What Is the Debt Validation Dispute Process (And Why It Can Stop Collectors Cold)

The debt validation dispute process is one of the most powerful — and most overlooked — tools in federal consumer protection law. Here is how it works at a glance:

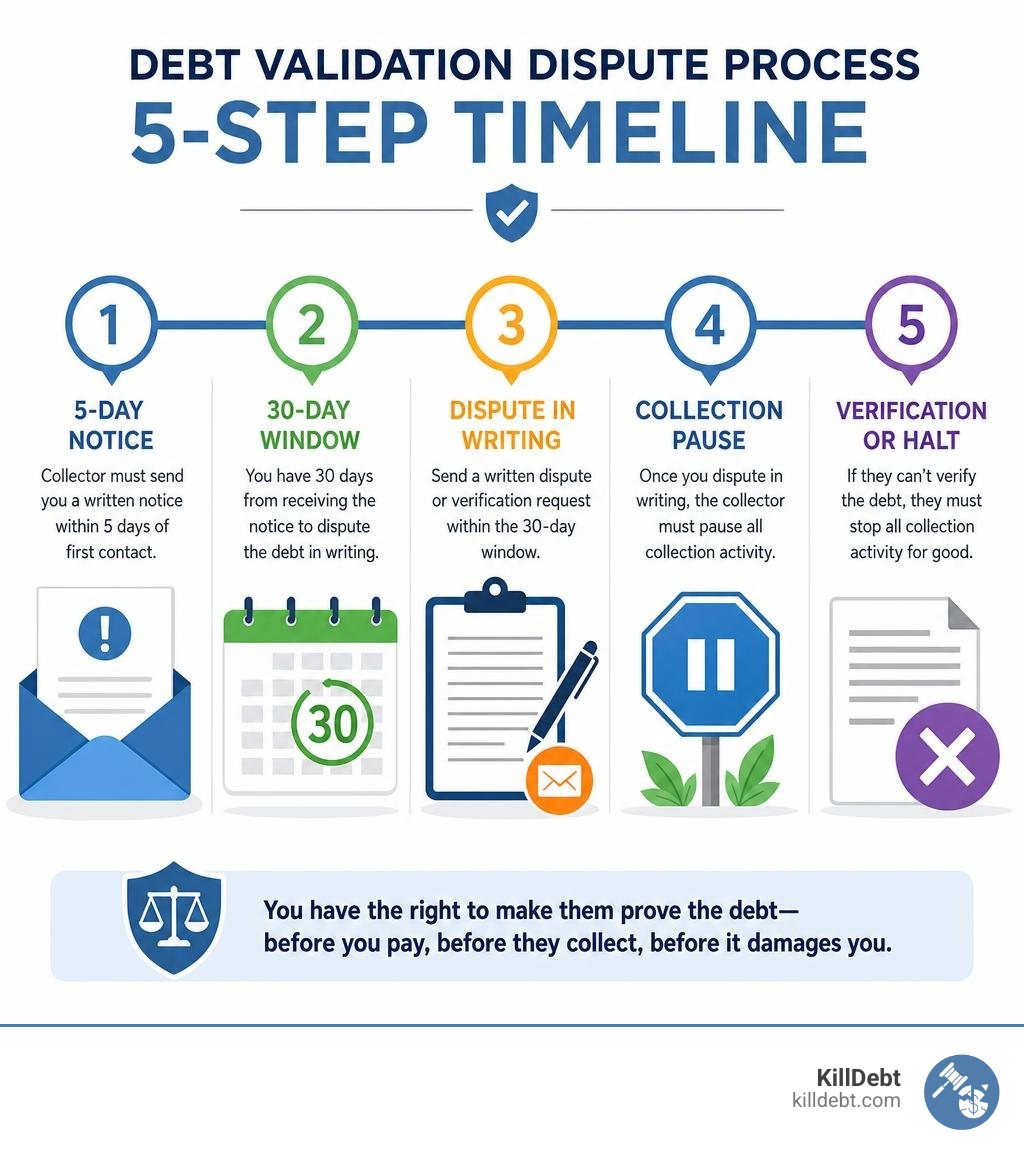

The debt validation dispute process in 4 steps:

Receive the validation notice — the debt collector must send you a written notice within 5 days of first contact, listing the debt amount, creditor name, and your dispute rights.

