What to Do If You're Facing an Auto Loan Repo Lawsuit

If you've received a court summons over a repossessed car, here's what you need to know right now:

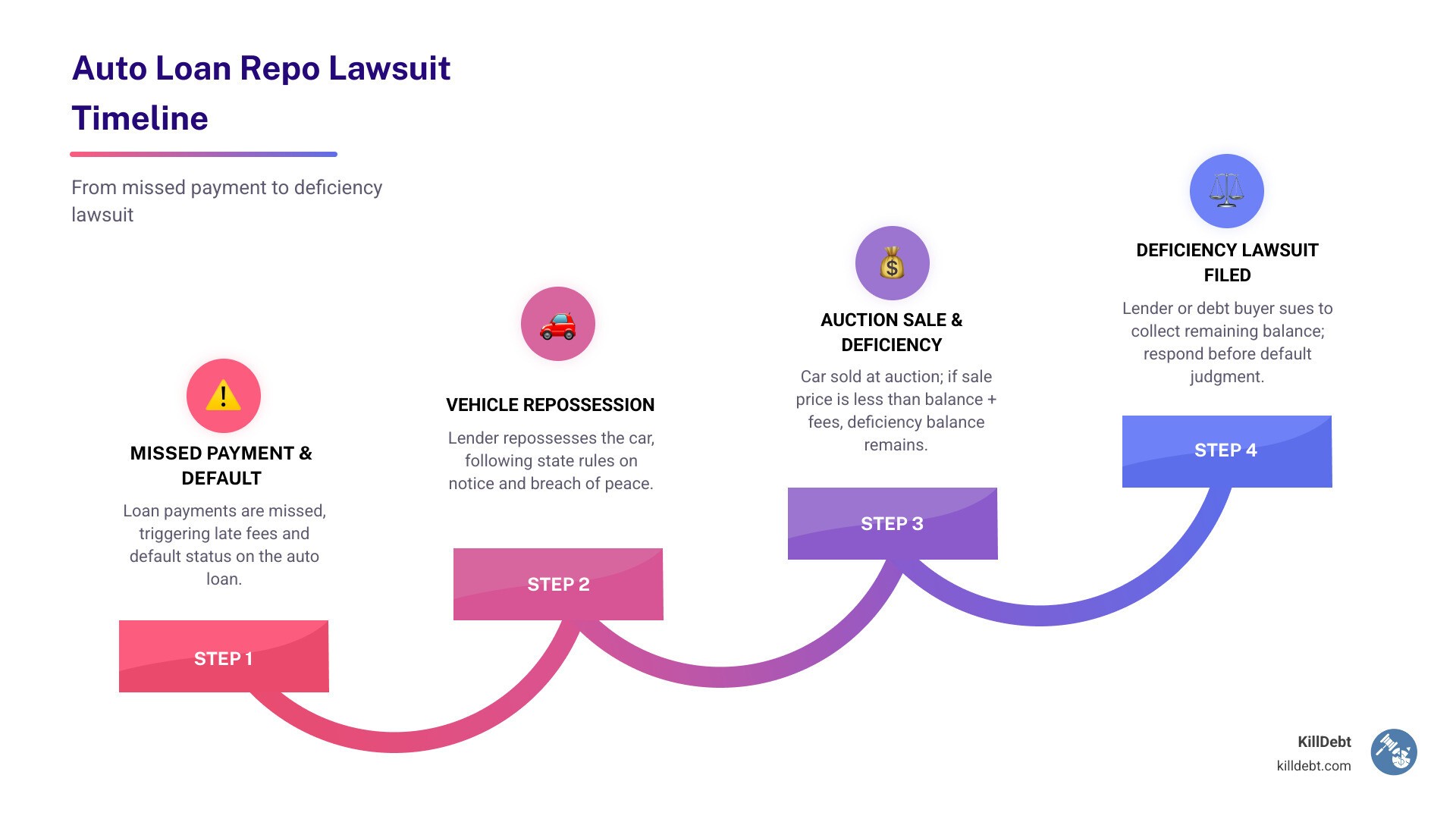

Quick Answer: Auto Loan Repo Lawsuit Basics

Your car was repossessed — the lender sold it, usually at auction.

The sale didn't cover what you owed — that gap is called a deficiency balance.

The lender (or a debt buyer) is now suing you to collect that remaining amount.

You have legal rights and defenses — improper notice, breach of peace, and unreasonable sale price can all be challenged.

You must respond to the lawsuit before the deadline or the court will issue a default judgment against you automatically.

Facing an auto loan repo lawsuit is one of the most stressful debt situations a person can find themselves in. One day your car is gone. A few weeks later, a summons arrives at your door demanding thousands of dollars — even though the lender already sold the vehicle.

This happens because most auto loans are secured debt. When you default, the lender can repossess and sell the car. But if the auction price doesn't cover your full loan balance, fees, and repossession costs, you still owe the difference. For example, if you owed $15,000 and the lender sold the car for $8,000, you could be on the hook for the remaining $7,000 — plus added fees.

