What It Really Means to Defend Against Credit Card Debt Collection

Knowing how to defend credit card debt collection lawsuits can mean the difference between losing your wages to garnishment and walking away with the case dismissed — or settled for a fraction of what they're demanding.

Here's how to defend yourself against credit card debt collection, fast:

File a written Answer with the court before your deadline (usually 14–35 days from being served)

Deny allegations you cannot verify — do not admit anything unless you are certain it is true

Raise affirmative defenses in your Answer (statute of limitations, lack of standing, wrong amount, identity theft)

Demand proof — send a debt validation letter and use discovery to force the collector to produce documentation

Check for FDCPA violations — illegal collector conduct can give you counterclaim leverage

Negotiate a written settlement if the evidence is strong against you — debt buyers often accept 30–50 cents on the dollar

If you just received a summons, here is what you need to understand right now:

Debt buyers — companies like Midland Funding, Portfolio Recovery Associates, and LVNV Funding — purchase old credit card accounts for as little as 2 to 8 cents on the dollar. They then sue consumers to collect the full balance, often with incomplete records and thin documentation. The CFPB logged over 150,000 debt collection complaints in 2025, and a significant portion involved debts consumers did not actually owe.

The system is designed to win by default. Most consumers do nothing, miss the deadline, and lose automatically — no evidence required. That is exactly what debt buyers count on.

But if you respond? The whole game changes.

Responding forces the collector to actually prove their case — that they own the debt, that the amount is correct, and that they have the legal right to sue you. Many cannot. Cases collapse during discovery. Settlements drop dramatically. Some get dismissed entirely.

You have more power here than you think. But only if you act.

I'm Brian Parker, and for over 30 years I've been in the courtroom defending consumers against creditors, debt buyers, and collection law firms — I've seen every documentation trick and legal shortcut they use. I built KillDebt specifically to teach people how to defend credit card debt collection lawsuits using the same strategies I've used to protect thousands of clients. Let's walk through exactly what to do.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

What to Do in the First 7 Days After Being Served

Opening your door to find a process server handing you a summons and complaint is a gut-wrenching experience. It is easy to freeze up, but time is your most valuable resource right now. The countdown begins the exact day you are served, not the date printed on the court documents.

Depending on your location, your response window is incredibly tight:

In Florida: You have exactly 20 calendar days to file a written response.

In Michigan: You have 21 days if you were personally handed the papers, or 28 days if you were served by mail or are outside the state.

If you miss this window, the plaintiff (the debt collector suing you) will file for a default judgment. A default judgment is an automatic win for the collector. Once they have a judgment, they can legally freeze your bank accounts, garnish up to 25% of your disposable income, and place liens on your property.

To prevent this, you must act decisively. Here is your immediate 7-day action plan:

Verify the Deadline: Mark the exact calendar date your Answer is due. Do not guess; count the days from the date of service.

Review the Summons and Complaint: Identify who is suing you. Is it your original credit card company (like Capital One or Chase) or a debt buyer (like Midland Credit Management or Portfolio Recovery Associates)?

Pull Your Credit Reports: Go to AnnualCreditReport.com and pull your reports. Look for the original account, when it was charged off, and the date of your last payment.

Read Every Paragraph: The complaint will contain numbered paragraphs. You will need to respond to each one.

Get Professional Guidance: If you want a step-by-step roadmap tailored to your situation, check out our guide on Sued for a Debt? Here's Exactly What to Do in the First 7 Days to ensure you do not miss a single critical step.

