When They Sue You Without Proof, You Have More Power Than You Think

If you're trying to figure out how to argue lack of evidence in a lawsuit, here's the fast answer:

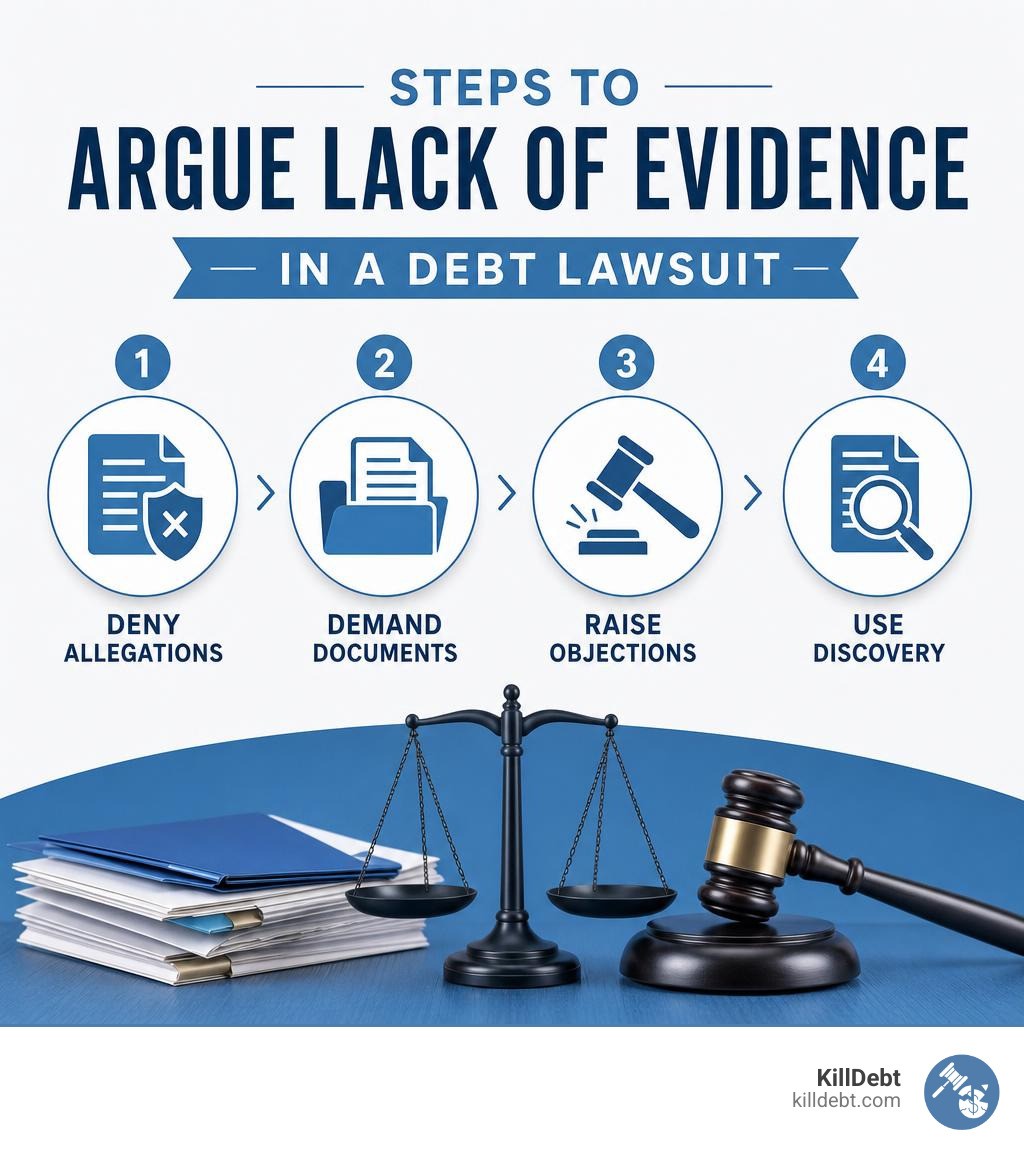

Deny the allegations — force the plaintiff to prove every claim

Request documentation — demand the original contract, chain of custody, and proof of ownership

Raise objections — challenge hearsay, speculation, and lack of foundation

File an Answer — respond before the deadline or risk automatic default judgment

Use discovery — send written requests for all documents the collector is relying on

Challenge standing — ask whether they actually have the legal right to sue you

You just got served. There's a court date on the paper. Maybe it's a credit card debt, a medical bill, or an account you barely recognize. The number looks wrong. The company suing you isn't even the original creditor.

