What You Need to Know About Local Court Debt Recovery Right Now

Local court debt recovery is the legal process creditors use to sue you for an unpaid debt — and if you've just received a summons, a Statement of Claim, or a collection letter with a court deadline, you're in the right place.

Here's what you need to know fast:

You typically have 14–30 days to respond to a debt lawsuit (varies by state/jurisdiction)

If you do nothing, the court can enter a default judgment against you — allowing wage garnishment, bank levies, and property liens

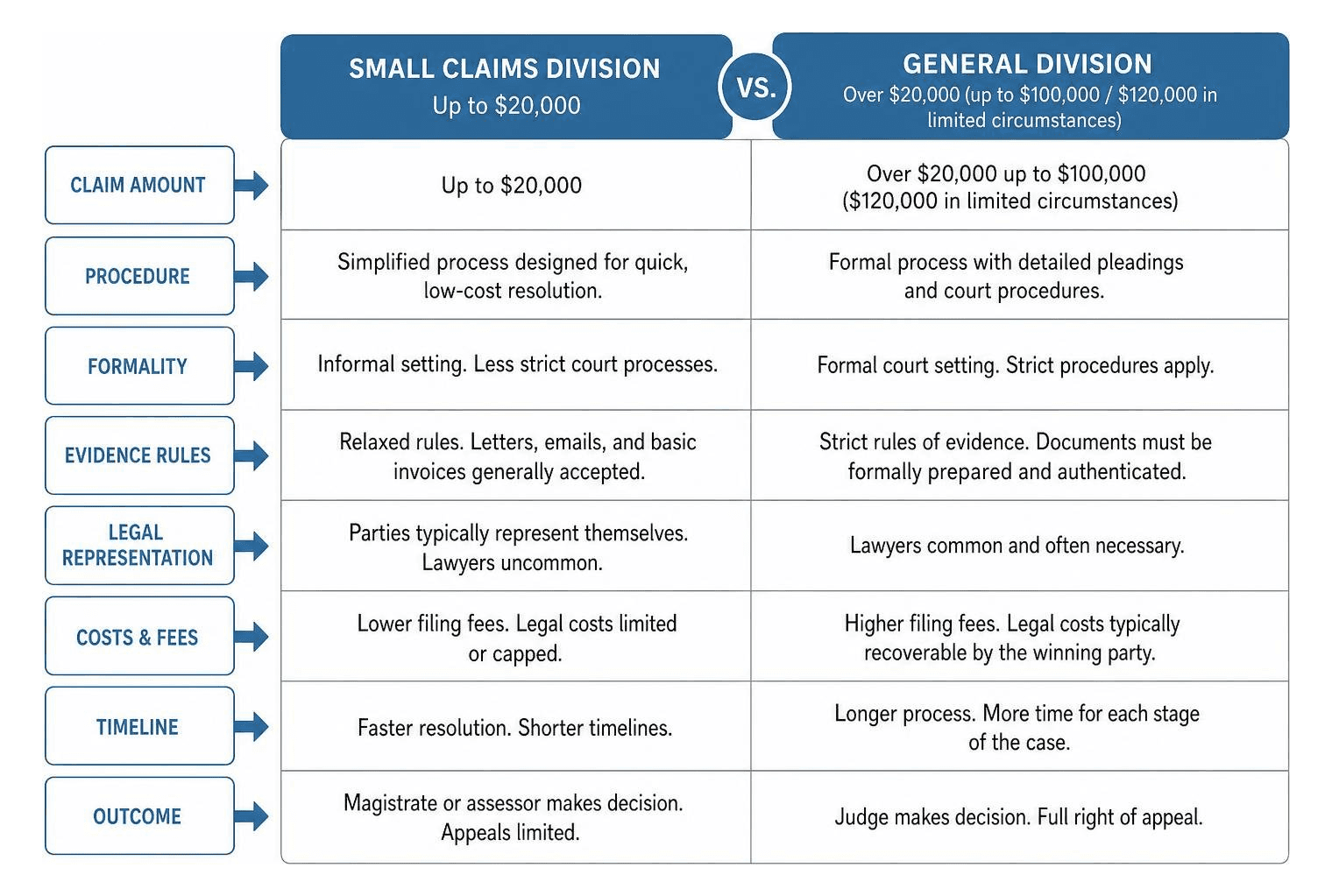

In NSW, debts under $20,000 go to the Small Claims Division; debts over $20,000 go to the General Division of the Local Court

