What to Do When You're Facing a Debt Lawsuit (And the Clock Is Ticking)

A strong court debt defense strategy can mean the difference between a dismissed case and a wage garnishment that drains your paycheck before you even see it.

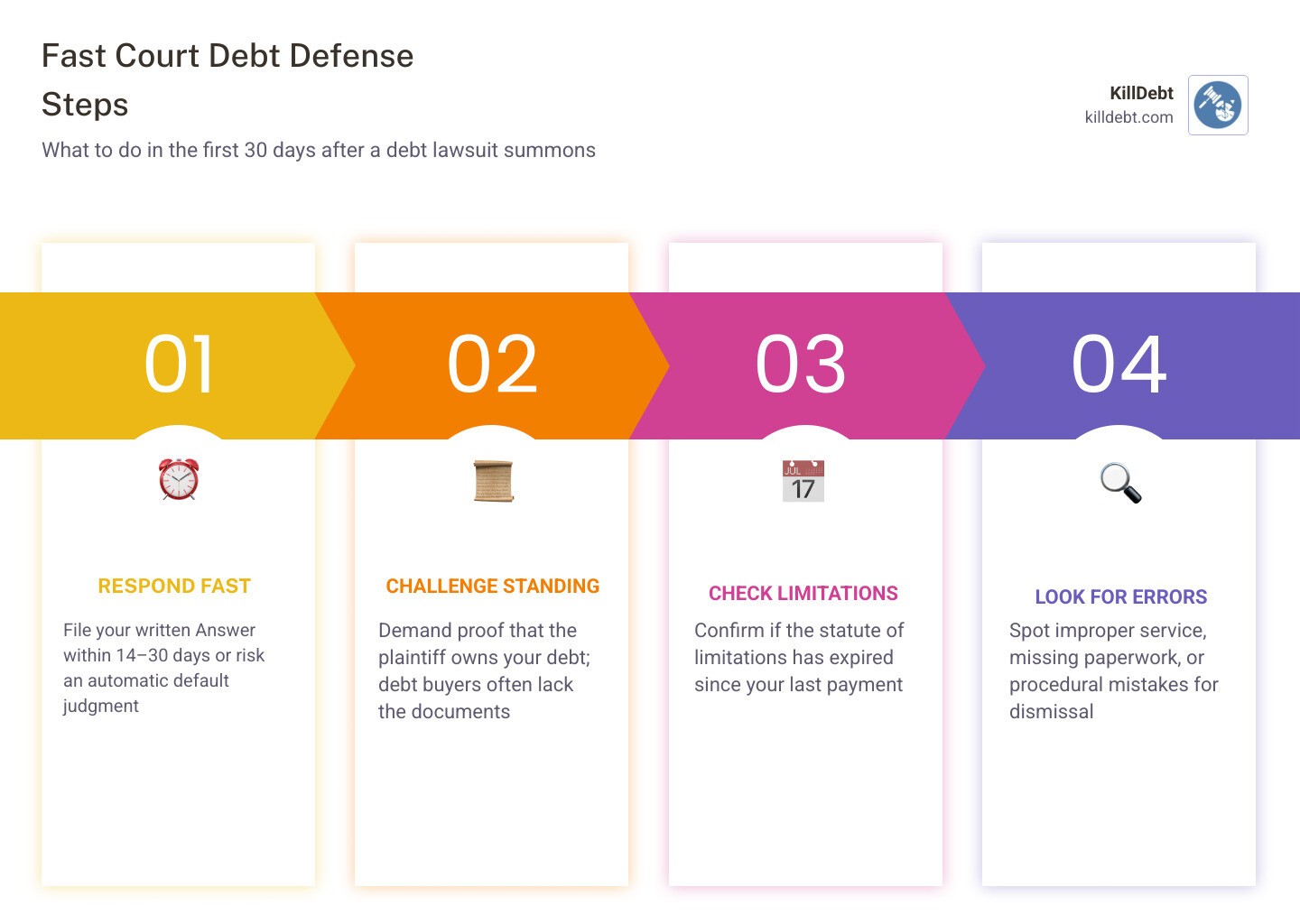

If you just got served, here's what matters most - fast:

Quick Answer: Core Court Debt Defense Strategies

Respond before the deadline - You typically have 14 to 30 days to file a written Answer. Miss it and the court can rule against you automatically.

Challenge standing - Demand proof that the plaintiff actually owns your debt. Debt buyers often can't produce it.

Check the statute of limitations - If too much time has passed since your last payment, the lawsuit may be invalid.

Look for procedural errors - Improper service, missing documentation, or filing mistakes can get a case dismissed.

Consider settlement - If documentation is weak, a negotiated settlement at 40-60% of the balance may be smarter than trial.

