What to Do When a Credit Card Company Takes You to Court

If a credit card company taking me to court is your reality right now, here is the short version of what you need to know:

Quick Answer:

Don't ignore it. You have a deadline — usually 14 to 30 days — to respond to the summons.

Respond in writing by filing a formal defence with the court.

Know your rights. The credit card company must prove you owe the debt — and the amount.

Check the statute of limitations. In most Canadian provinces, creditors only have 2 years to sue you.

Get help fast. A Licensed Insolvency Trustee, credit counsellor, or legal aid service can guide you — often for free.

Getting a knock at the door and being handed legal papers is one of the most stressful moments a person can face. Your heart races. Your mind goes blank. You wonder: Is this really happening?

It is — but it is not the end of the world.

Credit card companies do sue for unpaid debt, but it is far less common than most people think. The reality is that less than one in 10,000 debts ever results in a lawsuit. Most creditors and collection agencies rely on fear and pressure calls rather than actual court action.

That said, if you have been served, this is not the time to freeze or ignore it. A lawsuit becomes a crisis only when you do nothing.

This guide walks you through exactly what to do — step by step — so you can protect yourself without paying a fortune in legal fees.

The Legal Process of a Credit Card Company Taking Me to Court

When a credit card issuer decides to move beyond phone calls and letters, they enter the realm of civil litigation. This doesn't happen overnight. Usually, an account must be delinquent for several months—often 180 days or more—before the legal department or a third-party debt buyer pulls the trigger on a lawsuit.