The time limit to sue for a debt is generally 6 years from the last payment, the date the debt was owed, or the last written acknowledgment — whichever is latest

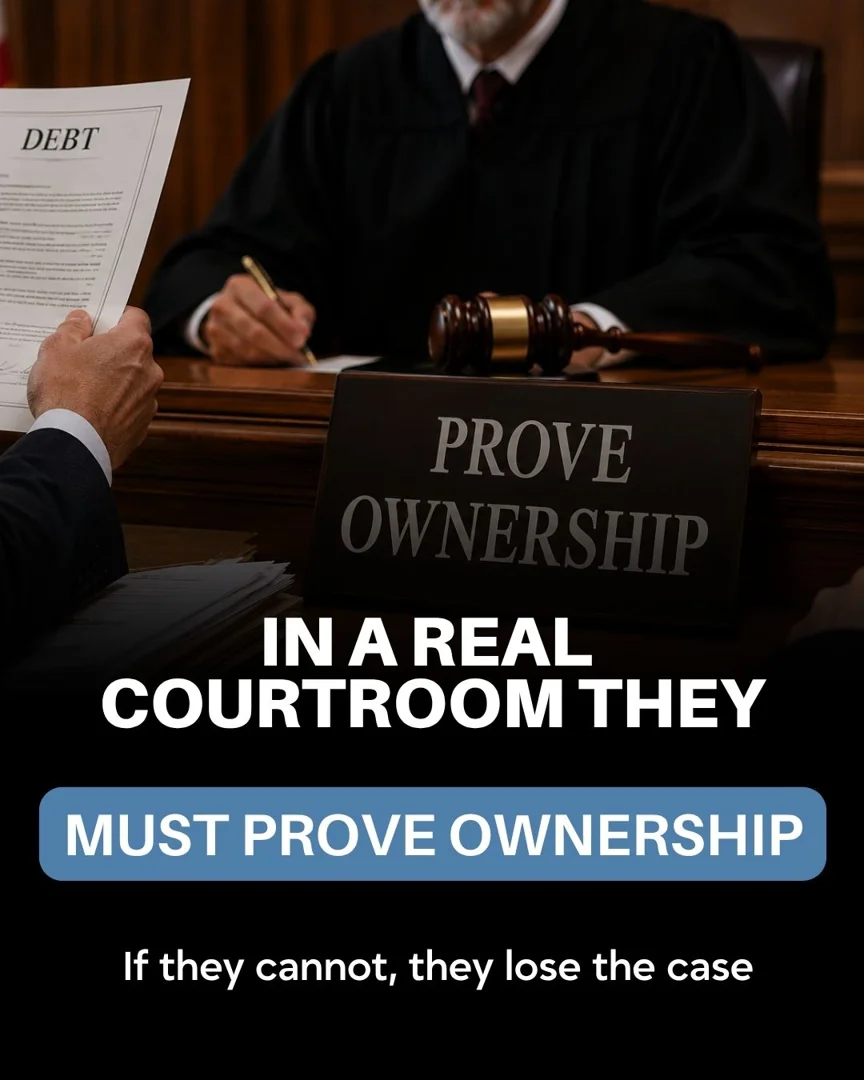

Debt collectors must prove they own the debt, that you owe it, and that the amount is accurate — they don't always succeed

The court process can feel overwhelming — unfamiliar forms, strict deadlines, and legal language designed for lawyers, not regular people. But knowing the rules gives you real power to fight back.

