When a Debt Buyer Sues You, Do They Actually Own Your Debt?

Quick answer: When a debt buyer sues you, they must prove they legally own your specific account by producing a complete set of chain custody debt documents — every bill of sale, assignment, and transfer record from the original creditor all the way to them. If any link in that chain is missing, broken, or unauthenticated, they may not have the legal right to sue you at all.

What a valid chain of custody requires:

Original credit agreement — proof the debt existed with the original creditor

Bill of sale or purchase agreement — showing the original creditor sold the debt

Assignment schedule — listing your specific account number in the transfer

Every intermediate transfer — documentation for each resale between buyers

Authenticated affidavit or witness — someone with personal knowledge to verify the records

Most people who get hit with a debt collection lawsuit assume the collector must have everything in order — or they wouldn't be suing, right?

Wrong.

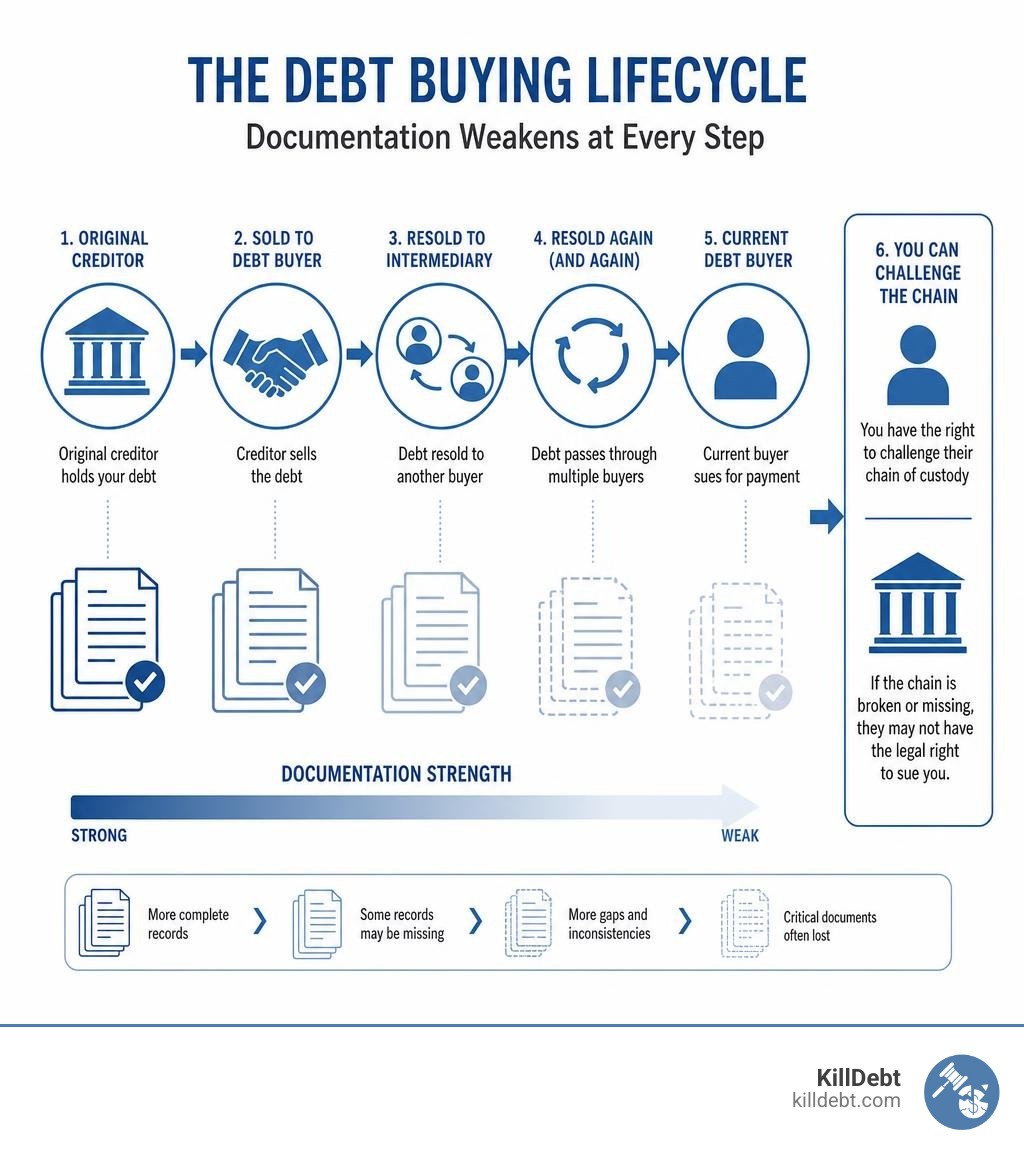

Debt buyers purchase huge pools of accounts — often thousands at a time — for as little as 4 cents on the dollar. By the time a debt has been sold and resold two or three times, critical documents get lost, account details get mixed up, and the paper trail becomes dangerously thin.

That thin paper trail is your defense.

Courts require debt buyers to prove they own your specific account. Not just that they bought a portfolio of debts — your account, specifically. If they can't produce every document in that chain, they may lack the legal standing to collect a single dollar from you.

I'm Brian Parker, and for over 30 years I've been in courtrooms across the country challenging exactly this kind of weak chain custody debt documentation — watching debt buyers crumble when they can't prove ownership. I built KillDebt to put those same courtroom strategies directly in your hands, fast and affordably. Let me walk you through exactly what to look for and how to use it.

What is the Chain Custody Debt Documents Trail?

To understand how to defeat a third-party debt buyer in court, we first need to understand what the chain of custody actually represents. In legal terms, "chain of custody" and "chain of title" are two sides of the same coin, but they track slightly different things.

Chain of Title refers to the legal ownership history of the debt. It is the paper trail showing who legally owned the right to collect the money at any given second.

