What Happens When a Credit Card Lawsuit Lands in Your Mailbox

Knowing how to fight a credit card lawsuit could be the difference between keeping your paycheck and losing it to a garnishment order.

Here's the short answer if you need it fast:

Respond before the deadline — typically 14 to 30 days after being served, depending on your state.

File a written Answer with the court — deny allegations you can't verify, and raise affirmative defenses.

Challenge the plaintiff's standing — especially if a debt buyer is suing you; they must prove they own the debt.

Check the statute of limitations — if it has expired, the lawsuit may be thrown out entirely.

Consider settlement or bankruptcy — both can resolve the case before a judgment is entered against you.

The stakes are real. More than 70% of credit card debt lawsuits end in default judgments — simply because the person being sued never responded. That judgment can lead to wage garnishment, bank account levies, and liens on your property.

And the debt doesn't have to be enormous. The average U.S. cardholder carries around $8,000 in credit card debt — enough for a debt buyer to file suit and win automatically if you do nothing.

Here's what makes this especially frustrating: many of these lawsuits are filed by debt buyers — companies that purchased your account for as little as 2 to 5 cents on the dollar, often with incomplete records. They may not even be able to prove they own your debt. But if you don't show up, it doesn't matter.

I'm Brian Parker, and for over 30 years I've defended consumers against creditors, debt buyers, and collection law firms in courtrooms across the country — which means I've seen exactly how to fight a credit card lawsuit and win, even when the odds look stacked against you. I founded KillDebt to put those same strategies directly in your hands, without the $1,500+ attorney price tag.

Let's walk through exactly what to do.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