I'm Brian Parker, and for over 30 years I've defended consumers against creditors, debt buyers, and collection law firms in courts across the country — including countless local court debt recovery cases just like yours. At KillDebt, I've turned that experience into tools and guides that put you on equal footing without the high cost of an attorney.

Understanding Local Court Debt Recovery: Small Claims vs. General Divisions

When a creditor or a third-party debt buyer decides to pursue a local court debt recovery lawsuit, the case is channeled into a specific division of the local court system based on the amount of money being claimed. Understanding which division handles your case is critical because the rules of evidence, filing fees, and the overall level of formality vary dramatically.

In jurisdictions like New South Wales (NSW), the Local Court is split into two primary divisions: the Small Claims Division and the General Division.

Small Claims Division: This division handles simpler, smaller disputes. If the debt is up to $20,000, the case proceeds here.

General Division: If the debt exceeds $20,000 (and goes up to $100,000, or $120,000 in limited circumstances), the case must be filed in the General Division.

While these specific thresholds are set in Australia, we see highly comparable structures in the United States, particularly in our primary service areas of Michigan and Florida. For instance, in Michigan, small claims are handled with highly relaxed rules, whereas the District Court handles formal civil cases up to $25,000, and Circuit Courts handle larger claims.

Understanding these thresholds is the first step in building your defense. If a creditor files in the wrong division or attempts to use formal court procedures for a minor claim, you can use that procedural misstep to your advantage.

Small Claims Division Limits and Procedures

The Small Claims Division is specifically designed to resolve disputes quickly and cheaply. If the debt is under $20,000, the court encourages an informal atmosphere where parties often represent themselves.

In this division, strict rules of evidence do not apply. The magistrate or assessor can review letters, emails, and basic invoices without requiring the formal, complex authentication processes needed in higher courts. Legal costs are heavily restricted or capped, meaning that even if you lose, you are generally not forced to pay thousands of dollars of the creditor's attorney fees.

To see how these minor civil procedures are structured, you can read the guide on How to Recover a Debt, which outlines the simplified steps used to resolve smaller claims without the heavy burden of formal trial procedures.

General Division and Formal Local Court Debt Recovery

Once a debt claim crosses the $20,000 threshold, the gloves come off. The case enters the General Division of the Local Court, where the environment is highly formal and the stakes are much higher.

In the General Division:

Formal rules of evidence apply strictly. You cannot simply hand a judge a printout of an email; it must be properly admitted under the rules.

Written witness statements and detailed affidavit evidence must be prepared and formally exchanged.

Legal costs are not capped. The general rule in the General Division is that the losing party pays the winning party’s legal costs, which can easily climb into thousands of dollars.

Because of this complexity, representing yourself in the General Division without proper guidance is highly risky. If you are facing a formal lawsuit in Michigan, for example, our detailed breakdown of Michigan Court Debt Cases explains how these district and circuit court dynamics function and what you must do to protect your bank accounts.

Global Jurisdictional Variations: US vs. Australia

While the terminology differs, local court debt recovery processes share striking similarities across the globe. Whether you are dealing with a local court in Sydney or a county court in Florida, the core battle remains the same: the creditor must prove you owe the money, and you must assert your legal rights.

In the United States, different states set their own unique boundaries for small claims and formal civil debt collection:

Alaska: Small claims are limited to $10,000, with filing fees ranging from $50 to $100. Formal civil cases go to the District Court (up to $100,000) or Superior Court (over $100,000).

Maine: Small claims are capped at $6,000. In recent years, Maine has shifted many debt collection cases into the regular District Court to allow for a more formal process where consumers can better raise defenses.

Virginia: The small claims division of the general district court hears cases up to $5,000.

