Understanding the Role of a Collection Agency for Court Fines

When you fail to pay a court-ordered obligation, the court doesn't just forget about it. Most court systems are not set up to act as long-term billing departments. Instead, they partner with a collection agency for court fines to handle the heavy lifting of tracking down payments.

In Florida and Michigan, courts have specific protocols for these referrals. For instance, the 36th District Court in Detroit takes an incredibly active approach. They utilize a mix of internal enforcement officers and external agencies like Linebarger, Goggan, Blair & Sampson, LLP to ensure delinquent cases are resolved.

Typically, there is a "grace period" before your name hits a collector's desk. While this varies by jurisdiction, many systems follow a 90-day or 180-day threshold. If you haven't paid or set up a payment plan within that window, the court "disposes" of the case by sending it to collections.

It is vital to understand the Difference Between Summons & Complaint in Debt Collection Lawsuit. While a standard debt collector might sue you in civil court, a collection agency for court fines is often working under a government contract, meaning they have the "teeth" of the state behind them from day one.

The High Cost of Delay: Fees and Penalties

The most painful part of having your debt referred to a collection agency for court fines is the immediate "markup." These agencies don't work for free; their fee is usually passed directly to you as a surcharge on top of your existing fine.

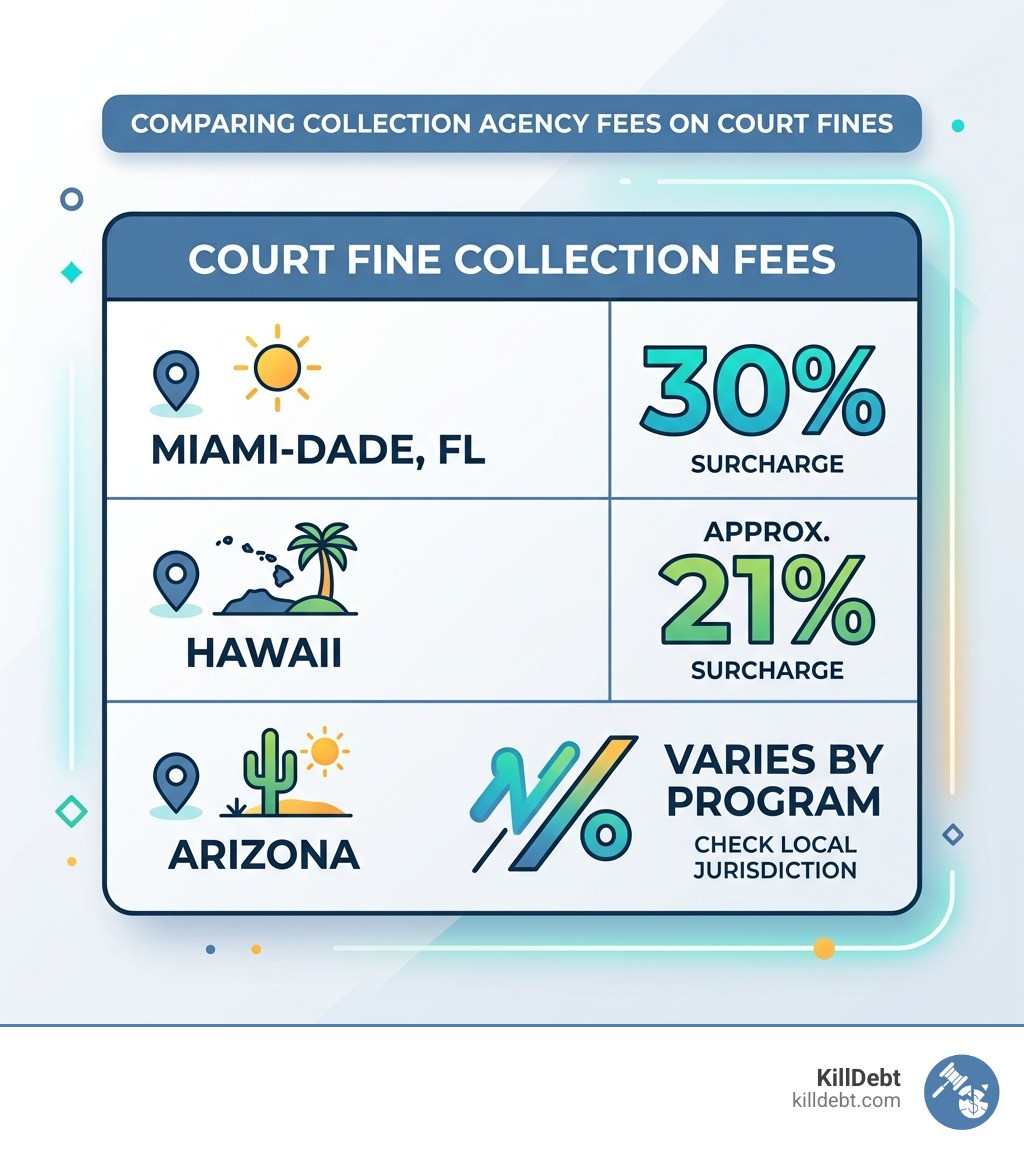

In Florida, specifically within the Miami-Dade Clerk of Courts system, the law allows for a staggering 30 percent surcharge to be added to the balance once it is referred to collections. If you owed $500, you now owe $650. In other regions, such as Hawaii, the fee is approximately 21%.

