they can garnish your wages, freeze your bank account, or place liens on your property.

The good news? You don't need to be a lawyer to fight back. A properly written response letter — filed on time — forces the debt collector to prove every claim they're making. Many cases settle or get dismissed once the debt collector simply shows up.

This guide will walk you through exactly how to write, file, and serve your response — step by step.

Understanding the Debt Summons and the Risks of Inaction

When you are served with legal papers, you are usually looking at two distinct documents: the Summons and the Complaint. Understanding the Difference Between Summons & Complaint in Debt Collection Lawsuit is your first step toward a solid defense. The summons is the official notice that you are being sued and provides instructions on where and when to respond. The complaint, on the other hand, lists the specific allegations the plaintiff (the debt collector) is making against you.

The biggest mistake we see is "head-in-the-sand" syndrome. Ignoring these documents doesn't make the debt go away; it makes it permanent. If you fail to file a response by the deadline, the court will likely grant a default judgment. This is essentially a "forfeit" win for the debt collector. With a judgment in hand, they can proceed to wage garnishment, where they can legally take up to 25% of your disposable earnings directly from your paycheck.

Timing is everything. You must know the Time to Respond: Debt Collection Lawsuit for your specific jurisdiction. While we focus on Florida and Michigan, it is important to see how these deadlines can vary.

State | Typical Response Deadline |

|---|---|

Florida | 20 Days |

Michigan | 21 Days (if served in person) |

Ohio | 28 Days |

California | 30 Days |

Note: Always check the specific date listed on your summons, as local rules or the method of service can change these windows.

How to Use a Debt Summons Response Letter Sample to Protect Your Rights

Using a debt summons response letter sample isn't just about filling in the blanks; it's about forcing the plaintiff to meet their burden of proof. In a civil case, the debt collector must prove that you owe the money, that they have the right to collect it, and that the amount is accurate. By filing an "Answer," you are telling the court that you intend to defend yourself.

For those in Michigan, resources like the Do-It-Yourself Civil Answer - Michigan Legal Help provide a foundation, but you must ensure your response follows strict legal formatting. To get started, follow our What to Do When Sued by a Debt Collector: Complete First Steps Guide.

Essential Components of a Debt Summons Response Letter Sample

Your response needs to be structured correctly for the court to accept it. It generally includes:

Court Caption: This is the header that lists the court name, the names of the Plaintiff and Defendant, and the Case Number.

Numbered Responses: Your Answer must correspond to the numbered paragraphs in the Complaint. For each paragraph, you have three choices:

Admit: You agree the statement is 100% true (e.g., your name and address).

Deny: You dispute the claim (e.g., you deny you owe the specific amount claimed).

Lack of Knowledge: You don't have enough information to admit or deny (this is common when a debt has been sold multiple times).

Prayer for Relief: This is the concluding section where you ask the court to dismiss the case or grant you costs.

Customizing Your Debt Summons Response Letter Sample for Court

A generic template is a start, but customization is key. You must include your personal details and the exact name of the plaintiff. Most importantly, you must sign the document. Some jurisdictions require a verification signature, which is a statement under oath that your responses are true.

Additionally, you should include a Certificate of Service, which is a statement telling the court how and when you sent a copy of your Answer to the plaintiff’s attorney. If you cannot afford the court's filing fee, don't panic. You can often file a fee waiver (such as Form FW-001 in some jurisdictions or local equivalents in Florida and Michigan) to ask the court to waive the costs based on your financial situation.

Winning Strategies: Affirmative Defenses and the Statute of Limitations

The "Answer" is your shield, but affirmative defenses are your sword. An affirmative defense is a reason why, even if the facts in the complaint are true, the plaintiff should still lose the case.

One powerful tool is Filing a Counter-Affidavit When Answering a Debt Collection Lawsuit. This can challenge the "evidence" the debt collector provides, which is often just a generic spreadsheet or a robosigned affidavit.