Send a written dispute or verification request — you have 30 days from receiving that notice to dispute the debt in writing.

Collection must stop — once you dispute in writing, the collector must pause all collection activity until they provide written verification of the debt.

Review what they send back — if they cannot verify the debt, they must stop calling, writing, reporting to credit bureaus, and suing.

Getting a letter or call from a debt collector is stressful. Most people either panic and pay, or panic and ignore it. Both are mistakes.

Here is the thing: debt collection is a $20 billion industry where debts are bought and sold constantly — often for as little as four cents on the dollar. That means the company contacting you may have never seen your original contract. They may have the wrong amount. The wrong person. A debt you already paid.

You have a federal right to make them prove it before you do anything else.

And if you have already received a summons or a court deadline, that urgency is even greater. Acting fast — and acting correctly — can be the difference between a default judgment and a real defense.

I'm Brian Parker, and for over 30 years I've been in courtrooms fighting debt buyers, collection agencies, and collection law firms — and I've seen the debt validation dispute process used to stop collectors in their tracks, even when the odds looked terrible. I built KillDebt to give you the same tools and strategies I've used to protect thousands of consumers, without the $1,500+ attorney bill.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

Understanding Your Rights: Validation Notice vs. Verification Request

To successfully navigate the debt validation dispute process, you must understand the difference between two critical documents that sound almost identical but serve completely opposite purposes.

Many consumers confuse the "validation notice" with a "verification request." Think of them as two sides of the same legal coin under the Fair Debt Collection Practices Act (FDCPA).

Feature | Validation Notice | Verification Request (Dispute) |

|---|---|---|

Who Sends It? | The debt collector sends it to you. | You send it to the debt collector. |

Why Is It Sent? | Required by federal law to disclose debt details. | To dispute the debt and force the collector to prove it. |

The Deadline | Within 5 days of their initial communication. | Within 30 days of your receipt of their notice. |

Legal Basis | FDCPA Section 809(a) | FDCPA Section 809(b) |

Impact | Triggers your 30-day clock to dispute. | Forces an immediate pause on all collection activity. |

When a third-party debt buyer purchases a portfolio of past-due accounts for pennies on the dollar, they rarely receive the actual signed contracts, comprehensive payment histories, or statements. They usually buy nothing more than a giant electronic spreadsheet filled with basic names, addresses, and dollar figures.

By initiating the dispute process, you are testing whether they actually have the legal right and documentation to collect that money. If you want to dive deeper into why these letters are your best shield, read our detailed guide on Debt Validation Letters: Your First Line of Defense Against Collectors.

What is a Debt Validation Notice?

Under federal law, a debt collector cannot just call you out of the blue and demand cash without putting the details in writing. Within five days of their first contact with you, they must send you a formal written document known as a Validation Notice.

According to the Consumer Financial Protection Bureau (CFPB), this notice must contain:

The exact amount of the alleged debt.

The name of the original creditor to whom the debt is owed.

An itemization of the debt (including interest, fees, payments, and credits).

A clear statement informing you that you have a 30-day window to dispute the debt.

A statement that if you do not dispute it, the collector will assume the debt is valid.

A statement that if you write to dispute the debt within 30 days, the collector must mail you verification of the debt.

If they fail to send this notice within five days of first contact, they are in direct violation of federal law.

Why the Debt Validation Dispute Process is Your Best Defense

The beauty of the debt validation dispute process is that it flips the script. It instantly shifts the burden of proof off your shoulders and places it squarely on the debt collector.

When you send a timely written dispute, the collector is legally required to halt all collection efforts. This means:

No more harassing phone calls (which are already strictly limited under Regulation F to no more than seven calls within a seven-day period).

No more collection letters arriving in your mailbox.

They cannot report the debt to credit bureaus, or if they have already reported it, they must mark it as "disputed." Reporting a disputed debt as undisputed is a major violation of the Fair Credit Reporting Act (FCRA).

They cannot file a lawsuit against you during this validation pause.

For anyone facing urgent threats of wage garnishment or a collection lawsuit, this legal "time-out" is incredibly valuable. It gives you the breathing room needed to assess the situation, gather your records, and build a defense.

