What Every Debt Defendant Needs to Know About Pretrial Motions

A motion to compel discovery is one of the most powerful tools available to someone defending against a debt collection lawsuit — yet most people facing a summons have never heard of it.

Here's the quick answer:

What it is: A formal request asking the court to order the other side to answer questions or hand over documents they've ignored or refused to produce.

When to use it: When a debt collector fails to respond to your interrogatories, dodges your document requests, or gives vague, evasive answers.

What it can do for you: Force the collector to prove they actually own your debt, have the right records, and can back up their claims in court.

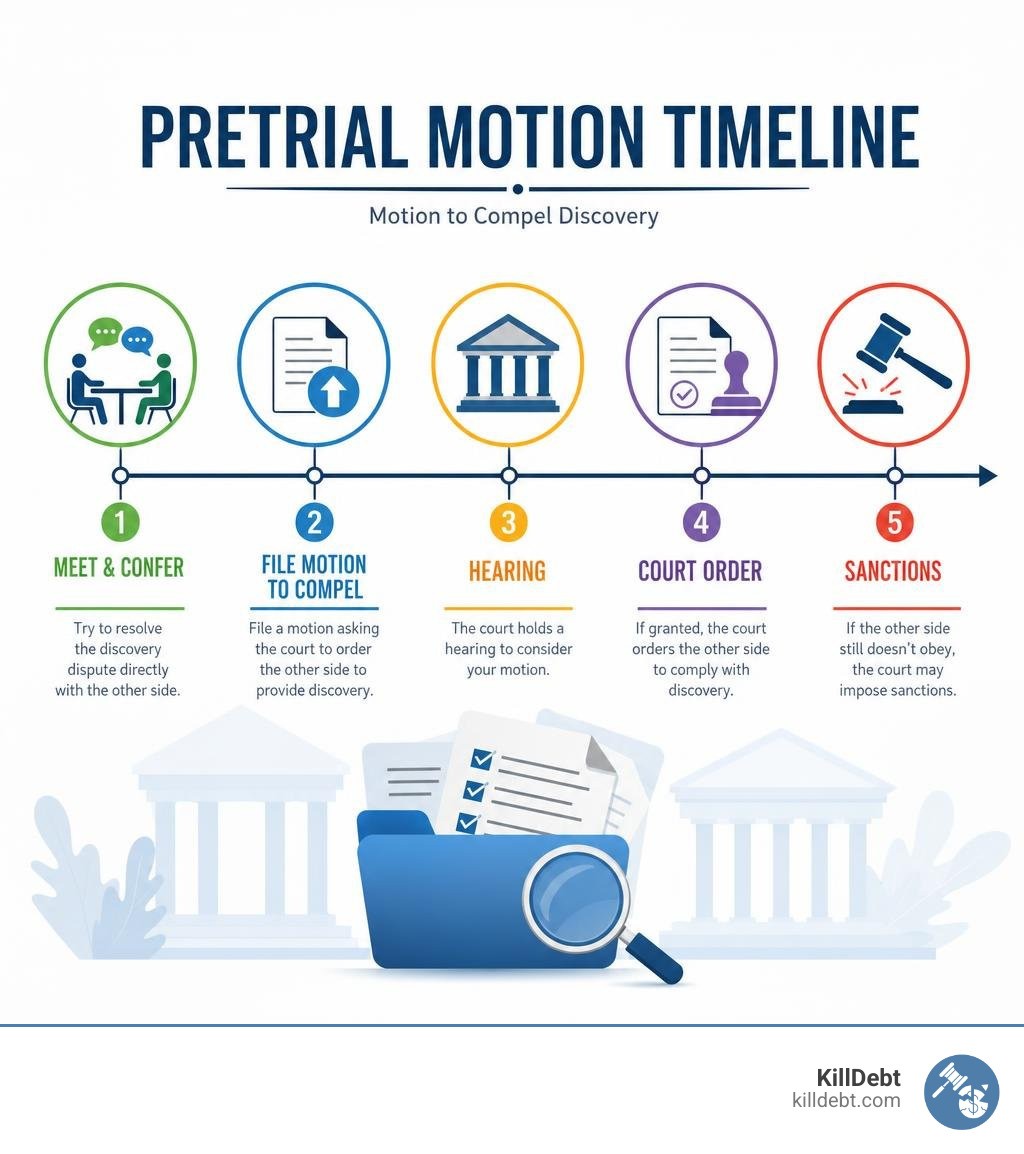

Key requirement: You must first attempt to resolve the dispute directly with the other side (a "meet and confer") before the court will hear your motion.

