What You Need to Know About Florida Debt Lawsuit Rights Right Now

If you're dealing with Florida debt lawsuit rights, here is what you need to know immediately:

Your key rights at a glance:

You have 20 days to respond to a debt lawsuit summons in Florida — missing this deadline can result in a default judgment against you

Debt collectors cannot contact you before 8 a.m. or after 9 p.m., and you can stop all contact by sending a written cease-and-desist letter

You have 30 days from the first collection notice to dispute the debt and demand written verification

Florida's statute of limitations on most written debts is 5 years — collectors cannot sue you after that window closes

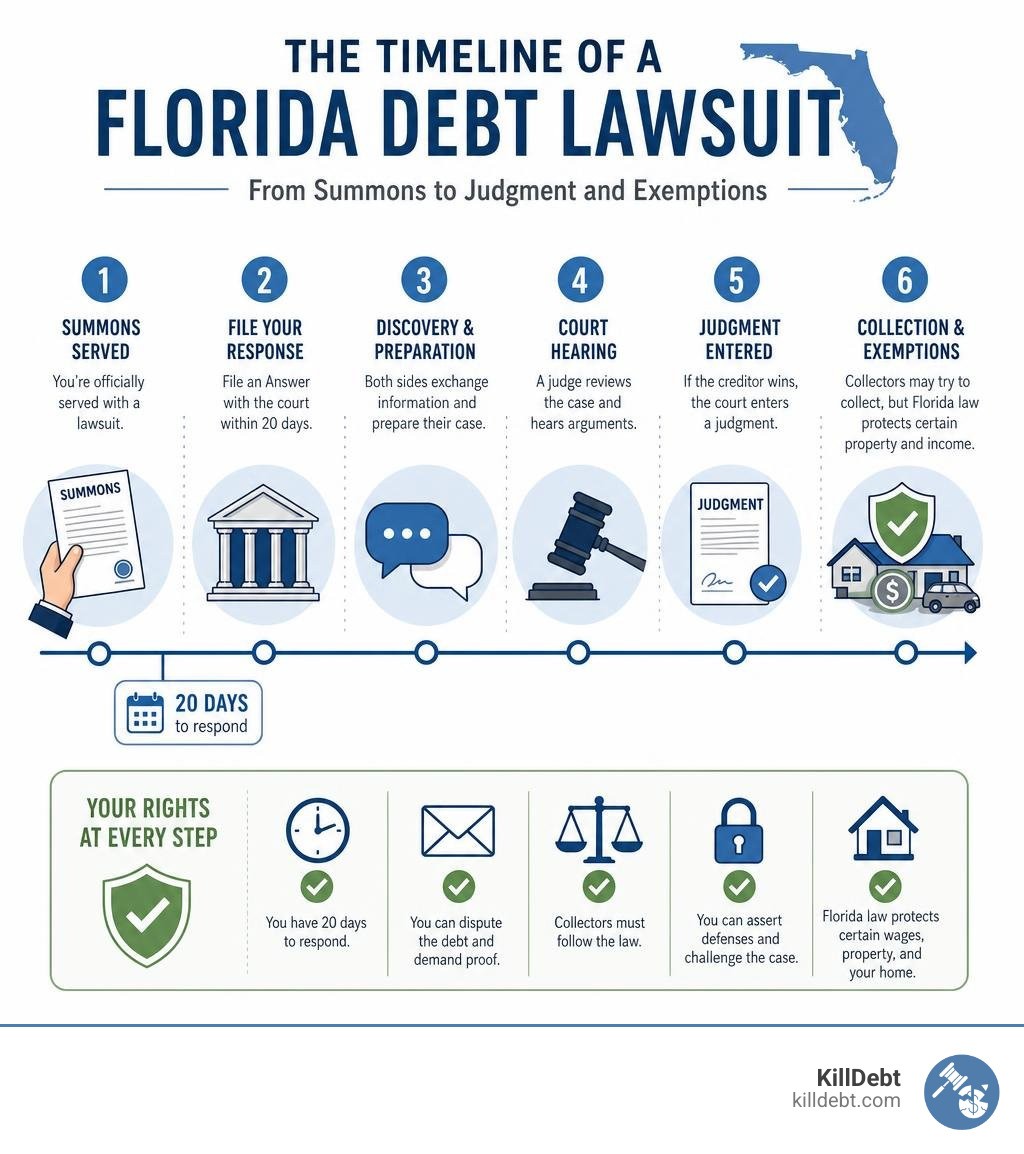

If a judgment is entered against you, Florida law protects certain wages, property, and your home from seizure

You can sue a debt collector who breaks the law and recover up to $1,000 in statutory damages plus attorney fees

Getting served with a lawsuit over an unpaid debt is one of the most stressful things that can happen to you financially. You might feel like the odds are stacked against you — and without the right information, they often are. Most people who are sued for debt never respond. That alone hands the collector an easy win.

But here's the truth: debt collectors don't always win. They have to prove they own the debt, that you owe it, and that the amount is correct. Many can't. And Florida law gives you real tools to fight back — whether you've just been served, received a threatening collection letter, or are worried about your paycheck being garnished.

I'm Brian Parker, founder of KillDebt, and I've spent over 30 years in the courtroom defending consumers against creditors, debt buyers, and collection law firms — giving me a front-row seat to every aspect of Florida debt lawsuit rights. In this guide, I'll walk you through exactly what those rights are and how to use them.

Understanding Your Florida Debt Lawsuit Rights under FDCPA and FCCPA

When you are facing a debt collector, you are protected by two powerful shields: the federal Fair Debt Collection Practices Act (FDCPA) and the state-specific Florida Consumer Collection Practices Act (FCCPA). Together, these laws establish your fundamental Florida debt lawsuit rights.

