What to Do When You Receive an Invalid Debt Notice

If you need to dispute invalid debt notice you received from a collector, here's the short version:

Send a written dispute letter to the debt collector

Do it within 30 days of receiving their notice

Send it via certified mail with return receipt requested

Request debt validation — demand they prove you owe the debt

Keep copies of everything

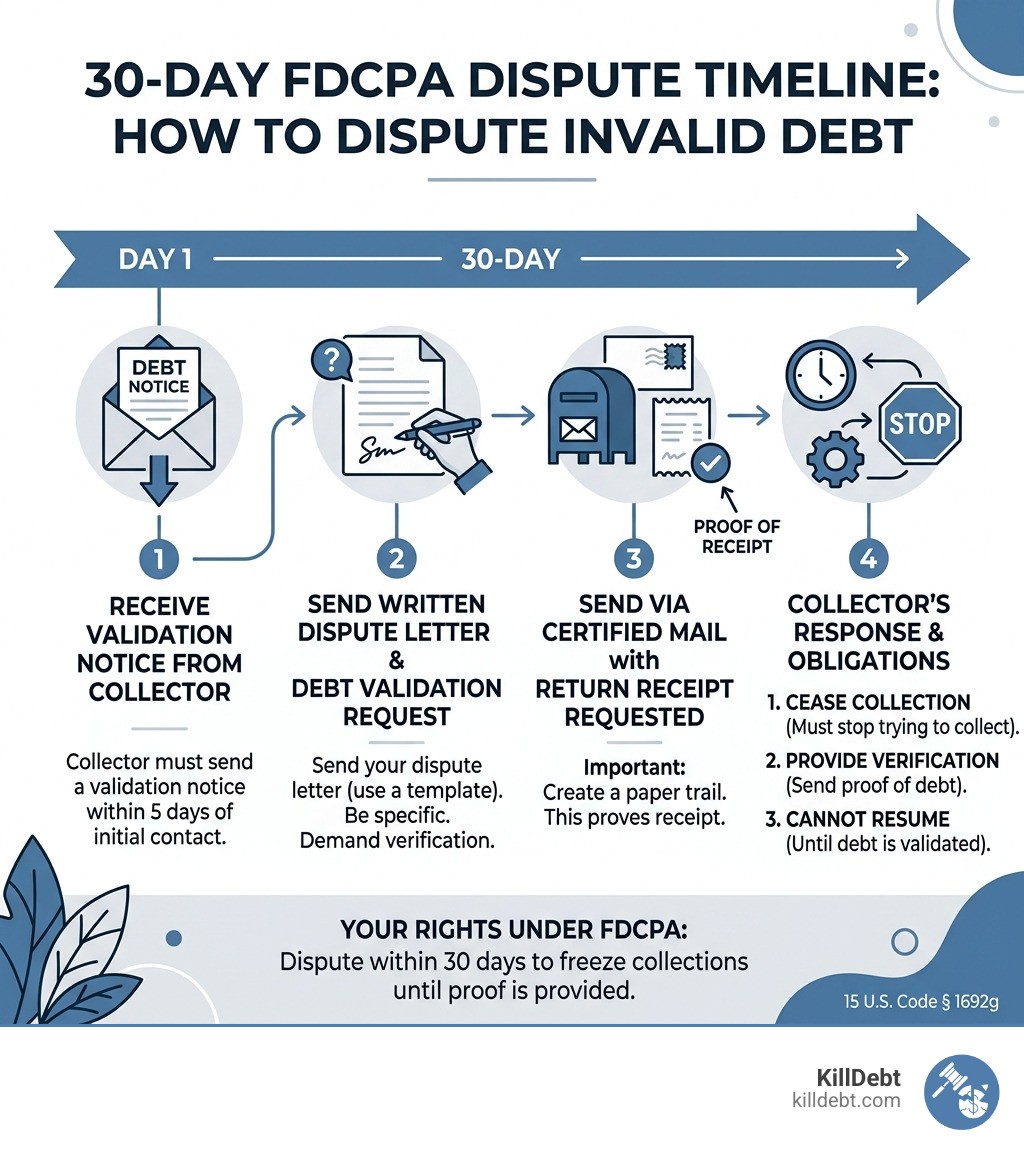

Once they receive your dispute, they must stop collection until they verify the debt. That's federal law.

