When Debt Feels Overwhelming, You Have More Power Than You Think

If you want to know how negotiate lower payments on your debt, here's the short answer:

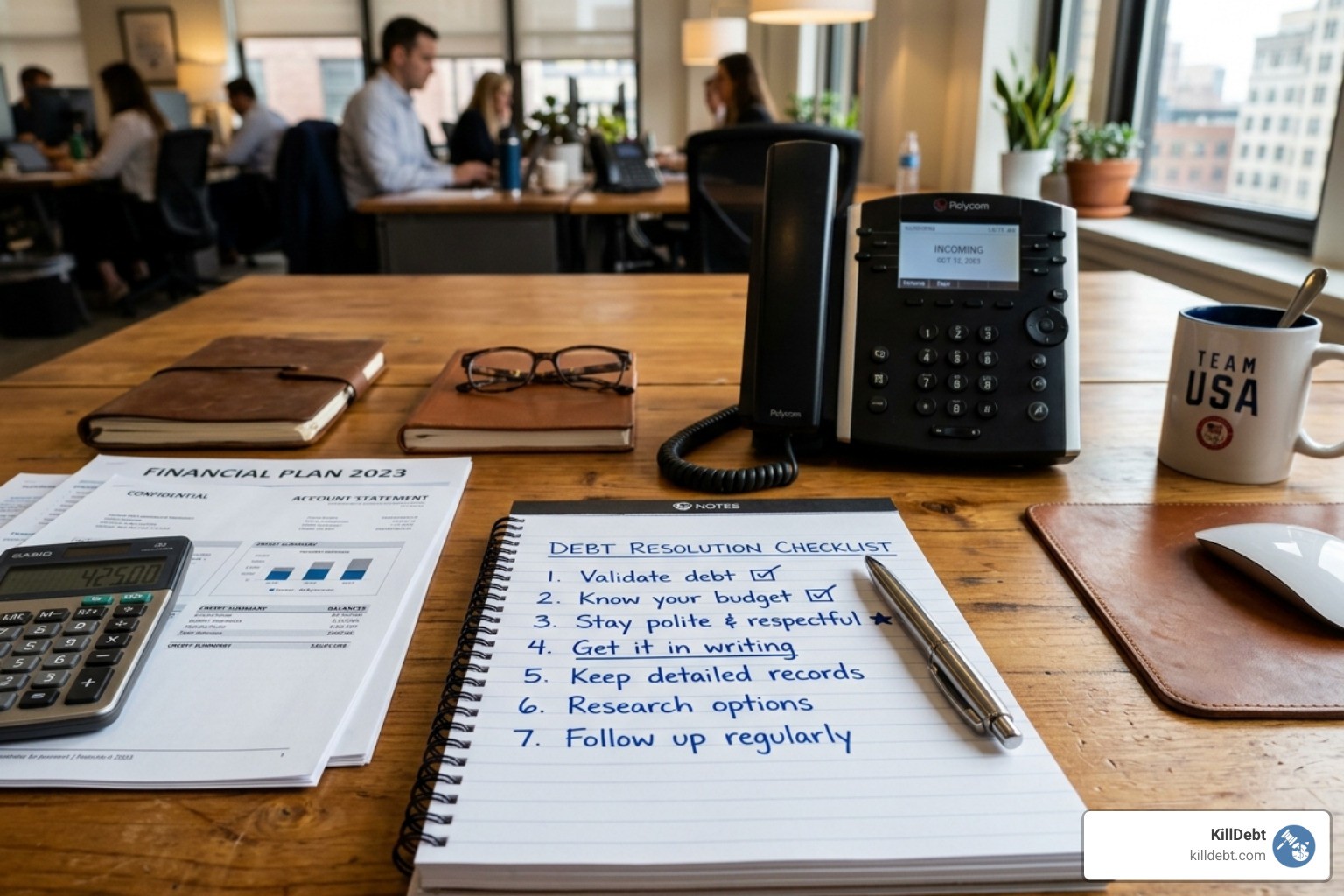

Validate the debt - Confirm you actually owe it and the amount is correct

Build a budget - Know exactly what you can afford to pay each month

Contact your creditor - Call and explain your financial hardship honestly

Make a specific offer - Propose a payment plan or lump-sum settlement

Get it in writing - Never pay a single dollar before you have a written agreement

That's the core process. But the details matter a lot — and knowing them can save you thousands.

American households are carrying a crushing load right now. In 2024, U.S. households held over $1.2 trillion in credit card debt. The average interest rate on accounts that actually charge interest hit 22.25% as of May 2025. That means for millions of people, most of their monthly payment is just feeding interest — not reducing what they owe.

It feels like a trap. And for a lot of people, it is.

But here's what most people don't realize: creditors would rather get something than nothing. That gives you real negotiating power — even if you've already missed payments, even if your debt is in collections, and even if you've received a lawsuit summons.

You don't have to accept the terms you were given. You can ask for better ones.