For a closer look at how these international and state-level jurisdictions manage debt petitions, you can review the official information sheet on DEBT CLAIM CASES to understand how courts require specific documentation before a creditor can secure a judgment.

Step-by-Step Court Process for Debt Recovery Cases

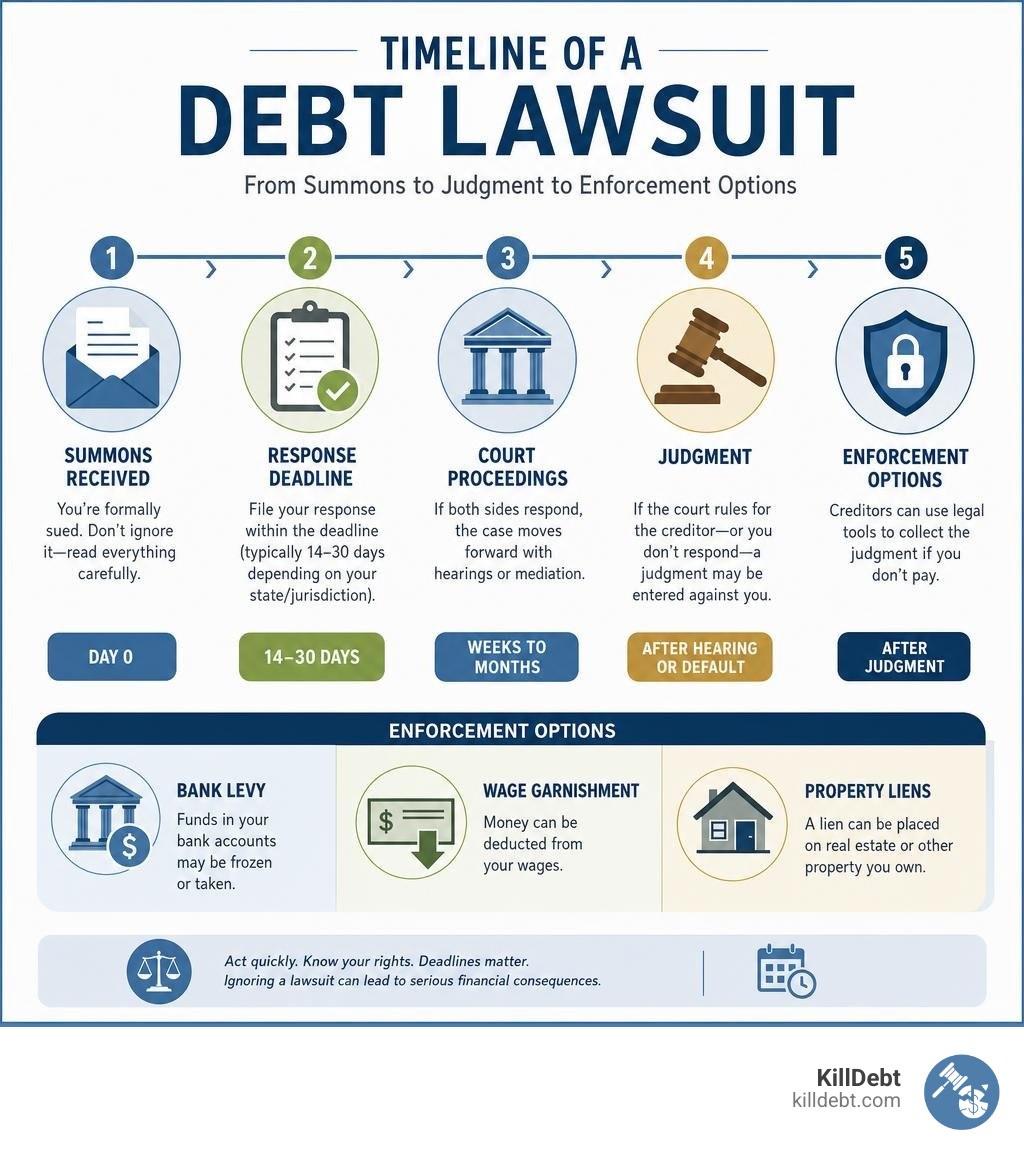

A debt recovery lawsuit does not happen overnight. It follows a structured, step-by-step legal process. If you ignore any of these steps, you hand the debt collector an easy victory. Let's break down exactly how a case moves through the local court system so you know what to expect.