Getting a debt collection letter in the mail is stressful. Getting one for a debt you don't recognize — or already paid — is even worse.

You might feel pressured to pay just to make it stop. Don't.

According to FTC data, 49% of complaints about debt collectors involve debts the consumer didn't actually owe. Collectors sometimes pursue the wrong person, inflate amounts, or chase debts that were already settled. It happens more than you'd think — because collection agencies often buy thousands of old debts cheaply, sometimes with incomplete or inaccurate records.

The good news? Federal law gives you powerful tools to fight back. The Fair Debt Collection Practices Act (FDCPA) requires collectors to verify a debt before they can keep pursuing you — as long as you know how to ask.

This guide walks you through exactly what to do, step by step.

Understanding Your Rights Under the FDCPA

When a debt collector reaches out, they aren't just making a friendly suggestion that you pay them. They are invoking a legal process, but that process has strict guardrails. The primary "shield" for consumers in the United States is the Fair Debt Collection Practices Act (FDCPA).

Specifically, 15 U.S. Code § 1692g - Validation of debts is your best friend. This section of the law mandates that within five days of their initial contact with you, a debt collector must send you a "validation notice."

This notice isn't just a bill; it must include:

The exact amount of the debt.

The name of the creditor to whom the debt is owed.

A statement that unless you dispute the validity of the debt within 30 days, the debt will be assumed valid by the collector.

A statement that if you notify them in writing within that 30-day period that the debt is disputed, they will obtain verification of the debt.

If they don't include these things, they are already breaking the law. We like to think of the FDCPA as the rulebook for a game where the collectors often try to cheat. Knowing the rules is the only way to win.

The Importance of the 30-Day Window

In debt collection, time is of the essence. The "validation period" is a 30-day window that starts from the moment you receive that initial validation notice.

Why is this window so critical? If you send your dispute invalid debt notice within these 30 days, the law forces the collector to freeze. They must cease all collection activities—no calls, no letters, no reporting to credit bureaus—until they mail you the verification of the debt.

If you wait until day 31, you can still dispute the debt, but you lose that automatic "pause button." The collector can keep hounding you while they look for the paperwork. Think of the 30-day window as a legal "time-out" that you have the power to call.

Federal vs. State Protections

While the FDCPA is a federal law that covers everyone in the U.S., states like Florida and Michigan have their own additional layers of protection.

For instance, Regulation F (12 CFR Part 1006) recently updated federal rules to clarify how collectors can communicate with you via email and text, and it introduced a "Model Validation Notice" that collectors are encouraged to use. This form includes a handy "tear-off" section to make disputing easier.

In Michigan, collectors are subject to the Michigan Occupational Code, which prohibits many of the same harassing behaviors as the FDCPA but provides local avenues for complaints. In Florida, the Florida Consumer Collection Practices Act (FCCPA) is even more robust than federal law in some areas, offering protections against "out of state" collectors who try to skirt the rules.

At KillDebt, we focus on these specific jurisdictions because we know the local court strategies that work. Whether you are in the Panhandle or the Upper Peninsula, the core strategy remains the same: force the collector to prove their claim before you give them a dime.

How to Dispute Invalid Debt Notice Step-by-Step

Disputing a debt isn't just about saying "I don't owe this" over the phone. In fact, never dispute a debt solely over the phone. Oral disputes don't trigger the same legal requirements for the collector to stop their activities. You need a paper trail.

Step 1: Review the Notice for Errors

Don't just look at the total. Look at the account number, the original creditor's name, and any fees they've tacked on. Collectors often buy "junk debt" for pennies on the dollar (sometimes as low as 4% of the value), and the data they receive is often riddled with errors.

Step 2: Draft Your Dispute Letter

You don't need to write a novel. You just need to state clearly that you are disputing the debt and requesting validation. We recommend using a formal tone. If you're feeling overwhelmed, our Debt Validation Letters: Your First Line of Defense Against Collectors guide provides a deeper dive into the "why" behind this strategy.