Here's the thing most people don't know: the plaintiff has to prove their case — you don't have to prove anything.

In a civil lawsuit, the burden of proof sits squarely on the person doing the suing. They must show it's "more likely than not" that you owe the money — roughly a 51% threshold. That sounds low, but debt buyers — companies that purchase old debts for as little as 4 cents on the dollar — often show up to court with incomplete records, missing contracts, and no real paper trail.

That's a weak case. And a weak case can be beaten.

Approximately 85% of civil cases settle before trial, often because one side recognizes the evidence problem early. When you know how to spot those gaps and raise the right objections, you shift the leverage back to yourself.

My name is Brian Parker, and for over 30 years I've been in courtrooms across the country showing consumers exactly how to argue lack of evidence in a lawsuit — fighting debt buyers, collection law firms, and creditors who count on you not showing up. I founded KillDebt to put those same strategies directly in your hands.

Understanding the Burden of Proof in Civil Debt Lawsuits

To win any legal fight, you have to understand the rules of the game. In a lawsuit, the most important rule is the "burden of proof." This dictates which party is responsible for presenting the evidence and how convincing that evidence must be.

In criminal cases, we all know the standard is "beyond a reasonable doubt"—a very high bar, close to 99% certainty. But a debt collection lawsuit is a civil matter. In civil court, the standard of proof is much lower. It is called the preponderance of the evidence.

The preponderance of the evidence standard simply means that a claim is more likely to be true than not true. If the judge or jury is 51% convinced by the plaintiff's story, the plaintiff wins.

This 51% threshold is a double-edged sword. While it is easier for a debt collector to meet than a criminal standard, they still must cross that 51% line with admissible, reliable evidence. They cannot simply wave a piece of paper with your name on it and demand a judgment.

If you are facing a collection lawsuit in Florida or Michigan, understanding how to hold them to this standard is your primary defense. If they cannot produce the documents to tip the scale past 50%, they lose.

Crucially, the burden of proof does not shift to you just because you are the defendant. You do not have to prove that you don't owe the debt; you merely have to show that the plaintiff has failed to prove that you do. For a deeper dive into these concepts, check out our More info about debt lawsuit defense.

The Plaintiff's Evidentiary Burden in Debt Collection

When a debt collector files a lawsuit, they must establish what is called a prima facie case. This means they must present enough basic, legally sufficient evidence to support their claim before you are even required to defend yourself.

In consumer debt cases, particularly those brought by third-party debt buyers, establishing a prima facie case is surprisingly difficult. A debt buyer is not the original creditor (like Chase, Citibank, or Capital One). They are a company that bought a portfolio of delinquent accounts.

To win, a debt buyer must prove three main elements:

Standing: They must prove they actually own your specific debt.

Chain of Custody: They must show a continuous, unbroken chain of title from the original creditor down to them. If the debt was sold three times, they need the bills of sale and assignment documents for all three transactions.

The Debt Details: They must prove the exact amount of the debt is accurate, including how interest and fees were calculated.

Often, debt buyers try to bypass these requirements by filing broad, unsupported declarations or affidavits from their own employees. These employees usually have never seen the original creditor’s files and have no personal knowledge of how your account was maintained.

When facing a motion for summary judgment, you must aggressively challenge these declarations. As highlighted in Summary Judgement Motions: Proving Lack of Admissible Evidence, any declaration or expert opinion submitted in support of a summary judgment must be backed by concrete, admissible facts. If the debt buyer relies on broad, sweeping statements without attaching the actual underlying records, you can argue that their evidence is legally inadmissible, preventing them from securing an easy win.

Absence of Evidence vs. Negative Evidence: What’s the Difference?

When you stand up in court to argue that a debt collector has no case, you need to understand a subtle but vital distinction: the difference between the absence of evidence and negative evidence.

This distinction is thoroughly explored in the legal-philosophical treatise On the Absence of Evidence.

Absence of Evidence: This occurs when there is simply a lack of data or documentation. For example, a debt collector claims you made a payment on a specific date to restart the statute of limitations, but they have no ledger, bank record, or receipt showing that transaction. The evidence simply does not exist.