Chain of Custody refers to the physical possession history of the actual, original documents—specifically the promissory note or original contract.

This distinction is massive when dealing with negotiable instruments. Under the Uniform Commercial Code (UCC) Article 3, which governs negotiable instruments like promissory notes, the party seeking to enforce the note must generally have physical possession of the original document or show exactly how they lost possession of it. You can read more about how physical possession functions under UCC Article 3 rules on physical possession.

When a third-party debt buyer files a lawsuit against you in Florida or Michigan, they do not start with the same natural credibility as an original creditor (like Chase or Citibank). Because they did not create the debt, they must legally establish their right to step into the original creditor's shoes. If there is a gap in the physical possession or the legal transfer of those chain custody debt documents, the debt buyer cannot establish their standing to sue in court. Without standing, the court lacks jurisdiction to hear the case, and the lawsuit must be dismissed.

Key Documents Required to Establish a Valid Chain of Ownership

If a debt buyer wants to prove they own your debt, they cannot just show up in court with a computer printout of your name and a dollar amount. They must present a clean, uninterrupted trail of specific legal documents. Here are the core components that must be present in a valid chain of custody:

The Original Credit Agreement: This is the contract you originally signed with the bank or credit card issuer. It lays out the terms, interest rates, and conditions of the account. If the debt buyer cannot produce this, they struggle to prove you ever agreed to the terms they are suing you under.

The Master Purchase Agreement: When debt is sold in bulk, the original creditor and the debt buyer sign a massive contract. This agreement outlines the terms of the sale of thousands of accounts.

The Bill of Sale: This is the receipt. It is a short document stating that on a specific date, the seller transferred a pool of accounts to the buyer.

The Assignment Schedule (or "Exhibit A"): This is the holy grail of debt collection defense. The Bill of Sale almost always references an attached schedule or data tape containing the specific accounts being transferred. If the debt buyer does not produce the page of that schedule showing your specific account number, name, and balance, they have not proven your debt was part of the sale.