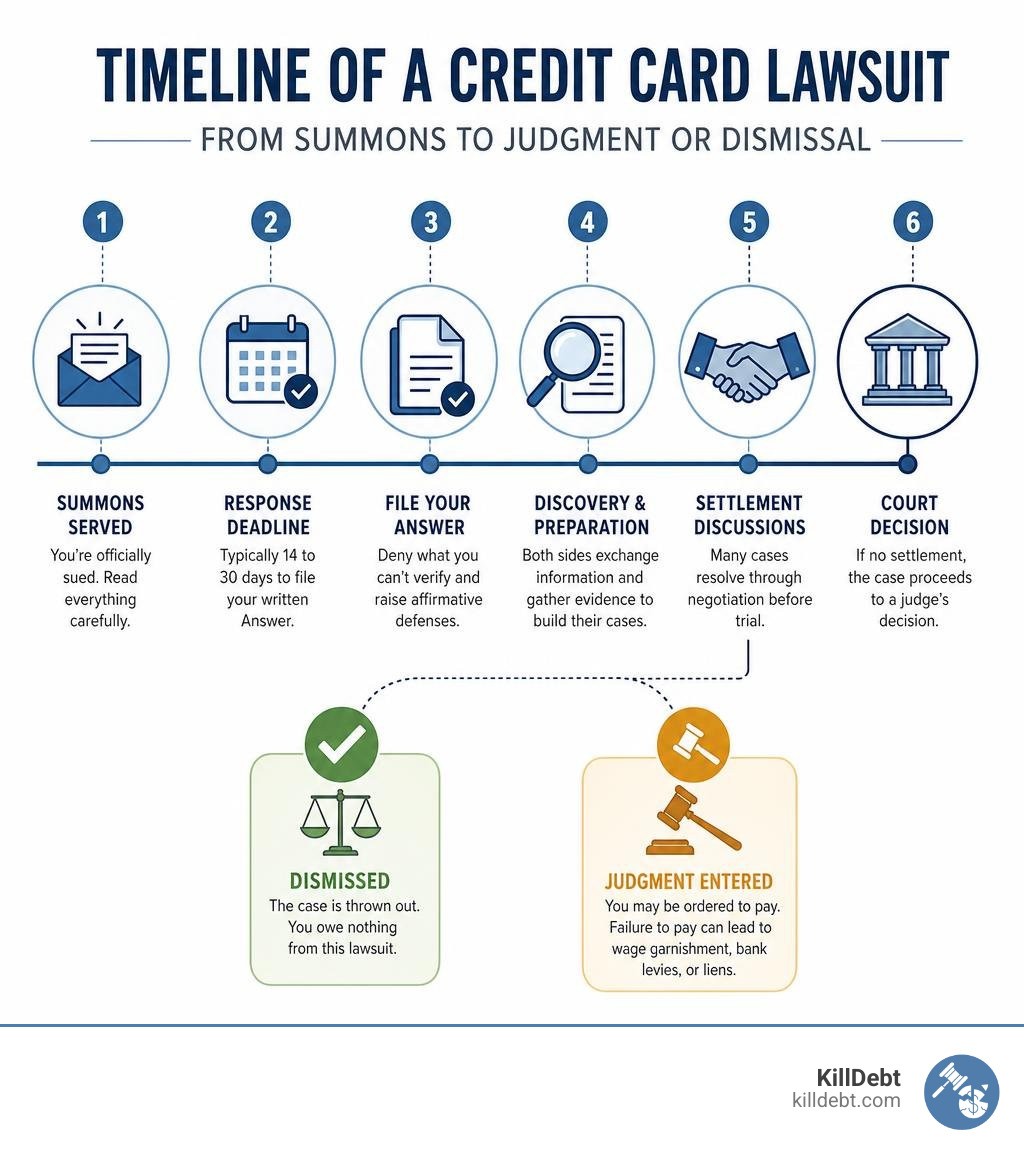

Sued for Debt: What to Do in the First 7 Days

When you are first served with a lawsuit, your adrenaline spikes. It is completely normal to feel a wave of panic, but the absolute worst thing you can do is stick those papers in a drawer and pretend they do not exist. Instead, take a deep breath. You have a window of time to act, and we are going to use every single day of it to build your defense.

During the first 7 days, your primary goal is information gathering and verification.

1. Read the Summons and Complaint Carefully

The lawsuit package consists of two main documents:

The Summons: This is the official court notice telling you that you are being sued. It contains critical details, including the name of the court, the case number, the names of the parties involved, and—most importantly—your deadline to respond.

The Complaint (or Petition): This is a list of numbered paragraphs detailing the allegations against you. It will state how much they claim you owe, the account number, and the legal theories (such as breach of contract or account stated) they are using to sue you.

To make sure you do not miss any critical first steps, check out our guide on Sued for a Debt: Exactly What to Do in the First 7 Days.

2. Identify Who is Suing You

Is the plaintiff your original credit card issuer (like Chase, Citibank, or Capital One), or is it a third-party debt buyer? Debt buyers purchase portfolios of defaulted accounts for pennies on the dollar and then file mass lawsuits to collect. Common debt buyers include:

Midland Credit Management (MCM) / Midland Funding

Portfolio Recovery Associates (PRA)

Jefferson Capital Systems

Cavalry SPV I

Knowing the difference between an original creditor and a debt buyer is the cornerstone of your defense strategy. Original creditors usually have direct access to your monthly statements and original signed agreements. Debt buyers, on the other hand, frequently buy these accounts as digital spreadsheets with little to no physical backup documentation.

3. Verify the Service of Process

Did you actually receive the lawsuit papers legally? "Service of process" is the formal delivery of the summons and complaint. If a process server left the papers with a random neighbor, or simply tossed them on your porch without speaking to you, the service may be legally defective. While improper service can sometimes buy you time to get the case dismissed, it rarely kills the lawsuit permanently because the creditor can simply serve you again. Still, it is a vital detail to note.

For a comprehensive overview of your initial options, you can also read the FTC's advice on What To Do if a Debt Collector Sues You or review our checklist on What to Do When Sued by a Debt Collector.

How to Fight a Credit Card Lawsuit: Step-by-Step

Once you have analyzed the summons, you must prepare your formal response, known as an Answer. This is a legal document where you respond directly to each numbered allegation in the plaintiff's complaint.

If you ignore the summons, the court will enter a default judgment against you. A default judgment is an automatic win for the creditor. Once they have this judgment, they can legally:

Garnish your wages: Under federal law (15 U.S.C. § 1673), wage garnishment is generally capped at 25% of your disposable earnings. However, state laws vary. For example, in Florida, head-of-household wage exemptions can protect your paycheck entirely if you provide more than half the support for a dependent. Michigan allows wage garnishment up to 25% of your disposable income or the amount by which your weekly income exceeds 30 times the federal minimum wage.

Levy your bank accounts: The creditor can freeze your bank accounts and seize the funds to satisfy the debt.

Place liens on your property: They can attach a lien to your home, meaning you cannot sell or refinance without paying them off first.

To prevent this nightmare scenario, you must learn How to Answer a Credit Card Lawsuit and follow the proper legal channels. For a deep dive into the drafting process, read our breakdown on How to Write an Answer to a Credit Card Lawsuit.

Let's break the process down into two manageable steps.

How to Fight a Credit Card Lawsuit Step 1: Draft Your Answer

Your Answer must follow specific formatting rules (often referred to as Rule 10 formatting). This includes a "caption" at the top of the page showing the court name, the parties' names, and the case/file number.

Below the caption, you will address each numbered paragraph of the complaint using one of three standard responses:

Admit: You agree that the statement is 100% true (e.g., "The Defendant resides in Oakland County, Michigan"). Only admit things that are indisputable.