The FDCPA is the federal baseline. It outlines what third-party debt collectors can and cannot do nationwide. However, Florida consumers enjoy some of the strongest protections in the country because our state law, the FCCPA, goes much further. Under Chapter 559 Section 72 - 2020 Florida Statutes - The Florida Senate , the state codifies 19 specific prohibited practices that debt collectors must avoid.

If a collector violates either of these acts, they aren't just behaving badly — they are breaking the law. You can use these violations as leverage in negotiations, as counterclaims in a lawsuit, or even as the basis to sue the collector for damages.

How the FCCPA Expands Your Florida Debt Lawsuit Rights

While the federal FDCPA only regulates third-party debt collectors (like collection agencies and debt buyers), the Florida FCCPA applies to anyone trying to collect a consumer debt. This includes original creditors, such as your credit card company, local hospital, or auto lender.

This is a massive advantage. If an original creditor harasses you, you cannot sue them under federal law, but you can sue them under Florida law.

Furthermore, the FCCPA allows you to recover:

Statutory damages of up to $1,000 per case.

Actual damages for out-of-pocket losses or emotional distress.

Punitive damages at the court's discretion for egregious violations.

Attorney’s fees and court costs, meaning if you win, the collector has to pay for your lawyer.

If you are dealing with aggressive out-of-state collectors, they must still comply with Florida's strict standards when communicating with a Florida resident. To understand how to leverage these violations to get a case thrown out, check out our Fight Debt Collection Lawsuit Complete Guide.

Rules of Engagement: Contact Limits and Prohibited Harassment

Debt collectors are notorious for trying to wear you down through psychological exhaustion. However, the law strictly limits their communication methods:

Time Restrictions: Collectors cannot call you before 8:00 a.m. or after 9:00 p.m. local time without your explicit consent.

Call Frequency: Under federal guidelines, collectors generally cannot call you more than seven times within a seven-day period regarding a specific debt.

Workplace Contact: Collectors cannot contact you at work if they know or have reason to know your employer prohibits such communications. If they call you at your job, simply tell them, "My employer does not allow me to receive these calls," and they must stop immediately.