This guide will show you exactly how — step by step, without expensive attorneys or shady debt settlement companies.

Preparation: The Foundation of How to Negotiate Lower Payments

Before you pick up the phone, you need to be armed with facts. If you go into a negotiation without a plan, the creditor's representative—who is trained to get as much money out of you as possible—will likely steer the conversation in their favor. Preparation is 90% of the battle when learning how negotiate lower payments.

We recommend starting with a cold, hard look at your finances. This isn't just about knowing what you owe; it's about knowing what you can actually afford to give up. If you promise a payment that breaks your budget, you'll be right back in this situation in three months, but with less credibility.

Confirming and Validating Your Debt

One of the biggest mistakes people make is acknowledging a debt before they've verified it's actually theirs. Under the Fair Debt Collection Practices Act (FDCPA), debt collectors are required to provide you with "validation information" within five days of their first contact. This must include the amount of the debt, the name of the creditor, and instructions on how to dispute it.

If you aren't sure about a debt, don't pay a dime. Instead, send a Debt Validation Letter: Your First Line of Defense Against Collectors. This forces the collector to prove they have the legal right to collect from you. In many cases, especially with "junk debt buyers," they may not have the original paperwork, which gives you massive leverage.

Also, keep an eye on the statute of limitations. In states like Michigan and Florida, creditors only have a certain number of years to sue you for a debt. If the debt is "time-barred," they can still ask for money, but they can't successfully sue you for it. Be careful: in some jurisdictions, making even a small $5 payment can "reset" that clock, giving them another several years to take you to court. For more on handling these initial contacts, check out our guide on Struggling with Debt Collectors.

Assessing Affordability for Lower Payments

Once you've confirmed the debt is valid, it’s time to look at your "take-home" pay versus your "must-have" expenses (rent, food, utilities). Whatever is left over is your "negotiation bucket."

You have two main paths:

Lump-Sum Settlement: You offer a one-time payment (usually 30% to 60% of the total) to wipe the slate clean. This is often the cheapest way to resolve debt if you have the cash.

Installment Plan: You negotiate a lower monthly payment or a lower interest rate to make the debt manageable over time.

When calculating your offer, always leave an emergency buffer. Do not offer every spare cent you have. If your car breaks down next month and you can't make your negotiated payment, the deal might be canceled. We suggest gathering proof of financial hardship—like medical bills, layoff notices, or bank statements—to show the creditor that your offer isn't just a "want," but a "need."

Strategic Tactics for Different Debt Types

Not all debts are created equal. The strategy for a credit card company is different from the strategy for a utility company or a mortgage lender.

Strategy | Interest Rate Reduction | Debt Settlement |

|---|---|---|

Best For | Current accounts/High APR | Defaulted accounts/Collections |

Credit Impact | Minimal/Positive | Moderate/Negative (7 years) |

Goal | Lower monthly cost | Pay less than total owed |

Tax Risk | None | Possible (1099-C) |

How to Negotiate Lower Payments on Credit Cards

If you are still current on your payments but the 22% interest rate is drowning you, call the number on the back of your card. Use your loyalty as leverage. If you’ve been a customer for five years and have a history of on-time payments, mention it.

Tell them: "I’ve been a loyal customer, but my current APR makes it hard to keep up. I’ve seen offers from competitors for much lower rates. What can you do to help me stay with you?"

If they say no, ask about hardship programs. Most major issuers (like Chase, Amex, or Capital One) have internal programs that can temporarily lower your interest rate or minimum payment for 6 to 12 months while you get back on your feet.

Negotiating with Original Creditors vs. Debt Collectors

There is a huge difference between negotiating with the bank that gave you the card and a collection agency that bought the debt for pennies on the dollar.

Original Creditors: They want to keep you as a customer but are also worried about a "charge-off" (where they write the debt off as a loss). They are often more willing to offer interest rate reductions or workout plans.

Debt Collectors: These companies bought your debt for maybe 5 to 10 cents for every dollar you owe. Because their "buy-in" is so low, they have much more room to settle. If you owe $5,000, they might have only paid $500 for it. Offering them $2,500 represents a massive profit for them, even though it's a 50% discount for you.

To understand how these settlements work in your favor, read more about Erasing Debt Worries: How Debt Settlement Can Work for You.

Mastering the Negotiation Call

Negotiating over the phone can be intimidating, but remember: the person on the other end is just an employee with a script. They have "settlement floors"—minimum amounts they are authorized to accept. Your goal is to find that floor.

Effective Communication and How to Negotiate Lower Payments

When you call, keep your tone polite but firm. Being rude will only make the representative less likely to go the extra mile for you.

Be Honest but Brief: Explain your hardship (job loss, illness, etc.) without giving your whole life story.

Use Specific Numbers: Don't say "I want a lower payment." Say "I can afford $150 a month, and not a penny more."

