You Have a Summons — Here's How Remote Debt Lawsuit Filing Works

If you've just been handed a court summons, or found one in your mailbox, understanding remote debt lawsuit filing could be the difference between losing by default and actually defending yourself.

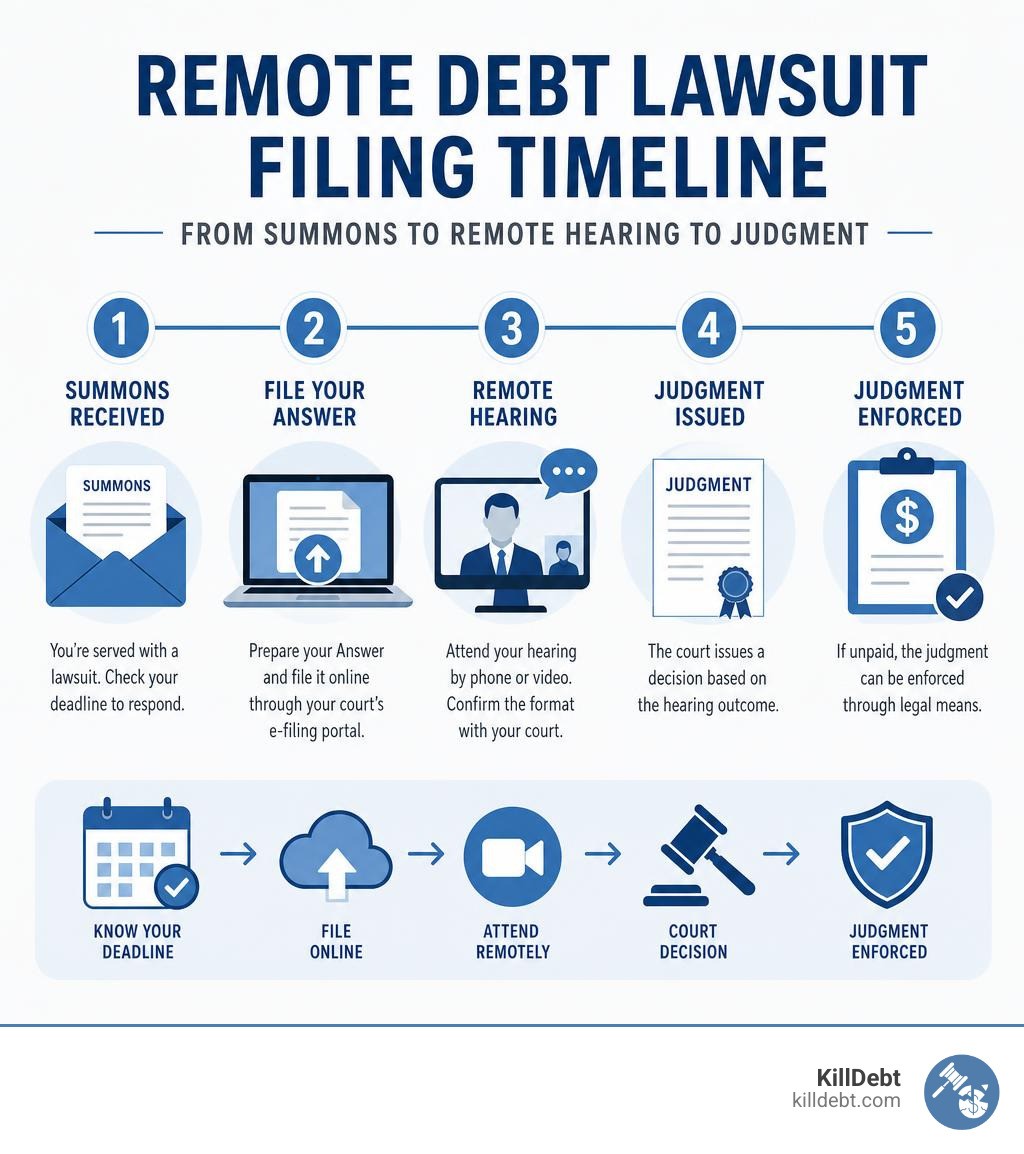

Quick answer — how to file or respond to a debt lawsuit remotely:

Check your deadline. Most states give you 14–30 days to respond after being served.

Access your state's e-filing portal. Courts in Florida, Illinois, Michigan, and most other states accept electronic filings online.

