What to Do When a Bill Collector Is Suing Me: Your First Steps

If a bill collector is suing me — or you — the single most important thing you can do right now is respond before your court deadline. Here is what that means in plain terms:

Quick Answer: What to Do If a Bill Collector Sued You

Find your deadline. Check the summons for your response date. Most states give you 14 to 30 days from the date you were served.

Do not ignore it. Ignoring the lawsuit almost always results in a default judgment against you — even if you don't owe the debt.

File a written Answer. Deny the allegations, raise your defenses, and file before the deadline.

Challenge the collector's proof. Debt buyers often lack the documents needed to win in court.

Explore settlement. Many collectors will settle for 25 to 60 cents on the dollar once you respond.

Debt collectors file roughly 4 million lawsuits against consumers in the United States every year. About 70% of those cases end in default judgments — not because the collector proved their case, but because the consumer never responded. A default judgment hands the collector the power to garnish your wages, freeze your bank account, and place liens on your property.

That outcome is not inevitable. Responding changes everything.

Most people served with a debt lawsuit feel overwhelmed and assume they have already lost. They haven't. Debt buyers — companies that purchase old debts for as little as 2 to 8 cents on the dollar — often have thin documentation and weak cases. A written Answer forces them to prove what they claim. Many collectors settle or drop the case entirely once a consumer actually shows up to fight.

I'm Brian Parker, and for over 30 years I've fought debt collectors, debt buyers, and collection law firms in courtrooms across the country — including countless cases where a bill collector was suing me clients who felt they had no options, and we won. I founded KillDebt to give you the same tools, strategies, and courtroom-ready documents I've used to protect thousands of consumers.

Immediate Action Plan: What to Do When a Bill Collector Suing Me Serves Court Papers

When a process server knocks on your door or you receive a certified letter, panic is a natural reaction. But once the initial shock wears off, you need to transition immediately into self-defense mode. The clock starts ticking the moment those papers touch your hands.

Your first move is to verify the paperwork. A legitimate lawsuit consists of two primary documents:

The Summons: This is the official court notice notifying you that you are being sued. It contains the court's name, the case number, and the deadline to respond.

The Complaint: This document outlines the plaintiff's allegations against you—how much they claim you owe, the original creditor, and the legal basis for the lawsuit.

To protect yourself, verify the service details. Write down the exact date, time, and method by which you received the papers. This is your "service date," and it is the anchor for your response deadline. Next, verify that the lawsuit is real. You can do this by looking up the case number on your local court's online portal or calling the court clerk directly using the phone number listed on the official court website.

Understanding the court's jurisdiction is also critical. Debt collection lawsuits are typically filed in small claims, county, or district courts depending on the amount of the debt. If you are in Florida or Michigan—our primary service areas—the rules of civil procedure dictate exactly how and where you must file your response. For a detailed breakdown of your immediate next steps, review our guide on Sued for a Debt Here s Exactly What to Do in the First 7 Days.

State-by-State Deadlines for Answering a Summons

Failing to meet your state's deadline is the fastest way to lose. While some states offer generous windows, others require rapid action. Here is a breakdown of common response windows across various jurisdictions:

Michigan: You generally have 21 days to file a written Answer if you were served in person, or 28 days if you were served by mail or outside the state.

Florida: In Florida small claims court (debts up to $8,000), you typically do not have to file a written Answer immediately. Instead, you must appear at a mandatory Pretrial Conference (usually scheduled 20 to 50 days out). However, in Florida County or Circuit Court (debts over $8,000), you must file a written Answer within 20 days of service.

Kentucky: You must file a written Answer within 20 days of being served.

Georgia: You have 30 days to file your Answer. However, Georgia has a unique safety valve: if you miss the deadline, you have an additional 15 days (up to day 45) to open the default "as a matter of right" by filing your Answer and paying court costs.