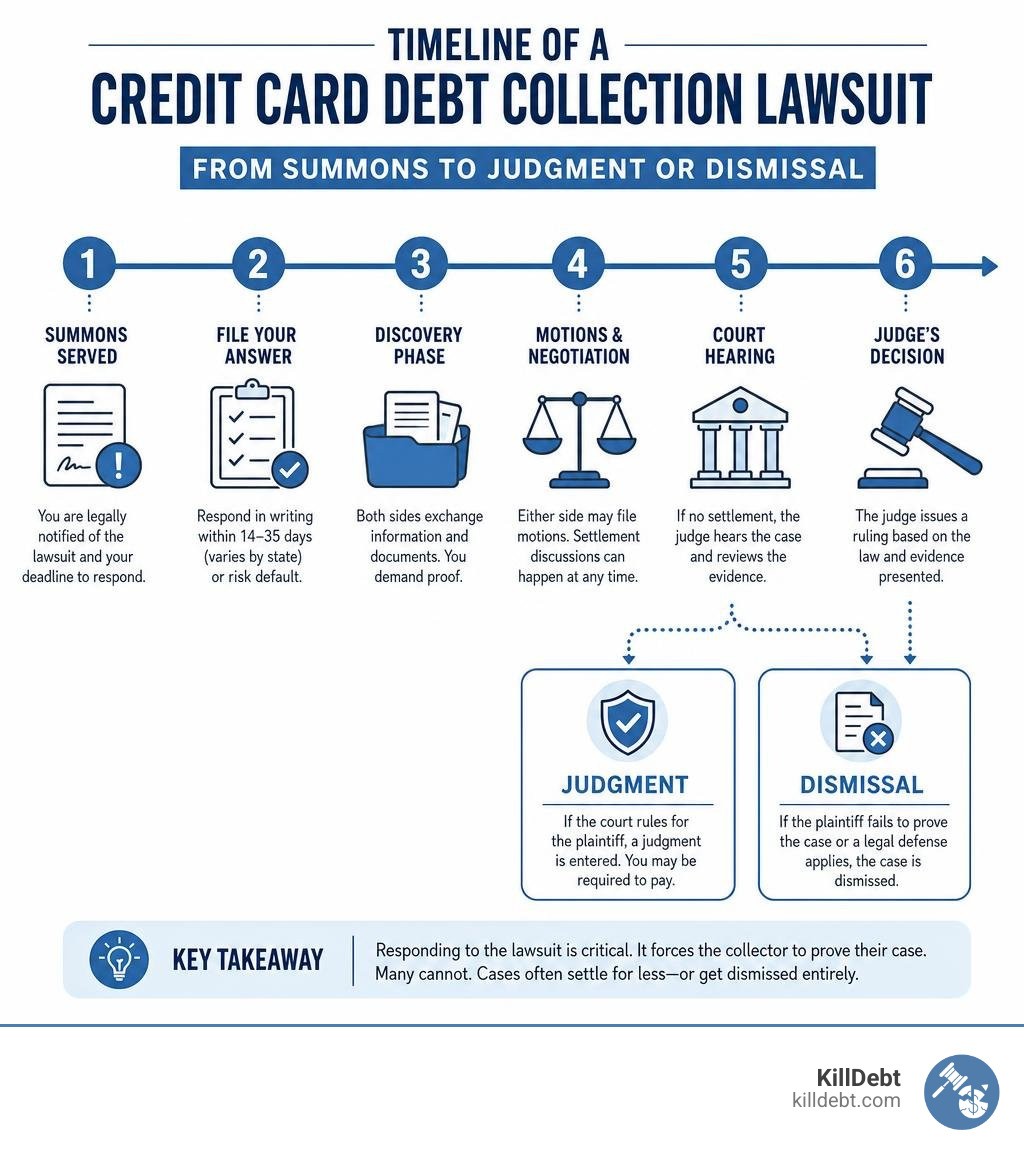

How to Defend Credit Card Debt Collection in Court

Defending yourself in court does not require a law degree, but it does require following the rules. Your first formal step is drafting and filing an Answer. An Answer is a written document where you respond to each allegation in the plaintiff’s complaint.

For every numbered paragraph in the complaint, you must choose one of three responses:

Admit: You agree the statement is 100% true. (Warning: Only admit things you are absolutely certain of, like your name. Never admit to the debt amount or the collector's ownership of the debt unless you have verified proof).

Deny: You dispute the statement. In debt buyer lawsuits, you should deny their claim that they own the debt and that you owe the specific amount. Denying forces them to bring actual proof to court.

Lack of Knowledge: You do not have enough information to know if the statement is true. This is highly effective when a debt buyer references complex corporate transactions or account transfers that you were not a party to.

For a deeper dive into the mechanics of this document, read our tutorials on How to Answer a Debt Summons and How to Write an Answer to a Credit Card Lawsuit.