What many people don't realize is that lenders must follow strict legal procedures during repossession and sale. If they didn't, you may have real defenses — even if you genuinely missed payments.

I'm Brian Parker, and for over 30 years I've fought creditors and collection law firms in courtrooms across the country, including cases involving auto loan repo lawsuits where lenders cut corners on notice, repossession conduct, and auction procedures. At KillDebt, we've distilled that experience into tools and guidance that help you fight back without paying attorney fees you can't afford.

Understanding the Auto Loan Repo Lawsuit and Deficiency Balances

When we talk about an auto loan repo lawsuit, we are usually talking about a "deficiency action." This is the legal process a lender uses to collect the "leftover" debt after your car has been taken and sold.

Think of your car loan as a two-part deal. Part one is the car itself, which acts as collateral. Part two is your personal promise to pay back the full amount of the loan. When the car is gone, that personal promise doesn't just evaporate. If the car sells for less than the loan balance, the lender views that remaining gap as an unsecured debt, much like a credit card.

In states like Florida and Michigan, the laws are very specific about how these balances are handled. According to Vehicle Repossession - FTC Consumer Advice, a deficiency is the difference between what you owe (plus legal and repossession costs) and what the lender gets from selling the car.

It is also important to know who is coming after you. Is it the original bank, or has the debt been sold to a "zombie" debt buyer? Understanding Who Is Suing Me Original Creditor Vs. Debt Buyer Explained is the first step in building your defense, as debt buyers often lack the original paperwork needed to win in court.

What Triggers an Auto Loan Repo Lawsuit?

The trigger for an auto loan repo lawsuit is almost always the "short sale" of the vehicle. Lenders don't usually want your car; they want the money. When they sell your car at a wholesale auction, it often goes for much less than its retail value.

If you owed $20,000 on a truck and it sells at a dealer auction for $12,000, you are suddenly looking at an $8,000 hole. Throw in $500 for the repo man, $300 for storage, and $1,000 in legal fees, and the lender is now filing a lawsuit for nearly $10,000.

Calculating the Deficiency Amount

Lenders are notorious for "fuzzy math" when calculating deficiency balances. We often see them pile on every imaginable fee to inflate the judgment amount.

Here is a typical breakdown of how that $7,000 or $10,000 balance is actually built:

Item | Amount |

|---|---|

Original Loan Balance | $18,000 |

Repossession Fee | $450 |

Storage & Cleaning Fees | $300 |

Auction/Sale Costs | $500 |

Total Debt Owed | $19,250 |

Minus Auction Sale Price | ($10,000) |

Final Deficiency Balance | $9,250 |

If you don't challenge these numbers, the court will assume they are correct. This is why it’s vital to understand Can a Debt Collection Agency Take You to Court and how to demand an itemized accounting of every penny they claim you owe.

Your Rights During and After Vehicle Repossession

Just because you missed a payment doesn't mean you've lost your civil rights. In fact, repossession agents have to follow strict rules. If they break them, the entire auto loan repo lawsuit could be tossed out of court.

One of the biggest rules is "Breach of the Peace." In Florida and Michigan, a repo agent can take your car from your driveway or a public street without a court order, but they cannot use force, they cannot break into a locked garage, and they cannot threaten you. If you are present and tell them to stop, continuing the repossession can be considered a breach of the peace.

According to How to Protect Yourself: Automobile Repossession | My Florida Legal, creditors in Florida have the right to seize the vehicle as soon as you default, but they must return any personal property found inside. If you're currently being hounded, our Debt Collector Suing Me Advice can help you navigate the immediate aftermath.

Recovering Personal Property Left in the Vehicle

We've seen cases where people lose their laptops, tools, and even medical equipment because it was in the car when the tow truck arrived. The lender has a security interest in the car, not your gym bag or your child's car seat.

In Michigan, lenders are generally required to hold your personal property for a specific period and notify you on how to retrieve it. You should send a written demand for your items immediately. If they refuse to return them or claim they "lost" them, you may have a counterclaim for conversion (the legal term for stealing your stuff).

For more details on your rights in these states, check out the Seizure of Property After Auto Loan Repossession FAQs - JustAnswer.

Notice Requirements and Commercially Reasonable Sales

This is where lenders mess up the most. After taking the car, the lender must send you a very specific legal notice. This notice tells you:

That the car was repossessed.

How much you need to pay to get it back (the right to redeem).

When and where the car will be sold.

Whether the sale will be a public auction or a private sale.

If they don't send this notice, or if the notice is missing required information, they may lose the right to sue you for a deficiency balance. Furthermore, the sale itself must be "commercially reasonable." If they sell a car worth $15,000 to the owner’s cousin for $500, that’s not reasonable, and we can fight that in court.

In Michigan, if you have already paid more than 60% of the loan, the lender is actually required to sell the vehicle within 90 days of repossession. Failure to do so can be a major defense in your Repossession Laws in Michigan - Upsolve.