Filing and Serving the Statement of Claim

The lawsuit officially begins when the plaintiff (the creditor or debt collector) files a Statement of Claim (or a Complaint in US jurisdictions) with the court and pays the required filing fee.

Once filed, the document must be properly served on you, the defendant. Proper service is not just a courtesy; it is a constitutional and legal requirement. The plaintiff must typically serve you in one of the following ways:

Personal Service: Handing the documents directly to you.

Substituted Service: If they can prove they made diligent efforts to find you but failed, they can apply to the court to serve you via post, email, or by leaving the papers with an adult at your home or workplace.

Once you are served, the clock starts ticking. In NSW, you have exactly 28 days to file a response (a Defence). In US jurisdictions like Oregon or Florida, the window is often 20 to 30 days. If you fail to file a written response within this window, the plaintiff can immediately apply for a default judgment.

If you are dealing with a small claims matter in Virginia, you might see a specific document structure. You can learn more about this by reviewing Using This Revisable PDF Form, which demonstrates how formal warrants are drafted and served on consumers.

Directions Call-Over, Review, and the Hearing

If you file a Defence, the court will schedule a directions call-over (often within six weeks of the Defence being filed). The call-over is a short court appearance where the registrar or magistrate decides how the case will proceed. The court might:

Refer the case to mediation or arbitration to encourage a settlement.

Set a timeline for the exchange of evidence.

Schedule a second directions call-over or a review date.

If the matter is not settled, it will be set down for a formal hearing. At least four weeks before the review date, you will be directed to exchange written witness statements or affidavit evidence with the other side.

At the final hearing, both parties present their arguments, question witnesses under oath, and submit physical evidence. The magistrate will then make a final decision and enter a judgment.

Appeals and Post-Judgment Enforcement Options

If you lose the case, or if a default judgment is entered against you, the creditor gains powerful legal tools to collect the money. However, you still have options.

If the magistrate made a legal error, you can appeal the decision to a higher court (such as the Supreme Court in NSW) within 28 days. If you do not appeal, or if the appeal is unsuccessful, the creditor can enforce the judgment using several methods:

Garnishee Orders / Wage Garnishment: Ordering your employer or bank to pay a portion of your wages or account balance directly to the creditor.

Writ of Execution / Seizure of Property: Authorizing a sheriff or court officer to seize and sell your non-exempt assets to pay the debt.

Judgment Liens: Placing a lien on your home, preventing you from selling or refinancing without paying the debt.

For a detailed look at how these enforcement mechanisms operate internationally, see Courts.ie - Enforcement of debt Judgments. If a judgment has already been entered against you and you want to understand the creditor's next steps, read our guide on Won a Judgement How to Collect.

Strategies for Defending Against a Debt Lawsuit

Many consumers assume that if they owe the money, they have no defense. This is a costly mistake. In a local court debt recovery lawsuit, the burden of proof is entirely on the plaintiff. They must prove every element of their case with admissible evidence. If they cannot, the court must dismiss the case.

When defending yourself, you must force the plaintiff to prove their standing to sue and the accuracy of their numbers. For a comprehensive roadmap on how to construct a strong defense in court, read our Michigan Court Defense Guide.

How to Defend Against a Local Court Debt Recovery Lawsuit

The strategy you use depends heavily on whether you are being sued by the original creditor (like your credit card company) or a third-party debt buyer (a company that bought your old debt for pennies on the dollar).