Family Contact: A collector cannot contact your family, friends, or neighbors to discuss your debt. They are only allowed to contact third parties once to ask for your location information (address, phone number, or workplace), and they cannot disclose that you owe money.

Cease and Desist: You have the right to tell a collector to stop contacting you entirely. Once they receive a written cease-and-desist letter, they can only contact you to confirm they are stopping contact or to notify you that they are taking a specific legal action, such as filing a lawsuit.

What to Do When You Receive a Debt Validation Notice

Your defense begins long before a lawsuit is filed. Within five days of their initial contact with you, a debt collector must send you a written "debt validation notice." This notice must contain:

The exact amount of the debt.

The name of the current creditor.

A statement that you have 30 days to dispute the debt.

A promise to provide verification of the debt if you dispute it in writing.

This 30-day window is critical. If you send a written dispute within this timeframe, the collector must halt all collection efforts until they mail you written proof of the debt.

If you do not recognize the debt or suspect the amount is incorrect, do not pay a single dime. Instead, send a formal dispute letter via certified mail with a return receipt requested. This creates a paper trail proving they received your request. For a step-by-step breakdown of how to handle this initial phase, read our What to Do When Sued by a Debt Collector Complete First Steps Guide.

How to Respond to a Florida Debt Summons and Complaint

If a creditor or debt buyer decides to sue, you will be served with a Summons and a Complaint. The Summons is the official court notice telling you that you are being sued, while the Complaint outlines the specific allegations against you.

In Florida, you generally have 20 calendar days from the day after you are served to file a written response with the court. This 20-day limit includes weekends and holidays. If the 20th day falls on a Saturday, Sunday, or legal holiday, your deadline is extended to the next business day.

For a comprehensive breakdown of the mechanics of this document, see our guide on How to Answer a Debt Summons.

Asserting Your Florida Debt Lawsuit Rights in Court

To protect your Florida debt lawsuit rights, you must file a formal written "Answer" to the complaint. Do not just show up to court or call the plaintiff's attorney; you must put your response in writing.

Your Answer must address every numbered paragraph in the Complaint. For each allegation, you have three options:

Admit: You agree that the statement is 100% true (e.g., admitting your name and address).

Deny: You dispute the statement. In debt defense, you should generally deny allegations regarding the balance owed or the plaintiff's ownership of the debt unless you have verified proof. Denying forces the plaintiff to produce real evidence.

Deny due to lack of knowledge: You do not have enough information to confirm or deny the statement (e.g., if a debt buyer claims they purchased the account from your original credit card company on a specific date).

At the end of your Answer, you must include a "Certificate of Service" stating that you mailed or e-filed a copy of your response to the plaintiff's attorney. To see what a properly formatted response looks like, review our Sample Answer to Debt Collection Lawsuit.

The Danger of Inaction: Default Judgments

If you ignore the summons or miss the 20-day deadline, the plaintiff will file a motion for a default judgment.

A default judgment means you lose the case automatically. The court accepts all of the collector's allegations as true and grants them the legal right to collect the money through aggressive post-judgment means, such as freezing your bank accounts or garnishing your wages.

If you have already had a default judgment entered against you, all hope is not lost. In Florida, you can file a motion to set aside or vacate the judgment if you can prove "excusable neglect" (a legitimate reason why you missed the deadline, such as improper service or a medical emergency) and a "meritorious defense" (a viable legal defense to the lawsuit).

To learn how to undo this damage, read our specialized guides on Setting Aside Default Judgment and Vacate Default Judgment Florida.

Key Defenses to Defeat a Debt Collector in Court

When you file your Answer, you also have the opportunity to assert "affirmative defenses." These are legal reasons why the plaintiff should not win, even if you did originally owe money to someone.