Deny: You dispute the statement. In debt collection defense, denial is your best friend. Denying an allegation does not mean you are lying; it simply means you are demanding that the plaintiff prove their claim. If you do not recognize the exact debt balance or the interest rates they are claiming, deny it.

Deny due to lack of knowledge: You do not have enough information to know if the statement is true (e.g., if a debt buyer claims they purchased your account on a specific date in 2024, you have no way of knowing their internal business transactions).

After responding to the individual paragraphs, you must list your affirmative defenses—the legal reasons why the plaintiff should not win even if some of their statements are true. (We will cover the best defenses in detail below).

To see what this looks like in practice, you can reference our Sample Answer to a Credit Card Lawsuit.

How to Fight a Credit Card Lawsuit Step 2: File and Serve Your Response

Once your Answer is drafted and signed, you must file it with the court clerk and serve a copy on the plaintiff's attorney.

Filing Deadlines: Do not miss your deadline! In Florida, you have exactly 20 days from the date you were served to file your Answer. In Michigan, you have 21 days if you were served in person, or 28 days if you were served by mail or outside the state.

Filing with the Court: You can often file your Answer electronically through the court's online portal or by physically visiting the courthouse clerk. Filing an Answer is free of charge in small claims and county courts.

Serving the Plaintiff: You must send a copy of your Answer to the plaintiff’s attorney. We highly recommend using Certified Mail with Return Receipt Requested so you have undeniable proof of service.

For more details on small claims court processes, you can review the guide on About Small Claims Collection Lawsuits - The Florida Bar or review Michigan-specific options at What Can You Do In Michigan If You Are Sued By A Credit Card ... .

The 4 Best Legal Defenses Against a Credit Card Debt Lawsuit

When you file your Answer, you must include your "affirmative defenses." If you do not raise these defenses in your initial Answer, the court may consider them waived forever.

The burden of proof rests entirely on the plaintiff. They must prove that you owe the debt, that they have the legal right to collect it, and that the amount they are claiming is accurate to the penny.

The following table compares the typical defense strategies depending on whether you are being sued by the original creditor or a third-party debt buyer:

Defense Strategy | Sued by Original Creditor | Sued by Third-Party Debt Buyer |

|---|---|---|

Statute of Limitations | Highly effective if the account has been inactive for years. | Highly effective; debt buyers frequently buy very old accounts. |

Lack of Standing / Chain of Title | Weak; they are the original party to the contract. | Extremely Strong; they must prove ownership of your specific account. |

Inaccurate Accounting / Fees | Moderate; challenge interest calculations and late fees. | Strong; debt buyers rarely have complete statement histories. |

FDCPA Counterclaims | Generally N/A (FDCPA applies to third-party collectors). | Strong; can be used as leverage if they used deceptive tactics. |

For a broader look at defensive legal strategies, check out our Debt Lawsuit Defense Guide and explore local consumer advocacy insights at Credit Card Defense - Florin Legal, P.A. .

Defense 1: The Statute of Limitations Has Expired

The statute of limitations is the legal time limit a creditor has to file a lawsuit against you. Once this period passes, the debt is considered "time-barred," and they can no longer legally sue you to collect.

Florida: The statute of limitations for credit card debt (which is typically treated as an open-ended account or a written contract) is 5 years.

Michigan: The statute of limitations for credit card debt is 6 years.

The clock typically starts ticking from the date of your last payment or the date you first defaulted on the account.

Let’s look at a June 2026 timeline example: If you live in Florida and your last credit card payment was made in March 2021, the 5-year statute of limitations expired in March 2026. If a debt buyer sues you in June 2026, you can raise the expired statute of limitations as an affirmative defense, and the judge should dismiss the case.

Warning: Be incredibly careful. Making even a tiny partial payment or formally acknowledging the debt in writing can "restart" the statute of limitations clock in many jurisdictions!

Defense 2: Lack of Standing and Chain of Title

If a third-party debt buyer is suing you, they must prove they have the legal right to do so. This is known as standing. To establish standing, they must produce a clean, unbroken "chain of title" showing the transfer of your specific account from the original creditor to any intermediary buyers, and finally to the plaintiff.

Often, debt buyers only attach a generic "Bill of Sale" to their lawsuit. This Bill of Sale usually says something like: "Originating Bank hereby sells a portfolio of 10,000 accounts to Debt Buyer LLC."

Unless they can produce the specific, redacted "Schedule A" or data tape printout showing your exact name, account number, and balance, they have not proven they own your debt. If they cannot produce these records during the discovery phase of the lawsuit, their case falls apart.

For a detailed explanation of this dynamic, read Who is Suing Me: Original Creditor vs. Debt Buyer and learn about local defense tactics in Debt Collection Lawsuits: How to Fight Back and Win in Florida .

