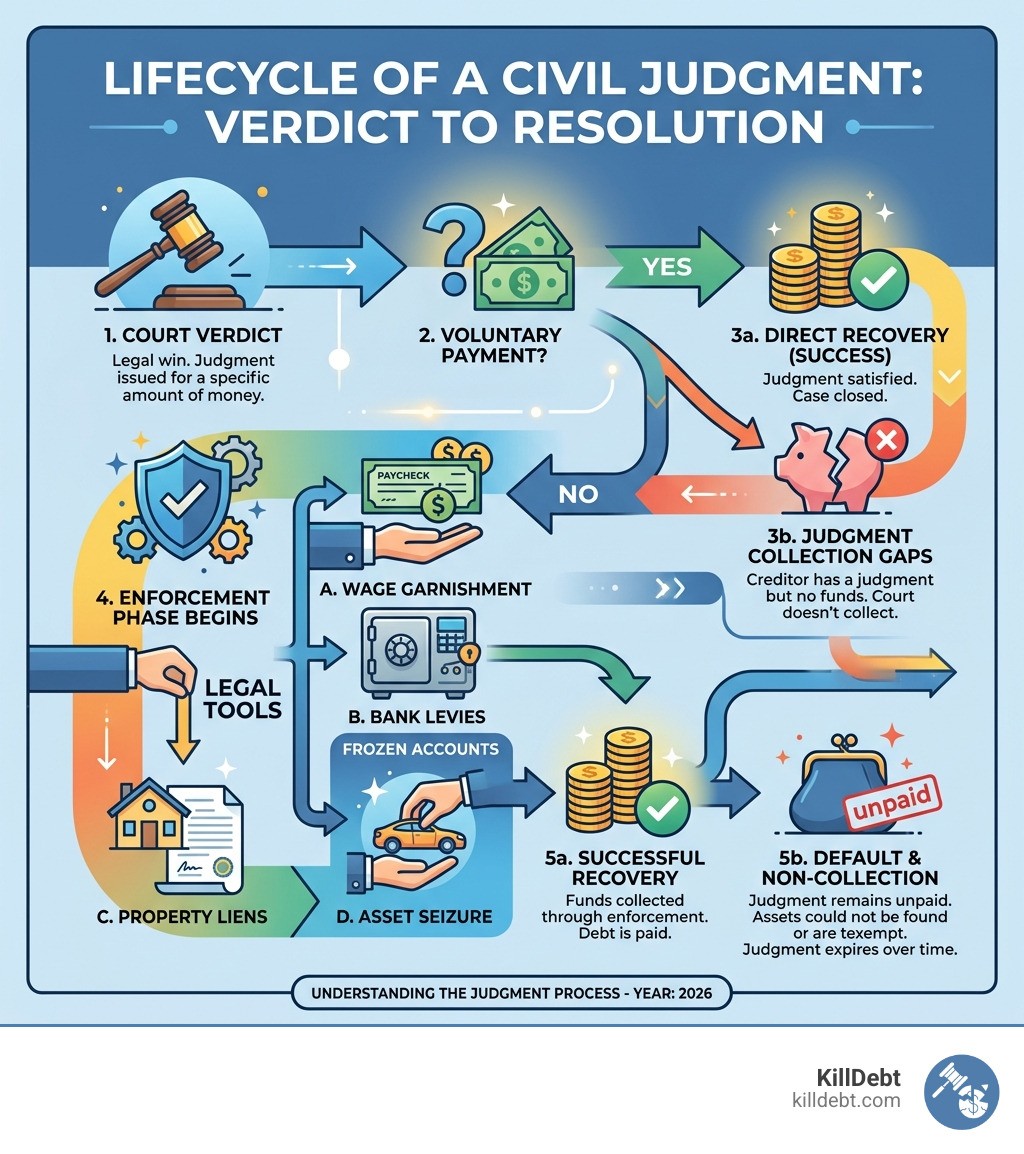

When a Court Win Doesn't Mean Getting Paid: The Civil Judgment Collection Gap

A civil judgement collection agency is a specialized firm that enforces unpaid court judgments on behalf of creditors - locating debtor assets and using legal tools like wage garnishment, bank levies, and property liens to recover money the court has already awarded.

Here's what you need to know at a glance:

What it is | A company hired to enforce an existing court judgment |

|---|---|

Who uses them | Creditors who won in court but haven't been paid |

Main tools used | Wage garnishment, bank levies, property liens, asset seizure |

Typical cost | Contingency fee (% of recovery) or outright judgment purchase |

Minimum judgment | Usually $1,000-$10,000+ depending on the agency |

Key law governing collectors | Fair Debt Collection Practices Act (FDCPA) |

Winning a lawsuit feels like the finish line. But for most people, it's only the beginning of a much harder fight.