Let's look at how the evidence differs depending on who is suing you:

Evidence Comparison Table

Evidence Type | Original Creditor Case | Debt Buyer Case |

|---|---|---|

Primary Proof of Contract | Original credit agreement signed by you. | Copy of credit agreement plus corporate transfer records. |

Account Statements | Complete monthly billing history from day one to charge-off. | Often just the final statement or a few scattered digital records. |

Proof of Transfer | Not required (they created the account). | Unbroken chain of Bills of Sale and assignment schedules. |

Witness Testimony | Employee of the bank who knows how their records are kept. | Debt buyer employee who has never seen the bank's original systems. |

The Role of Affidavits in Chain Custody Debt Documents

Because debt buyers rarely want to fly live witnesses to small claims or county courts in Michigan or Florida, they rely almost exclusively on written affidavits. An "Affidavit of Debt" or "Affidavit of Sale" is a sworn statement signed by an employee of the debt buyer, claiming that their records show you owe the money.

There is a massive legal problem with these affidavits: hearsay.

Under the rules of evidence, a witness can only testify to things they have personal, first-hand knowledge of. A debt buyer's employee does not have personal knowledge of how Chase Bank or Synchrony Bank kept their records five years ago. They did not work there. They did not mail you the statements.

To bypass this, debt buyers try to use the "Business Records Exception" to the hearsay rule. They argue that because they bought the digital files, those files are now their business records. However, courts have repeatedly ruled that simply importing another company's records into your database does not magically give your employees personal knowledge of how those records were created or maintained. You can learn more about how to expose these affidavit weaknesses by studying how debt buyers use affidavits.

Common Weaknesses in Debt Buyer Documentation You Can Challenge

When we analyze lawsuit filings, we look for the soft spots where the debt buyer’s case is structurally weak. Because they buy these accounts in bulk, their documentation is almost always riddled with errors.

Here are the most common vulnerabilities we exploit to defeat debt buyers:

Redacted or Missing Account Schedules: The debt buyer will file a Bill of Sale that says, "Seller hereby transfers the accounts listed on Exhibit A." But when you look at the lawsuit, Exhibit A is missing, or it is completely blacked out (redacted) except for one single line with your name. A redacted document with no authentication does not prove the entire contract was legally executed or that your account was properly included.

Missing Intermediate Transfers: If Bank A sold the debt to Buyer B, who sold it to Buyer C, who is now suing you, Buyer C must produce the transfer documents for both sales. If they only show the sale from Buyer B to Buyer C, they have a broken chain. They cannot prove Buyer B had the legal right to sell it in the first place.

Generic Bills of Sale: Many Bills of Sale are incredibly vague. They might state that the seller is transferring "certain charged-off accounts" without any specific reference to account numbers, dates, or the original lending institution.

When you identify these gaps, you can confidently stand up in court and explain to the judge how to argue lack of evidence to get the case thrown out.

Spotting Gaps in Chain Custody Debt Documents

To successfully challenge a debt buyer, you must become a detective. You have to look at the dates, the names, and the fine print on every document they attach to the summons.

Chronological Errors: We often find transfers that are physically impossible. For example, a Bill of Sale might claim that Buyer B sold the debt to Buyer C on June 10th, but the document showing Bank A selling the debt to Buyer B is dated June 15th. A company cannot sell a debt they do not own yet!

The Wrong Original Creditor: It is surprisingly common for debt buyers to list the wrong original creditor in their complaint. They might allege the debt originated with WebBank, but the statements they attach show the account was actually opened with Comenity Bank.

Unauthenticated Computer Records: Debt buyers love to print out a single sheet of paper from their own computer system and call it "proof" of the debt. However, under established legal precedents (such as the landmark federal case In re Vinhnee), computer-generated records require a qualified witness to testify about the reliability, security, and data integrity of the computer system that created them. A debt collector almost never has a witness who can lay this foundation.