Prepare your Answer. Respond to each allegation in the complaint — admit, deny, or state you lack knowledge.

File and serve. Submit your Answer through the court's portal and send a copy to the plaintiff.

Attend remote hearings. Many courts now hold hearings by phone or video — confirm the format with your court.

Verify your filing was received. Check the court docket to confirm your documents were actually filed.

Every year, roughly 10 million Americans are sued for debt — and about 90% lose by default simply because they don't know how to respond in time. The shift to remote and electronic court processes has made it easier than ever to defend yourself without setting foot in a courthouse. But it has also created new traps: missed deadlines, technical failures, and digital scams designed to confuse people who are already overwhelmed.

This guide cuts through the confusion. Whether you just received a summons, a threatening collection letter, or a court date notice, you'll find clear, actionable steps here.

I'm Brian Parker, founder of KillDebt, and I've spent over 30 years in courtrooms fighting debt collectors, debt buyers, and collection law firms — including navigating the growing world of remote debt lawsuit filing as courts shifted to electronic and virtual processes. I've seen what works, what fails, and exactly where collectors try to exploit the confusion.

What is a Remote Debt Lawsuit Filing?

A remote debt lawsuit filing refers to the initiation, management, or defense of a debt collection lawsuit using electronic court portals, digital document exchanges, and virtual hearings instead of physical, in-person court visits.

Traditionally, when a creditor or debt buyer sued a consumer, they had to physically deliver paper documents to the courthouse clerk. The consumer then had to mail a paper response or physically hand-deliver it to the court, followed by driving to the courthouse for every minor hearing.

In May 2026, the legal landscape looks entirely different. Most jurisdictions have transitioned to robust electronic filing systems (e-filing) and virtual courtrooms. This means debt buyers can file thousands of lawsuits simultaneously with the click of a button. For consumers, it means you can access court dockets, file your legal response, and even argue your case before a judge right from your kitchen table.

However, ignoring a digital summons carries the exact same consequences as ignoring a physical one: a swift default judgment that allows the collector to garnish your wages or freeze your bank accounts. If you've just discovered a lawsuit filed against you, your absolute first step should be reading our What to Do When Sued by a Debt Collector: Complete First Steps Guide to stop the clock and protect your rights.

Feature | Traditional Debt Lawsuit | Remote Debt Lawsuit |

|---|---|---|

Filing Method | Physical paper delivery to the court clerk | Online upload via secure e-filing portals |

Response (Answer) | Mailed or hand-delivered paper forms | Electronic submission; immediate docket updates |

Court Appearances | Driving to the courthouse, waiting in line | Zoom, Microsoft Teams, or telephonic hearings |

Case Tracking | Waiting for mail or calling the court clerk | 24/7 access to digital court dockets |

Risk of Default | High (due to confusion or lost mail) | High (due to technical glitches or missed emails) |

How Courts Handle Remote Filings, Hearings, and Trials

Both state and federal courts have established digital frameworks to streamline civil litigation. While federal courts rely heavily on the PACER system, state courts—where the vast majority of consumer debt collection lawsuits are filed—have created localized e-filing portals and guidelines for virtual litigation.

When a creditor initiates a remote debt lawsuit filing, they upload their complaint and summons directly to the court’s electronic database. Once you are served, you must use these same digital pathways to file your Answer.

If your case proceeds past the initial filing stage, the court will likely schedule a remote hearing or conference. Instead of sitting on hard wooden benches in a crowded courtroom, you will log into a virtual platform like Zoom or Microsoft Teams. These virtual hearings are just as formal and legally binding as in-person proceedings. You must dress appropriately, speak only when prompted, and ensure your internet connection is stable.

To understand how these digital milestones fit into the broader litigation process, review our guide on the Debt Collection Lawsuit Timeline: What Happens Next After You're Served.

State-Specific Rules for Remote Debt Lawsuit Filing

Because court rules are highly localized, how you navigate a remote debt lawsuit filing depends entirely on where you live. Since we operate and focus our expertise in Florida and Michigan, let’s look at how these two states handle remote litigation:

Florida Remote Litigation Rules

Electronic Portals: Florida relies on the Florida Courts E-Filing Portal for all civil submissions. This secure portal allows self-represented (pro se) litigants to register for a free account, upload documents, and pay any necessary filing fees electronically.