Step 3: Send via Certified Mail

This is non-negotiable. You need proof that they received your letter within the 30-day window. Use USPS Certified Mail with a Return Receipt Requested. When that green card comes back to you in the mail with a signature, staple it to your copy of the letter. This is your "get out of jail free" card if they try to claim they never heard from you.

Drafting Your Dispute Invalid Debt Notice Letter

When you sit down to write your dispute invalid debt notice, keep it simple but firm. You aren't asking for a favor; you are exercising a right.

Your letter should include:

Your full name and current address.

The collector's name and address.

The account number associated with the debt.

A clear statement: "I am writing to dispute the validity of this debt."

A request for the name and address of the original creditor (if different from the current one).

A demand for "debt validation" including the original contract or itemized statement of charges.

A request to cease all communication except via mail.

By citing the FDCPA (15 U.S.C. § 1692g), you let them know you aren't an easy target. It's like showing a badge; it tells the collector that you know the law and you aren't afraid to use it.

Proving Delivery and Record Keeping

We've seen too many consumers lose their cases because they "lost the receipt." Don't be that person. Create a "Debt Defense File" immediately.

This file should contain:

The original letter you received from the collector (and the envelope it came in—the postmark date is vital!).

A copy of the dispute letter you sent.

Your Certified Mail receipt and the signed Return Receipt.

A log of every phone call you receive, including the date, time, and the name of the person you spoke to (even if you just told them to stop calling).

If a collector violates the law, these records are the evidence you'll use to sue them for statutory damages. Under the FDCPA, you can be awarded up to $1,000 plus attorney fees for their violations.

What Constitutes Proper Debt Validation?

Many collectors will respond to your dispute by sending a single page that just repeats the information from their first letter. That is not validation.

Validation requires the collector to provide actual proof that the debt exists and that they have the legal right to collect it.

Type of Proof | Informal Verification (Weak) | Legal Validation (Strong) |

|---|---|---|

Debt Amount | A printout from the collector's own computer. | An itemized statement from the original creditor showing all charges/payments. |

Ownership | A letter saying "We bought this debt." | A "Chain of Title" showing every sale from the original creditor to the current collector. |

Agreement | A mention of a "contract." | A copy of the signed original agreement or contract. |

Identity | Just your name on a list. | Proof that you are the person who actually signed for the credit. |

Under 12 CFR § 1006.38 - Disputes and requests for original-creditor information, if you request the original creditor's info, they must provide it. If the original creditor is the same as the current one, they must explicitly tell you that.

When to Dispute Invalid Debt Notice for Paid Accounts

There is nothing more frustrating than being hounded for a debt you already took care of. This often happens because of a "lag" in communication when a debt is sold. You pay the original creditor, but they've already sold the "paper" to a collector, and the message doesn't get through.

If you are in this situation, your dispute invalid debt notice needs to be backed up by cold, hard facts.

Send copies (never originals!) of your cancelled checks.

Include bank statements showing the payment.

If you have a "Paid in Full" letter from the original creditor, that's your "golden ticket."

Check out the CFPB's advice on what to do if a collector contacts you about a debt you already paid for more official guidance.

Handling Identity Theft and Errors

If the debt isn't yours because someone stole your identity, a simple dispute letter isn't enough. You need to provide the collector with an Identity Theft Report from the FTC (IdentityTheft.gov) or a police report.

When you provide this documentation, the collector is legally required to stop reporting that debt to credit bureaus. If they continue to report it, they are in violation of the Fair Credit Reporting Act (FCRA), and you may have grounds for a lawsuit.

Dealing with Time-Barred Debts and Credit Reporting

Every debt has an expiration date, known as the Statute of Limitations. Once this time passes, the debt is "time-barred." This means the collector can still ask you to pay, but they cannot legally sue you to force payment.

In Michigan, the statute of limitations for most contract debts (like credit cards) is 6 years. In Florida, it's generally 5 years for written contracts and 4 years for oral agreements.