According to the American Bar Association, over 80% of civil judgments are never collected. The court hands you a piece of paper saying you're owed money. What it doesn't do is put that money in your bank account.

That gap - between a legal win and actual payment - is exactly where civil judgment collection agencies operate.

Whether you're a creditor trying to recover what you're owed, or a debtor suddenly facing enforcement actions, understanding how this process works is critical. Enforcement can mean frozen bank accounts, garnished paychecks, or liens on property - often without much warning.

This guide breaks down the full process in plain language, so you know exactly what to expect on either side of a judgment.

Understanding the Role of a Civil Judgement Collection Agency

When a court issues a judgment, it is essentially a legal declaration that one party owes another a specific amount of money. However, the court does not act as a collection service. It is the responsibility of the creditor to actually get the money. This is where a civil judgement collection agency steps in.

These agencies are not your typical "call and harass" debt collectors. They are Judgment Recovery Specialists who focus specifically on the post-judgment phase. Their work involves deep-dive asset tracing, skip-tracing (finding people who have moved or are hiding), and professional enforcement of court orders.

A civil judgement collection agency employs a team that often includes private investigators, skip-tracers, and specialized attorneys. Their goal is to turn that piece of paper from the judge into actual cash. They operate under strict legal frameworks, including the Fair Debt Collection Practices Act (FDCPA), which dictates how they can interact with debtors. If you are on the receiving end of these calls, it is vital to understand What is a Debt Collector Under the FDCPA? Your Rights Explained to ensure your rights aren't being trampled during the enforcement process.

Why 80% of Civil Judgments Go Uncollected

It is a staggering statistic: nearly 80% of all civil judgments are never recovered. But why is the "success rate" of the American legal system so low when it comes to actually paying out?

The primary reason is debtor resistance. Many debtors, especially in business disputes, are experts at "judgment proofing" themselves. This includes:

Hiding Assets: Moving money into offshore accounts, or transferring ownership of property to relatives or "shell" companies.

Layered Ownership: Creating complex corporate structures where the entity that owes the debt has no actual assets, while a sister company holds all the wealth.

Lack of Information: Creditors often don't know where the debtor works or where they bank, making it impossible to trigger garnishments.

Aged Judgments: The longer a judgment sits, the harder it is to collect. People move, businesses close, and assets dissipate.

For many individuals, Struggling with Debt Collectors becomes a game of cat and mouse. Without the specialized tools of a civil judgement collection agency, most creditors simply give up because the cost of finding the money exceeds the value of the judgment itself.

Common Methods Used by a Civil Judgement Collection Agency

To beat the 80% failure rate, agencies use high-tech and high-pressure tactics. They don't just wait for a check to arrive in the mail; they go hunting.

The process usually begins with a "digital magnifying glass" approach. Agencies use proprietary financial databases and public records to build a profile of the debtor’s life. They look for real estate filings, vehicle registrations, and even professional licenses. In states like Florida, the process is very specific; for instance, you can learn How to Collect a Judgment in Florida through the Division of Corporations, where judgment liens are filed to "attach" to a debtor's personal property.

Enforcement Tactics: Garnishment, Liens, and Levies

Once assets are located, the agency moves to seize them. This is the "teeth" of the judgment.

Wage Garnishment: The agency gets a court order requiring the debtor's employer to withhold a portion of their paycheck (usually up to 25% of disposable income) and send it directly to the creditor.

Bank Levies: This is often the most effective tool. The agency identifies where the debtor banks and "freezes" the account. The bank is then legally required to turn over the funds in the account up to the amount of the judgment.

Property Liens: A lien is placed against the debtor’s real estate. While it doesn't always result in immediate cash, the debtor cannot sell or refinance the home without paying off the judgment first.

Till Taps: In business cases, a "keeper" can be placed at a business location to take cash directly out of the register as sales are made.

If you're worried about these actions, you should read our guide on Can Debt Collectors Take My Wages and Bank Account? to see what the limits are in Michigan and Florida.

The Asset Discovery Process for a Civil Judgement Collection Agency

If a debtor’s assets aren't obvious, the agency uses "discovery" tools. This includes Debtor’s Examinations, where a debtor is forced to appear in court and answer questions under oath about their finances. If they lie, it’s perjury. If they don't show up, a judge can issue a bench warrant for their arrest.

Agencies also use subpoenas to get records from third parties, like banks, utility companies, or even the debtor’s customers. In Michigan, the process is detailed through resources like Michigan Legal Help, which outlines how to use the court system to force a debtor to reveal where their money is hidden.

Costs, Fees, and Choosing a Civil Judgement Collection Agency

Hiring a civil judgement collection agency isn't free, but the "price" depends on how much risk you want to take. Most agencies specialize in judgments over a certain amount—typically $5,000 or $10,000.