Negative Evidence: This is the positive result of a search or test that yielded no finding. For instance, if you request a search of the original creditor’s master database for a signed credit agreement, and the search returns a certified report stating "No record found," that is negative evidence. It is affirmative proof that the document does not exist.

In legal argumentation, relying blindly on the absence of evidence can sometimes lead to a logical fallacy known as argumentum ad ignorantiam (the argument from ignorance). This is the mistake of claiming that a proposition is true simply because it has not been proven false, or vice versa.

However, in a lawsuit, the rules of the burden of proof transform this logical fallacy into a valid legal defense. Because the plaintiff bears the burden of proving their claims, the absence of evidence on an essential element of their case is legally fatal to their lawsuit. If they cannot produce the contract or the assignment history, their lack of evidence serves as immediate grounds for dismissal.

How Argue Lack Evidence Lawsuit Strategies Using Logical Fallacies

Debt collection attorneys are notorious for "table pounding." There is an old legal adage: "If you have the facts on your side, pound the facts. If you have the law on your side, pound the law. If you have neither, pound the table."

When a debt buyer has no real evidence, their attorney will often attempt to distract the court using rhetorical tricks and logical fallacies. To defend yourself effectively, you must learn to identify and expose these strategies.

According to the defense guide Responding to Table Pounding: Defense Through the Exposure of Fallacies, here are the most common fallacies used by collection lawyers:

The Red Herring: The collector's attorney will try to introduce irrelevant facts to distract the judge. For example, they might point out that you had a high credit score in 2021 or that you have a history of paying other bills. This has absolutely nothing to do with whether they can prove they own this specific debt today.

Post Hoc Ergo Propter Hoc (Temporal Fallacy): They may argue that because your name is on a general list of thousands of sold accounts, and you once had a credit card with the original creditor, then your specific account must be included in their purchase. This is a logical leap. A temporal or loose association does not equal legal proof of ownership.

Argumentum ad Ignoriam (Appeal to Ignorance): They might argue: "The defendant hasn't proven they didn't spend this money, so they must owe it." This is a direct violation of the burden of proof.

When you hear these arguments, do not get defensive. Point them out to the judge. Explicitly state: "Your Honor, the plaintiff is attempting to shift the burden of proof. They are committing an argument from ignorance. It is their job to prove I owe this debt to them, not my job to prove I do not."

How Argue Lack Evidence Lawsuit: The Ultimate Defense Guide

If you want to know how to argue lack of evidence in a lawsuit and win, you need a systematic, step-by-step game plan. You cannot simply show up to court on your trial date and announce that the other side has no proof. You must build your defense systematically from the moment you receive the summons.

Step 1: File Your Answer Immediately

The worst thing you can do is ignore the lawsuit. If you do not file a formal written Answer within the strict legal deadline, the court will enter a default judgment against you. Once they have a default judgment, they can garnish your wages and freeze your bank accounts without ever having to prove their case.

In Florida: You have exactly 20 days to file a written Answer.

In Michigan: You have 21 days if you were served in person, or 28 days if you were served by mail or outside the state.

When you write your Answer, you must explicitly deny their allegations. Denying an allegation does not mean you are lying; it simply means you are demanding that they prove it. You can find a template for this in our Sample Answer to Debt Collection Lawsuit.

Step 2: Assert Lack of Standing and Chain of Custody

In your Answer, raise affirmative defenses. Explicitly state that the plaintiff lacks standing to sue because they have failed to show an unbroken chain of custody transferring ownership of the alleged debt from the original creditor to the plaintiff.

Step 3: Initiate the Discovery Process

Discovery is the pre-trial phase where both parties must exchange information. This is where you force the debt collector's hand. Send them formal, written discovery requests, including:

Requests for Production of Documents: Demand the original signed contract, the complete payment history, and the specific bill of sale showing your account was transferred.

Interrogatories: Ask them to identify every witness who has personal knowledge of your account and to state the exact date and method of every assignment of the debt.

If they fail to provide these documents—which they often do—you can file a motion to compel. Learn exactly how to do this in our guide on How to Compel Discovery in a Debt Case.