CRITICAL WARNING: Be extremely careful. In some states, making even a $5 "good faith" payment or acknowledging in writing that you owe the debt can "restart the clock." This gives the collector a brand new 6-year window to sue you. This is why we tell people: Dispute first, talk later.

For more on this, read our article on Struggling with Debt Collectors.

How Disputes Affect Your Credit Score

When you dispute invalid debt notice, the collector must notify the credit bureaus that the account is "disputed." They cannot report it as a standard delinquent debt without that "disputed" tag.

If they fail to mark it as disputed, or if they report information they know is false, they are violating the FCRA. A successful dispute can lead to the debt being removed from your credit report entirely, which can result in a significant "bump" to your credit score.

Rights Regarding Expired Debts

If a debt is time-barred, a collector cannot threaten to sue you. If they say, "We will take you to court" over a 10-year-old credit card debt in Michigan, they have violated the FDCPA. Threats of legal action that cannot legally be taken are a major "no-no" in the collection world.

Common Mistakes and Reporting Violations

The biggest mistake people make? Ignoring the letter.

Ignoring a debt collector doesn't make them go away; it makes them more aggressive. They might assume you have no defense and move straight to filing a lawsuit. If you get sued and don't respond, they get a "default judgment," which allows them to garnish your wages or freeze your bank account.

Another common mistake is "overshadowing." This is when a collector sends you a letter that says you have 30 days to dispute, but then calls you the next day demanding payment "immediately." This "overshadowing" of your dispute rights is a legal violation.

If you find yourself facing a summons, don't panic. Read our What to Do When Sued by a Debt Collector: Complete First Steps Guide to get your bearings.

Where to Report FDCPA Violations

If a collector is harassing you, calling you at 6:00 AM, or refusing to validate a debt, you need to report them.

CFPB (Consumer Financial Protection Bureau): The heavy hitters. They track patterns of abuse.

FTC (Federal Trade Commission): Great for reporting scams and identity theft.

State Attorney General: In Florida or Michigan, the AG's office has consumer protection divisions specifically for this.

What to Do If the Collector Fails to Validate

If 30 days pass and the collector hasn't sent you validation, but they keep calling or reporting the debt, they are in the wrong.

At this point, you should:

Send a "Final Notice" or "Cease and Desist" letter.

File a complaint with the CFPB.

Consult with a consumer rights platform (like KillDebt) to see if you have a case for statutory damages.

If they can't prove you owe it, they shouldn't be collecting it. Period.

Conclusion

Dealing with debt collectors feels like a David vs. Goliath situation, but the FDCPA gives you the stones for your sling. By knowing how to dispute invalid debt notice correctly, you shift the burden of proof from your shoulders to theirs.

At KillDebt, we believe that everyone deserves a fair fight. That’s why we created a DIY legal defense system powered by ParkerGPT. Our AI isn't just a chatbot; it’s trained on consumer debt law and real court strategies developed over 30+ years by attorney Brian Parker.

We don't just give you a template; we analyze your specific situation. And with our new Court Tester, you can even practice your motion in front of an AI judge before you ever step foot in a courtroom. You'll have an AI co-counsel whispering strategy in your ear, helping you identify the exact weaknesses in the collector's case.

Don't let collectors bully you into paying for their mistakes. Fight back with KillDebt and take control of your financial future today.

Frequently Asked Questions (FAQ)

Can I dispute a debt after the 30-day window has passed?

Yes, you can dispute a debt at any time. However, if you do it within the first 30 days, the collector must stop collection activities until they provide validation. After 30 days, they can continue to collect while they process your request. It’s always better to act fast, but late is better than never.

Does sending a dispute letter stop a debt collection lawsuit?

Not necessarily. A collector can still file a lawsuit during the 30-day window, although many wait to see if you'll pay. If you are served with a lawsuit, a dispute letter is not a legal answer to the court. You must file a formal "Answer" with the court to avoid a default judgment.

What happens if the debt collector ignores my dispute letter?

If they ignore your letter and continue to contact you or report the debt to credit bureaus, they are likely violating the FDCPA. This is where your record-keeping pays off. You can use their lack of response as a primary defense if they ever try to sue you, and you may even be able to sue them for their non-compliance.