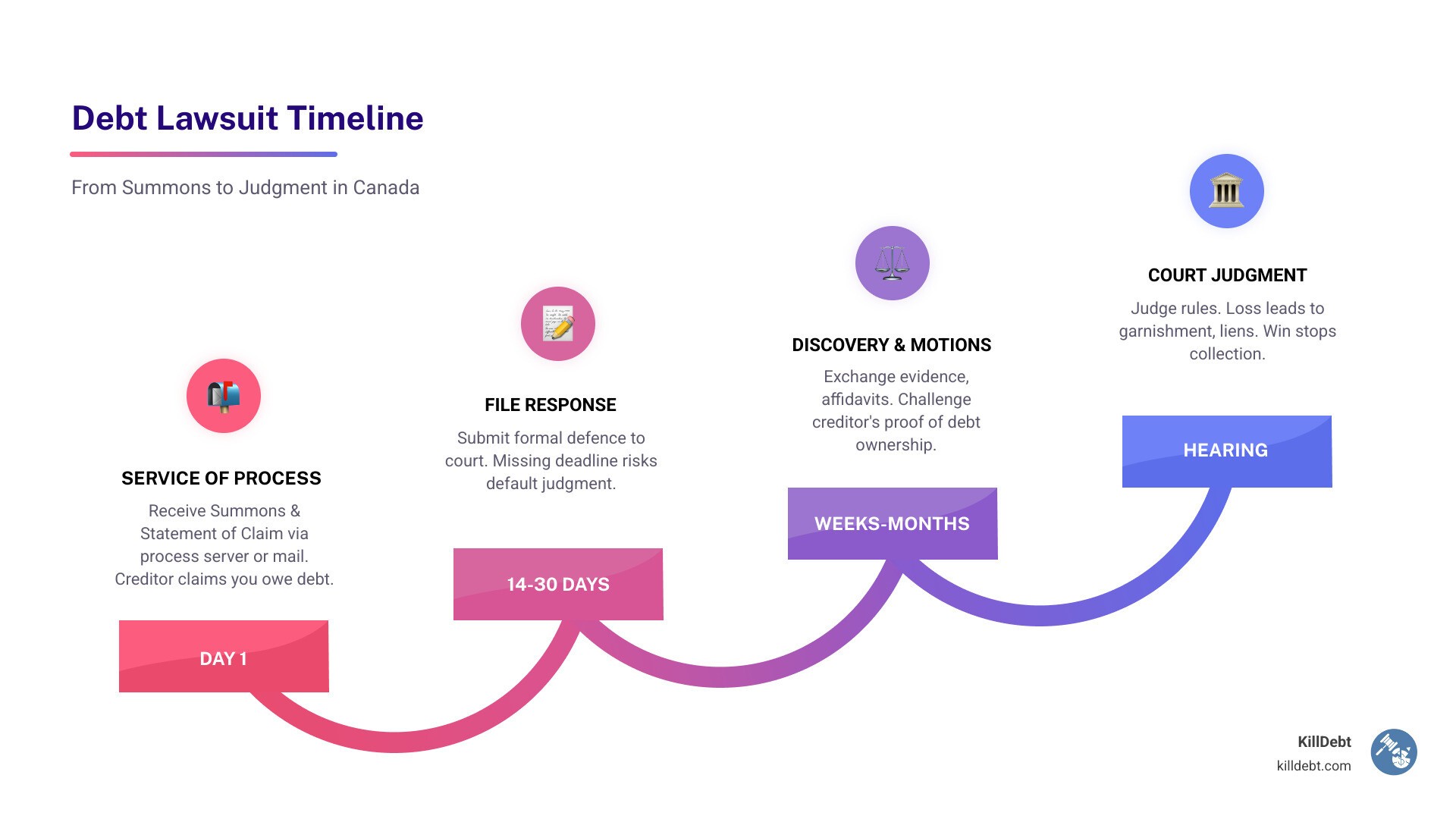

The process officially begins with the "service of process." This is when you are handed a package of legal documents, typically by a process server or via registered mail. These documents usually consist of a Summons and a Statement of Claim (or Notice of Claim).

It is vital to understand the difference between a summons and a complaint (or Statement of Claim). The Summons is the court's official notice telling you that you are being sued and providing the deadline for your response. The Statement of Claim is the document written by the credit card company’s lawyers detailing why they think you owe them money and exactly how much they are seeking.

You might be sued by the original creditor (like RBC, TD, or Scotiabank) or by a debt buyer. Debt buyers are companies that purchase portfolios of old debt for pennies on the dollar. If you don't recognize the name of the company on the papers, don't panic—it’s likely a debt buyer. Knowing who is suing you is the first step in building your defense.

If you are wondering, "Have you been sued by a debt collector?" the answer is in those papers. Look for a court seal or a court file number. If those are present, it is a real lawsuit, not just another collection letter.

How to Respond to a Summons and Statement of Claim

The single biggest mistake we see people make is doing nothing. In the legal world, silence is considered a "confession." If you do not respond, the credit card company will ask the judge for a default judgment. This means they win automatically, and they can start taking your money without further warning.

The 20-Day Window

In many jurisdictions, such as Ontario, you have a strict 20-day window to file your response. Other provinces may offer 14 to 30 days. This time to respond to a debt collection lawsuit is your most precious resource.

Filing a Defence

To stop the default judgment, you must file a "Statement of Defence." This is a formal document where you address the allegations made in the Statement of Claim. You don't need to be a lawyer to do this, but you do need to be precise. You can admit to parts of the debt that are true, but you should dispute anything that is incorrect, such as the interest calculations or the total balance.

Following a complete first steps guide ensures you don't miss technical requirements like "serving" the plaintiff (the credit card company) with a copy of your response before filing it with the court.

Legal Defenses and Provincial Statutes of Limitations

When a credit card company taking me to court becomes a reality, you aren't defenseless. The law requires the creditor to meet the burden of proof. They must prove that the debt is yours, that they have the legal right to collect it, and that the amount is accurate.

One of your strongest tools is debt validation. You have the right to demand original contracts and a full accounting of how the balance was calculated. If the creditor is a debt buyer, they often lack the original paperwork, which can lead to the case being dismissed.

Provincial Statutes of Limitations

The "statute of limitations" is a law that sets a deadline for how long a creditor has to sue you. In most Canadian provinces, this clock starts from the date of your last payment or the last time you acknowledged the debt in writing.

Province/Territory | Statute of Limitations (Years) |

|---|---|

Alberta, BC, Ontario, Saskatchewan, New Brunswick, Nova Scotia | 2 Years |

Quebec | 3 Years |

Manitoba, Newfoundland, PEI, Yukon, NWT, Nunavut | 6 Years |

If the debt is older than these timeframes, it is "time-barred." This is a powerful defense in a debt collection case. However, the court won't check this for you—you must raise it in your Statement of Defence.