Some of the most powerful defenses in a Florida debt collection case include:

Lack of Standing: This is highly effective against third-party debt buyers (like Midland Credit Management or Portfolio Recovery Associates). To sue you, they must prove they actually own your specific debt. They must show a complete "chain of custody" (assignment contracts) from the original creditor down to them. If they are missing a single link in that chain, they lack standing, and the case should be dismissed.

Invalid or Missing Documentation: Florida courts require plaintiffs to attach the contract or account application to the lawsuit. If they sue on a credit card debt without attaching the cardholder agreement or account statements showing how they calculated the balance, their case is legally deficient.

Bankruptcy Discharge: If the debt was previously discharged in a Chapter 7 or Chapter 13 bankruptcy, it is highly illegal for a collector to sue you or attempt to collect it.

Mistaken Identity: The debt belongs to someone else with a similar name, or you were the victim of identity theft.

If you happen to be researching rules in other states, you might look at Defenses in a Debt Collection Case - Michigan Legal Help or read up on How To Defend and Dismissed Debt Collectors Lawsuit in Michigan? from experienced Collections / Creditor - Debtor Rights Attorneys in Michigan . However, in Florida, you must follow the Florida Rules of Civil Procedure. For a deeper dive into these strategies, read our comprehensive Debt Lawsuit Defense Guide.

The 5-Year Florida Statute of Limitations

The statute of limitations is one of your strongest affirmative defenses. It is the legal deadline for a creditor to file a lawsuit against you. Once this window closes, the debt becomes "time-barred." While they can technically still write or call you to ask for payment, they cannot legally sue you or threaten to sue you.

In Florida, the deadlines are:

Written Contracts: 5 years (this includes credit cards, medical bills, auto loans, and personal loans).

Oral Contracts: 4 years.

The clock typically starts ticking from the date of your first missed payment (the date of default).

Warning: Do not make a partial payment or sign a written acknowledgment of an old debt. Doing so can restart the statute of limitations clock, resetting their 5-year window to sue you!

Post-Judgment Executions: Wage Garnishment, Levies, and Exemptions

If a creditor wins a lawsuit and gets a judgment, that judgment remains valid in Florida for up to 20 years and can be renewed for another 20 years. Armed with a judgment, the creditor can pursue several aggressive methods to collect:

Writ of Garnishment: Directed to your employer to seize a portion of your paycheck.

Bank Account Levy: Directed to your bank to freeze and seize funds in your accounts.

Property Seizures: Seizing non-exempt personal property or placing a lien on your real estate.

However, Florida is incredibly debtor-friendly. Our laws provide robust exemptions to protect your hard-earned income and assets from being wiped out. To understand your protections under the law, you can consult the Debtors' Rights in Florida pamphlet and review our detailed guide on Florida Wage Garnishment Laws.

Florida Asset Exemptions Comparison

Exemption Type | Protection Amount / Rules | Key Requirements |

|---|---|---|

Homestead Exemption | Unlimited equity in primary residence | Up to 0.5 acres in a city; up to 160 acres in rural areas |

Head-of-Family Wages | 100% exempt if net income is $750/week or less | Must provide more than 50% of support for a dependent |

Personal Property | Up to $1,000 (up to $5,000 if not using Homestead) | Per individual under the Florida Constitution |

Motor Vehicle | Up to $5,000 of equity protected | Can combine with personal property exemption |

Joint Spousal Property | Protects assets held as "Tenancy by the Entirety" | Debt must be owed by only one spouse, not both |

The Florida Head-of-Family Wage Exemption

If you qualify as a "head of family" (sometimes called head of household), your wages are entirely exempt from garnishment if you earn $750 or less per week in net pay.

To qualify, you must provide more than half of the financial support for a child, spouse, or other dependent (such as an elderly parent). If your net wages exceed $750 per week, they can only garnish the amount allowed under federal law (typically up to 25% of your net pay), but only if you have agreed in writing to allow the garnishment. Without your written consent, they cannot garnish your wages at all if you are a head of family.