State-Specific Defense Rules

In Michigan, if you are sued on an "open account" or "account stated," the plaintiff might attach an affidavit of account. Under Michigan law, if you want to deny this effectively, you must file a notarized Defendant's Counter Affidavit alongside your Answer. Failing to do so can allow the court to take the plaintiff's affidavit as absolute truth. For detailed state guidance, consult Going to Court to Defend a Debt Collection Case.

In Florida, small claims courts (which handle cases up to $8,000) operate under a "pre-trial conference" system. When you are served in Florida, you are often given a date to appear for a pre-trial conference. You must show up to this conference or your Answer will not save you from a default. If you are facing a lawsuit in the Sunshine State, we recommend reviewing Debt Collection Lawsuits: How to Fight Back and Win in Florida and keeping up with resources from How to Protect Yourself: Debt Collections | My Florida Legal .

How to Defend Credit Card Debt Collection Using the Statute of Limitations

The statute of limitations is the legal time limit a creditor has to file a lawsuit against you. Once this period expires, the debt becomes "time-barred." While you still technically owe the money, the collector loses the legal right to sue you to collect it.

The statute of limitations clock is measured from the date of first default (usually 30 days after your last payment).

State | Credit Card / Open Account | Written Contract |

|---|---|---|

Florida | 4 Years | 5 Years |

Michigan | 6 Years | 6 Years |

Warning: Making even a tiny partial payment or signing a written agreement to pay after default can completely restart the statute of limitations clock in both Florida and Michigan. Never pay a dime on an old, expired debt until you have evaluated your legal options.

If the debt is past these time limits, you must explicitly raise the Statute of Limitations as an affirmative defense in your Answer. If you do not raise it, the judge cannot apply it, and you can still lose the case.

How to Defend Credit Card Debt Collection by Challenging Standing

"Standing" is the legal right to bring a lawsuit. When an original creditor (like Citibank) sells your debt to a debt buyer, the debt buyer must prove they actually own your specific account.

Debt buyers usually purchase accounts in massive portfolios containing thousands of charged-off credit card accounts. They receive a bulk "Bill of Sale" and a digital spreadsheet (a data tape). When they sue you, they often provide a generic Bill of Sale that says they bought "a portfolio of accounts" but fails to mention your name or account number.

You can challenge their standing by pointing out these documentation gaps:

They lack a complete, unbroken chain of title showing every transfer of the account from the original creditor to the current plaintiff.

They cannot produce the original credit agreement signed by you.

Their affidavits are signed by "robo-signers" who have no personal knowledge of your original account records.

Demanding Proof: The Power of Debt Validation and Discovery

If you are within the initial collection phase (before a lawsuit is filed), you have the right under the Fair Debt Collection Practices Act (FDCPA) to demand debt validation. You must send this request in writing within 30 days of their first contact. Use our Debt Validation Letter Template to draft a formal demand.

Once a lawsuit is filed, the validation letter is no longer enough—you must use court-ordered discovery to force the debt collector to show their cards. Discovery is a formal legal process where both parties must exchange evidence.

As a self-represented defendant, you can send the plaintiff two powerful discovery tools:

Interrogatories: Written questions they must answer under oath (e.g., "State the name of every corporation that owned this account before you").

Requests for Production: Demands for physical documents (e.g., "Produce the original signed credit card agreement and the complete itemized transaction history from the date of opening to charge-off").

Because debt buyers purchase these accounts for pennies on the dollar, they rarely have the actual documentation. When forced to comply with discovery, many debt buyers choose to dismiss the case rather than spend the time and money tracking down original bank records.

Turning the Tables: FDCPA Violations and Counterclaims

The Fair Debt Collection Practices Act (FDCPA) protects you from predatory collection behavior. If a debt collector violates the FDCPA, you do not just have a defense—you have a counterclaim that can force them to pay you.

Common FDCPA violations include:

Threatening arrest, jail time, or wage garnishment without a court judgment.

Calling you before 8:00 AM or after 9:00 PM.

Continuing to call you at work after you told them your employer prohibits it.

Misrepresenting the amount you owe or adding unauthorized interest and fees.

Contacting third parties (like neighbors or family members) and revealing that you owe money.