Specialized Debt Subtypes: Florida courts have modernized how they categorize these cases. For instance, in Miami-Dade County, the Eleventh Judicial Circuit introduced a New Case Subtype for Consumer Debt Cases Now Available on Florida's e-Filing Portal, allowing for better tracking and faster resolution of credit card and medical debt disputes.

Small Claims Rules: If your debt is under $8,000, it will likely proceed under Florida’s small claims rules. The Florida Bar provides detailed guidance on About Small Claims Collection Lawsuits - The Florida Bar , highlighting that pre-trial conferences are frequently held remotely via Zoom, where judges often order the parties to participate in virtual mediation to settle the debt before trial.

Michigan Remote Litigation Rules

Justice for All Initiative: Michigan has been a national leader in simplifying court access. Under the Michigan Supreme Court's Advancing Justice for All in Debt Collection Lawsuits initiative, the state has actively worked to reduce default judgments by providing clearer remote resources and standardized digital forms.

DIY Civil Answer Tools: If you are sued in Michigan, you do not have to draft an Answer from scratch. You can utilize the Do-It-Yourself Civil Answer tool provided by Michigan Legal Help to generate a legally sound response.

Remote Court Preparation: Michigan courts heavily utilize remote hearings for case management conferences. If you need to defend yourself in a Michigan courtroom virtually, review their official guide on Going to Court to Defend a Debt Collection Case to learn how to log in, present evidence, and follow local protocol.

Answering in Justice Courts: For smaller debt amounts filed in local district or justice courts, make sure to read our highly specific walkthrough on crafting a Justice Court Debt Answer.

Consumer Protections and Abusive Debt Collectors in the Digital Era

While remote court procedures offer convenience, they have also emboldened abusive, fraudulent, or "phantom" debt collectors who use digital tools to scale their harassment. Fortunately, federal consumer protection laws still apply with full force in the digital space.

The Fair Debt Collection Practices Act (FDCPA) and the Consumer Financial Protection Bureau’s (CFPB) Regulation F govern how debt collectors can communicate with you. Regulation F explicitly limits how often collectors can call you and outlines strict rules for digital communications, including emails, text messages, and social media direct messages.

If you've been targeted by collection efforts, acting quickly is vital. Learn exactly how to handle the initial onslaught by reading our guide on what to do if you are Sued for a Debt? Here's Exactly What to Do in the First 7 Days.

To put the scale of abusive debt collection into perspective, look at these recent enforcement actions taken by the Federal Trade Commission (FTC):

Stark Law Scheme: The FTC and the Illinois Attorney General returned more than $4 million to over 10,000 consumers targeted by the Stark Law phantom debt collection scheme, which coerced consumers into paying debts they did not actually owe.

GAFS Group: The FTC sent payments totaling more than $1 million to 1,966 consumers harmed by a massive debt collection scheme involving GAFS Group, LLC and its related entities.

Robocall Violations: In 2023, the FTC returned more than $540,000 in refunds to consumers harmed by abusive collectors who used illegal robocalls and deceptive threats of arrest or immediate lawsuits.

Fake New York Debts: In October 2021, the FTC returned $772,512 to consumers targeted by a New York-based debt collection scheme involving entirely fabricated debts.

Georgia-Based Settlement: The FTC mailed refund checks totaling more than $516,000 to 3,977 consumers as part of a settlement with an abusive Georgia-based debt collection business.

These statistics prove that just because a collector files a lawsuit or threatens you with a remote debt lawsuit filing, it does not mean their claim is legitimate or that they have followed the law.

Spotting Illegal Tactics in a Remote Debt Lawsuit Filing

When defending against a remote lawsuit, you must watch for specific illegal tactics frequently employed by predatory collectors:

Shortened Validation Periods: Under Regulation F, a debt collector must provide a validation notice containing specific details about the debt. They must calculate the validation period end date as at least 30 days after the assumed receipt date (which is legally defined as 5 business days after the letter was mailed, excluding weekends and public holidays). Deceptive collectors often artificially shorten this window to pressure you into paying. This exact violation was the basis of the federal class-action lawsuit Nicholas Jeffers v. Arcon Credit Solutions, LLC.

"Rent-a-Tribe" High-Interest Schemes: Some online payday lenders try to bypass state usury laws (which cap interest rates in Florida and Michigan) by partnering with Native American tribes to claim "sovereign immunity." They then use collection agencies to threaten out-of-state borrowers. As detailed in the class action Rachel Lessen v. FSST Management Services, LLC, these loans—sometimes carrying APRs exceeding 700%—are often legally void in the consumer's home state, and their collection can be successfully challenged.