Common Objections When Evidence is Weak or Absent

If your case goes to a hearing or trial, the debt collector will try to introduce whatever weak documents they have. This is where you must stand up and object. If you do not object, the judge will admit their weak evidence, and once it is admitted, the judge can use it to rule against you.

To block their documents, you need to master the basic evidentiary foundations. The State Bar of Michigan's guide on Evidentiary foundations highlights that all evidence must meet strict standards of reliability before it can be considered by a court.

Here are the most powerful objections you can raise in a debt collection lawsuit:

Hearsay: Hearsay is an out-of-court statement offered to prove the truth of the matter asserted. When a debt buyer tries to introduce a printout of an electronic spreadsheet from the original creditor, that printout is hearsay.

The Business Records Exception: Debt buyers will try to bypass hearsay by claiming the spreadsheet is a "business record." To qualify for this exception, they must present a witness or a certified affidavit from someone who actually worked for the original creditor and can testify to how those records were created and maintained. A declaration from the debt buyer's own employee, who has never worked for Chase or Citibank, is legally insufficient.

Lack of Foundation: If a witness begins testifying about your account history, object to a lack of foundation. The witness must first explain how they know this information. If they have never reviewed the original source documents, they lack the legal foundation to testify.

Speculation: Object to speculation if the plaintiff’s attorney or witness starts guessing about how interest was calculated, when a payment was made, or why a document is missing. Witnesses are only allowed to testify to facts within their personal, direct knowledge.

Spoliation and Character Evidence: Advanced Defense Tactics

When fighting a debt collection lawsuit, you may occasionally run into situations where the plaintiff has actively destroyed, deleted, or failed to preserve critical documents. This is where advanced defense tactics like spoliation come into play.

Spoliation is the intentional, reckless, or negligent destruction, alteration, or failure to preserve evidence that is relevant to a pending or reasonably foreseeable lawsuit.

Under Florida law, as outlined in Spoliation of Evidence: A Double-Edged Sword, once a party reasonably anticipates litigation, they have an absolute legal duty to preserve all relevant evidence. If they fail to do so, the court can impose severe sanctions.

The most powerful remedy for spoliation is an adverse inference instruction. This is a ruling by the judge telling the jury (or concluding themselves, in a bench trial) that because the plaintiff destroyed or failed to keep the records, the court must assume that those missing records would have hurt the plaintiff's case and helped yours.

If a debt buyer sues you but claims they "no longer have" the original credit card statements or the assignment contract, you should argue that their failure to preserve these essential records constitutes spoliation, severely weakening their case.

How Argue Lack Evidence Lawsuit Rules Under FRE 404 and Spoliation

In addition to spoliation, you can use the rules governing character evidence to block debt collectors from using dirty tactics.

Under Federal Rule of Evidence 404 (and the corresponding Michigan Rules of Evidence, which you can review in the Michigan Courts Evidence Benchbook), character evidence is generally inadmissible to prove that a person acted in conformity with a specific character trait on a particular occasion.

Rule 404(b) explicitly prohibits the introduction of "other crimes, wrongs, or acts" to prove a person's propensity to act a certain way.

In a debt collection lawsuit, collectors will sometimes try to introduce evidence of your past financial difficulties. They might try to show that you defaulted on a different loan five years ago, or that you have other collection accounts on your credit report. They want the judge to think: "They defaulted before, so they probably defaulted here too."

This is classic, prohibited propensity evidence. You must immediately object under Rule 404.

Your Argument: "Objection, Your Honor. Under Rule 404, the plaintiff cannot introduce evidence of prior alleged debts or financial history to prove propensity. Whether I had a dispute with a different company years ago is completely irrelevant to whether this specific plaintiff can prove I owe this specific debt to them today."

When you are representing yourself in a debt collection lawsuit, the legal terminology can feel like a foreign language. To help you navigate this process, we have broken down some of the most common questions and terms you will encounter.

Legal Term | Definition | Impact on Your Case |

|---|---|---|

Nonsuit | A motion filed by the plaintiff to voluntarily drop the lawsuit, often because they realize they lack the evidence to win. | The case ends immediately, though they may try to refile later if it is without prejudice. |

Dismissal with Prejudice | A permanent court order ending the lawsuit. The plaintiff is forever barred from suing you for this debt again. | This is the ultimate victory. The debt is legally dead. |

Dismissal without Prejudice | The court dismisses the current lawsuit, but the plaintiff is allowed to refile it later if they gather better evidence. | A temporary win. You must monitor the statute of limitations to see if they run out of time to refile. |

Default Judgment | A ruling in favor of the plaintiff because the defendant failed to respond to the lawsuit. | This allows the collector to garnish your wages and freeze your bank accounts. Avoid this at all costs! |

Conclusion

When a debt collector sues you, they are betting on your silence. They expect you to ignore the summons, skip the court dates, and allow them to walk away with an easy default judgment.