These logical and structural gaps are classic chain of assignment issues that can completely dismantle a collector's case.

How to Use Chain of Custody Defenses in a Debt Lawsuit

If you have been served with a summons and complaint in Florida or Michigan, the clock is ticking. You generally have 20 days in Florida and 21 days in Michigan to file a written Answer. If you do not respond, the debt buyer will win a default judgment, allowing them to garnish your wages or freeze your bank accounts.

Here is the step-by-step strategy we use to fight back:

Deny Ownership Allegations: In your written Answer, do not admit that the plaintiff owns the debt. If you are not 100% certain of their ownership (and you shouldn't be, because they haven't proven it yet), state: "Defendant is without knowledge or information sufficient to form a belief as to the truth of the allegations and therefore denies the same."

Raise Affirmative Defenses: List "Lack of Standing" and "Failure to State a Claim" as affirmative defenses. State that the plaintiff has failed to show a complete, authenticated chain of title transferring the specific account to the plaintiff.

Send Discovery Requests: Once the Answer is filed, the real fun begins. You have the right to demand they produce the unredacted purchase agreements, the complete assignment schedules showing your account, and the data integrity logs for their computer records.

Initiate the Debt Validation Dispute: If you are still in the early stages of collection before a lawsuit is filed, you must leverage the debt validation dispute process immediately.

Conclusion

You do not have to lie down and let a multi-billion-dollar debt buyer steamroll you. When these companies sue consumers, they are playing a numbers game. They expect 90% of people to ignore the lawsuit, allowing them to get easy default judgments.

When you stand up, answer the lawsuit, and demand to see their chain custody debt documents, you flip the script. You force them to spend time and money trying to locate documents they likely never had in the first place.

At KillDebt, we believe in complete self-defense empowerment. We built ParkerGPT, an AI trained on over 30 years of real-world consumer defense strategies developed by attorney Brian Parker. It doesn't just give you generic templates; it analyzes your actual court summons, spots the documentation weaknesses, and drafts customized, court-ready responses.

And if you want to test your arguments before you ever walk into a courtroom, our brand-new Court Tester tool lets you run an AI courtroom simulation. You can upload your filings, argue your motion in front of an AI judge, face off against an AI opposing counsel, and have an AI co-counsel whispering winning strategies directly to you.

Do not let broken chains drag you down. Check out our affordable pricing and services and let us help you fight back today.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments.

Frequently Asked Questions (FAQ)

What happens if a debt collector cannot produce a complete chain of custody?

If a debt collector cannot produce a complete, authenticated chain of custody, they cannot prove they have the legal right to collect the money. In court, this results in a lack of standing. We can use this failure to file a Motion to Dismiss or a Motion for Summary Judgment. In the vast majority of cases where the consumer fights back and demands these documents, the debt buyer will choose to dismiss the case voluntarily rather than expose their lack of documentation to a judge.

How does the FDCPA protect me against unverified debt buyers?

The Fair Debt Collection Practices Act (FDCPA) is a powerful federal shield. Under the FDCPA, a debt collector must send you a written validation notice containing specific information about the debt within five days of their initial communication. Once you receive this, you have a 30-day window to dispute the debt in writing. When you send a dispute, the collector must cease all collection activities—including phone calls and lawsuits—until they obtain verification of the debt and mail it to you. You can use our specialized debt validation letters to force them to put up or shut up.

Can a debt buyer sue me if the original creditor went out of business?

Yes, they can try, but it makes their job infinitely harder. If the original creditor is out of business (for example, an old retail store credit card issuer that has folded), the debt buyer will find it virtually impossible to get an authenticated affidavit from an employee of that original bank. Since they cannot get a witness from the original creditor to authenticate the records under the business records exception, their entire chain of custody collapses under the weight of hearsay objections. This is a classic scenario where understanding who is suing me reveals the fatal flaw in their lawsuit.