Never ignore it - Up to 90% of people don't respond to debt lawsuits, and almost all of them lose by default.

Getting served with a lawsuit is scary. But here's the thing: most debt lawsuits have real weaknesses. Debt buyers often purchase old accounts for pennies on the dollar - and the paperwork they get with those accounts is frequently incomplete, inaccurate, or missing entirely. That gives you more leverage than you might think.

I'm Brian Parker, founder of KillDebt, and I've spent over 30 years in the courtroom going up against creditors, debt buyers, and collection law firms - building and testing court debt defense strategies that actually work for real people. This guide distills that experience into clear, actionable steps you can use right now.

Immediate Steps After Receiving a Summons

When that thick envelope lands on your doorstep in May 2026, the adrenaline spike is real. But once you catch your breath, you need to look at the calendar. In debt defense, time is your most precious resource—and your biggest enemy if you waste it.

In Florida and Michigan, the clock starts ticking the moment you are served. Depending on the court and the state, you generally have between 21 and 30 days to file a formal, written Answer. If you miss this window, the plaintiff (the person suing you) will likely file for a default judgment.

A default judgment is essentially a "forfeit" win for the debt collector. With that piece of paper, they can:

Garnish your wages: Taking a chunk of your paycheck before it hits your bank account.

Freeze your bank accounts: Leaving you unable to pay rent or buy groceries.

Place liens on your property: Making it impossible to sell your home or car without paying them first.

Your first seven days are critical. You need to read the summons and complaint carefully. Who is suing you? Is it the original creditor (like Chase or Citibank) or a debt buyer you've never heard of? What is the exact amount they claim you owe? For a detailed breakdown of these first moves, check out our What to Do When Sued by a Debt Collector: Complete First Steps Guide and our roadmap for Sued for a Debt? Here’s Exactly What to Do in the First 7 Days.

Developing Your Court Debt Defense Strategy

Developing a court debt defense strategy isn't about "getting out" of a debt you legitimately owe; it's about holding the plaintiff to the legal standard required by the court. In a civil lawsuit, the burden of proof lies entirely with the plaintiff. They must prove that the debt is yours, the amount is correct, and they have the legal right to collect it.

One of the most effective ways to fight back is through affirmative defenses. These are facts or legal arguments that, if proven, can defeat the plaintiff's claim even if everything they said in the complaint is true. Common defenses include:

Statute of limitations: The debt is too old to sue over.

Lack of standing: The plaintiff doesn't own the debt.

Improper service: You weren't served the lawsuit correctly according to state law.

Identity theft: You didn't open the account or authorize the charges.

You should also look for violations of the Fair Debt Collection Practices Act (FDCPA). If the collector harassed you, called at illegal hours, or lied about the debt, you might even have a counterclaim. For more on these concepts, see Common Defenses in a Consumer Debt Case | NY CourtHelp and our comprehensive Debt Lawsuit Defense Guide.

Challenging Standing and Debt Ownership as a Court Debt Defense Strategy

This is often the "silver bullet" in a court debt defense strategy. Most debt lawsuits today are filed by third-party debt buyers. These companies buy "portfolios" of defaulted debt for pennies on the dollar.

The problem? They often receive very little documentation. To win, they must prove a clear chain of title. This means they must show a paper trail from the original creditor to every middleman, ending with them. If there is a gap in that trail—if they are missing a single "Assignment of Debt" document—they may lack the legal standing to sue you.

When you file your Answer, you should demand to see the original contract and the full chain of assignment records. If they can't produce these, you can move to have the case dismissed. Using Debt Validation Letters: Your First Line of Defense Against Collectors early on can also help flush out these weaknesses before you even reach the courtroom.

Using the Statute of Limitations as a Court Debt Defense Strategy

A "Zombie Lawsuit" is a case filed on a debt that is so old it should be dead. Every state has a statute of limitations, which is the time limit a creditor has to sue you.

Florida: Generally 5 years for a written contract.

Michigan: Generally 6 years for most contract and debt claims.

The clock usually starts from the date of your last payment or the date the account went into default. If a debt buyer sues you after this period has expired, the debt is "time-barred." However, the court won't automatically dismiss it for you—you must raise the statute of limitations as an affirmative defense in your Answer. If you don't, you waive that right.

Be careful: in some states, making even a $5 payment or promising to pay can "restart" the clock. This is why we tell people never to pay a cent until they’ve verified the age of the debt. Learn more about killing these old debts in our guide on How to Win a Zombie Lawsuit.

Procedural Defenses and the Discovery Process

Sometimes, a case can be won on technicalities before you ever argue about the money. Procedural defenses focus on the "how" of the lawsuit. For example, did the process server actually hand you the papers, or did they just throw them in your bushes? Improper service is a valid reason to file a motion to dismiss.

