When a Paycheck Is on the Line: What You Need to Know About Homestead Exemption Wage Garnishment

Homestead exemption wage garnishment laws can be the difference between keeping your paycheck and losing a chunk of it to a creditor — and most people facing garnishment don't even know these protections exist.

Here's the quick answer:

A homestead exemption protects equity in your primary home from creditors

In some states — especially Virginia — it can also be used to shield garnished wages, if you file the claim at the right time

In Florida, a separate but powerful head-of-household wage exemption protects all net earnings up to $750/week — and that protection follows your money into your bank account for up to 6 months

Four states (Texas, Pennsylvania, North Carolina, South Carolina) ban wage garnishment entirely for consumer debts

Federal law limits garnishment to the lesser of 25% of disposable earnings or the amount above $217.50/week — but state law can do much better

The catch? You have to claim these protections. They don't kick in automatically. Miss the deadline on your garnishment summons, and you could lose your right to fight back entirely.

I'm Brian Parker, and I've spent over 30 years in courtrooms defending consumers against creditors, debt buyers, and collection law firms — including fighting homestead exemption wage garnishment cases where the right filing at the right moment made all the difference. In this guide, I'll walk you through exactly how these protections work and how to use them before it's too late.

What is a Homestead Exemption and How Does It Protect You?

At its core, a homestead exemption is a legal shield designed to keep you from becoming homeless. It protects a specific amount of equity (and in some states, an unlimited amount) in your primary residence from being seized by judgment creditors to pay off debts.

If a creditor wins a debt collection lawsuit against you, they usually receive a judgment. With that judgment in hand, they can place a judgment lien on your property or attempt a forced sale. However, the homestead exemption ensures that a designated dollar amount of your home's value is completely off-limits to these creditors.

How much is protected depends heavily on where you live. For a complete breakdown of how each state handles this protection, you can review the Homestead Exemptions by State: Creditor Protection Comparison Chart.

It is important to remember that homestead exemptions only protect you against unsecured creditors (like credit card companies, medical debt collectors, or personal loan providers). They will not stop a foreclosure if you stop paying your mortgage, nor will they protect you from property tax liens or federal tax levies.

Understanding the Link Between Homestead Exemption and Wage Garnishment

You might be wondering: What does a home exemption have to do with my weekly paycheck?

In many jurisdictions, the legal definitions of "homestead" and "personal property" exemptions overlap. When a creditor attempts to garnish your wages or execute a bank levy, they are targeting your disposable earnings. In certain states, the law allows you to apply your unused homestead exemption balances or general personal property exemptions to shield cash, bank accounts, and even active wage garnishments from being handed over to a creditor.

This is a critical strategy in urgent self-defense. If a creditor has already won a debt collection lawsuit and obtained a judgment, they will typically target your bank account next. To understand how they do this and what is at risk, read our guide on Can Debt Collectors Take My Wages and Bank Account.

By understanding how state laws allow for "asset conversion" or the application of homestead deeds to cash assets, you can legally block a creditor's attempt to siphon money directly from your employer or your checking account.

How to Claim a Homestead Exemption for Wage Garnishment in Virginia

Virginia has a highly specific and unique method for using a homestead exemption to protect wages. Under Virginia Code § 34-17, a debtor can set apart their homestead exemption to protect garnished wages, but the timing is incredibly strict.

To protect your wages using this method, you must file a Homestead Deed in the land records of the city or county where you live, and then file a Request for Exemption Hearing (Form DC407) with the court.

The Deadline: You must file this claim after the garnishment summons is served on your employer, but prior to or upon the return date listed on the garnishment summons. If you miss this date, the court will order the money turned over to the creditor, and your opportunity is gone.

The Limits: Virginia's homestead exemption protects up to $5,000 per person in real or personal property (which can include wages). This amount doubles to $10,000 for individuals who are 65 or older, and you can add an additional $500 for each dependent you support.