Texas: In Justice Court, you have 14 days to file an Answer. In County or District Court, your Answer is due by 10:00 AM on the Monday following the expiration of 20 days from service.

Washington: You have 20 days to respond if served within the state.

To learn more about federal guidelines and consumer rights regarding lawsuits, check out the What To Do if a Debt Collector Sues You | Consumer Advice page hosted by the FTC.

What Happens If You Ignore the Lawsuit?

If you choose to ignore the court papers, the bill collector does not just go away. In fact, ignoring them is exactly what they want you to do.

When you fail to respond, the plaintiff will file a motion for a default judgment. Because you did not show up to defend yourself, the judge will take the collector's allegations as absolute truth. Once the judge signs the default judgment, the bill collector gains powerful legal tools to collect the money, including:

Wage Garnishment: The collector can order your employer to withhold a portion of your paycheck. In Michigan, wage garnishment is a common and aggressive collection tool. In Florida, head-of-family exemptions protect some wages, but you must actively claim this exemption in court to stop the garnishment.

Bank Levies: The collector can instruct your bank to freeze your accounts and turn over your balances to satisfy the debt.

Property Liens: A judgment can be recorded against your real estate, preventing you from selling or refinancing your home without paying off the debt first.

Severe Credit Damage: A court judgment will linger on your public records and severely damage your credit health for years.

To prevent this snowball effect, you must act. Learn more about the exact litigation path in our article on the Debt Collection Lawsuit Timeline What Happens Next After You re Served.

Understanding the Plaintiff: Original Creditor vs. Debt Buyer

To mount a successful defense, you must understand exactly who is suing you. There is a massive operational difference between being sued by your original creditor (like Chase, Citi, or a local hospital) and being sued by a third-party debt buyer.

Debt buyers purchase portfolios of delinquent, charged-off debts for pennies on the dollar—typically between 2 and 8 cents per dollar of debt. Industry giants like Encore Capital Group (which operates through its subsidiaries Midland Funding and Midland Credit Management) and Portfolio Recovery Associates (PRA) buy millions of accounts at a time.

Because these accounts are bought in bulk, the transactions are executed via a "data tape"—a giant digital spreadsheet containing basic details like your name, address, last four digits of the account number, and the alleged balance.

What the debt buyers don't receive are the actual contracts, signed applications, monthly statements, or customer service logs. This documentation gap is their greatest weakness and your greatest leverage. For a deep dive into how this dynamic works, read our article Who is Suing Me Original Creditor vs. Debt Buyer Explained.

How to Verify If the Bill Collector Suing Me Actually Owns the Debt

If a third-party debt buyer is suing you, they must prove they actually own your specific debt to have the legal right (standing) to sue you. To do this, they must demonstrate an unbroken chain of title from the original creditor down to them.

If your debt was sold from Citibank to Debt Buyer A, then to Debt Buyer B, and finally to the plaintiff, the plaintiff must produce a signed Bill of Sale and Assignment for every single transfer in that chain.

Furthermore, they cannot just show a generic, blanket Bill of Sale that says "Citibank sells 10,000 accounts to Debt Buyer A." They must produce the specific redacted annex or schedule that lists your individual account number and balance. Under strict evidentiary rules—such as the Business Records Exception (Rule 803(6) of the Michigan and Florida Rules of Evidence)—a debt buyer's employee cannot simply sign an affidavit claiming they know the original creditor's records are accurate. They have no personal knowledge of how the original creditor maintained those records.

In states like Georgia, landmark cases like Nyankojo v. North Star Capital Acquisition and Wirth v. CACH, LLC established that debt buyers must produce specific, account-level written assignments to prove standing. While these are Georgia cases, the same fundamental principles of standing and contract law apply in Florida and Michigan courts. If there is a single gap in their paperwork, they cannot prove they own the debt, and the case should be dismissed.

How to Draft and File Your Written Answer

Your written Answer is your formal response to the allegations made in the Complaint. It is not the place to tell your life story or explain why you fell on hard times. The court only wants to know whether you agree or disagree with the plaintiff's specific claims.