Debt buyers purchase thousands of old accounts in bulk. During these bulk transactions, critical documentation is often lost or never transferred. To win a lawsuit, a debt buyer must prove:

Chain of Title: They must show a complete, uninterrupted chain of ownership transfers from the original creditor down to them. If they are missing a single assignment agreement, they lack the legal standing to sue you.

The Exact Amount: They must prove the principal, interest, and fees were calculated correctly according to the original contract. They cannot simply make up a number or rely on a single summary sheet.

By demanding that the debt buyer produce the original contract, the complete chain of title, and the itemized billing statements, you expose the weaknesses in their case. Often, they will choose to dismiss the lawsuit rather than spend the time and money trying to locate these documents.

Asserting Affirmative Defenses and Protecting Exempt Assets

An affirmative defense is a legal reason why the plaintiff cannot win, even if the allegations in their complaint are true.

The most powerful affirmative defense in debt collection is the statute of limitations. In NSW, Michigan, and Florida, the time limit to start a court case to recover a debt is generally six years from when the money became owed, the last repayment was made, or the debt was last acknowledged in writing (whichever came last). If the creditor waits too long to sue, the debt becomes legally unenforceable.

If you lose the lawsuit, you must focus on protecting your exempt assets. Under the law, certain income and property are protected from creditors:

Exempt Earnings: In many jurisdictions, a certain portion of your weekly take-home pay is safe from garnishment (for example, in Maine, up to $604 per week or 75% of your disposable earnings is exempt).

Government Benefits: Social Security, disability, and unemployment benefits are generally completely protected from debt collectors.

Home and Vehicle Equity: Homestead exemptions protect a specific amount of equity in your primary home and personal vehicle.

Conclusion

Facing a local court debt recovery lawsuit is stressful, but you do not have to navigate the court system alone. At KillDebt, we believe that every consumer deserves access to a powerful, affordable defense.

That is why we created ParkerGPT, an AI legal defense system trained on real-world court strategies developed over 30+ years by experienced consumer defense attorneys. ParkerGPT analyzes your lawsuit documents, spots critical weaknesses in the collector's evidence, and generates custom, court-ready responses with step-by-step instructions.

To help you feel completely prepared before you step into a courtroom, we recently rolled out our brand-new Court Tester. Court Tester is an advanced AI courtroom simulation built directly on the facts of your actual case. You simply upload your real court filings, and within minutes, you are arguing your motion in front of an AI judge, facing off against an AI opposing counsel, while a private AI co-counsel whispers winning strategies that only you can see.

Don't let debt collectors take your hard-earned money by default. Take control of your case, analyze your documents, and build a winning defense today. Explore our plans and start your defense journey at the KillDebt DIY Legal Defense portal.

Get started with KillDebt pricing

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments.

Frequently Asked Questions (FAQ)

What is the statute of limitations for recovering a debt in court?

The statute of limitations is the legal deadline for a creditor to file a lawsuit against you. In most local court jurisdictions, including NSW, Michigan, and Florida, this limit is six years. The clock restarts if you make a partial payment or acknowledge the debt in writing. Once this six-year period expires, the debt is considered "time-barred," and you can use this as an absolute defense to have the lawsuit dismissed.

What happens if I ignore a court summons or Statement of Claim?

If you ignore a court summons, you lose by default. The plaintiff will ask the court for a default judgment. Once the judge signs this judgment, the creditor can immediately begin aggressive collection tactics, including freezing your bank accounts, garnishing your wages, and placing liens on your real estate. Never ignore a court date; even a simple response buys you time to negotiate.

Can I recover my legal costs if I win the case?

In the Small Claims Division, legal costs are generally not recoverable, meaning each party pays their own lawyer. However, in the General Division of the Local Court, the court has broad discretion, and the general rule is that the losing party pays the winning party's legal costs. If you successfully defend a claim in the General Division, you can ask the court to order the creditor to pay your legal expenses.