Once the initial Answer is filed, you enter the discovery process. This is the formal exchange of information. You have the right to send:

Interrogatories: Written questions the plaintiff must answer under oath.

Requests for Production: Demands for specific documents (like the original signed agreement).

Requests for Admission: Statements the plaintiff must either admit or deny.

Discovery is where most debt buyers' cases fall apart. When they realize they have to spend time and money digging up old records they don't have, they often choose to dismiss the case or offer a very low settlement. To strengthen your position during this phase, consider filing a Key to Strong Answer in a Collection Lawsuit: Solid Counter-Affidavit. If you are in Michigan, the Going to Court to Defend a Debt Collection Case | Michigan Legal Help resource offers excellent local procedural guidance.

When to Fight vs. When to Settle

Not every case needs to go to trial. Sometimes, the most effective court debt defense strategy is a strategic retreat—also known as a settlement.

If the plaintiff actually has the documentation and the debt is within the statute of limitations, fighting to the bitter end might just result in you paying the full debt plus their attorney fees. In these cases, mediation can be a godsend. Mediation is a confidential meeting where a neutral third party helps both sides reach an agreement.

Common settlement outcomes include:

Lump-sum settlement: Offering a single payment, often ranging from 40% to 60% of the total balance, in exchange for the lawsuit being dismissed with prejudice.

Payment plans: A structured schedule to pay back a portion of the debt over time.

Before you agree to anything, ensure the agreement is in writing and states that the lawsuit will be dismissed and the debt considered "satisfied in full." For a deeper dive into these choices, see our Fight Debt Collection Lawsuit: Complete Guide.

Identity Theft and Mistaken Identity

If the debt isn't yours, you shouldn't pay a dime. Mistaken identity happens more often than you'd think—especially if you have a common name or a relative with a similar name. Identity theft is even more common, with 45% of families carrying credit card debt and millions of records exposed in data breaches every year.

If you are being sued for a debt resulting from fraud:

File a police report: This is your primary evidence.

Affidavit of Fraud: Provide a sworn statement explaining that you did not open the account.

Unauthorized user status: If you were just an authorized user on someone else's account, you are generally not legally responsible for the debt.

You can find templates for these responses in our Sample Answer to Debt Collection Lawsuit. If the lawsuit involves a vehicle, our Auto Repossession Debt Suit Defense guide covers specific protections for car loans.

Conclusion

Facing a debt lawsuit in May 2026 doesn't have to mean financial ruin. Whether you are in Florida or Michigan, the law provides you with protections—but you have to be the one to claim them. By responding on time, challenging the plaintiff's evidence, and understanding your rights, you take the power away from the debt collector and put it back in your hands.

At KillDebt, we believe that everyone deserves a fair fight. That’s why we built ParkerGPT, an AI legal defense system trained on the real-world strategies of attorney Brian Parker. We don't just give you templates; we provide a DIY system that analyzes your specific lawsuit, identifies the exact weaknesses in the collector's case, and generates court-ready documents.

Want to see how you'd do in court before you actually go? Our brand new Court Tester tool allows you to upload your filings and practice your arguments against an AI judge and opposing counsel. It’s like having a private co-counsel whispering the winning strategy in your ear.

Don't let a debt collector dictate your future. Take control of your case at KillDebt and start building your defense today.

Frequently Asked Questions (FAQ)

What happens if I ignore the lawsuit?

Ignoring a lawsuit is the single biggest mistake you can make. Roughly 90% of people fail to respond to debt lawsuits, leading to an automatic win for the collector via default judgment. Once they have that judgment, they can seize assets, place liens on your home, and garnish your wages for years to come. In many states, these judgments can be renewed, meaning the debt could follow you for 20 years or more.

Can I defend myself without a lawyer?

Yes. This is called pro se representation. While the legal system can be intimidating, debt collection cases are often straightforward enough for consumers to handle themselves—provided they have the right tools. The key is following court rules and meeting every deadline. Procedural mistakes (like failing to serve the plaintiff's attorney with a copy of your Answer) are the most common reasons pro se defendants lose.

What are common invalid defenses to avoid?

The court operates on law, not emotion. While your situation may be heartbreaking, the following are generally not legal defenses: • Financial hardship: "I lost my job and can't afford to pay" doesn't mean you don't legally owe the money. • Intent to pay: "I was planning to pay it back next month" is not a defense against a current claim. • Unawareness of debt: "I forgot I had this credit card" doesn't invalidate the contract. • Moral obligation: "I'm a good person" won't stop a judge from signing a judgment. Focus your court debt defense strategy on documentation, standing, and the law.