Deadlines matter: In federal court, file before the discovery cutoff. In California state court, you have 45 days from the date verified responses are served — miss that window and you lose the right entirely.

Pretrial motions like this one level the playing field. Debt collectors count on defendants doing nothing. When you know how to use the court's own rules against them, the dynamic changes fast.

I'm Brian Parker, founder of KillDebt, and over my 30+ years fighting debt collectors in courtrooms across the country, I've used the motion to compel discovery — and the related pretrial motions covered in this guide — to expose missing documentation, broken chain of title, and outright bluffs by debt buyers. Whether you're just getting started or already staring down a court deadline, this guide will walk you through exactly what to do.

What is a Motion to Compel Discovery in a Debt Lawsuit?

When a debt buyer or credit card company sues you, they cannot simply show up on trial day with a random dollar figure and expect the judge to hand them a judgment. They must go through the discovery phase. This is the formal, court-supervised process where both sides exchange evidence.

As a defendant, you have the right to request proof. You can ask for the original credit agreement, the itemized statement of account, and the assignments showing how the debt was sold from the original creditor to the debt buyer.

Unfortunately, debt collectors often ignore these requests. They operate on volume, hoping you will panic and default. When they refuse to hand over the evidence you legally requested, you do not have to sit back and take it. You can file a formal request asking the judge to step in.

To understand how to force their hand and demand the records they are hiding, read our guide on How to Compel Discovery Debt Case.

When is a Motion to Compel Discovery Appropriate?

A motion to compel is appropriate when the plaintiff fails to comply with their discovery obligations. In consumer debt cases, this typically occurs when the collector:

Fails to answer your interrogatories (written questions).

Refuses to produce documents proving the chain of title or account history.

Fails to respond to requests for admission.

Provides incomplete, evasive, or heavily redacted responses.

If you need help drafting your initial questions to the collector so you can set up this legal trap, check out our guide on how to Answer Interrogatories Debt Case.

Compelling Initial Responses vs. Compelling Further Responses

There is a major procedural difference between a complete failure to respond and an inadequate response:

Compelling Initial Responses: If the debt collector completely ignores your discovery requests and the statutory deadline (usually 30 to 45 days) passes without a word, you are compelling an initial response. In many jurisdictions, because they failed to respond at all, they have waived their right to object to your requests.

Compelling Further Responses: If the collector sends back timely responses but fills them with evasive answers and boilerplate objections (e.g., "objected to on the grounds that it is overbroad, burdensome, and not reasonably calculated to lead to admissible evidence"), you must move to compel further responses. This requires a much more detailed legal argument showing why their objections are invalid.

Procedural Requirements and Deadlines for Discovery Motions

Filing a motion is not just about telling the judge that the other side is being unfair. You must follow strict procedural rules. Because KillDebt specializes in defending consumers in Florida and Michigan, we focus heavily on the rules in those states, as well as the federal rules if your case is in federal district court.

Jurisdiction | Governing Rule | Meet & Confer Required? | Key Timeline / Deadlines |

|---|---|---|---|

Federal Court | Yes (Strict Certification) | Must file within a reasonable time, typically before the court-ordered discovery cutoff. | |

Florida State | Yes | Must be filed and heard before trial. Specific circuits have ex parte rules for total non-response. | |

Michigan State | Yes | Governed by MCR 2.313; must be filed promptly after the deficiency occurs. |

Other states have similar frameworks. For example, Tennessee litigants rely on Rule 37.01: Motion for Order Compelling Discovery. \| Tennessee Administrative Office of the Courts , while Louisiana uses Louisiana Code of Civil Procedure Tit. III, Art. 1469 \| FindLaw to govern these disputes. No matter where your case is, procedural precision is mandatory.