Can You Use a Homestead Exemption for Wage Garnishment in Other States?

Other states also allow residents to protect their wages or bank balances using state-specific property and homestead exemptions:

Oklahoma: Under the 2023 Oklahoma Statutes Title 31. Homestead and Exemptions §31-1, residents can protect their principal residence (including manufactured homes) from forced sale. Additionally, Oklahoma automatically exempts 75% of all current wages earned during the last 90 days from garnishment.

Wisconsin: According to Wisconsin Statutes § 815.20 (2025), the homestead exemption protects up to $75,000 in equity. While this primarily protects the physical home, Wisconsin courts have historically interpreted exemption laws broadly to protect the debtor's basic comforts, and temporary absences do not impair this protection.

Arkansas: Arkansas takes a different approach, exempting the first $25 of weekly net wages automatically, plus up to 60 days' worth of wages, provided the total claimed does not exceed the state's personal property exemption limits ($500 for married residents/heads of households).

State-by-State Comparison: Virginia vs. Florida vs. Other States

Because asset protection laws are determined at the state level, the amount of protection you receive depends entirely on your zip code.

Below is a comparison of how different states handle homestead and wage protections as of May 2026:

State | Homestead Exemption Limit | Wage Garnishment Protection | Unique Asset Protection Rules |

|---|---|---|---|

Florida | Unlimited (Constitutional) | 100% exempt up to $750/week for Head of Household | 6-month bank account protection; broad Tenancy by the Entirety |

Michigan | Up to $40,000 (adjusted for inflation) | Follows federal limits (75% protected) | Strong protections for married couples holding joint bank accounts |

Virginia | $5,000 (doubles if 65+) | Follows federal limits; can use Homestead Deed to protect wages | Strict deadlines to file Homestead Deed before the return date |

Kansas | Unlimited (Acreage limits apply) | 75% of disposable earnings protected | Must use state exemptions; see the Kansas Bankruptcy Exemptions Calculator (2026) |

For Michigan residents, keeping your home safe is straightforward but capped. You can learn more about the specific limits by checking Michigan's homestead exemption rules.

Florida's Powerful Homestead and Wage Protections

Florida is widely considered the strongest asset protection state in the country. If you live in Florida, you have access to a suite of constitutional and statutory protections that can stop creditors cold.

First, Florida offers an unlimited homestead exemption for your primary residence (up to 1/2 acre in a municipality or 160 acres in an unincorporated area).

Second, Florida's wage protections are incredibly robust. Under the Head of Household Exemption, if you provide more than half of the financial support for a child or other dependent, your wages are 100% exempt from garnishment if your net earnings are $750 or less per week.

Even better, Florida extends this protection to your bank account. Under Fla. Stat. 77.041, these exempt wages remain completely protected for up to six months after they are deposited into your financial institution, even if they are commingled with other funds, as long as they can be traced back to your earnings.

States with Complete Wage Garnishment Bans

If you are lucky enough to reside in one of these four states, creditors cannot touch your paycheck for ordinary consumer debts (like credit cards, medical bills, or personal loans) at all:

Texas

Pennsylvania

North Carolina

South Carolina

In these states, wage garnishment is reserved almost exclusively for child support, alimony, taxes, and federal student loans. For standard credit card judgments, your wages are completely safe from garnishment.

Other Crucial Exemptions to Protect Your Wages and Assets

If you do not qualify for a homestead exemption or a head-of-household wage protection, you still have options to shield your assets from collection.

State and federal laws provide several other common exemptions:

Personal Property Exemptions: Most states allow you to protect a baseline amount of personal property. For example, in Florida, you can protect up to $4,000 of personal property per person if you do not claim the homestead exemption.

Vehicle Exemptions: You can protect a portion of equity in your vehicle (e.g., up to $1,000 in Florida, which can be combined with other personal property exemptions).