Common Defenses Against a Credit Card Company Taking Me to Court

Time-Barred Debt: The statute of limitations has expired.

Incorrect Amount: The creditor added illegal fees or miscalculated interest.

Identity Theft: You never opened the account or authorized the charges.

Lack of Standing: The company suing you hasn't proven they actually own the debt.

Bankruptcy/Proposal: You have already discharged the debt through a legal insolvency process.

Proving these defenses often requires filing a counter-affidavit, which is a sworn statement where you present your version of the facts.

Potential Consequences of Losing the Lawsuit

If you ignore the lawsuit or lose in court, the creditor receives a "Judgment." This is a court order that turns an unsecured credit card debt into a powerful legal weapon.

A judgment creditor has several ways to collect:

Wage Garnishment: They can contact your employer and take a portion of your paycheck before you even see it.

Bank Freeze: They can "levy" your bank account, meaning the bank freezes your funds and sends them to the creditor.

Property Liens: They can place a lien on your home, preventing you from selling or refinancing until the debt is paid.

Consequences of a Credit Card Company Taking Me to Court and Winning

The financial impact is severe. In many provinces, a creditor can garnish up to 30% of your gross income. Furthermore, a judgment will stay on your credit report for 6 to 10 years, making it nearly impossible to get a mortgage, car loan, or even a new apartment. This is why understanding the consequences is so important—it’s not just about the money; it’s about your future.

Exploring Resolution Options to Stop Legal Action

Even if you've been served, it is rarely too late to settle. Credit card companies don't actually want to go to trial; trials are expensive and time-consuming.

If you are in a position where the credit card company sues you and you have no money, you might be what lawyers call "judgment proof." This means you have no seizable assets or garnishable income (like Social Security or certain disability benefits).

Settlement Possibilities

You can often settle a debt for 30% to 60% of the total balance if you can offer a lump sum. If you negotiate a settlement, always get it in writing before sending a single penny. A verbal promise from a collector is worth nothing in court.

Debt Relief to Stop Lawsuits

If the lawsuit is for a large amount and you have other debts, a Consumer Proposal or Bankruptcy provides an "Automatic Stay of Proceedings." This is a federal law that forces the credit card company to stop the lawsuit immediately—even if they were about to garnish your wages the next day.

Conclusion

Facing a credit card company taking me to court is a heavy burden, but you don't have to carry it alone or spend thousands on a lawyer. At KillDebt, we believe that every consumer deserves a fair fight.

Our DIY legal defense system is powered by ParkerGPT, an AI trained specifically on consumer debt law and real-world court strategies developed over 30 years by attorney Brian Parker. We provide you with the tools to analyze lawsuit documents, identify creditor weaknesses, and generate court-ready responses.

Want to see how you'd fare in front of a judge? Our new Court Tester allows you to simulate your hearing. You can argue your motion against an AI opposing counsel while a private AI co-counsel whispers the winning strategy in your ear.

Don't let a default judgment ruin your financial future. Protect your finances and fight back against credit card lawsuits today. We are here to help you turn the tables on debt collectors and reclaim your peace of mind.

Frequently Asked Questions (FAQ)

Can I go to jail for not paying credit card debt in Canada?

No. There is no "debtor's prison" in Canada. You cannot be arrested for being unable to pay a credit card bill. If a collector threatens you with jail time, they are violating provincial consumer protection laws and the federal prohibited practices.

What is the minimum amount a credit card company will sue for?

There is no hard rule, but most companies won't sue for less than $1,000 to $2,000 because the legal fees would outweigh the recovery. However, in Small Claims Court (which handles debts up to $35,000 in Ontario), it is much cheaper for them to sue, so they may pursue smaller amounts.

Can I settle the debt after the lawsuit has already started?

Absolutely. In fact, filing a Statement of Defence often gives you more leverage to settle because the creditor realizes you are going to make them work for the money. Many cases are settled on the courthouse steps or during a mandatory settlement conference.