The Mandatory Meet-and-Confer Obligation

You cannot jump straight to filing a motion. Judges despise discovery disputes and expect adult litigants to try to work things out first.

Before filing, you must conduct a "meet-and-confer." This means sending a formal letter (and ideally following up with a phone call or video conference) detailing exactly what is missing and giving the other side a reasonable deadline (usually 10 to 14 days) to cure the issue.

If you do not include a signed certification in your motion stating that you attempted in good faith to resolve the issue, the judge will likely throw your motion out without even reading it.

Preparing the Motion to Compel Discovery Package

A complete motion package is highly structured. To give yourself the best chance of success, your filing should include:

Notice of Motion: States the date, time, and location of the hearing.

The Motion Itself: A clear explanation of what was served, when it was due, and how the plaintiff failed to comply.

Good-Faith Certificate (Declaration): Proof of your meet-and-confer efforts.

Memorandum of Points and Authorities: The legal arguments and case law supporting your right to the documents.

Exhibits: Copies of your original requests, the green card or proof of service, and your meet-and-confer letters.

If you are dealing with evasive answers rather than a total lack of response, some states require a "separate statement." For example, California has highly specific formatting rules under CRC 3.1345, which you can study in the California Motion to Compel — Practitioner's Guide \| LawSnap . Even if your state (like Florida or Michigan) does not require a formal separate statement, it is excellent practice to include a clear, side-by-side chart showing your request, their objection, and your argument for why they must answer.

To make this easy, you can download a customizable Motion to Compel Discovery \| Free PDF & Word Template to help draft your paperwork.

Defeating Debt Collector Evidence: Striking Affidavits and Opposing Motions

In most debt lawsuits, collectors try to bypass trial altogether by filing a Motion for Summary Judgment. To do this, they rely heavily on a "sworn affidavit" from an employee who claims to have reviewed the records and verified that you owe the money.

These affidavits are almost always junk. They are frequently "robo-signed" by employees who have never actually looked at your specific file, or they attempt to introduce original creditor records without meeting the strict legal exceptions for hearsay.

To learn how to spot these fake or legally insufficient documents during your lawsuit, see our guide on Debt Case Document Review.

How to File a Motion to Strike a Debt Buyer's Affidavit

If a debt buyer attaches a third-party affidavit to support their claims, you can file a Motion to Strike.

Under the rules of evidence in Florida and Michigan, documents created by another company (like the original credit card issuer) are hearsay when introduced by a debt buyer unless they meet the Business Records Exception. To qualify, the person signing the affidavit must have personal knowledge of how those records were kept at the time they were created.

A debt buyer's employee rarely has personal knowledge of how Chase or Citibank kept their databases five years ago. If they cannot establish a proper chain of title and personal knowledge, you can move to strike the affidavit. If the judge strikes their affidavit, the collector's entire evidentiary foundation crumbles.

Responding to and Opposing a Motion to Compel

What if the tables are turned and the debt collector files a motion to compel discovery against you?

Do not ignore it. Unopposed motions are almost always granted automatically. Instead, file an opposition brief within your state's deadline (usually 9 to 15 days before the hearing).

You can defeat their motion if you can show:

They failed to meet and confer in good faith.

Their requests are irrelevant to the lawsuit (e.g., asking for your tax returns in a simple credit card case).

Your objections were "substantially justified."

You require a protective order to prevent the disclosure of highly sensitive, non-public personal information.

Resolving the Case Early: Motion for Judgment on the Pleadings

A Motion for Judgment on the Pleadings is a tool used to end a lawsuit early when the facts of the case are completely undisputed and the law clearly favors one side.

If you want a bird's-eye view of how this motion fits into your overall defense strategy, read our Fight Debt Collection Lawsuit Complete Guide.

When to File a Motion for Judgment on the Pleadings

This motion is filed after the defendant has filed their Answer, and the "pleadings" (the Complaint and the Answer) are closed.