An Answer typically consists of three parts:

The Responses: You must respond to every numbered paragraph in the Complaint. You have three choices for each paragraph:

Admit: You agree the statement is completely true (use this sparingly, such as for your name and residency).

Deny: You dispute the statement. Denying forces the plaintiff to prove it.

Deny for Lack of Knowledge: You do not have enough personal information to know if the statement is true (highly useful for allegations regarding how the debt was bought or calculated).

Affirmative Defenses: These are legal reasons why the plaintiff should not win, even if the factual allegations are true (e.g., the statute of limitations has expired).

Certificate of Service: A signed statement certifying that you have sent a copy of your Answer to the plaintiff's attorney.

Once completed, you must file the original Answer with the court clerk and mail a copy to the plaintiff's attorney via Certified Mail with a return receipt requested. This ensures you have irrefutable proof of timely filing. For step-by-step guidance on drafting this document, read our comprehensive guide on How to Answer a Debt Summons.

Common Defenses to Defeat a Bill Collector Suing Me in Court

When drafting your Answer, you must raise your "affirmative defenses." If you do not raise them in your initial Answer, you may waive your right to use them later. Here are the most powerful defenses to consider:

Statute of Limitations: This is the legal time limit a creditor has to sue you. In Florida, the statute of limitations for credit card debt and open accounts is 4 years (5 years for written contracts). In Michigan, the statute of limitations is 6 years. If the collector sues you after this window has closed, the debt is "time-barred," and the court must dismiss the case.

Lack of Standing / Chain of Title Gaps: As discussed, if the plaintiff is a debt buyer and cannot produce the unbroken chain of assignments proving they own your specific account, they have no right to sue you.

The Borrowing Statute Defense: Some states have "borrowing statutes" that apply the statute of limitations of the state where the contract was executed or where the creditor is located. For example, under Kentucky's borrowing statute (KRS 413.320), if a Delaware-based bank (like Chase or Discover) issues a card, Delaware's shorter 3-year statute of limitations might apply instead of Kentucky's 5-year limit.

FDCPA Violations: If the debt collector violated the Fair Debt Collection Practices Act (FDCPA)—by harassing you, misrepresenting the debt, or threatening actions they cannot legally take—you can raise these violations as counterclaims.

To explore these strategies in depth, read our Fight Debt Collection Lawsuit Complete Guide.