Defense 3: Incorrect Debt Amount or Mistaken Identity

Do not assume the plaintiff's math is correct. Debt collectors frequently tack on unauthorized interest, convenience fees, and attorney costs that were never agreed to in your original cardholder agreement.

Additionally, mistaken identity is incredibly common in the debt buying industry. Clerical errors, similar names, or identity theft can result in a debt collector suing the completely wrong person for a debt they never incurred. If you do not recognize the account, demand that they produce the original signed credit agreement and full monthly statements to prove you are the responsible party.

Defense 4: FDCPA Violations as a Counterclaim

Under the federal Fair Debt Collection Practices Act (FDCPA), third-party debt collectors are strictly prohibited from using abusive, unfair, or deceptive practices. If a debt collector has violated your rights, you can file a counterclaim against them. Common violations include:

Threatening legal actions they do not actually intend to take (or cannot legally take).

Calling you before 8:00 AM or after 9:00 PM.

Contacting your employers, family members, or neighbors about your debt.

Failing to send a written debt validation notice within 5 days of their initial contact.

If you sue a debt collector for FDCPA violations, you can recover up to $1,000 in statutory damages, plus actual damages and your attorney fees. This provides massive leverage when negotiating a dismissal of their lawsuit. You have a strict one-year limit from the date of the violation to file an FDCPA claim.

Resolving the Lawsuit: Settlement vs. Bankruptcy

If you do not want to fight the case all the way to a trial, you have other viable paths to resolve the litigation.

1. Debt Settlement

Most debt buyers purchase portfolios for 2 to 5 cents on the dollar, which means they have a massive profit margin. Because of this, they are highly motivated to settle. You can often negotiate a lump-sum settlement for 30% to 60% of the total balance claimed.

If you choose to settle, follow these golden rules:

Get it in writing first: Never send a single penny until you have a signed settlement agreement in your hands.

Require dismissal with prejudice: The agreement must state that upon receipt of payment, the lawsuit will be dismissed "with prejudice." This means they can never sue you for this specific debt again.

Avoid verbal agreements: Phone representatives will promise the world, but if it isn't in writing, it doesn't exist.

For a comprehensive strategic guide, check out our Fight Debt Collection Lawsuit Complete Guide or read Michigan's court navigation resources at Going to Court to Defend a Debt Collection Case | Michigan Legal ... .

2. Bankruptcy

If you are facing multiple lawsuits, overwhelming medical bills, or credit card balances you have no hope of paying, bankruptcy might be the right path.

Filing for bankruptcy triggers an automatic stay. This is a powerful federal injunction that immediately halts all collection activities, including active lawsuits, pending court dates, bank levies, and wage garnishments. A Chapter 7 bankruptcy can completely discharge (wipe out) your credit card debt, giving you a totally clean financial slate.

Conclusion: Take Control of Your Debt Defense

You do not need to spend thousands of dollars on a defense attorney to protect your hard-earned money. Defending yourself pro se (without a lawyer) is entirely possible when you have the right tools.

At KillDebt, we have built a DIY legal defense system designed to level the playing field. Powered by ParkerGPT—an AI trained specifically on consumer debt law and real-world court strategies developed over 30+ years by attorney Brian Parker—our system analyzes your actual lawsuit documents, uncovers hidden weaknesses, and generates professional, court-ready Responses.

And if you want to practice before stepping foot in a real courtroom, we just rolled out Court Tester. It is an AI courtroom simulation built on your actual case. You upload your real filings, and within minutes, you are arguing your motion in front of an AI judge, facing off against AI opposing counsel, with a private AI co-counsel whispering winning strategies directly to you.

Do not let a default judgment ruin your credit and drain your bank account. Check out our KillDebt Pricing page today and discover how easy it is to fight back and win.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments

Frequently Asked Questions (FAQ)

What happens if I ignore a credit card lawsuit?

If you ignore the lawsuit, the plaintiff will win a default judgment against you. This allows them to freeze your bank accounts, garnish up to 25% of your paycheck, and place liens on your personal property or home. To bust common myths about ignoring these cases, read Debt Collection Lawsuit Myths.

How do I check if the statute of limitations has expired on my debt?

Look through your personal financial records or pull your free credit reports to find the date of your "last payment" or "date of first delinquency." Compare this date to your state's limits (5 years in Florida, 6 years in Michigan). If the time elapsed is greater than your state's limit, the debt is time-barred.

Can a debt collection agency take you to court?

Yes. If a debt collection agency or debt buyer has purchased the legal rights to your debt, they have the standing to sue you in civil court. However, they must still prove the entire chain of custody to win if you challenge them. Learn more about their legal limits in Can a Debt Collection Agency Take You to Court.