It is appropriate when, taking everything the plaintiff says in their complaint as 100% true, they still do not have a legal case. Common examples in debt defense include:

Statute of Limitations: The collector's own complaint shows that the last payment was made eight years ago, and the state's statute of limitations is only six years.

Failure to State a Claim: The plaintiff sued you for "breach of contract" but failed to attach any contract or even allege that a contract existed between you and them.

Comparing Judgment on the Pleadings vs. Summary Judgment

While both motions can end a case without a trial, they look at different things:

Motion for Judgment on the Pleadings: The judge looks only at the four corners of the Complaint and the Answer. No external evidence, discovery responses, or affidavits are allowed.

Motion for Summary Judgment: The court looks at the entire evidentiary record, including deposition transcripts, discovery responses, and affidavits, to determine if there is a "genuine dispute of material fact."

Sanctions and Remedies for Discovery Non-Compliance

If a court orders a debt collector to produce records and they continue to play games, the court can impose severe sanctions under RULE 1.380. FAILURE TO MAKE DISCOVERY; SANCTIONS (in Florida) or MCR 2.313 (in Michigan).

Historically, courts were hesitant to award financial sanctions. In the famous Columbia Survey, only one instance out of about 50 motions decided under Rule 37(a) resulted in the court awarding expenses. The provision requiring the defeated party to pay unless they had "substantial justification" was rarely enforced.

However, in July 2026, courts are far less tolerant of discovery abuse. If you win your motion to compel, the court can order the collector to pay your reasonable expenses, including any filing fees or travel costs.

If the collector still refuses to comply with a direct court order, you can ask for "terminating sanctions," which can include:

Striking the collector's pleadings.

Prohibiting them from introducing any evidence at trial.

Entering a default judgment in your favor (dismissing the case with prejudice).

In Florida's Sixth Judicial Circuit, the court has even established streamlined ex parte procedures under [PDF] Motions to Compel Discovery - Sixth Judicial Circuit to handle total failures to respond without requiring a lengthy hearing, moving directly to compliance and sanctions. Similar strict approaches are used across other Florida districts, as outlined in [PDF] EX PARTE MOTIONS TO COMPEL DISCOVERY IN CIVIL ACTIONS. .

Conclusion

Defending yourself against a debt collector does not mean just sitting back and waiting for a trial. By using pretrial motions like a motion to compel discovery, a motion to strike affidavits, or a motion for judgment on the pleadings, you can actively attack the collector's case and force them to put up or shut up.

At KillDebt, we provide you with the exact tools you need to take control of your case. Our DIY legal defense system features ParkerGPT, an AI trained specifically on consumer debt law and real-world strategies developed over 30+ years by attorney Brian Parker.

We also just rolled out our brand-new Court Tester! This is an AI courtroom simulation built on your actual case. You can upload your real filings and, within minutes, practice arguing your motions in front of an AI judge, against AI opposing counsel, while a private AI co-counsel whispers winning strategies that only you can see.

Don't let debt buyers bully you with unverified claims. Discover how easy it is to fight back by visiting Empower your debt defense with KillDebt.

Get started with KillDebt pricing

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments.

Frequently Asked Questions (FAQ)

What happens if a debt collector ignores a motion to compel?

If a judge signs an order compelling discovery and the collector ignores it, you should immediately file a Motion for Sanctions. You can ask the judge to dismiss the case entirely because the plaintiff is refusing to follow court orders.

Can I file a motion to compel without an attorney?

Yes! Pro se litigants have the exact same right to conduct discovery and file motions as licensed attorneys. While the rules can seem intimidating, courts must give you a fair opportunity to present your case. For step-by-step guidance on navigating this without an expensive lawyer, read our Debt Lawsuit Defense Guide. You can also review general federal drafting tips in the Federal Pro Se Clinic guide.

How long does a debt collector have to respond to discovery?

In both Florida and Michigan, a party generally has 30 days to respond to written discovery requests (like interrogatories or document requests) after they are served. This can sometimes be extended to 45 days if the requests were served along with the initial summons and complaint. If you are drafting your initial response to their lawsuit, make sure to read our guide on how to file a Sample Answer to Debt Collection Lawsuit.