Common Defenses to an Auto Loan Repo Lawsuit

When we look at an auto loan repo lawsuit, we aren't just looking for "excuses." We are looking for legal violations committed by the lender. These are called "affirmative defenses." If proven, they can reduce the amount you owe to zero or even lead to the lender paying you damages.

Our Auto Repossession Debt Suit Defense and Debt Lawsuit Defense Guide go into deep detail, but here are the heavy hitters:

Affirmative Defenses in an Auto Loan Repo Lawsuit

Improper Notice: As mentioned, if the lender failed to send the "Notice of Intent to Sell" or the "Explanation of Deficiency" according to state UCC (Uniform Commercial Code) rules, they might be barred from collecting a dime.

Breach of the Peace: If the repo man threatened you or damaged your property, this is a valid defense. In the case of Gary Gray Auffarth et al. v. Recovery Zone, Inc., plaintiffs sued because the car was lifted while someone was still inside. That is a massive legal "no-no."

Commercially Unreasonable Sale: If the lender sold the car for a ridiculously low price at a "closed" auction where only a few dealers were invited, you can challenge the sale price.

Military Protections: Under the Servicemembers Civil Relief Act (SCRA), active-duty military members have special protections against repossession without a court order.

Statute of Limitations for an Auto Loan Repo Lawsuit

Lenders don't have forever to sue you. In most states, the statute of limitations for a contract-based lawsuit is between four and six years from the date of your last payment or the date of the default.

If the lender waits too long to file the auto loan repo lawsuit, the debt becomes "time-barred." You still technically owe it, but they can't use the court system to force you to pay. Check the Debt Collection Lawsuit Timeline What Happens Next After Youre Served to see where you stand in the process.

How to Respond When You Are Sued for a Car Loan

The absolute worst thing you can do is ignore the summons. If you don't respond, the lender wins by default. A default judgment allows them to garnish your wages, freeze your bank accounts, and put liens on your property.

To stop this, you must file a written "Answer" with the court. This is a formal document where you respond to each paragraph in the lender's complaint. You don't have to prove your whole case yet; you just have to "deny" their claims and list your defenses to keep the case alive.

We provide a What to Do When Sued by a Debt Collector Complete First Steps Guide and a Fight Debt Collection Lawsuit Complete Guide to help you draft these documents without needing a $300-an-hour lawyer.

Challenging a Deficiency Judgment

Even if the lender has a strong case, you can still negotiate. Most lenders would rather take a lump sum of 30% or 50% now than spend years trying to garnish $50 a week from your paycheck.

If you've already been sued, check out Have You Been Sued by a Debt Collector for negotiation strategies. In extreme cases, where the deficiency is massive (like $20,000+), bankruptcy might be an option to wipe the debt entirely, but we always suggest trying to fight the lawsuit or settle first.

Avoiding a Lawsuit Through Voluntary Repossession

If you know you can't make the payments, you might consider "voluntary repossession" or surrendering the car.

Pros: You save on repossession fees (which can be $500+) and you avoid the "midnight tow truck" stress.

Cons: You still owe the deficiency balance, and it still hits your credit report as a repossession.

Don't fall for the Debt Collection Lawsuit Myths 7 Things That Wont Save You—giving the car back voluntarily does not mean the debt goes away. You should only do this if you get a written agreement from the lender stating they will waive the deficiency in exchange for the car.

Conclusion: Fight Back with KillDebt

Facing an auto loan repo lawsuit feels like being kicked while you're down. You've already lost your transportation, and now the bank wants to take your future wages. But you don't have to take it lying down.

At KillDebt, we believe the legal system shouldn't only work for people who can afford expensive attorneys. That's why we created a DIY legal defense system powered by ParkerGPT. This AI isn't just a chatbot; it’s trained on the real-world court strategies I’ve used for over 30 years. It analyzes your specific lawsuit documents, identifies the lender's mistakes, and generates court-ready responses for you.

We also just rolled out our Court Tester—an AI courtroom simulation. You can upload your actual filings and "practice" your arguments against an AI opposing counsel in front of an AI judge. It’s like having a private co-counsel whispering strategy in your ear, helping you prepare for the real thing.

Whether you are in Florida, Michigan, or anywhere else, the law provides you with protections. Don't let a default judgment ruin your financial future. Visit KillDebt.com today and let us help you stand up to the banks and win.

Frequently Asked Questions (FAQ)

Can a lender sue me if I voluntarily gave the car back?

Yes. Unless you have a signed "Accord and Satisfaction" or a written agreement stating that the surrender satisfies the entire debt, they can and will sue you for the deficiency balance.

What happens if the lender breached the peace during repo?

If the repo agent broke the law (e.g., entered your locked fence, used physical force), you may have a complete defense against the deficiency. In some cases, the lender may even owe you statutory damages under the UCC or the Fair Debt Collection Practices Act (FDCPA).

How long does a lender have to sue me for a deficiency in 2026?

As of May 2026, most states follow a statute of limitations between 4 and 6 years. However, this clock usually restarts if you make a partial payment or acknowledge the debt in writing. Always check your specific state's rules for written contracts.