How to claim it: If you receive a notice of garnishment, you must act quickly. You have 20 days from receiving the garnishment packet to file a formal "Claim of Exemption and Request for Hearing" form with the court clerk. To learn more about this process, read our article on Homestead Exemption Wage Garnishment.

Protecting Your Home and Personal Property

Florida offers some of the strongest property protections in the nation:

Homestead Protection: Your primary residence is completely protected from forced sale by judgment creditors, regardless of how much equity you have in the home. This protection applies to up to half an acre of land in an incorporated city or up to 160 acres in an unincorporated area.

Personal Property Exemption: You can protect up to $1,000 of personal property (furniture, electronics, clothing, etc.). However, if you do not claim or benefit from the homestead exemption, you can claim an additional $4,000 "wildcard" exemption, bringing your total personal property protection to $5,000.

Vehicle Exemption: You can protect up to $5,000 of equity in a single motor vehicle.

Spousal Exemption: If an asset (like a bank account or home) is owned jointly by a married couple as "Tenancy by the Entireties," a creditor cannot touch it if the judgment is against only one spouse.

How to Report Violations and Sue Debt Collectors for Damages

If a collector violates your Florida debt lawsuit rights, you do not have to sit back and take it. You can turn the tables and go on the offensive.

First, document everything. Keep a detailed call log, save all voicemails, take screenshots of text messages, and keep every letter they send you.

Next, you can file formal complaints with:

The Federal Trade Commission (FTC)

The Consumer Financial Protection Bureau (CFPB)

The Florida Office of Financial Regulation (OFR)

Finally, you can sue the collection agency in federal or state court. Under the FDCPA, you have one year from the date of the violation to file a lawsuit. If you win, you can recover statutory damages, actual damages, and your attorney's fees.

Conclusion

Facing a debt collection lawsuit in Florida can feel like stepping into a boxing ring without gloves. But when you understand your Florida debt lawsuit rights, the playing field levels out immediately. The collectors are relying on your fear and silence to get a quick, cheap default judgment. By simply standing up, filing an Answer, and asserting your defenses, you disrupt their business model.

At KillDebt, we believe that high-quality legal defense shouldn't cost thousands of dollars in attorney fees. That’s why we built our DIY legal defense system powered by ParkerGPT — an AI trained specifically on consumer debt law and real-world court strategies developed over 30+ years by our founding attorney, Brian Parker.

Unlike generic AI tools, ParkerGPT analyzes your actual lawsuit documents, uncovers critical weaknesses in the collector's case, and generates court-ready responses with simple, step-by-step instructions.

We have also rolled out our brand-new Court Tester tool. Court Tester is an advanced AI courtroom simulation built on your actual case. You can upload your real court filings, and within minutes, you will be practicing your arguments in front of an AI judge, facing off against AI opposing counsel, while a private AI co-counsel whispers winning strategies directly to you.

Don't let debt collectors dictate your financial future. Empower your legal defense with KillDebt today and take control of your case.

Get started with KillDebt pricing

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments.

Frequently Asked Questions (FAQ)

What happens if I ignore a debt collection lawsuit in Florida?

If you ignore the lawsuit, the plaintiff will win by default. This default judgment gives them the immediate power to garnish your wages, freeze your bank accounts, and place liens on your property. If you find yourself in this situation, you must act immediately to see if you can file a motion to vacate the judgment. To learn how, read How to Vacate Judgment.

Can a debt collector contact my family or employer in Florida?

Generally, no. They can only contact your employer or family members once, and solely for the purpose of obtaining your location information (address, phone number, or workplace). They are strictly prohibited from telling your family or employer that you owe money or discussing the details of your debt.

How long does a judgment last in Florida?

A court judgment in Florida is valid and enforceable for up to 20 years. Additionally, a judgment creditor can record a certified copy of the judgment to create a lien on your real estate, which lasts for 10 years and can be renewed for an additional 10 years.