The most common defense is the Statute of Limitations. This is the legal "expiration date" for a debt. In Florida and Michigan, the statute of limitations for credit card debt (often classified as an open-ended account or written contract) typically ranges from 4 to 6 years. If the debt is older than this and you haven't made a payment, it is time-barred debt, and the collector has no legal right to sue you. Be careful: making even a small partial payment can sometimes "restart the clock" on the statute of limitations.

Using Affirmative Defenses in Your Debt Summons Response Letter Sample

When drafting your debt summons response letter sample, consider including these defenses if they apply:

Lack of Standing: The plaintiff (often a third-party debt buyer) hasn't proven they actually own your specific debt.

Expired Statute: The time limit to sue has passed.

Improper Venue: They sued you in the wrong county.

Debt Paid or Discharged: You already paid this debt, or it was wiped out in a discharged bankruptcy.

Uncredited Payments: They are suing for the wrong amount because they didn't apply your previous payments.

Step-by-Step: Filing and Serving Your Answer to the Court

Once your letter is drafted, you need to make it official.

Prepare the Forms: If you are in Michigan, you might use form MC 03, Answer (Civil) - Michigan Courts. Ensure you have the original for the court and copies for yourself and the plaintiff.

File with the Clerk: Take your Answer to the courthouse listed on your summons. The clerk will stamp it. This is a critical step in the Debt Collection Lawsuit Timeline: What Happens Next After You're Served.

Serve the Plaintiff: You must "serve" the other side. The best way is via certified mail with a return receipt requested. This provides you with proof that the plaintiff's lawyer received your response.

File Proof of Service: Once you have served the plaintiff, you may need to file a simple document with the court clerk stating that service was completed.

After filing, the case enters the discovery phase, where both sides exchange information. This is often where debt collectors realize they don't have the paperwork to win and may offer a settlement negotiation. Avoid common mistakes like missing the deadline by even one day, as clerks are rarely authorized to give extensions.

Conclusion

Navigating the legal system can feel like walking through a minefield, but you don't have to do it alone. At KillDebt, we believe that every consumer deserves a fair fight. Our DIY legal defense system is powered by ParkerGPT, an AI trained specifically on consumer debt law and real-world strategies developed over 30 years by attorney Brian Parker.

We offer more than just a debt summons response letter sample. Our platform analyzes your actual lawsuit documents, identifies specific legal weaknesses in the collector's case, and generates court-ready responses tailored to your situation.

Want to see how you'll perform before you step into the courtroom? Our brand-new Court Tester allows you to run an AI courtroom simulation. You can upload your filings and argue your motion in front of an AI judge, with an AI co-counsel whispering strategy in your ear.

Don't let a debt collector take your hard-earned money without a fight. Protect your rights and fight back against debt collectors today with the power of AI and decades of legal expertise on your side.

Frequently Asked Questions (FAQ)

What is the difference between a debt validation letter and a response to a summons?

A debt validation letter is a tool used under the Fair Debt Collection Practices Act (FDCPA) before a lawsuit is filed. You typically have 30 days from the first collection notice to request validation. A response to a summons is a formal legal answer filed with a court after a lawsuit has begun. Sending a validation letter to a collector does not stop the clock on a court summons.

When should I consider hiring a lawyer or using legal aid for a debt lawsuit?

If your case involves a massive amount of money or complex legal issues, you might ask, "Do I Need a Lawyer for a Debt Collection Lawsuit?" While many people successfully defend themselves pro se (on their own), those with low income can look for legal aid or local bar associations in Florida or Michigan for assistance.

What happens after I file my Answer with the court?

After you file, the "automatic win" for the collector is off the table. The court will likely set a date for a pretrial hearing or a trial. During this time, you can engage in discovery (asking the collector for proof of the debt) or receive settlement offers. If you reach a deal, ensure you get a written agreement before paying a cent.