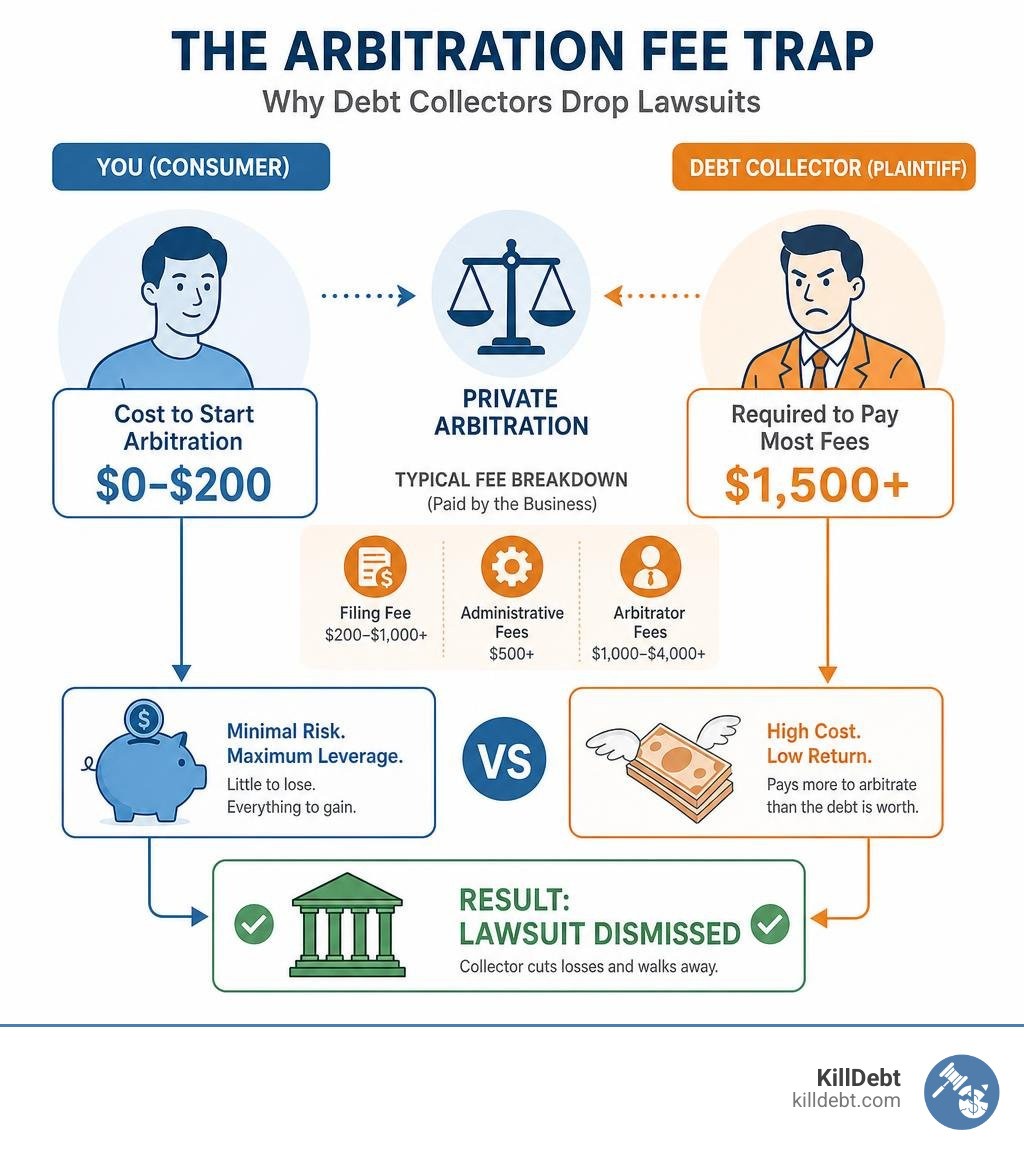

Using Private Arbitration as a Defense Strategy

One of the most powerful, underutilized weapons in consumer defense is the private arbitration clause found in almost every major credit card agreement.

These clauses state that either party can elect to resolve any dispute through private, binding arbitration (usually via AAA or JAMS) instead of court. If you file a Motion to Compel Arbitration alongside your Answer, the court must stay (pause) the lawsuit while the parties arbitrate.

This creates what consumer attorneys call the Arbitration Fee Trap. While it costs you very little to initiate consumer arbitration, the rules of AAA and JAMS require the business to pay the lion's share of the filing, administrative, and arbitrator fees—often ranging from $1,500 to over $5,000.

If the debt collector is suing you for a $2,000 credit card balance, it makes zero financial sense for them to pay $3,000 in arbitration fees to chase it. In the majority of cases, once faced with a properly drafted Motion to Compel Arbitration, debt buyers will simply dismiss the lawsuit.

Warning: You must file your motion to compel arbitration early. In Georgia, the Tillman Group v. Keith precedent established that actively litigating the merits of the case in court before moving to compel arbitration waives your right to arbitrate.

The Discovery Phase and Settlement Negotiations

If the case proceeds past the initial Answer, it enters the Discovery Phase. This is the formal process where both sides exchange evidence. You have the right to send discovery requests to the debt collector, including:

Requests for Production: Demanding the original contract, complete monthly statements, and the specific bill of sale.