Under the FDCPA, you can recover up to $1,000 in statutory damages, plus any actual damages (such as emotional distress) and your attorney's fees. To understand how these rules apply, explore our guide on FDCPA Explained.

Negotiating a Settlement Without an Expensive Attorney

If the collector actually has the documentation to prove their case and the statute of limitations has not expired, fighting to a trial might be risky. In this scenario, negotiating a settlement is often the cheapest and most predictable path.

Debt buyers are highly motivated to settle. Since they bought your debt for 2 to 8 cents on the dollar, a settlement of 30% to 50% of the balance is still highly profitable for them.

Follow these rules for successful negotiation:

Never Settle Verbally: A collector's verbal promise is worth nothing. Never pay a single dollar until you have a signed settlement agreement in your hands.

Get the Right Terms: Ensure the agreement states the payment "fully satisfies the debt" and that the lawsuit will be dismissed with prejudice (meaning they can never sue you for this debt again).

Pay Wisely: Never give a debt collector direct access to your bank account or send a personal check. Pay via cashier's check or money order.

Demand Credit Reporting Cleanup: Ask for a "pay-for-delete" agreement where they agree to completely remove the collection tradeline from your credit report.

For a comprehensive blueprint on how to structure these conversations, read How to Negotiate With Debt Collectors: A 2026 Guide - Firstcard .

Conclusion

Defending yourself against credit card debt collection does not require a massive legal budget. It requires action, organization, and the right tools. By filing your Answer on time, demanding proof of ownership, and raising legitimate legal defenses, you can disrupt the debt buyer's automated business model and force them to the negotiating table—or out of court entirely.

At KillDebt, we developed a DIY legal defense system powered by ParkerGPT—an AI trained specifically on consumer debt law and real-world court strategies designed by attorney Brian Parker over his 30+ year career. Unlike generic AI tools, ParkerGPT analyzes your actual lawsuit documents, uncovers critical chain-of-title weaknesses, and generates court-ready Answers and discovery requests customized for Florida and Michigan jurisdictions.

We also introduced Court Tester, an AI courtroom simulation built directly on your actual case. By uploading your real filings, you can practice arguing your motion in front of an AI judge, face off against AI opposing counsel, and receive real-time strategy tips from a private AI co-counsel. Combined with our Case Searcher tool, KillDebt gives you everything you need to fight back and win at a fraction of the cost of a traditional law firm.

Ready to take control of your case? Explore KillDebt DIY Legal Defense today.

IMPORTANT LEGAL DISCLAIMER

This educational content is based on general legal principles and my experience in debt collection defense. It is provided for informational purposes only and does not constitute legal advice. Laws vary by state and by local court. For specific legal advice, consult a qualified attorney licensed in your jurisdiction. No attorney-client relationship is created by reading this guide.

Critical Multi-State Variations: FDCPA applies uniformly at the federal level, but state consumer protection laws may provide additional rights and remedies. Statute of limitations periods vary significantly by state and debt type. What constitutes sufficient debt validation varies in practice across jurisdictions. State-specific rules on call frequency, written notice requirements, and permissible collector conduct may differ from federal minimums.

Frequently Asked Questions (FAQ)

What happens if I miss the deadline to file an Answer?

If you miss the deadline, the plaintiff will file for a default judgment. Once entered, the collector can garnish your wages, freeze your bank accounts, and place liens on your property. If you have already missed the deadline, you must act immediately to file a Motion to Vacate Default Judgment. You will need to show the court a valid reason why you missed the deadline (such as improper service) and that you have a meritorious defense to the lawsuit.

What is the difference between being sued by an original creditor versus a debt buyer?

An original creditor (like Capital One) has direct access to all your original statements, signed applications, and payment histories. They are harder to beat on documentation grounds. A debt buyer (like Midland Credit Management) purchased the account in bulk and rarely has the original records. Debt buyers are much easier to defeat by challenging standing and demanding chain of title documentation.

Can I defend myself in court without hiring a lawyer?

Yes, you can represent yourself pro se (as a self-represented litigant). While the legal system can feel intimidating, local courts in Florida and Michigan offer self-help resources. Furthermore, modern legal technology has democratized the process, allowing you to access institutional-grade legal defense strategies without paying thousands of dollars in attorney hourly fees.