Step-by-Step Guide to the Debt Validation Dispute Process

Now that you know your rights, let's look at how to execute this process step-by-step. To make this work, you must be precise, keep immaculate records, and use certified mail. If you want a quick, comprehensive master template, you can read our breakdown of the Letter of Debt Validation.

Step 1: Review the Collector's Notice for Errors

Do not take the collector's word for anything. Treat their validation notice like a rough draft that is full of mistakes. Grab your own financial records and compare them. Look closely for these common errors:

Incorrect Amounts: Are they tacking on illegal interest, mysterious "processing fees," or collection costs that were never authorized in your original contract?

Identity Theft/Wrong Person: Is this debt actually yours, or do you share a similar name with the actual debtor? Debt buyers frequently mix up consumer files.

Debts Already Paid: Did you settle this debt years ago?

Time-Barred Debt (Statute of Limitations): Every state has a legal time limit for how long a creditor can sue you to collect a debt.

In Florida, the statute of limitations for most written contracts and credit cards is 5 years.

In Michigan, the statute of limitations for breach of contract and debt collection is 6 years.

Note: If the debt is past these state-specific deadlines, it is "time-barred." While collectors in some areas can still write or call you to ask for payment, they cannot legally sue you. If they threaten a lawsuit on a time-barred debt, they are violating the FDCPA. Be extremely careful: making even a tiny partial payment on a time-barred debt can "reset" the clock, starting the statute of limitations all over again!

Step 2: Draft Your Dispute Letter

Your letter does not need to be a 10-page legal brief. In fact, keeping it simple and direct is highly effective. You do not want to volunteer extra personal or financial information that the collector can later use against you.

Your letter should state that you are exercising your rights under FDCPA Section 809(b) to dispute the debt and request verification. Specifically, ask them to provide:

Proof that you owe the debt (such as a copy of the original contract or agreement).

An itemized breakdown of the alleged balance, showing how they calculated the interest and fees.

Documentation proving they have the legal license and authority to collect debts in your state (especially important in Florida and Michigan, which have specific state regulatory licensing laws).

The name and address of the original creditor.

Avoid writing a long story about why you fell behind on your bills. Simply state: "I am writing to formally dispute the validity of this alleged debt and request verification of the same." To save time, you can download a pre-formatted, legally sound Debt Validation Letter Template.

Step 3: Initiating the Debt Validation Dispute Process in Writing

Once your letter is ready, do not just drop it in a standard mailbox with a regular stamp. If the collector claims they "never received it," your 30-day dispute window will close, and you will lose your strongest legal leverage.

You must send your letter via USPS Certified Mail with Return Receipt Requested (the physical green card or the electronic return receipt).

This gives you:

A unique tracking number to prove exactly when the letter was mailed.

Official proof of delivery showing the date and the signature of the person at the collection agency who accepted it.

A legally binding paper trail that you can present to a judge if the collector violates the pause and attempts to sue you or report the debt.

Keep a physical folder containing a copy of the exact letter you sent, the certified mail receipt, and the signed green card once it arrives back in your mailbox. If you want to see what a completed version looks like, check out this Example Debt Validation Letter.

What Happens After You Dispute?

Once the debt collector receives your certified letter, the ball is in their court. Under federal regulation § 1006.38 Disputes and requests for original-creditor information. | Consumer Financial Protection Bureau , they must immediately cease all collection activities.

They cannot call you, they cannot write to you, and they cannot report the debt to credit bureaus. If they have already reported the debt, they must notify the credit reporting agencies that the account is actively disputed. If you suspect they are ignoring your letter, you should send a Dispute Invalid Debt Notice to protect your credit profile.

What if you send multiple letters? Under CFPB rules, if a dispute is "duplicative" (meaning you send the exact same dispute repeatedly without providing any new, material information), the collector can refuse to respond, but they must notify you of their reasoning. Always include new evidence (like a bank statement or a settled receipt) if you are disputing a second time.

Let's look at the two potential paths your dispute will take.

If the Collector Validates the Debt

If the collector manages to dig up documentation and sends it to you, do not panic. First, analyze what they sent.

Under current federal court rulings, the legal standard for "verification" is surprisingly low. The collector does not necessarily have to provide a perfectly preserved original contract signed in ink. In many jurisdictions, they only need to provide written confirmation from the original creditor that the amount matches what is in their files.