Feature | Contingency Model | Outright Purchase | Upfront Fee Model |

|---|---|---|---|

Cost to You | $0 upfront | $0 (You get paid) | Fixed initial fee |

Your Profit | 50% - 65% of recovery | 1% - 10% of judgment value | 100% of recovery |

Risk | Agency takes the risk | Agency takes the risk | You take the risk |

Speed | Slow (months/years) | Immediate cash | Varies |

When looking for Judgment Collection Services, it’s important to see if they offer "future pay" or "assignment" options.

Fee Structures: Contingency vs. Outright Purchase

Most people prefer the contingency model. The agency covers all the legal costs, filing fees, and investigator bills. In exchange, they keep a large percentage (often 50%) of whatever they recover. If they recover nothing, you owe nothing.

An outright purchase is different. Some agencies will "buy" your judgment for a small lump sum (pennies on the dollar). You get cash today, and they own the right to collect the full amount later. This is a great option if you just want to move on with your life. Understanding the Debt Collection Lawsuit Timeline can help you decide if you have the patience for a long-term contingency battle.

Criteria for Selecting a Civil Judgement Collection Agency

Not all agencies are created equal. When choosing, look for:

State-Specific Expertise: Enforcement laws in Michigan are very different from Florida. Ensure they know the local court rules.

BBB Accreditation: Look for an "A" rating to ensure they don't use illegal "strong-arm" tactics that could get you in legal trouble.

Industry Specialty: Some agencies focus on commercial debts, while others handle personal injury or small claims judgments.

In-House Legal Team: Do they have their own lawyers, or do they have to hire outside counsel?

You might wonder, Do I Need a Lawyer for a Debt Collection Lawsuit? Often, a specialized agency is more effective at the collection stage than a general practice attorney.

Debtor Rights and Legal Protections During Enforcement

If you are the one being collected against, don't panic. You still have rights. Even with a judgment, a civil judgement collection agency must follow the FDCPA. They cannot threaten you with violence, use profane language, or call you at 3:00 AM.

More importantly, certain assets are exempt from collection:

Social Security & VA Benefits: These are generally protected from garnishment by federal law.

Head of Household Exemptions: In Florida, if you provide more than half the support for a child or dependent, your wages may be entirely exempt from garnishment.

Tools of the Trade: Often, the equipment you need to work (like a mechanic's tools or a laptop) cannot be seized.

Primary Residence: Michigan and Florida have "homestead" protections that make it very difficult for a creditor to force the sale of your primary home.

The first step in defending yourself is often sending Debt Validation Letters. Even if there is a judgment, you have a right to see the accounting of how much is owed, including interest and fees. If you've just discovered a judgment against you, check out our Complete First Steps Guide.

Conclusion: Take Control of the Judgment Process

Whether you are a creditor tired of holding a worthless piece of paper or a debtor facing aggressive enforcement, the key is proactive defense and expert knowledge. A civil judgement collection agency has powerful tools, but they aren't invincible.

At KillDebt, we believe in leveling the playing field. We provide a DIY legal defense system powered by ParkerGPT, an AI trained specifically on consumer debt law and real court strategies developed over 30+ years by attorney Brian Parker.

If you’re being sued or facing a judgment, don't go in blind. Use our Court Tester—an AI courtroom simulation built on your actual case. You can upload your real filings and, within minutes, practice arguing your motion in front of an AI judge. You'll face AI opposing counsel while a private AI co-counsel whispers the winning strategy only you can see.

Don't let a judgment ruin your financial future. Whether you need to fight a lawsuit or settle a debt for pennies on the dollar, we have the tools to help you win.

Start your defense with KillDebt today and turn the tables on the collectors.

Frequently Asked Questions (FAQ)

How long does the judgment collection process usually take?

It varies wildly. If the debtor has a steady job and a known bank account, a civil judgement collection agency can start getting money in 30 to 60 days. However, if the debtor is "dodgy" or hiding assets, it can take years. Most judgments are valid for 10 to 20 years and can be renewed, so agencies are often willing to play the long game.

What happens if a judgment debtor has no visible assets or hides them?

If a debtor is truly "judgment proof" (no job, no bank account, no property), the agency will usually "monitor" them. They will run credit reports every few months. The moment the debtor gets a job, buys a car, or inherits money, the agency pounces. Some agencies use aggressive "veil piercing" to go after the owners of a business personally if they suspect fraud.

How can I check if there is a judgment against me and what should I do?

You won't find judgments on a standard credit report anymore due to changes in reporting laws. Instead, you need to check the "Public Records" at your local county clerk's office or the Secretary of State's office. If you find one, your first move should be to determine if you were properly served. If not, you may be able to "vacate" the judgment and fight the original case.