Interrogatories: Written questions they must answer under oath.

Requests for Admissions: Statements they must admit or deny.

If a debt buyer cannot produce these documents during discovery, their case falls apart, giving you immense leverage to settle or win a dismissal.

Strategy Option | Pros | Cons |

|---|---|---|

Litigation / Full Defense | • Can result in complete dismissal | • Requires court appearances |

Debt Settlement | • Guarantees resolution | • Requires lump-sum cash or payment plan |

If you choose to negotiate, aim to settle for 25% to 50% of the alleged balance if dealing with a debt buyer. Never agree to a settlement over the phone without receiving a written, signed settlement agreement first. Ensure the agreement includes a "pay-for-delete" clause, requiring them to completely remove the collection tradeline from your credit reports. For more details on managing this phase, review our Debt Lawsuit Defense Guide.

Conclusion

Facing a debt collection lawsuit is stressful, but you do not have to navigate it alone or spend thousands of dollars on a private defense attorney. The system is designed to favor those who show up and fight. By understanding your rights, meeting your deadlines, and challenging the collector's evidence, you can take control of your financial future.

At KillDebt, we provide a DIY legal defense system powered by ParkerGPT—an advanced AI trained specifically on consumer debt law and the real-world court strategies developed over my 30+ years as a consumer defense attorney. Unlike generic AI tools, ParkerGPT analyzes your actual lawsuit documents, uncovers critical procedural weaknesses, and generates customized, court-ready Answers and Motions to Compel Arbitration.

We've also just rolled out our brand-new Court Tester tool! Court Tester is an advanced AI courtroom simulation built directly on the facts of your actual case. You can upload your real court filings, and within minutes, you'll practice arguing your motions in front of an AI judge, facing off against AI opposing counsel, while a private AI co-counsel whispers winning strategies only you can see.

Don't let a default judgment ruin your credit and drain your bank account. Take action, protect your hard-earned wages, and fight back today. Get started with KillDebt's AI defense tools and let us help you defeat the bill collectors once and for all.

Get started with KillDebt pricing

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

About Brian Parker

I have over 30 years of experience defending consumers against debt collection lawsuits and have seen every tactic, threat, and pressure play that collectors use. Through KillDebt and ParkerGPT, I have systematized the proven defense strategies that actually work - so consumers can respond from a position of knowledge, not fear. My approach focuses on aggressive legal defense based on documented case success rather than false hope that leads to default judgments.

Frequently Asked Questions (FAQ)

Can a debt collector garnish my wages or levy my bank account without suing me first?

No. Except for specific federal debts (like federal student loans or back taxes), a standard debt collector or debt buyer has absolutely no authority to garnish your wages or touch your bank account without first suing you, winning the lawsuit, and obtaining a formal court judgment. Only after a judgment is entered can they apply for a writ of garnishment or bank levy. Certain income, such as Social Security benefits, veterans' benefits, and disability payments, is completely exempt from garnishment under federal law. For more details, consult the Debt Collection FAQs - FTC Consumer Advice resource.

How does the statute of limitations work, and can it be restarted?

The statute of limitations is the legal deadline for a creditor to file a lawsuit. The clock typically starts on the date of your last payment or the date the account went into default. However, be incredibly careful: in many states, making a partial payment, agreeing to a payment plan, or even formally acknowledging in writing that you owe the debt can restart the statute of limitations clock from zero. If a collector contacts you about an old, time-barred debt, do not make a "good faith" payment until you have verified the debt's legal status.

Where can I get free or low-cost legal help if I am sued?

If you cannot afford a private consumer defense attorney, you still have options. You can reach out to local legal aid organizations in your county. Residents of Michigan can access invaluable self-help resources, forms, and legal aid directories through How to Deal with Debt Collectors - Michigan Legal Help . Additionally, many consumer protection attorneys work on a contingency fee basis if there are clear FDCPA violations, meaning they only get paid if they win damages from the collector.