However, if they do send verification, review it closely:

Does the payment history match your records?

Are the interest rates and fees accurate to the original contract?

Is the debt past the statute of limitations?

If the debt is verified and accurate, you have several options: you can negotiate a settlement for a fraction of the total balance, set up a payment plan, or prepare a formal court defense if they decide to file a lawsuit. If you are already facing a court summons, you must file a formal written "Answer" with the court within your state's deadline (usually 20 days in Florida and 21 days in Michigan) to avoid losing by default.

If the Collector Fails to Validate

This is where the magic happens. Because debt buyers buy portfolios so cheaply, they often find that retrieving original documents from years ago is simply too expensive or entirely impossible.

If they cannot validate the debt, they have two choices:

They can ignore your letter and simply stop trying to collect from you.

They might quietly package your debt up and sell it to another debt buyer (which starts the loop over again, though the new collector must also respect your dispute rights).

If they fail to validate the debt but continue to call you, write to you, or report the unverified debt to credit bureaus, they are violating the FDCPA. Under federal law, you can sue a non-compliant debt collector for up to $1,000 in statutory damages, plus your actual damages and attorney's fees.

Conclusion

Navigating the debt validation dispute process can feel overwhelming, but it is your absolute best tool for leveling the playing field against aggressive collection agencies. Debt collectors are businesses looking for the easiest path to a payday. When you stand up, demand proof, and assert your federal rights, you make collecting from you highly unprofitable.

If you are currently facing a collection letter, a threatening phone call, or a terrifying court summons in Florida or Michigan, you do not have to fight this battle alone — and you do not need to spend thousands of dollars on a defense attorney.

At KillDebt, we provide a DIY legal defense system powered by ParkerGPT — an AI trained specifically on consumer debt law and real courtroom strategies developed over 30+ years by veteran consumer defense attorney Brian Parker.

Unlike generic AI tools, KillDebt analyzes your actual lawsuit filings, identifies the collector's legal weaknesses, and generates court-ready responses with simple, step-by-step instructions.

And if you want to practice your defense before stepping foot in front of a judge, our brand-new Court Tester tool allows you to run a courtroom simulation. You can upload your actual filings and, within minutes, argue your motion in front of an AI judge, face off against AI opposing counsel, and receive real-time, private strategy whispers from an AI co-counsel.

Take control of your financial future today. Use KillDebt to build your defense and stop collectors in their tracks.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

Frequently Asked Questions (FAQ)

Can I still request validation after the 30-day window has passed?

Yes, you can still send a validation or dispute letter after the initial 30 days have expired. However, you lose your automatic legal protections. If you dispute within the first 30 days, the collector must stop collection efforts until they verify the debt. If you send the letter on day 31 or later, the collector is not legally required to stop calling, writing, or reporting to credit bureaus while they look for the documentation. However, sending a late letter is still highly beneficial. If the collector cannot find the documentation, they still cannot legally win a lawsuit against you, and exposing their lack of records early on can prevent them from suing in the first place.

What should I do if a debt collector sues me?

If you receive a court summons and complaint, the debt validation dispute process alone will not save you. You cannot simply send a validation letter to the collector and assume the lawsuit will go away. Once a lawsuit is filed, you are on the court's calendar. You must file a formal written "Answer" to the summons within the strict legal deadline: • Florida: 20 days from the date you were served. • Michigan: 21 days from the date you were served (or 28 days if you were served by mail or outside the state). If you miss this deadline, the court will issue a "default judgment" against you. This gives the collector the legal right to garnish your bank accounts or garnish your wages.

How do I spot and protect myself from debt collection scams?

The debt collection space is filled with scammers who buy leaked personal data and try to scare consumers into paying debts they do not even owe. Protect yourself with these rules: • Never give out sensitive financial info: Do not give your bank account, credit card, or Social Security number to a collector who called you out of the blue. • Demand written notice: If a collector refuses to send you a physical validation notice in the mail or via email, hang up. Legitimate collectors are required by law to provide this. • Check for scam indicators: Scammers often use threats of immediate arrest, police action, or physical harm. Legitimate collectors cannot threaten to have you arrested. • Submit complaints: If you are being hounded by a fake or abusive collector, file an official complaint with the CFPB and your state’s Attorney General.