Set Expiration Dates: If you're offering a lump sum, tell them the offer is only good for 48 or 72 hours. This creates a sense of urgency.

Escalate if Necessary: If the first person says "I can't do that," politely ask to speak with a supervisor or the "settlement department." The front-line customer service reps often don't have the authority to grant deep discounts.

Getting the Agreement in Writing

This is the most critical step. Never, ever pay a debt settlement based on a verbal promise. We have seen countless cases where a consumer pays a "settlement," only for the creditor to claim it was just a partial payment and continue hounding them for the rest.

A valid written agreement must include:

The exact amount to be paid.

The date the payment is due.

A statement that the debt will be considered "paid in full" or "settled in full."

A promise to stop all collection activity and update the credit bureaus.

Keep copies of this letter and your proof of payment (like a bank statement or a copy of the check) forever. Seriously—forever. Debt has a way of being resold even after it's paid, and you'll need that "receipt" to kill the ghost debt later.

Understanding the Risks and Long-Term Impacts

While knowing how negotiate lower payments can save your budget, it isn't without side effects. You need to go in with your eyes open.

Potential Risks of Successful Negotiations

The biggest "hidden" cost of debt settlement is the tax man. If a creditor forgives more than $600 of debt, the IRS considers that forgiven amount as taxable income. You will likely receive a 1099-C form at the end of the year. For example, if you settle a $10,000 debt for $4,000, the $6,000 "discount" is treated as if you earned $6,000 in wages. You'll owe taxes on it unless you can prove you were "insolvent" (your debts exceeded your assets) at the time.

Another risk is account closure. Most creditors will close your account once you enter a hardship program or settle the debt. This can hurt your credit score in two ways: it reduces your total available credit (increasing your utilization ratio) and it shortens your average age of accounts.

Finally, there's the risk of aggressive collections. If you stop making payments to save up for a lump-sum settlement, the creditor might decide to sue you instead of negotiating. This is why know your rights regarding Can Debt Collectors Take My Wages and Bank Account. In Florida and Michigan, there are specific exemptions that protect some of your income, but a judgment still makes life very difficult.

When to Seek Professional Help

DIY negotiation is powerful, but it has limits. If you are being sued—meaning you've received a formal summons and complaint from a court—the clock is ticking. You usually have only 20 to 30 days to respond.

Many people fall for Debt Collection Lawsuit Myths: 7 Things That Won't Save You, like thinking that if they ignore the lawsuit, it will go away. It won't. It will result in a "default judgment," which allows the collector to garnish your wages or freeze your bank account.

If you're at this stage, you don't necessarily need a $300-an-hour attorney, but you do need a professional strategy. This is where legal tech can bridge the gap, helping you file the right papers to keep the collector from getting an easy win.

Conclusion: Take Control of Your Financial Future

Learning how negotiate lower payments is a skill that pays dividends for a lifetime. Whether you are dealing with a credit card company, a medical bill, or a persistent debt collector, the principles remain the same: validate the debt, know your numbers, stay professional, and get everything in writing.

At KillDebt, we believe that everyone deserves a fair fight. You shouldn't be bullied into a financial corner just because you don't have a law degree. That's why we created ParkerGPT, our DIY legal defense system. Trained on the real-world strategies of attorney Brian Parker—who has over 30 years of experience fighting for consumers in Michigan and Florida—ParkerGPT helps you analyze lawsuit documents and generate court-ready responses.

And if you're nervous about how you'll perform in a negotiation or a hearing, our brand-new Court Tester allows you to practice in an AI-powered courtroom simulation. You can argue your motion in front of an AI judge and face off against AI opposing counsel before you ever step foot in a real courthouse.

You have the power to settle your debts and move on with your life. Don't let the collectors have the last word.

Frequently Asked Questions (FAQ)

What percentage should I offer for a lump-sum settlement?

A good starting point is 50% of the balance. However, if you are dealing with a junk debt buyer (a company that bought your old debt from a bank), you can often start as low as 30%. Original creditors are usually firmer, typically settling in the 60% to 80% range. Always start lower than what you can actually afford so you have room to "negotiate up" to your real limit.

Will negotiating lower payments hurt my credit score?

If you negotiate a lower interest rate while staying current, the impact is minimal. However, if you settle for less than the full balance, it will be reported to credit bureaus as "Settled" or "Account paid for less than full balance." This is a negative mark that stays on your report for seven years. That said, a "settled" account is much better for your score than an "unpaid collection" or a "judgment," and it allows you to start rebuilding your credit much sooner.

What if the creditor sues me during negotiation?

Don't panic, but don't wait. A lawsuit is just a more formal stage of negotiation. You can still settle a debt even after a lawsuit has been filed. In fact, filing a strong "Answer" to the lawsuit often makes the collector more willing to settle because they realize you aren't going to be an easy target. For a step-by-step on this, see our What to Do When Sued by a Debt Collector: Complete First Steps Guide and our overview of what happens when Have You Been Sued by a Debt Collector.