Communicating with Represented Consumers: Under FDCPA Section 1692c(a)(2), if a debt collector knows you are represented by an attorney, they are strictly prohibited from contacting you directly. In Renee Clancy v. Radius Global Solutions, LLC, a collector faced federal liability for sending direct payment demands to a consumer months after being notified of legal representation.

Foreclosure and Preclusion Scams: Debt buyers sometimes attempt to file remote collection suits on debts that have already been resolved or are barred by prior foreclosure actions. If a collector files a lawsuit that is legally barred by prior court rulings, you can move to dismiss it under legal doctrines like claim preclusion, as demonstrated in Buczek v. Setrus LLC.

Unauthorized Account Seizures: In complex digital disputes, aggressive creditors may attempt to seize online accounts or digital assets without proper court orders, violating non-disclosure agreements or terms of service. Such digital overreaches are heavily litigated in federal courts, as seen in cases like Krishna Okhandiar and Remilia Corporation LLC v. John Duff III.

Step-by-Step: How to Defend Yourself Remotely

If you have been served with a lawsuit, do not panic. The remote filing system allows you to mount a powerful defense right from your computer. Follow these steps to protect yourself:

Step 1: Calculate Your Deadline

As soon as you receive the summons, look at the date you were served. In Florida and Michigan, you typically have 20 to 30 days to file a response. Missing this deadline is the single biggest mistake consumers make. To make sure you don't miss your window, read our breakdown on the Time to Respond to Debt Collection Lawsuit.

Step 2: Draft Your Answer

Your "Answer" is a formal written response to the collector’s Complaint. You must address every single numbered paragraph in their Complaint. For each paragraph, you have three options:

Admit: You agree the statement is 100% true (e.g., your name is spelled correctly).

Deny: You dispute the statement (e.g., you deny that you owe the specific amount claimed). Note: Denying a claim forces the debt collector to actually prove it with real evidence.

Deny for Lack of Knowledge: You do not have enough information to know if the statement is true (e.g., if they claim they purchased the debt from a specific bank on a specific date).

For step-by-step drafting instructions, read How to Answer a Debt Summons. You can also look at a Sample Answer to Debt Collection Lawsuit or download a Debt Summons Response Letter Sample to see exactly what this document should look like.

Step 3: Assert Affirmative Defenses

An affirmative defense is a legal reason why the collector cannot win, even if the debt was originally yours. Common defenses include:

Statute of Limitations: The debt is too old to legally sue over (in Florida, the limit is generally 5 years; in Michigan, it is 6 years).

Lack of Standing: The debt buyer cannot prove they actually own your specific account through a complete chain of title.

Paid or Settled: The debt was already resolved.

Step 4: File the Answer Electronically

Log into your state's e-filing portal (such as the Florida E-Filing Portal or MiFILE in Michigan). Upload your Answer in PDF format, pay any required fee (or file a fee waiver if you qualify), and submit it. To understand what happens once your paperwork is submitted, check out our guide on What Happens After Summons.

Step 5: Serve the Plaintiff

You must send a copy of your filed Answer to the debt collector's attorney. In a remote lawsuit, this is usually handled automatically through the e-filing portal's electronic service system, but you must double-check that their correct email address is listed.

Preparing Evidence for a Remote Trial

If your case goes to trial, it will likely be conducted over a video conferencing platform. Preparing for a virtual trial requires a unique set of preparation steps:

Respond to Discovery Requests: Before trial, the collector may send you "Requests for Admission" or "Interrogatories" (written questions). You must answer these in writing within strict deadlines. Failing to respond to discovery requests can result in the court automatically assuming you admit to everything, causing you to lose the case instantly.

Organize Your Electronic Evidence: Gather your bank statements, proof of payments, or debt dispute letters. Convert them into clear, legible PDF files. You must upload these documents to the court portal and serve them to the opposing attorney well in advance of the trial date.

Prepare Your Virtual Space: Treat the video call like a real courtroom. Find a quiet, well-lit room with a neutral background. Test your microphone and camera ahead of time.

Understand "Judgment Proof" Status: If you genuinely have no income or assets that can legally be seized (such as relying solely on protected Social Security benefits, disability, or making below the state-protected wage threshold), you may be "judgment proof." Even if the creditor wins a judgment, they cannot legally take your protected income. Be prepared to present a financial affidavit at a remote periodic payment hearing to prove this status.