Retirement Accounts: ERISA-qualified retirement plans, 401(k)s, and IRAs are almost universally protected from judgment creditors. In Florida, all IRA types—including inherited IRAs—are protected without any dollar cap.

Federal Benefits Protection: Federal law automatically requires banks to protect up to two months of direct-deposited federal benefits (such as Social Security, VA benefits, and federal retirement) from being frozen or garnished.

To learn more about how to assert these rights in Florida, refer to Debtors' Rights in Florida: Claiming Your Exemptions From Judgments.

Step-by-Step Guide: How to Assert Your Exemptions and Stop Garnishment

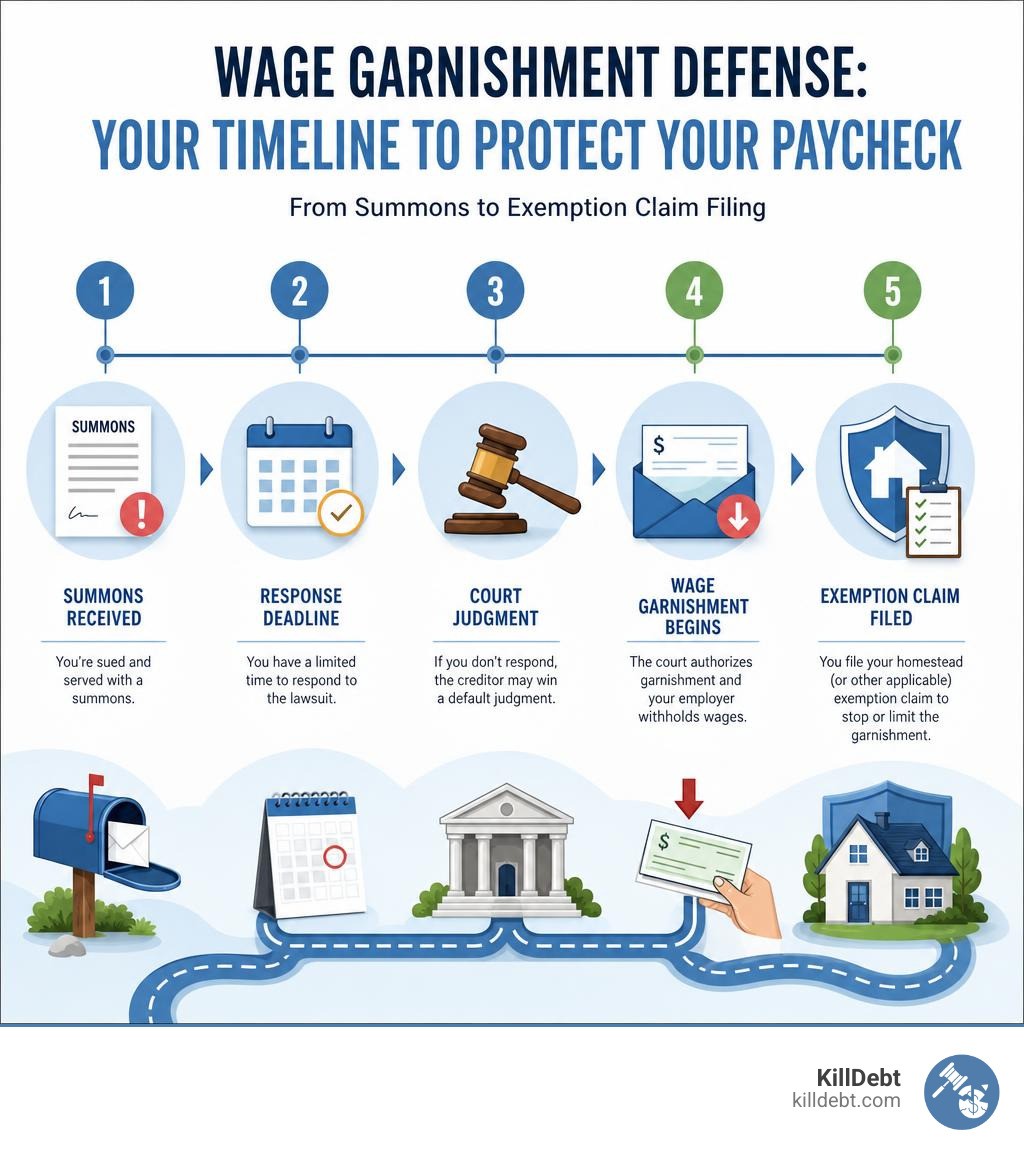

If you have received a garnishment summons or a notice of a bank levy, you must act quickly. This is a time for urgent self-defense.

Here is the step-by-step process to protect your money:

Do Not Ignore the Summons: A garnishment is usually the result of a default judgment because a debtor ignored a prior debt collection lawsuit. If a Civil Judgement Collection Agency is contacting your employer, the clock is ticking.

Obtain the Exemption Form: Your employer or bank is legally required to provide you with a notice of garnishment and an exemption claim form (such as Form DC407 in Virginia or the Claim of Exemption form under Florida Statute 77.041).

Fill Out and Notarize the Form: Clearly list the exemptions you are claiming (e.g., Head of Family, Homestead, or Social Security benefits).

File and Serve within the Deadline: In Florida, you have exactly 20 days from receiving the notice to file your claim with the court clerk and mail copies to the creditor and the garnishee (your bank or employer).

Prepare for the Hearing: If the creditor objects to your exemption claim, the court will schedule a hearing. If they do not object within the statutory timeframe (usually 8 to 14 business days), the garnishment must be dissolved.

Warning: Be careful not to sign any contracts that contain a "waiver of exemptions." Some predatory lenders insert clauses where you voluntarily waive your right to claim a homestead or wage exemption. Always read the fine print before signing loan documents.

Take Control of Your Financial Future with KillDebt

Facing a wage garnishment or a bank levy is stressful, but you do not have to navigate the complex legal system alone. Hiring an expensive attorney isn't your only option to protect your hard-earned wages and your home.