But when you know how to argue lack of evidence in a lawsuit, you flip the script. By filing a timely Answer, demanding proof of ownership, and raising sharp evidentiary objections, you expose the reality of their business model: they bought a cheap, incomplete file, and they do not have the proof to back up their claims.

You do not have to navigate this stressful process alone. At KillDebt, we built a DIY legal defense system powered by ParkerGPT—an AI trained specifically on consumer debt law and real-world courtroom strategies developed over my 30+ years as a consumer defense attorney.

Unlike generic legal templates, ParkerGPT analyzes your actual lawsuit documents, spots the exact evidentiary gaps in the plaintiff's complaint, and generates highly customized, court-ready Responses and Discovery demands tailored to Florida and Michigan rules.

And if you want to practice your defense before stepping foot in a real courtroom, we just rolled out our brand-new tool: Court Tester. Court Tester is an AI courtroom simulation built on your actual case. You upload your lawsuit filings, and within minutes, you are arguing your motion in front of an AI judge, facing AI opposing counsel, with a private AI co-counsel whispering winning strategies directly to you.

Do not let debt collectors bully you with a lawsuit they cannot prove. Take control of your case, protect your hard-earned money, and fight back.

Ready to get started? Explore our options and find the perfect plan for your defense at Get started with KillDebt pricing.

Frequently Asked Questions (FAQ)

What is the difference between a nonsuit and a dismissal?

If a debt collector realizes they do not have the documents to prove their case, they will often try to slip out of the lawsuit quietly before the judge can rule against them. They do this by filing a notice of nonsuit or a voluntary dismissal. • Nonsuit / Voluntary Dismissal Without Prejudice: The plaintiff voluntarily withdraws the lawsuit. However, because it is "without prejudice," they reserve the right to sue you again in the future for the exact same debt. They often do this to buy time to search for the missing paperwork or to sell the debt to another collector who will try to sue you again. • Dismissal With Prejudice: This means the case is permanently closed. The plaintiff cannot sue you again, and they cannot sell the debt to anyone else. If you have already filed your Answer and forced them into discovery, you should argue that any dismissal should be with prejudice. Point out to the judge that you have spent time, energy, and resources defending yourself, and the plaintiff should not get a "second bite at the apple" just because they filed a lawsuit without having their evidence ready. For a comprehensive strategy on securing a permanent dismissal, read our Fight Debt Collection Lawsuit Complete Guide.

Can a debt collector win a lawsuit without the original contract?

The short answer is: No, not if you hold them to the fire. A third-party debt buyer almost never has the original, signed physical contract. Instead, they will show up with a generic "Cardmember Agreement" printed off the internet from the year they claim you opened the account. To win without the original contract, they must prove the "chain of custody." They must show how the rights to your specific account were legally transferred from the original creditor to them. This requires signed bills of sale with specific schedules listing your account number. If they do not have these documents, you can completely dismantle their case. One of the most effective ways to do this is by filing a solid counter-affidavit. A counter-affidavit is a formal, notarized statement where you dispute their claims under oath, which legally forces them to produce the original verification documents. Learn how to execute this strategy in our guide: Key to Strong Answer in a Collection Lawsuit: Solid Counter-Affidavit.

What should I do immediately after receiving a summons?

First, do not panic. Second, look at the calendar. The moment you are served with a summons, a strict legal clock begins ticking. • In Florida: You have 20 calendar days to file your written Answer with the court and serve a copy on the plaintiff's attorney. • In Michigan: You have 21 days (if served in person) or 28 days (if served by mail). If you miss this deadline, the debt collector wins automatically through a default judgment. Many people fall victim to common myths, believing that if they ignore the papers, or if their name is spelled slightly wrong, the lawsuit isn't valid. These mistakes will cost you your bank account and your paycheck. Read more about what won't work in Debt Collection Lawsuit Myths: 7 Things That Won't Save You.