Beyond the flat percentage fees, interest may continue to accrue. If a civil judgment was entered against you for these costs, that judgment can stay on your record for decades, quietly damaging your credit and preventing you from making major purchases like a home or car. You might also wonder, Can Debt Collectors Take My Wages and Bank Account? When it comes to court debt, the answer is a resounding yes. Governments have "super-powers" that private credit card companies don't—they can often garnish your wages or seize bank funds with far less red tape.

How to Resolve Your Unpaid Court Debt

If you’ve discovered your case is in collections, don't panic, but do act fast. The goal is to stop the bleeding—meaning stopping the accumulation of interest and preventing further enforcement actions like license suspensions.

The first step is always verification. You need to ensure the amount they claim you owe is accurate. We always recommend sending Debt Validation Letters: Your First Line of Defense Against Collectors. Even with government debt, you have a right to see the breakdown of the original fine versus the collection fees.

Locating Your Case and the Assigned Collection Agency for Court Fines

Most modern court systems provide an online portal where you can search by your name, citation number, or case number. For example, if you are Struggling with Debt Collectors in Florida, you can check the Miami-Dade Clerk’s online system to see exactly which agency has your account.

If you can't find your case online, call the Clerk of the Court in the county where the fine originated. Ask for the "Collections Department." They will provide you with:

The name of the agency (e.g., Linebarger, PCR, or PayCourt).

Your unique reference number.

The total balance including the collection surcharge.

Payment Methods and Portals for Court Debt

Once your debt is with a collection agency for court fines, the court clerk will often refuse to take your money. You must pay the agency. Common portals include:

PayCourt: Often used for Virginia and regional court collections.

Pioneer Credit Recovery (PCR): A major player that handles high volumes of court debt.

GovPal: A common interface for government-related payments.

Western Union: Many agencies accept "Quick Collect" payments for those who don't have a bank account.

In Michigan, the 36th District Court allows for online payments but also encourages those with financial hardships to submit a financial statement to request an installment payment agreement.

Legal Protections and Consequences of Unpaid Court Debt

Ignoring a collection agency for court fines is significantly more dangerous than ignoring a medical bill. Because the debt is owed to the "Sovereign" (the state or county), they have unique tools to force your hand.

In Arizona, for example, the Consolidated Collections Unit uses the Debt Setoff (DSO) program. This allows the state to intercept your tax refunds, lottery winnings (over $600), and even gaming winnings to pay off your court debt.

Your Rights Under the FDCPA and State Laws

You might think that because you owe the government, you have no rights. That’s not true. What is a Debt Collector Under the FDCPA: Your Rights Explained covers third-party agencies even when they are collecting for a court.

The Fair Debt Collection Practices Act (FDCPA) prohibits:

Calling you before 8 a.m. or after 9 p.m.

Using profane or abusive language.

Threatening arrest (unless a warrant actually exists).

Lying about the amount you owe.

If you are in Michigan, you can find specific local resources through Michigan Legal Help to understand how state law further restricts what collectors can do.

Severe Penalties for Ignoring a Collection Agency for Court Fines

If you choose to stay in the "ignore it and it will go away" phase, here is what typically happens:

License Suspension: This is the most common "stick." Courts notify the DMV, and your driving privileges are revoked until a "clearance" or "D-6" form is issued.

Registration Stoppers: You won't be able to renew your car's tags.

Tax Intercepts: Your state tax refund disappears before it ever hits your mailbox.

Bench Warrants: In some criminal or "show cause" cases, a judge may issue a warrant for your arrest for "Failure to Pay."

Credit Damage: Agencies like PCR report delinquent debt over $25 to the major credit bureaus, which can tank your score for seven years.

Conclusion

Dealing with a collection agency for court fines is a high-stakes game. Between the 30% surcharges and the threat of losing your driver's license, the "wait and see" approach is a recipe for financial disaster.

At KillDebt, we believe that everyone deserves a fair shake, even when the opponent is the government. Our DIY legal defense system, powered by ParkerGPT, was built on over 30 years of legal expertise from attorney Brian Parker. We don't just give you generic advice; we provide tools like our brand-new Court Tester—an AI courtroom simulation where you can upload your filings and practice arguing your case before an AI judge.

Whether you're looking for What to Do When Sued by a Debt Collector: Complete First Steps Guide or you need to generate a specific response to a collection notice, we have the technology to help you fight back. Don't let a simple fine turn into a lifetime of credit problems. Take control of your court debt today.

Frequently Asked Questions (FAQ)

Can I negotiate a settlement for court fines?

Generally, the "base" fine is non-negotiable because it was set by a judge or statute. However, many agencies will allow for payment plans. If you can prove financial hardship, some courts (like those in Michigan) may allow you to perform community service in lieu of certain fees, or they may waive the collection surcharge if you pay the original fine in full—though this is rare once the agency has the file.

What if I already paid the fine but got a collection notice?

This happens more often than you’d think due to "processing lag." If you paid the court right as they were transferring the file to the collection agency for court fines, the agency might not know yet. Your Move: Do not just tell them you paid. Send a copy of your court receipt or bank statement showing the cleared payment to the agency via certified mail. Ask the court clerk for a "Letter of Clearance" to prove the debt is satisfied.

Are restitution and public defender liens sent to collections?

In many jurisdictions, like Miami-Dade, restitution (money paid to a victim) and public defender liens are handled differently. These are often excluded from third-party collection agency assignments and must be paid directly to the Clerk of the Court. Always check your specific case status to see if these "exempt" debts are being tracked separately.