At KillDebt, we provide a DIY legal defense system powered by ParkerGPT—an AI trained specifically on consumer debt law and real-world court strategies developed over 30+ years by myself, attorney Brian Parker.

Unlike generic AI tools, ParkerGPT analyzes your actual lawsuit or garnishment documents, identifies critical procedural weaknesses, and generates court-ready responses with simple, step-by-step instructions.

And if you want to practice before you step into a real courtroom, our brand-new Court Tester allows you to run an AI courtroom simulation. You can upload your actual filings and argue your motion in front of an AI judge, against AI opposing counsel, while a private AI co-counsel whispers winning strategies directly to you.

Don't let debt collectors take what is yours. Protect your wages and home with KillDebt today, and stop wage garnishments in their tracks.

Frequently Asked Questions (FAQ)

Can a homestead exemption protect my wages if they are already in my bank account?

Yes, but only in certain states and only if you can trace the funds. In Florida, wages protected by the head-of-household exemption remain protected for six months after deposit, even if they are commingled with other money. You must be prepared to show bank statements tracing those deposits back to your payroll.

Can I lose or waive my homestead exemption rights?

Yes. You can lose your homestead protections if you permanently relocate to another state, abandon the property as your primary residence, or engage in a fraudulent transfer (such as transferring the title of your home to a relative solely to hide it from creditors). You can also waive these rights contractually in some states, though Florida makes waiving head-of-family protections highly difficult, requiring specific disclosures in 14-point type.

What is the difference between federal and state wage garnishment limits?

Federal law sets the absolute baseline: creditors can garnish no more than 25% of your disposable weekly earnings, or the amount by which your weekly pay exceeds 30 times the federal minimum wage ($217.50 per week), whichever is less. However, states are free to create much stronger protections. For example, Florida protects 100% of wages for heads of household earning under $750/week, and Michigan provides its own set of protective calculations.