To build a comprehensive strategy for your day in court, read our ultimate guide: Fight Debt Collection Lawsuit: Complete Guide.

Risks, Benefits, and Technical Considerations of Remote Litigation

Remote litigation is a double-edged sword. While it democratizes access to justice in many ways, it also introduces technical and procedural hurdles that can catch consumers off guard.

The Benefits

Convenience and Accessibility: You don't have to take a full day off work, pay for downtown parking, or arrange for childcare to attend a 10-minute hearing. You can participate from your home or even a parked car during your lunch break.

Reduced Courtroom Anxiety: Facing aggressive debt collection lawyers in a formal courtroom can be incredibly intimidating. Presenting your case through a screen can lower stress levels and help you stay focused on your arguments.

The Risks and Pitfalls

Automated Filing Failures: Many consumers turn to cheap, generic online document generation services to draft their answers. However, as highlighted in the federal class-action lawsuit Palanti v. Lawble, Inc., some of these automated services fail to actually file the documents with the court. The consumer assumes their defense is handled, only to discover weeks later that a default judgment was entered because the automated system glitched. Always verify your filing directly on the court's public docket.

The Digital Divide: If you do not have a reliable high-speed internet connection, a computer, or a smartphone, participating in a remote trial is incredibly difficult.

Privacy and Security Concerns: Remote litigation requires uploading highly sensitive financial documents—such as bank statements, tax returns, and Social Security numbers—to digital portals. You must ensure you are using secure, official court portals and never share sensitive documents via unencrypted email.

Take Control of Your Defense with KillDebt

Navigating a remote debt lawsuit filing can feel like trying to learn a foreign language while walking a tightrope. The electronic portals are confusing, the rules are rigid, and the stakes are incredibly high.

That is why we built KillDebt. We provide a DIY legal defense system powered by ParkerGPT—an advanced AI trained specifically on consumer debt law and real-world court strategies developed over 30+ years by veteran consumer defense attorney Brian Parker.

Unlike generic legal tools that simply fill in the blanks of a template, ParkerGPT:

Analyzes your actual lawsuit documents: Upload a photo or PDF of your summons and complaint.

Identifies legal weaknesses: The AI instantly spots FDCPA violations, expired statutes of limitations, or chain-of-title gaps.

Generates court-ready responses: Receive a customized Answer and Affirmative Defenses tailored specifically to Florida or Michigan court rules.

We also just rolled out our brand-new tool: Court Tester.

Court Tester is an AI courtroom simulation built directly on the facts of your actual case. You upload your real court filings, and within minutes, you are practicing your arguments in front of an AI judge, going head-to-head against an AI opposing counsel, while a private AI co-counsel whispers winning strategies in your ear that only you can see. It is the ultimate dress rehearsal, ensuring you are confident, prepared, and ready to win your remote hearing.

Don't let a debt collector win by default. Visit KillDebt today to analyze your summons for free and take control of your financial future.

Get started with KillDebt pricing

Important Legal Disclaimer

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments

Frequently Asked Questions (FAQ)

What happens if I miss a remote court hearing?

If you fail to log into a scheduled Zoom or telephone hearing, the judge will almost certainly enter a default judgment against you. This gives the collector the legal right to pursue wage garnishments, put liens on your property, or freeze your bank accounts. If you missed a hearing due to an emergency or because you never received the link, you must immediately file a "Motion to Vacate Default Judgment," explaining your excusable neglect.

Can a debt collector sue me online without serving physical papers?

No. While the lawsuit itself is managed remotely, the constitutional right to due process requires that you are properly notified of the lawsuit. In Florida and Michigan, "service of process" generally requires a process server or sheriff to physically hand you the summons and complaint, or leave it with a resident of your household. Some states allow service by certified mail. While some courts are experimenting with electronic service (via email or social media) in extreme cases where a defendant is actively hiding, physical service is still the standard requirement.

How do I know if a remote debt lawsuit filing is legitimate?

Scammers frequently send fake court summonses or emails claiming you have been sued in an attempt to scare you into making an immediate payment. To verify if a lawsuit is real: 1 Search the official court docket: Go to the county clerk’s website for the county where you live and search your name in their public records. 2 Call the clerk of court: Find the official phone number for your local courthouse and ask the clerk to verify if a case has been filed under your name. 3 Never pay over the phone immediately: A legitimate court will never demand payment via gift cards, wire transfers, or cryptocurrency to settle a lawsuit.